Stock and bond markets are celebrating, with good reason.

By David Enna, Tipswatch.com

For the second month in a row, U.S. inflation came in below expectations in November, clearing the way for speculation that the Federal Reserve could soon pivot away from interest rate increases in 2023.

The Consumer Price Index for All Urban Consumers rose just 0.1% in November on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 7.1%. Both of those numbers were below expectations of 0.3% for the month and 7.3% year over year.

Core inflation, which removes food and energy, also came in below expectations, rising 0.2% for the month and 6.0% for the year.

The all-items increase of 7.1% was the smallest 12-month increase since the period ending December 2021, the BLS said. The core increase of 6.0% was the smallest since August 2021.

Obviously, this inflation report will be greeted with joy in the stock and bond markets, providing a clear signal that the Federal Reserve can set a path toward less-aggressive monetary tightening. Just a few minutes ago, I heard a Bloomberg commentator suggest that we need to revive the “transitory” description for U.S. inflation. Uh … let’s not get ahead of ourselves.

The BLS noted that the cost of shelter (up 0.6% for the month and 7.1% for the year) was the biggest factor in all-items inflation, more than offsetting a 2.0% decline in the cost of gasoline (which is still up 10.1% year over year.). Other highlights from the report:

- Food costs were up 0.5% for the month, continuing a string of sharply higher monthly price reports. Food at home costs are now up 12.0% year over year.

- The index for fruits and vegetables increased 1.4% in November, after falling 0.9% in October. On the positive side, the index for meats and poultry fell 0.2% for the month.

- Apparel costs were up 0.2% for the month and 3.6% for the year.

- The costs of medical care services fell 0.7% for the month.

- Costs for used cars and trucks fell for the fifth month in a row, down 2.9% for the month and 3.3% year over year (after rising sharply in 2021).

- Costs of new vehicles held stable, but are up 7.2% year over year.

- The index for airline fares fell 3.0% over the month, following a 1.1% decrease in October.

Overall, this was a positive inflation report, with the one exception of food prices, which are continuing to increase at a brisk pace. The cost of shelter, also higher, is considered a lagging indicator of past price increases rolling into effect. Shelter costs could eventually begin to fall in 2023.

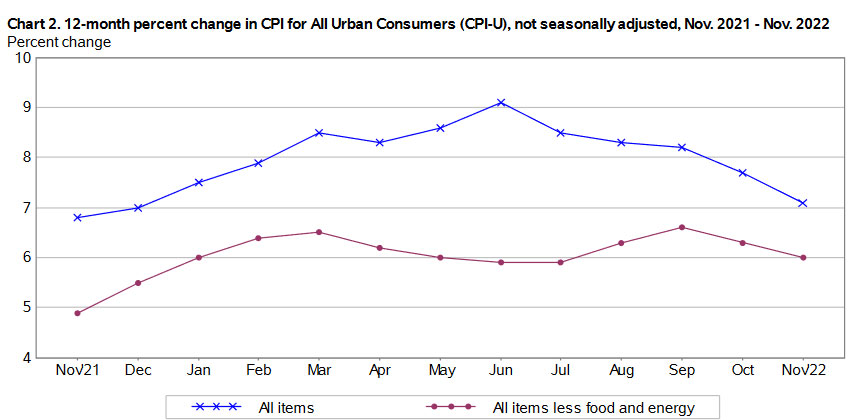

Here is the trend in all-items and core inflation over the last 12-months, showing the consistent declines in all-items inflation since early summer, drawing closer to core inflation as gasoline prices have declined:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates on I Bonds. For November, the BLS set the CPI-U inflation index at 297.711, down 0.1% from October.

For TIPS. The November report means that principal balances for all TIPS will decline 0.1% in January, after rising 0.41% in December. However, TIPS principal balances will have increased 7.1% for the year ending on January 31. Here are the new January inflation indexes for all TIPS.

