Data for three months indicate the I Bond’s variable rate could fall to 0.0%. What does it mean for investors?

By David Enna, Tipswatch.com

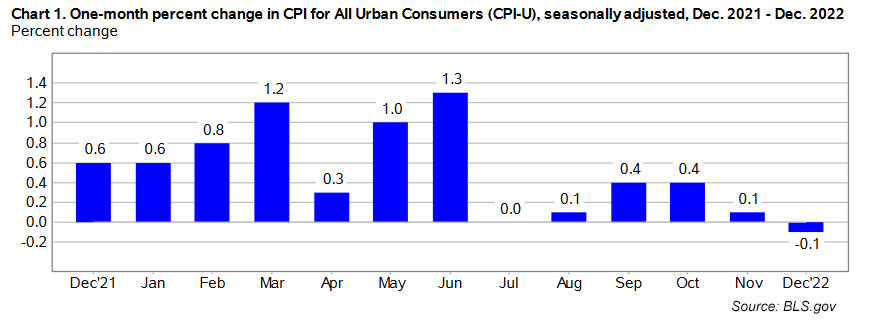

U.S. inflation transitioned to deflation in December, with the all-items Consumer Price Index for All Urban Consumers falling 0.1% for the month, after increasing just 0.1% in November, the Bureau of Labor Statistics reported today. Inflation for the year 2022 ended at 6.5%, falling below 2021’s 7.0%.

All-items inflation was below the consensus estimates of 0.0% for the month and 6.6% for the year, but more recent projections cited -0.1% for the month. Core inflation, which removes food and energy, ran at 0.3% for the month and 5.7% for the year, matching expectations.

So these numbers aren’t really much of a surprise. Expectations of easing inflation had sent the U.S. stock market surging higher — and Treasury yields falling — over the last two weeks. The S&P futures were up just slightly at 9 a.m., indicating a lack of euphoria (at least so far).

The BLS noted that gasoline prices, which fell 1.5% in the month, were the largest factor in the all-items index moving negative. Gasoline prices are now up just 0.4% year over year. More items from the report:

- Food at home prices were up 0.2% for the month and 11.8% for the year. The index for meats, poultry, fish, and eggs increased 1.0% in December, but costs of fruits and vegetables fell 0.6%.

- Shelter costs rose 0.8% for the month and were up 7.5% for the year. Shelter tends to be a lagging index, with leases rolling over gradually. Rents were up 0.8% for the month.

- Apparel costs rose 0.5% for the month but were up just 2.9% for the year.

- Costs for used cars and trucks fell 2.5% for in December, the sixth consecutive month of declines. New vehicle prices also fell by 0.1%.

- The index for medical care services rose 0.1% for the month, after declining the two previous months.

This report presents positive news on U.S. inflation, but a lot of the December decline was due to falling gasoline prices. Food prices also moderated. Both of those factors are welcome for U.S. consumers. Shelter costs continued moving higher, but that was expected with higher rent costs rolling into effect. Clearly, U.S. housing prices are at least at a standstill with mortgage rates nearly doubling over the last year.

This disinflationary trend could continue for several months, because last year’s CPI numbers were quite high from January to June, making month-to-month baseline numbers hard to exceed. Even if monthly numbers rise, annual inflation should be declining in the first half of 2023. After June, inflation could pick up again, but that’s a long way off:

Here is the one-year trend for both all-items and core inflation over the last year, showing the dramatic fall in all-items inflation since June, and more recently the gradual fall in core inflation:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For December, the BLS set the CPI-U index at 296.797, a decline of 0.31% from the November number. Over the last year, non-seasonally adjusted inflation has increased 6.45%.

For TIPS. The December inflation report means that principal balances for all TIPS will fall 0.31% in February, following a decline of 0.10% in January. But over the last year, ending in February, principal balances will be up 6.45%.

Take for example CUSIP 912828WU0, a TIPS that matures July 15, 2024. Its inflation index will start the month of February at 1.25381 and end the month at 1.25009. This isn’t great news, but it is how TIPS work, tracking official U.S. inflation. Here are the new February Inflation Indexes for all TIPS.

For I Bonds. The December report is the third in a six-month series that will set the I Bond’s new inflation-adjusted variable rate. The reset will be on May 1 for I Bonds purchased from May to October 2023, but eventually will roll into effect for all I Bonds. Through December, inflation has run at 0.00%, meaning the I Bond’s new variable rate would be 0.00%, down dramatically from the current 6.48%. Here are the numbers:

Three months remain, and a lot can happen in three months. But as I noted earlier, the very high baseline numbers from 2022 indicate that disinflation, or deflation, could continue through June. But those baseline numbers really only effect the annual rate; the month-to-month inflation rate could move higher from January to March, but we are still likely to see a lower variable rate at the May reset.

For regular I Bond investors, this points to purchasing your 2023 I Bond allocation — $10,000 per person per calendar year — before May 1 to lock in the current 6.89% for six months, which includes the fixed rate of 0.4%. For short-term I Bond investors who bought in 2022, the next variable rate could give you an exit window with a very low three-month interest penalty.

