By David Enna, Tipswatch.com

Opinion: Nominal and real yields for mid- to longer-term Treasurys are lower than they should be. The Federal Reserve is aggressively tightening, sending clear signals it wants interest rates heading higher. But the result is lower yields on 5- to 30-year Treasurys.

Why is this happening? Some guesses: 1) The bond (and stock) markets are beginning to price in a slowdown in U.S. economic growth, most likely leading to a recession in 2023; 2) The markets don’t fully buy the Fed’s determination to keep fighting inflation no matter what; and/or 3) The markets believe that U.S. inflation is under control and will slip much lower in 2023.

Since Nov. 1, the nominal yield on a 5-year Treasury note has declined 57 basis points, from 4.18% to 3.61%. The real yield on a full-term 5-year Treasury Inflation-Protected Security has declined 15 basis points, from 1.61% to 1.47% as of Friday’s market close, based on Treasury estimates.

That’s significant. TIPS yields have been holding at higher levels than comparable nominal Treasurys. When that happens, the market is pricing in lower future inflation. And when that happens, TIPS go on sale versus their nominal counterparts. TIPS are attractive right now.

Thursday’s 5-year TIPS reopening

On Dec. 22, the Treasury will offer $19 billion in a reopening auction of CUSIP 91282CFR7, creating a 4-year, 10-month TIPS. (FYI, that $19 billion size is the largest in history for any 5-year TIPS reopening, up from $17 billion in last December’s comparable auction.)

CUSIP 91282CFR7 had an originating auction on Oct. 10, 2022, which at the time I called a “unicorn event” because of a slew of factors making that offering attractive. It ended up auctioning with a real yield of 1.732%, highest for this term in 15 years, and the coupon rate was set at 1.625%, also the highest for this term in more than 15 years.

And now it will be reopened Thursday. This TIPS trades on the secondary market, and you can track its current real yield and price in real time on Bloomberg’s Current Yields page. At Friday’s close it was trading with a real yield of 1.46% and a price of $100.76 for $100 of value. The price is at a premium because the real yield is now below the coupon rate of 1.625%.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.46% means an investment in this TIPS will exceed U.S. inflation by 1.46% for 4 years, 10 months. If inflation averages 2.2%, you’d get a nominal return of 3.66%, on par with a nominal U.S. Treasury. But if inflation averages 4.5%, you’d get a nominal return of 5.96%.

Pricing. This TIPS will carry an inflation index of 1.00576 on the settlement date of Dec. 30. That means investors at Thursday’s auction will be paying roughly $101.34 for about $100.58 of accrued principal, along with an additional 34 cents of accrued interest. Put another way, an investor placing an order for $10,000 of par value of this TIPS will be paying about $10,134 for $10,058 of principal. That’s a rough estimate and things could change by Thursday.

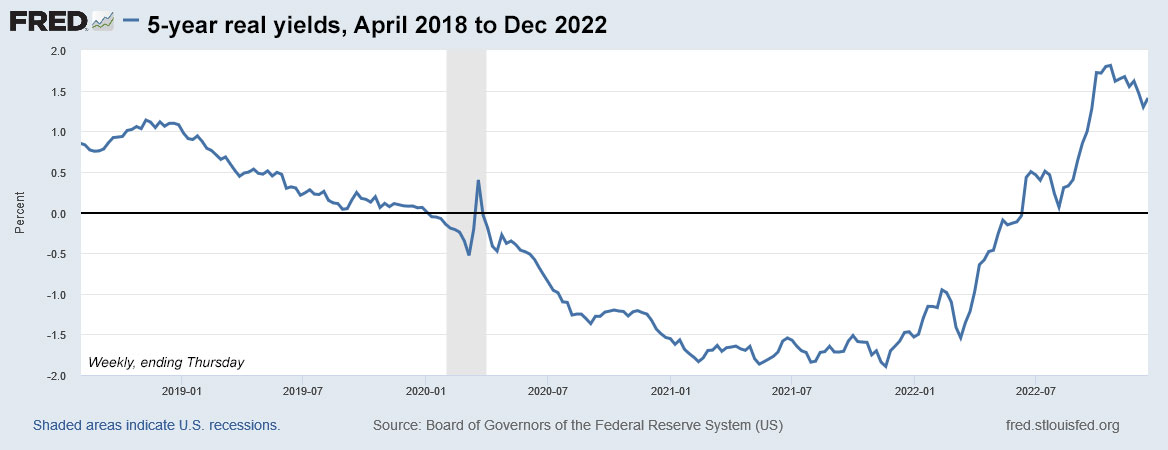

Here’s the trend in the 5-year real yield over the last 4 1/2 years, showing how yields have declined since peaking in October, but remain historically attractive:

