Will the Federal Reserve take this as a signal to begin slowing interest rate increases?

By David Enna, Tipswatch.com

The stock and bond markets finally got a positive surprise today with the release of the October inflation report, with monthly and annual numbers coming in well below expectations.

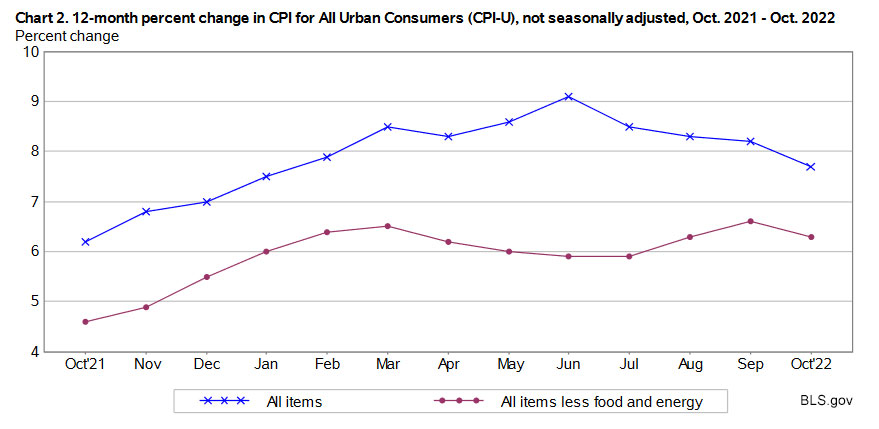

The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.4% in October on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported. Over the last 12 months, the all-items index increased 7.7%. Core inflation, which removes food and energy, rose 0.3% for the month and 6.3% year over year. All of these numbers were below expectations, as shown in the chart.

The BLS noted that the 7.7% increase in all-items inflation was the smallest 12-month increase since the period ending January 2022. This was the second month in a row that U.S. inflation ran at 0.4%, which sets an annual pace of 4.8%, well below the 2022 high of 9.1% set in June. Realistically, even 4.8% remains unacceptably high, but inflation watchers can take some comfort that the U.S. inflation appears to be trending down.

The October “cool-down” came despite a 4.0% monthly increase in the price of gasoline, breaking three consecutive months of steep declines. Gasoline prices remain 17.5% higher year over year. Also, shelter costs rose 0.8% and are now up 6.9% year over year. The BLS said shelter costs accounted for more than half of the increase in October inflation. The shelter increase was the highest for the category since August 1990. More from the report:

- The costs of food at home increased 0.4% for the month, down a bit from recent trends and the smallest monthly increase since December 2021. But food at home prices are still up 12.4% year over year.

- The index for meats, poultry, fish, and eggs rose 0.6% over the month. In contrast, the index for fruits and vegetables fell 0.9% in October.

- The rent index rose 0.7% over the month.

- The costs of medical care services fell 0.6% in October and were up 5.4% year over year.

- Apparel costs also fell, down 0.7% for the month.

- The costs of used cars and trucks fell 2.4% for the month and are up only 2% over the last year, following a strong surge higher in 2021. The costs of new vehicles were up 0.4% for the month and 8.4% year over year.

- The index for airline fares fell 1.1% in October.

The BLS noted that the October report was a “mix of increases and declines,” and the overall result was an inflation rate below economist expectations. Here is the 12-month trend in all-items and core inflation, clearly showing the gradual trend downward in all-items inflation since early summer.