Today’s report is sending real yields down sharply, which could affect the Dec. 22 reopening auction of CUSIP 91282CFR7, which two months ago auctioned with a real yield of 1.732%. This morning that TIPS is trading on the secondary market with a real yield of 1.27%.

For I Bonds. The November report is the second in a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on May 1 based on inflation from October 2022 to March 2023. As of November, inflation is up 0.3%, which translates to an variable rate of. 0.60%. But it’s far too early to say where inflation is heading over the next four months. Here are the numbers:

What this means for future interest rates

The U.S. stock market is set to open sharply higher in a few minutes, a predictable response to this inflation report. And in the bond market, yields are sharply lower. All of this is anticipating that weakening inflation will allow the Federal Reserve to gradually stall future increases in interest rates. I think the Fed will go ahead with a 50-basis-point increase tomorrow, but give dovish signals about future rate increases.

It’s impossible to say at this point that inflation has truly been “tamed,” but we will now be entering a phase where year-over-year comparisons should cause inflation to continue declining. In January 2022, non-seasonally adjusted inflation increased 0.84%; in February 2022, 0.91%; and in March 2022, 1.34%. It’s unlikely U.S. inflation in future months will match those numbers, so year-over-year inflation should continue to decline in early 2023.

The Federal Reserve appears to have a path ahead that will allow it to hold short-term interest rates near the level it announces tomorrow.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Fantastic site. Many thanks for your hard work…

Still trying to understand TIPS… one thing that is confusing to me is the significant spread in real yields for TIPS that have roughly similar maturity dates. When I look at the WSJ summary for today (12/29/22), I see that a 2027 Jan 15 maturity is trading with real yield of 1.807 while an October 15 maturity is trading with a real yield of 1.613.

I guess that in the event of deflation, there is less potential downside for bonds that have a lower inflation index (generally those issued more recently). Aside from this, is there something else going on here ? If I do not care about Jan 15 2027 vs October 15 2027 maturity, is there some other reason I might purchase the lower yielding maturity ?

There is some logic to this pricing, as you noted. Some investors shy away from buying additional accrued inflation, so the demand is lower and the yield is higher. There are two TIPS maturing in Jan 2027 and both have sizable inflation accruals, 23% and 48%. One of them has a coupon rate of 2.375% so it is selling at a premium price. The one with the coupon rate of 0.375% and the lower inflation accrual has a real yield of 1.802% — that looks like a “relative” bargain.

the tips auction is december 22. what day will treasury direct take the money out of my bank savings account to pay for my tips purchase?

The settlement date is Dec 30

Well, it certainly was a strange day today. The stock market actually finished down a tad today.

The 10/15/27 TIPS yields went-up from 1.34% yesterday to 1.43% today before closing back down to 1.35%.

The 4/15/27 TIPS yields went-up to 1.55%. So, I bought what will probably be my last batch of that maturity date.

Since I was expecting yields to crash after the FED meeting, I was pleasantly surprised.

The conundrum that I have now it that I’d like to purchase some 2028 TIPS maturities next year.

However, April is a long time off and if there’s a recession leading up to that auction that should put the final nail in the coffin for 2028 TIPS yields.

The other option is to purchase some of the other TIPS maturities that are selling with an inflation adjusted price near par.

A 2031 maturity TIPS was going for a little over $101 today. So, I’d only be out around 1% if deflation lasted for neary 9 years.

A 2026 maturity TIPS was going for over $103. That would have more exposure to deflation because of the shorter term of around 4 years.

Both of those TIPS maturities still have yields over 1%. With things the way they’re going that might not last too much longer.

Another strange day in the strangest year for Treasurys in history. I’ll probably buy a bit more of the 5-year reopening on Dec. 22, but I really would like to lock down a 10-year maturing in 2033, coming in January. I think rates “should” hold up reasonably well until then, but nothing is certain.

Hi David.