Inflation breakeven rate

With a 5-year nominal Treasury note closing Friday with a yield of 3.62%, this TIPS currently has an inflation breakeven rate of 2.16%, a rate that seems surprisingly low for a short-term investment in a time of 7.1% U.S. inflation. Over the last five years, inflation has been averaging about 3.9%.

So we come back to my point that real yields on TIPS have been declining much less than those on nominal Treasurys of the same term. Why? Investors are betting that U.S. inflation will decline to historical levels very quickly. I’ll take the other side of that bet: I think inflation will average more than 2.16% over the next five years, so this TIPS is an attractive investment.

Here is the trend in the 5-year inflation breakeven rate over the last 4 1/2 years, showing that inflation expectations have been sliding lower since March 2022.

Final thoughts

Although I have loaded up on TIPS maturing in 2027 this year, I am likely to be a buyer at Thursday’s auction. A real yield of 1.46% is historically attractive. Yes, yields could climb higher, but this TIPS is a safe hold-to-maturity investment. I will also be looking with strong interest at the new 10-year TIPS to be auctioned Jan. 19, filling a 2033 spot in my TIPS ladder.

Some TIPS investors don’t like buying additional principal at a premium price, but I think a real yield of around 1.46% — if it holds through Thursday — is good enough to overcome that objection. Since October 2009, there have been 41 TIPS auctions of the 4- to 5-year term and only two have generated a real yield above 1%. Real yields could eventually head even higher, but I feel the need to nibble away at these while they are available.

One note: I do think U.S. inflation (specifically non-seasonally adjusted inflation) could hit a brief, illusionary low-inflation or deflationary spell early in 2023. The year-ago inflation numbers will be hard to beat: January, 0.84%; February, 0.81%; March, 1.34%, April, 0.56%, May 1.10% and June, 1.37%. That will mean the annual inflation number should be declining, even as U.S. prices continue to increase. It’s something to be aware of if you fret about your TIPS investments month to month.

My schedule

When this auction closes at 1 p.m. Thursday, I am likely to be on the road to visit relatives for the holiday. I won’t be able to post the results immediately. You can find results on this page soon after the auction closes.

Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

Here’s a history of recent 4- to 5-year TIPS auctions, highlighting the only two auctions over the last 13 years with real yields higher than 1%.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Great article! You mention possibly filling in the 2033 gap with the January 19th 10-year TIPS auction and I’m considering the same. When I created my 30-year ladder (on the secondary market with settlement date of 11/1/22) I bought an extra $72,000 par value (adjusted settlement principal $73,393) worth of CUSIP#91282CEZ0 bonds maturing in 2032 to cover the year 2033. I paid $67,570 for those extra bonds for a yield to maturity of 1.507%. I’m now wondering how I would go about deciding in January whether it makes sense to sell those bonds (at whatever the market price is at that time) and purchase a comparable amount of 2033 bonds at auction. I’ve never personally seen a write-up of how to make such decisions related to filling in the gap years and am curious if you have any thoughts. Thanks!

Making sure I understand all this correctly – if I purchased $10k in TIPS in today’s auction, it means I paid $10,114 for $10,000 in principal. Only the principal is guaranteed if I hold the security until maturity; the $114 premium is the price you pay for an attractive real yield.

Is the real yield of 1.5% the yield above the rate of inflation per year, or is it the aggregate real yield after 5 years? If 1.5% is the real yield after 5 years, that translates to about 0.3% per year. Also not sure I understand the difference between high yield vs. interest rate. Are the semiannual interest payments for today’s 5-year TIPS 1.504% or 1.625%? Thanks for clarifying.

If you bought $10,000 par value of this TIPS you were buying $10,057.60 principal because of the inflation index (1.00576) at the closing date. Because of the premium price you paid about $10,113.51 for that principal.