What this means for TIPS and I Bonds

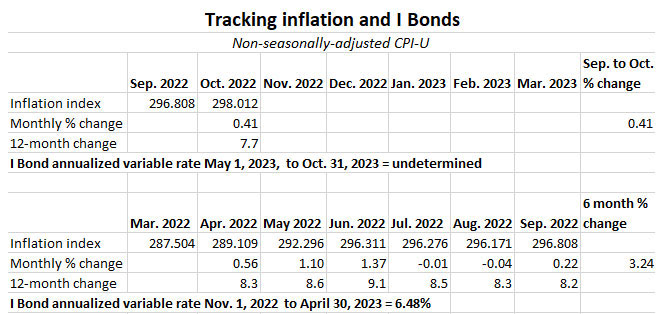

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For October, the BLS set the inflation index at 298.012, an increase of 0.41% over the September number. The annual increase was 7.7%.

For TIPS. The October inflation number means that principal balances for all TIPS will increase 0.41% in December, after a 0.22% increase in November. For the year ending in December, TIPS principal balances will have increased 7.7%. Here are the new December Inflation Indexes for all TIPS.

For I Bonds. The October report is the first in a series of six — from October to March — that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset May 1. So far, that increase is 0.41%, but just one month of data is meaningless. Here are the numbers:

What this means for future interest rates

Clearly, the softening of the inflation trend in October could give the Federal Reserve reason to opt for a 50-basis-point increase in the federal funds rate in December, instead of 75 basis points. In fact, I’d say that is likely if prices continue to stabilize, and the Fed could potentially pause its rate increases in spring to summer 2023. But inflation doesn’t follow predictable patterns.

Core inflation at 6.3% remains much too high. The Fed knows this. The markets know this. Rate increases are likely to continue, but possibly the pace of increases will be slowing. Inflation tracker Michael Ashton posted this today on his E-piphany site:

The Fed … will take the peak in Core as a reason to step down to 50bps at the next meeting, then probably 25bps, and ending at around 5%. If rates are at 5% and median inflation is around the same level late next year, it isn’t clear that much higher rates would be called for especially in a recession. But neither will much lower rates. So I think overnight rates get to 5% and then stay stuck there for a while.

The immediate result of today’s inflation report was a sizable drop in real and nominal yields, with the 10-year Treasury note dropping from 4.12% to about 3.92% and the 10-year TIPS real yield falling from about 1.70% to about 1.54%. But we have learned to expect volatility in the bond market, one of the hallmarks of 2022.

The result, however, could be a lower real yield on the 10-year TIPS to be reopened at auction on November 17. I will be posting a preview of that auction over the weekend.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Uncertainty surrounds this week’s 10-year TIPS auction | Treasury Inflation-Protected Securities

Hopefully, the FED will stick with it’s projected course of increasing rates. But, it looks like they’ll be getting progressively smaller.

For the most of this year, I’ve been converting maturing CD’s into TIPS because the real yields have been steadily rising.

Yesterday, the yields ended the day at 1.69% on a 5 year TIPS (Bloomberg). Today, it sank to 1.46%. 23 basis points in one day!

Today, a 5 year nominal Treasury is yielding 3.94%. That creates a reasonable TIPS breakeven rate of 2.48%.

However, if those 5 year brokered CD’s maintain a 5.0% yield the TIPS breakeven rate is a more expensive 3.54%.

That 5% brokered CD is also just above the annualized future inflation of 4.9% based soley upon October’s number (October’s 0.41% times 12).

Since that 4.9% is greater than 3.54%, TIPS are still a better deal right now.

What the average inflation will be for the next 5 years is anyone’s guess.

2.5% average inflation over the next 5 years is probably a certainty.

3.5% average inflation is possible.

So right now, TIPS are still a better deal than nominal Treasuries.

But 5% CD’s are looking more attractive if inflation settles in at around 3.5%.

Since TIPS are based upon the seasonally unadjusted CPI-U, that’s the measure of inflation that I track.

It is very dangerous to make decisions based on one month of change in core CPI data, as in the Oct 2022 increase of .27%. The table below shows monthly change in core CPI back to March 2021. You will notice that in every case but one, a change in core CPI of .32% or less was immediately followed by at least two months of change in core CPI where each month exceeded .50%. The exception was the three month period Jul Aug Sep 2021 where each month had a low change in core CPI, but for the next five months, each month’s change in core CPI exceeded .50%.

