It is CUSIP 912810RA8, first auctioned on Feb. 13, 2013. It wasn’t a great investment back in 2013. But now …

By David Enna, Tipswatch.com

Earlier this week, on Wednesday afternoon, I did something I’ve never done before: I bought a TIPS on the secondary market. Oh sure, many of you have done that many times before. But not me. I’m the “buy at auction and hold to maturity” guy.

Why would I do that? Because I had been eyeing the potential to buy a TIPS, probably with a maturity of around 20 years, with a real yield to maturity higher than 2.0%. Each day, sometimes several times a day, I’d take a look at TIPS maturing in 2040 to 2044, which seemed to be the sweet spot for that 2.0% real yield. (The 30-year TIPS — which I would not buy — actually had a lower real yield.)

The U.S. Treasury, unfortunately, stopped offering 20-year TIPS at auction back in January 2009 and very few were ever offered. I’ve argued it would be an excellent addition to the TIPS lineup, but the Treasury doesn’t seem to listen to me. The lack of this maturity creates a “hole” in TIPS maturities, with zero TIPS maturing from July 2032 to February 2040.

My personal TIPS ladder, until this week, ended with a 30-year TIPS I purchased back in 2011, with a still-sweet coupon rate of 2.125%. I wanted to extend that ladder by one final issue.

I had looked earlier in the day on Wednesday and found nothing I could snag above 2.0%. But I checked again Wednesday afternoon and noticed that CUSIP 912810RA8, which matures Feb. 15, 2043, was being offered with a real yield to maturity of 2.02% for my investment of $10,000. So … I bought it. This chart shows why I thought a 20-year real yield above 2.0% looked historically attractive:

Let’s look at CUSIP 912810RA8

The originating auction for this 30-year TIPS was on Feb. 21, 2013, and yes, I wrote a preview article about that auction. (I’ve been at this a long time.) I wasn’t too impressed. Even then I was worried if I would live long enough for the TIPS to reach maturity:

“My strategy with TIPS is to buy them and hold them to maturity. I don’t ever look at their prices on the secondary market, I don’t care. Viewed this way, TIPS are a very conservative, very predictable, and very boring investment. The problem with a 30-year TIPS is: Will I live long enough to see it mature? I am 59. I could live to 89.”

Oh, to be young again. Now I am 69, and looking at very same TIPS. My biggest problem back in 2013 was that the Federal Reserve had launched into quantitative easing, forcing Treasury yields lower. I noted that real yields at that point — around 0.60% — were historically low, which is not good for a very long-term investment. From my 2013 preview article:

“Someday – maybe soon, or maybe not – 30-year TIPS will again be yielding 1.5%, or 2%, or more. When that day comes, the secondary-market value of a long-term TIPS yielding 0.6% is going to be crushed.”

Zoom forward to November 2022. Now, finally, the real yield to maturity for this TIPS — at least on Wednesday — had finally broken the 2.0% barrier, reaching 2.02%. The original investors in CUSIP 912810RA8 had indeed taken a beating. The original auction got a real yield to maturity of 0.639%, setting the coupon rate at 0.625%. Investors paid an unadjusted price of $99.62 for $100 of par value. On Wednesday, this TIPS was selling on the secondary market with a price of $76.73, down 23% from the original purchase price.

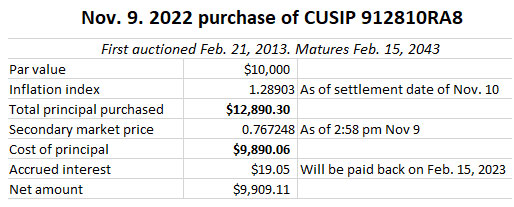

Now, let’s look at the basics of my purchase of $10,000 of par value in this TIPS:

Note that I purchased $12,890 in principal in this TIPS for just $9,890. That means I paid below the par value of $10,000, which is guaranteed to be returned at maturity, even if severe deflation sets in. (I consider this more of an oddity that a true issue.) But more importantly, note that the original purchaser of this TIPS had accumulated $2,890 of inflation accruals, but the rise in the real yield from the original coupon rate of 0.625% to Wednesday’s real yield of 2.02% had wiped out that entire inflation accrual. Of course, the holder of this TIPS had collected a coupon rate of 0.625% along the way, but losing your entire inflation accrual is … painful.

This is a reason I am definitely not a fan of long-term Treasurys of any type, unless the nominal or real yields are historically attractive. And this TIPS investment could end up biting me if real yields continue climbing to 3% or 4%. But … no problem, I am holding to maturity, if I live that long.

Did I luck out?

Who knows, but Thursday’s weaker-than-expected inflation report has sent Treasury yields plummeting. As of the market close Thursday, CUSIP 912810RA8 was trading with a real yield of 1.83%, down about 19 basis points in one day, and its price was about $79.69 for $100 of value, about 3.8% higher than the price I paid. But … who cares? I really do intend to hold this to maturity.