1.5% real per year.

1.504% yield. Unadjusted price of 100.556; with adjustment and interest, $1000 in par costs $1014.76.

I’m very new to this. The site: https://www.treasurydirect.gov/auctions/announcements-data-results/ lists the cost as $101.135096. Is this incorrect?

You also have to pay two months’ worth of accumulated interest. Confusingly, that’s listed as $3.41240 per _thousand_, so $0.34124 per hundred. Adding that in gets you to $101.476336.

Wednesday update, 11:30 a.m: It looks like real yields are slipping a little this morning, one day before the auction. This TIPS is currently trading with a real yield of 1.44% and a price of $100.87. And a reminder: I will be on the road Thursday and will not post auction results quickly.

I am in on this one for my Roth IRA. I bought some of the original issue too. I don’t fully understand the numbers, but I believe that inflation is going to be persistent for quite a while, so I am hoping for the best.

Or in a case of the deflationary environment I-bonds paying 0.4% on the deflation protected principle would be the secure money winner?

If a deflationary variable rate exceeds 0.4%, it would wipe out the fixed rate, resulting in a six-month composite rate of 0.0%.

Perhaps inflation has finished and then a worse case appears… deflation. Seems like in a case of the deflationary environment TIPS would be a poor investment compared to fixed Treasury bonds or fixed rate bank CD’s no?

Yes, nominal Treasurys will perform better under severe deflation.

Deflationary periods have happened before, after severe inflation, in the past.

I am needing more tax advantaged space for purchase of these higher yielding TIPS..I currently own a significant amount of cusip 91282CFM8 which is yielding a profit over my auction purchase. Is there any red flag I am not aware of to persuade me against selling some of that 5 year treasury and purchasing more of the 5 year tips at auction this week? I understand you cannot offer “investment advice per se” but this seems like a no-brainer to me…

CUSIP 91282CFM8 is a 5-year Treasury note that matures Sept 2027. (I own that one, too, and I am holding it.) I am assuming you can sell this at a profit and if the TIPS is more appealing, go for it. The inflation breakeven rate on that swap would be about 2.7%, a bit steeper than the current breakeven.

Are there any differences between buying at the auction vs. the secondary market? What do I need to understand about either way? Pros/Cons?

Not a huge difference. Non-competitive investors at the auction don’t know the yield they will get in advance, but they get the “high yield,” which is the highest yield the Treasury must provide to complete the auction. That is an advantage. You are more in control on the secondary market, but may face iffy bid/ask spreads, especially for smaller purchases. TIPS on the secondary market may have very large inflation accruals, which you have to buy in addition to the par price you might think you are paying.

Real yields are going up! Fingers crossed we get to 1.6% by Thursday.

Well, we’ve got 1.5%. Still, not bad.

I placed an order with my broker for the reopening of the 5-Year Tips, but it says “expiration 12/22/2022 8:30 AM”??

Not sure, but could mean that your order can’t be canceled after 8:30 am Thursday.

Right, it seems that 8:30 AM is the cut-off time to place orders for the Treasury auction. After that, it can neither be cancelled.

With Tips….. the principle is affected by the monthly inflation rate. I believe if the inflation rate for 3 consecutive months is for example is 0.5, o.3, 0.1, ie. there is “disinflation”, meaning a reduction in the inflation rate, but it is still inflation, so the principle would increase by 0.5%, then 0.3%, then 0.1% respectively. Only if there is actual deflation for a month, ie, if inflation is for example for three months 0.4, then -0.1, then 0.3, then the principle would increase 0.4%, reduce by 0.1%, then increase by 0.3%. Is my understanding correct? thank you!

This is correct

For TIPS, is the inflation adjustment based on annual inflation (like I-Bonds), or is it based on Year over Year. Will the principal amount go down because of the “illusionary” year over year? It isn’t really deflation, as prices continue to go up. But it can lower the principal amount? So do TIPS really keep up with inflation?

The TIPS inflation adjustment is based on non-seasonally adjusted monthly inflation, from two months earlier. The Treasury creates inflation indexes for every day of the month. Right now, in December, the balances are rising 0.41% for the month. In January, they will fall 0.1% over the month, based on November’s -0.1% non-seasonal inflation. As I noted in the article, monthly inflation could continue to rise in the first half of 2023, but annual inflation is likely to decline because of the very high monthly numbers from last year.