Thanks for all your articles about I Bond and TIPS . Can you please give me your opinion about the coming up 10 years TIPS? I am very naive with TIPS. I bought my first one (5 years TIPS) in October after I read your article and thanks. What is the real for you to buy it. I plan to hold it until mature and it will be in my regular act.

Thanks,

PHuynh

It’s too early to have a strong opinion and the bond market is very volatile right now. It’s a new issue. At this point, the real yield would be 1.35%, which I would buy. Let’s see what happens next month. The auction is Jan 19.

Thanks David.

I have read some very strong arguments for inflation not getting down near to the Fed’s target range of around 2%, and rather leveling off at around 4% after a year or so. The arguments, too deep to mention here, get into macro-economic factors (as far as we know them today). Shades of 1980 stagflation but extended. The 10 year breakeven is currently 2.19% and the 5 year breakeven is 2.25%. I am therefore in for the upcoming 5 yr TIPS auction. I’ll also pick up a paper I bond at refund time, then 3-6 month notes over the next several months.

I am also in the camp of inflation falling into a range of 4% to 5% by the end of 2023, but probably being stubborn from then on. Inflation breakeven rates do look unrealistic, but I’ve learned I can’t predict future inflation. I just expect it and plan for it.

Long time reader – love the blog!

Please check my logic…. my TIPS allocation is fully utilized, however there is a large batch of 5 year TIPS maturing 4/15/23 held in Fidelity tax advantaged account. Thinking of selling some of those now to fund the upcoming 5 year TIPS auction to move the maturity date out to 2027. Other than the buy-sell spread, would I be leaving any money on the table to sell now rather than wait for the maturity?

I like the idea, but I’ve never sold a TIPS on the secondary market and can’t say what sort of bid/ask spread you would face. Would there be a commission on that sale? That TIPS (which I also own) is selling at a discount (which you could capture by holding), but it probably wouldn’t make a huge difference.

No commission. Fidelity is quoting a “3rd party price” of 98.930. Depth of book is showing 98.875 (4.051 yield) bid and a 99.011 (3.632 yield) ask. Moving forward to the preview page shows a 98.843 price and a 118.326 inflation-adjusted price (inflation factor 1.197110). Executed.

Imagine we have 0% inflation for decades, then 10% inflation for one year, then 0% inflation again for another several decades.

After the one year of inflation, a lot of people are going to find themselves ‘behind the curve’… they are now living in a new world with 10% higher prices, even though the official inflation rate is now zero.

What will their reaction be? They will likely push for increased wages, or cut consumption, or both, until their budgets balance again.

In other words, there will be an ‘inflation hangover’ even if the Fed gets the rate down to target relatively quickly. How long will that last, and what will the effects of that be?

Wall Street? ” A huge asteroid is headed for earth, expected to extinguish all life on the planet. This is a good time to buy stocks and average down!”

Any thoughts about sequence risk as it applies to realized inflation?

My thought is that inflation is painful, especially for retired people who have limited resources to compensate. So incorporating inflation-protection into your portfolio is a wise move, especially when real yields are positive, as you can find now with both I Bonds and TIPS.

Has today’s drop in the five year real rate to 1.29% changed your view of the upcoming auction on 12/22?

At what level would you not participate?

No, probably not. One issue will be that this TIPS is going to auction at a premium price, right now about $101.62 for $100 of par. Inflation accruals won’t be much of an issue, though.

Hi David,

This statement confuses me:

“The November report means that principal balances for all TIPS will decline 0.1% in January”

I thought principal balances only decrease if there is deflation. In this case there is only a reduction in inflation, ie. disinflation, but not deflation, so shouldn’t that just mean a reduced increase in the principle rather than a decrease in the principle?

thank you

Remember that TIPS inflation accruals are based on non-seasonally adjusted inflation, which was down 0.1% in November, even though seasonally adjusted was up 0.1%. These numbers balance out over the year.