Date Core CPI % change

2021-03-01 271.347 .30

2021-04-01 273.669 .86

2021-05-01 275.715 .75

2021-06-01 277.922 .80

2021-07-01 278.794 .31

2021-08-01 279.306 .18

2021-09-01 280.017 .25

2021-10-01 281.705 .60

2021-11-01 283.179 .52

2021-12-01 284.770 .56

2022-01-01 286.431 .58

2022-02-01 287.878 .51

2022-03-01 288.811 .32

2022-04-01 290.455 .57

2022-05-01 292.289 .63

2022-06-01 294.354 .71

2022-07-01 295.275 .31

2022-08-01 296.950 .57

2022-09-01 298.660 .58

2022-10-01 299.471 .27

Hmm It is claimed that debasing the currency is an age-old technique of governments.

(A History Of Interest Rates by Homer & Sylla) Useful for inflating away unmanageable debt.

Indeed fiat money can inflate more or less endlessly to replace all debt denominated in that money. Until political revolution, that is.

See, pundits get the debt all wrong:

-some pundits say debt is not a problem, and will never be a problem (not true)

-some pundits say debt is a problem, and we will face some catastrophic deflation in the economy because of it (also not true)

Debt is a problem, but a problem that can be “managed” by currency debasement. Eventually, the dollar will lose all value.

But right here and right now, that’s neither here nor there, because what you need is a strategy to keep up with the inflation that is happening now. Yes I know, easier said than done.

What will this mean for the break-even rates?

I’d expect break-evens to be falling today, and they were already fairly low. The 10-year breakeven closed yesterday at 2.42%, and right now looks to be about 2.37%.

But wouldn’t a lower break-even rate make TIPs more attractive?

Preferably, I would like to have a high real yield and zero break-even.

Yes, more attractive versus a nominal Treasury of the same term.

Thank you for the updated information on Oct CPI.

This is my first year holding TIPS in Treasury Direct and I would like to know what my tax liability will be for TY 2022. For example TIPS 91282CEJ6 is showing an Inflation-Adjusted Value of $5,245.70 as of Oct 17, 2022. Is this the year end value for this TIPS or does Treasury Direct adjusted to Dec 31, 2022? If they adjust to Dec 31, 2022 how is it calculated?

So my tax liability would equal the Inflation-Adjusted Value minus my cost basis.

Thanks

Your yearly tax liability for TIPS is a combination of 1) the coupon interest payments, reported on form 1099-INT and 2) the inflation accruals for that year, reported on form 1099-OID. That adjusted value you see does not include the coupon payments. Make sure to log into TreasuryDirect to get your tax forms early in the year. Since TIPS accruals are applied daily, I’d think the 1099-OID would include accruals through the end of December.

Thank you

Maybe the market’s expectation for this inflation number were a bit too high. October is one of the lower inflation months, non-seasonally adjusted. The last 20 years of Octobers averaged 0.01%. November and December are lower yet, non-seasonally adjusted at -0.20% and -0.18%.

I did feel that 0.7% looked high, after three months of relatively tame inflation. Gas and food prices were the key, but other trends kept the increase from meeting the prediction.

Excellent summary and good news for the economy. I think I-bonds are an excellent investment in declining inflation as they look backward. TIPS are interesting in a stable or rising inflation environment. I’ll be looking for an inflection point to begin shifting my I bond portfolio to TIPS or perhaps equities depending on circumstances.

Even though I am heavily invested in inflation-indexed securities I don’t take much comfort in an annual inflation rate of ‘only’ 7.7%. Surely allowing inflation to rise to over 4X its preferred level of 2% (June 9.1%) reeks of incompetence.

We will have another jobs report before the Fed meeting, which might keep it in the 75bps camp…. thank you for all your articles and insight – purchased my first TIPS last month 🙂