The secondary market for TIPS is complex and if you intend to dip in with purchases, you need to understand the basics of any purchase … par value, inflation index, market price, accrued interest. I hope this article will help.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you, I have learned so much from your website and am trying to wrap my head around how TIPS on secondary market works. This article helps a lot. But one thing that still confuses me. How do we get a real ytm of 2.02% for 912810RA8? Could you kindly walk through the calculation? Also does a real ytm of 2.02% mean that the semi-annual interest you receive is 1.01% (=2.02/2) * inflation-adjusted principle, going forward till maturity?

The 2.02% real return comes from two sources. First is the fixed interest rate which is 0.625% for this security. The rate never changes for the life of the bond. The amount of the semiannual interest payment will increase if the Treasury’s inflation adjustment causes the bond principal to increase (and it almost always does), but the rate does not vary.

The remaining 1.395% of the real return comes from the difference between what is paid for the bond and what the Treasury says the bond principal is worth. In this case, our hero paid $989 for each bond that the Treasury said was worth $1,289. If he holds to maturity, he will capture that difference (think of it as you would a “capital gain” on a stock) which will result in a final total real return of 2.02%. Wait!, you say, That’s a 30% capital gain!, but spread out over the 20+ years to maturity this works out to a 1.395% real yield for this portion of the real return.

Excellent reply, thank you!

Question for you David. I’m 49 and want to slowly build a TIPS ladder that will supplement my Social Security from ages 70 to 90 to provide a guaranteed floor of annual income. Initially, I thought I would just buy a new 10-year TIPS at auction in my IRA every year, but seeing this post has me wondering if buying on the secondary market would be better (at least for now) considering that I could buy a long-term TIPS for less than principal and even par value. Almost seems too good to be true. Am I missing something?

I agree that this could be a good time to begin building a TIPS ladder on the secondary market, but only because of the attractive real yields. The discount to par and principal all works out “more or less” the same if you buy at auction or on the secondary market. High coupon rate = premium price. Low coupon rate = discounted price. The one factor that matters most of all is the real yield to maturity. TIPS are priced on the secondary market to reflect the market conditions. Day to day, you may find yields you like. Good time to buy? Maybe. Will tomorrow be a better deal? Maybe. I just say buy and don’t look back.

Thank you. I appreciate your website. I’ve always owned Vanguard’s TIPS fund and started buying I bonds 2 years ago for me and my wife. However, I finally decided to dive into individual TIPS as well despite their complexity (which always discouraged me) – the Explore TIPS book and your website have been instrumental in my education.

Pingback: I Bonds vs. TIPS: Right now, it’s clearly ‘advantage TIPS’ | Treasury Inflation-Protected Securities

Good purchase with moderate accrual do to low coupon rate and price discount to get Wednesday ‘s higher yield. There were times in the past when coupon rates were higher and the premium due to principal accruals are now substantial. In the highly unlikely but still possible event of a major prolonged deflation there’s a remote chance of loss of principal at maturity. Would that concern you?

Buying accrued inflation is a minor issue, in my opinion, but less of an issue when you are getting it at a discount. I’m not particularly concerned about prolonged deflation. Fact is, I own many TIPS purchased over the years and they all have accrued principal and all have the same deflation risk.

Hi David — I’m trying to understand to what extent buying on the secondary market is really more complex than just shopping for a desired maturity date and an acceptable YTM quote. A brokerage will quote you the total cost to purchase a given quantity of TIPS, and one can adjust the quantity up or down until the total investment amount matches the amount one wishes to invest. Confirm the purchase, and at maturity you will have earned the quoted real yield on every dollar you just used to buy the TIPS, right?

Does a hold-to-maturity investor really need to perform a deeper analysis than this? Is there a way to go wrong? Thanks for your thoughts!

It’s more a matter of understanding what you are buying and how it is priced. The issues on the secondary market are 1) the premium/discount to par can be higher than you might expect, 2) the accrued inflation can be quite high, meaning you will be buying additional principal (at a discount or premium), and 3) buying small quantities of TIPS may mean you get a lower real yield than you see originally quoted. Also, for very short-term TIPS, the real yield might look quite wacky. All of that is fine and not a problem, as long as the investor understands what is happening before hitting “submit order.”

Right, so I understand that on the secondary market one may not pay anything close to exactly $10,000 for TIPS with face value of $10,000. So I guess my question, restated, is “once the brokerage (Vanguard) has prepared your order and is displaying the actual net amount of the investment (say $11,499), and the YTM (say 2.033%), and you submit that order, is there a world in which you might end up NOT earning exactly the 2.033% real on the $11,499?”

I think the real yield is locked in at the purchase, yes.