If the inflation rate for I-Bonds is 6.4% for six months, is this the same rate that is applied to the principal of TIPS?

I Bonds earn a variable interest rate based on six months of inflation. The current variable rate of 6.48% is based on the 3.24% inflation we experienced from March to September. TIPS earn inflation accruals month by month, and would have earned 3.24% for that six months period (+ 2 months lag time). That annualizes out to about 6.48%.

I prefer not to pay the excess principal so I bought the 4/15/27 instead on the secondary market today. The real yield was 1.63%.

Looks like a great buy.

Thank you for the article and education. I am still learning about TIPS. Your answer and patience are greatly appreciated.

Comparing 91282CFR7 the reopening auction on 12/22/22 to the one that T. Lee purchased with the real yield of 1.63% which I assumed it’s 91282CEJ6 ( I could only find this one with the same maturity date) with the coupon rate of 0.125%, a few questions come to mind so I can try to wrap my head around TIPS:

1. Why is paying excess principal bad if the coupon rate of 1.625% is higher than the projected real yield? If I were to pay $10,134 for 91282CFR7 as projected, will I be getting at least $10,134 back at maturity or only the par value of $10,000?

2. Is the real yield the only thing that matters when comparing different TIPS with similar terms? Vanguard shows “Yield to worst and maturity”, not “Real yield”. Is “Yield to maturity” the same as “Real yield” in the secondary market?

3. Since the coupon rate is higher on 91282CFR7, does that mean if the inflation were to drop below zero %, this TIPS can still earn the coupon rate as interest?

4. I understand that buying in the secondary market, there is a spread cost to purchase, but is it better to buy the “known” Real yield, than the “unknown” Real yield in this comparison?

Thank you. I know that these are very basic questions but as a beginner, TIPS can be really confusing.

1. Some investors tend to shy away from buying large amounts of additional principal, so the yield might have to be a bit higher for those TIPS.

2. Real yield is by far the most important factor for TIPS with similar terms. I don’t quite get the concept of yield to worst, but I do understand it is simply stating that is the worst yield that can result from the investment.

3. The coupon rate will always be paid out until maturity, so there is an advantage to a higher coupon rate. But a lower coupon rate TIPS will sell at a deeper discount. It probably all works out the same.

4. The spread becomes a bigger issue when you make a smaller purchase, but the brokerage should be giving you accurate information on what you will be paying. You can look at that and decide yes or no.

Here’s why I purchased the 4/15/27 – first, the problem I’m solving is that I have cash in my IRA that I’m not distributing this year. I want to distribute it in 2027. I don’t need any income from it to buy things in the meantime. With the 4/27, I only get 0.125% paid out every 6 months and the bulk of the real yield of 1.63% will come at maturity when I want it. If I buy the 10/27, then I’ll be getting all my real yield from the coupon of 1.625% and I’ll have to figure out how to invest that money every 6 months. And I won’t likely find inflation protection unless I buy more high-coupon, excess principal TIPS. So for my problem, low-coupon, discount bonds are the way to go. The “set it and forget it” approach.

Someone who wants current income to buy things now would prefer the 10/27 for its higher coupon. It’s not a matter of one security being better than the other. It depends on what the purpose of the security is in your situation.

YTW and YTM are the same for non-callable bonds. YTW only comes into play with callable so not an issue with TIPS.

There is a spread in the secondary market, but it’s pretty narrow for TIPS, a few basis points. There’s no spread at auction since it’s all bid and that’s what I usually do. And if you’re not buying 6 figures, you usually have to go down the ask list to find someone who will sell you a smaller amount. So the best ask was 1.64% when I purchased and I had to go down the list and wound up giving up 1 basis point. Not a big deal.

Excellent information.

Thank you for your reply.

I am not buying a 6-figure purchase. The comparison is for my attempt to understand the complex security such as TIPS (complex for me:-)

Since in Vanguard’s case, only the Yield to Worst/Maturity is displayed, how will I determine the “Real Yield”?

For example:

As of 12/21/22 at 2PM. CUSIP 912828V49 has a coupon rate of 0.375%. Purchase Price of $95.21. Yield to Worst of 1.596%. It has a factor of 1.23225 and a Maturity Date of 1/15/27. The yield at issue was 0.436% and the Price at issue was $99.406.

I really appreciate the education to help me understand what I am buying.

I will be posting a guide to the “language of TIPS” on Tuesday morning. Hope that will help. In this case, that yield to worst of 1.596% is the real yield. The factor of 1.23225 is the current inflation accrual, so that means you will be purchasing 23% extra principal above par. The coupon rate is 0.375%, well below the current real yield, so the TIPS is trading at a discount price of $95.21 for $100 of value. All the “at issue” information isn’t really relevant.

Thank you so much. The guide will be really helpful. If you have a way and are willing to share your spreadsheets, that will be wonderful.

I am going through your TIPS Q&A on “How the cost of a TIPS is set” right now trying to replicate the calculations, so I don’t end up with a nasty surprise when buying in an auction with the available funds in an IRA.

Happy Holidays! Thank you again for the education.

I bought the 4/15/27 in June and August in the secondary market. The yield to maturity was only 0.492% and 0.581%. How quickly the yield has changed.

Mr. Enna, Thanks as always for all the great information. Appreciate all the time and effort involved. Just a humble suggestion. Is it possible to add the “Comments” link at the top of the article too? I come here several times a day to learn from your answers and the community as a whole. Especially during TIPS events. Get really excited when the comments count goes up. This section is pure gold just like your writing.

I don’t think I can add a link but I did add a “latest comments” feature to the right-hand side-panel. I think you could only see that on the computer desktop version.

No problem and Thanks again!

“The Federal Reserve is aggressively tightening, sending clear signals it wants interest rates heading higher. But the result is lower yields on 5- to 30-year Treasurys.”

“Why is this happening? Some guesses:”

4) Foreign investors buying Treasuries.

To understand, let’s look for example at the Japanese. Their own bonds yield little to nothing while their currency is depreciating against the dollar. Buying Treasuries make sense to them as they get a relatively good yield AND the Treasury principal is appreciating as the dollar is appreciating against the Yen. Win Win.

Treasury data through October instead shows the Japanese to be net sellers of U.S. Treasury bonds this year.

https://ticdata.treasury.gov/resource-center/data-chart-center/tic/Documents/s1_42609.txt

“In theory, theory and practice are the same. In practice, they are not.”

Unless the TIC data is false.

Yogi Berra: “Nobody is buying Treasuries anymore, the prices are too high”!

LOL

Hi David,

My wife and I are planning on investing 20k in either this 5 year reopening Tips on Thursday, or two 10k I bonds in early January.

Can you offer an opinion on what you think makes the most sense?

thank you

Chris

As a pure investment, I’d say the TIPS is more attractive, since the yield will be 100 basis points higher. But the I Bond is simple, flexible, tax-deferred. I will be buying I Bonds next year, for sure, but not sure if I will pull the trigger in January.

>I will be buying I Bonds next year, for sure, but not sure if I will pull the trigger in January

Hmm, would you mind elaborating your thought process on that please ? Do you see higher probability of higher fixed rate in May 2023 ? I remember you mentioned in one of your earlier posts (might have been last year) that the fixed rates tend to be close to half of 10-year TIPS yields. Since we are limited to 10k annual allocation for I-bonds, it would make sense to look at the rates in April 2023 and make a decision at that time. Alternatively, get 5k worth now and 5k worth in May. I can’t make my mind on what I should do. So some insight in your thought process would be great.

PS. I’m not looking at these short term. These are more into “hold for 15-20 years” territory.

Regular Reader, in early January I will be publishing a guide to buying I Bonds in 2023. A lot of people do buy every January and just get it done. That’s fine. But for a long-term investor, buying anytime through April will earn exactly the same return. So you can wait until mid April, if you want, and you will know the new variable rate and have a decent idea if the fixed rate will increase.

Wondering if I should build a 5 year fixed income ladder now, or wait 6 months, to take advantage of the best yield overall?

No way to say. I’m not a financial adviser, so I can only offer an opinion: I bought a 5-year Treasury note a couple months ago and got a yield of 4.25%. Now that yield is down to 3.65%, so buying earlier was better, but who knew? The advantage has moved to 5-year bank CDs, with some yields still close to 5%. Or brokered CDs? It’s impossible to say where rates are heading.