Do you consider your TIPS ladder as a replacement for holding other bonds (lets say in a 60/40 portoflio for example)? Just curious what the fixed income side of your overall portfolio strategy looks like. I’m approaching 50 and beginning to think more about this.

Yes, I do consider all the TIPS and I Bonds I own as part of my fixed-income allocation, along with some traditional Treasurys and bank CDs. My core bond fund is Vanguard’s Total Bond Fund. Inflation protection makes up about 15% of my overall portfolio.

How did you decide the amount and length/structure of your TIPS ladder? I’m presuming delaying SS.

I just started following you, great posts, thank you!

It’s been haphazard, through buying 5- and 10-year TIPS at auction, but only when I liked the real yield. So I have some empty spots in 2030 and 2031. If I see attractive yields I might fill those soon, through the secondary market.

Ladd, for a ladder to delay SS, you first calculate what yearly expenses you want the ladder to pay. When I was 49, I started making a ladder to pay expenses from 59.5 to 70. So I was buying 10-20 year maturities back then. I’m 63 now and each year some bonds mature to match those expenses. The interest you get each year from all the bonds helps to reduce the amount of principal committed to the ladder.

Is the take away from this that the secondary market exposes the risks of the long term (your original auction purchase)? But are you not happy with your recent purchase on the secondary market?

The long-term risks are apparent at the originating auction, with a 30-year TIPS having a duration of 30 years, meaning its price will swing sharply with even small interest rate moves. This purchase was a small addition to my TIPS ladder and yes, I am happy with it.

I guess my question was, will you buy in the secondary market again? I am struggling with too or not.

I’ll probably use the secondary market again, if real yields continue to be attractive.

Excellent! Thank you so much David for explaining…I’m still trying to wrap my head around the secondary market. Every explanation gets a little more understanding through my skull. 🙂

You referenced long-term treasuries and your aversion to them ‘unless the nominal yields are historically attractive’. What are your thoughts about the long bond now (barely) at over 4%? Do you have any forecast, gut feeling, etc. about where this yield is going? My own feeling is that it’s still a bit early to go out this far in duration, especially when we’re still in a hiking cycle. I’m guessing long yields will most likely peak in the spring of ’23 at the earliest. But these things are impossible to predict… On the other hand, I also believe we have a lot of secular deflationary forces at work which will (at some point) rear their heads once more. Good buying opportunities might not last long. Like you, I buy and hold to maturity. Thoughts? Thanks and kudos.

I’m generally adverse to buying TIPS or nominals with a term longer than 10 years because of the potential volatility. Did interest rates actually hit a flex point this week? Amid all market fluctuations, it’s hard to say. But the October inflation report did push yields down, even for the 4-week Treasury bill. If yields are peaking, longer maturities make sense. The Fed will eventually back off, but when? I expect to hear signals.

Hi David,

I have been following your blog for past year or so. Thanks for the detailed analysis you do for your readers.

Since this thread got into interest rate speculation, I thought of something that I wanted to ask for a while. I remember you mentioned a chart that displayed that the yields start falling off the cliff as soon as feds start reducing the rates – and that the window to get the peak rates is fairly small. Based on your previous experience, does that happen when The Fed actually reduce the rates or does it tend to happen speculatively as soon as there’s QE-like language in the Fed notes ?

This time could be different, since the Fed is likely to “pause” instead of going immediately to rate cuts. That didn’t happen in 2020, when the pandemic struck. I wrote a series of articles on what happened from 2013 to 2019, the last Fed tightening cycle. In 2019 the Fed did repeated rate cuts and launched them fairly quickly: https://tipswatch.com/2021/07/12/2019-federal-reserve-reverses-course-bond-funds-take-off/

You must be buying these for your heirs? When I saw the long dates was guessing you were 40!

Who knows? My wife will probably make it her mid-90s, at least, I predict. My main goal in this exercise was to see if I could get a longer-term TIPS with a real yield higher than 2.0%.

Your heirs will gratefully remember your wisdom as they continue to hold these securities to maturity.

What would you think about a TIPS on the secondary market that was maturing in three years with a rate of 2.25% and a real yield slightly under that (over 2%)? If inflation averages 3.5% over the next three years, that’s 5.5% plus total yield. If it’s in a taxable account, you’re getting enough interest to pay the taxes. Three year treasury security at 5.5% and maybe more seems like a pretty good bet.

Treasury yields dropped dramatically Thursday, and I think the bond market is closed Friday for Veterans Day. I think you might be talking about the TIPS that matures in Jan 2025 with a coupon rate of 2.375%. So you’d be paying about a 1% premium for par value + 57% accrued principal. Real yield at the close Thursday was 1.887%. So $10,000 par of that TIPS will cost about $15,736. On the plus side, you’d get the coupon rate on the higher accrued principal.