Can you explain why the real yield on 9128284H0 is 0.504% over the coupon when it sold for only 0.340% under par? Was there some very large inflation adjustment built in at that point?

CUSIP 9128284H0 will mature April 15, 2023, and it has a coupon rate of 0.625%. That coupon rate was set at the original auction in April 2018. The coupon rate never changes, but the real yield to maturity of a TIPS is market-determined and changes several times a day for the people looking to buy that TIPS. The original auction sets the coupon rate; after that the market determines the real yield, and resulting price, for new buyers.

Oh, I see–it is the current real yield!

But…the real yield on the ‘unicorn’ is the same as when I bought it. So I’m confused-ish.

You mentioned the “unicorn,”so I assume you mean CUSIP 91282CFR7, the TIPS that first auctioned in October with a real yield of 1.732%. Now it has a real yield of 1.46%. The coupon rate, which is 1.625%, has remained the same.

For a short term play (6 months) I’m thinking about a quasi-hedge: 50% Treasury bond at 4.5% APR and 50% in a TIPS bond that’s currently under par, both held to maturity. If a recession emerges and deflation causes the TIPS inflation index to decline, the T-bill interest will offset that loss. If the inflation index goes up then I’ll have positive income from both.

I also mix short-term nominal Treasurys (to meet near-term cash needs) and longer-term TIPS (part of my fixed income allocation focused on safety).

If there is a showdown in Congress over raising the debt ceiling, which according to news reports could happen by mid 2023, what would be the best way to manage near-term cash needs to be absolutely sure that you’ll have timely access to these funds (considering checking accounts, MM funds, High Yield Savings accounts, T bills, and/or TIPS etc.)?

I suppose that checking and high yield savings accounts would be most accessible if the situation turns dire, which I don’t think will happen. We had something similar a few years ago and 4-week Treasurys got a boost in yield because of the “risk.”

US has to issue a load of bonds in the near future to cover huge deficits on top of refunding requirements. A recession, especially a sharp one will only make it worse. Fed has two options, flood the market with bonds, thereby raising rates and the deficit, or print dollars to fund the issuance. I’ll bet on the latter option along with financial repression and maybe yield curve control as well as the Fed tries to reduce indebtedness via moderate inflation. This will raise the odds of long term stagflation, a perfect scenario for TIPs. If I’m wrong I get my money back in five years.

No one wants stagflation, an awful scenario. But investors in TIPS would benefit if inflation stays high and interest rates have to hold at high levels. TIPS funds and ETFs would (probably) do well because inflation accruals would increase while NAV value holds or rises.

Not enamored of tips funds. At least with bonds I’m guaranteed to get back at least par regardless of where interest rates are at maturity.

I am with you, but some people want to hunt for capital gains. I’d rather have predictability.

Since I’ve also “loaded-up” on the 2017 maturites, I’m going to pass on this auction. Heck, I ‘ve even stashed some taxable funds into 2017 TIPS.

At my age I don’t like going-out further than 5 years. So, I don’t find the upcoming January auction for 2033 terrible attractive (the wife hates it).

The 2028 TIPS auction doesn’t happen until April. After the November drop in the yields, that seems almost an eternity away.

Last week, the yields on the 2031 maturity TIPS recovered enough so that you could get them for a inflation adjusted price below par ($9,983.98 for 10K).

Since somebody’s eventually going to have to pay the RMD on my IRA, I bought enough of them to cover my RMD for 2031.

Someone else on this forum said that they used their estimated future RMD amounts to create a TIPS ladder.

I use this approach as a rationalization for purchasing TIPS farther-out than 5 years. So far, the wife has even grudgingly gone along with it.

Basically, I just want to purchase as much TIPS as I can while the yields stay north of 1%. How long that’s going to last is anyone’s guess.

It continues to be fascinating to look at your break-even charts, so thank you for always compiling these. I will be participating – I missed the original auction waiting for a CD to mature, and it is interesting to re-read your post of the original auction (and the comments), where there was some disappointment the real yield was not higher. How our expectations change in a remarkable year for Treasuries.