See my recent post: I Bonds: A not-so-simple buying guide for 2023

And also: Short-term I Bond investors: Be patient with your exit strategy

If this disinflationary trend continues for several months, investor interest in I Bonds and TIPS is likely to wane. In fact, short-term investors should probably look at attractive nominal investments like a 1-year Treasury bill at 4.73%. But clearly we can’t be certain that the inflationary monster has been tamed in the long run.

What this means for future interest rates

The Federal Reserve seems highly committed to raising short-term interest rates by 25 basis points in early February, pushing the federal funds rate to 4.50% to 4.75%. Could that be the last rate increase? More likely, the second-to-last rate increase?

This morning’s Bloomberg report has this headline: “US Inflation Cools Again, Putting Fed on Track to Downshift“. Plus, rather comically, “Stocks Drop as In-Line CPI Fails to Sustain Rally“.

I have been theorizing that the Federal Reserve has been issuing hawkish public statements over the last month to try to cool market fervor over a stall — and then potential cuts — in interest rates. The bond market, though, hasn’t been listening, with mid- and long-term nominal and real yields falling in recent weeks.

I think we are nearing the end of this rate-hiking cycle. But the Fed has to continue to slash its massive holdings of U.S. Treasurys, and that roll-off or even sell-off should elevate bond yields, eventually. The unknown factor is the health of the U.S. economy and job market. If a recession hits with a vengeance, the Fed will back off, quickly and somewhat aggressively.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am wondering what impact you foresee from the BLS changing the way CPI is calculated for January (reported in February). I am hoping you will have an article about that.

I knew that this is coming, but I haven’t seen details. This is a routine change, but in the past has been made bi-annually and now will be made each year at the January report.

Nice article David. TIPS are new to me also. I read in another article that TIPS value adjust daily. How does this work & where can I find more information on it & how to track it? My broker sold me some TIPS. It sounded like it made sense at the time, but I really don’t know how they work.

I have two resources that will help. 1) my Q&A on TIPS: https://tipswatch.com/why-tips/ and 2) TIPS In-Depth: https://tipswatch.com/tips-in-depth/ …. The daily inflation adjustment is based on nonseasonally adjusted inflation two months earlier. The Treasury uses the CPI index for that month to set daily inflation indexes for TIPS. This way, TIPS always have a current accrued principal and can be traded with that amount known.

Hi David, I too am a long time I Bond buyer and enjoy seeing their value never go down. I bought a five and ten year TIPS in Fall ’21 (ouch) in a brokerage account and feel the pain whenever I check my account. I know holding to maturity ensures return of principle, but am wondering…

If I buy a TIPS in Treasury Direct, would it mark to market throughout it’s life like they do in my brokerage account? How about non-inflation treasuries bought the same way?

Thanks, Mike

No, TreasuryDirect does not show a market value for your TIPS holdings, and you cannot sell your TIPS at TreasuryDirect. It will show an inflation-adjusted value, but only as of the last compounding date. So there can be a several-month lag time. Pretty weird and not super helpful. But it does show the original price per $100 you paid, which is sort of helpful. Same with regular Treasuries.

Thanks – good to know

It’s an artifact of the I-Bond formula that is actually is better to have 8% annualized inflation in one six month period and 2% annualized deflation in the next period rather than a constant 6% rate during the 12 months. If there is any deflation (unlikely but possible) it will definitely be an opportunity to exit.

I think you intended the six month to go from 8% to 4%, not 2%. The average of 8% and 4% seems like it would give a yearly average of 6%, but in fact two 6% periods is slightly better than an 8 followed by a 4. 8 followed by 4 is equal to a period of 4 followed by 8, but is less than two periods of 6%.

Most people get their raises in the first three or four months of the year. Do you think this might push the CPI higher than expected?

It could, sure. The Fed has been worried about wage increases. Also consider that Social Security recipients received an 8.7% increase starting in January. But I doubt these will be a major factor in the near term.

Assuming the variable rate goes to zero percentage for the I-Bond, what’s your insights for the upcoming 10-year Tips? Thanks.

The I Bond variable rate is unrelated, but the declining inflation rate and optimism about a Fed pivot is driving the 10-year real yield down, fairly dramatically. The most recent 10-year TIPS is now trading on the secondary market with a real yield of 1.22%, down from 1.485% at the most recent auction.

It would be like holding 100 bills unless you have a fixed rate for the six months until the next reset. It would possibly be a good time to take a 3 month penalty on the zero variable rates (if you have a zero fixed rate) and wait until the next reset or even just buy into the .40 fixed rate bonds if you can afford to pay the tax on the interest on what you cash in. I am sure David will discuss the options in depth.

What happens if I-bonds go to 0.0%? Is that the same as holding cash then, over the life of the bond? Newbie here, so just wondering. Thanks!

If the variable rate goes to 0.0%, and the I Bond has a fixed rate of 0.0%, then the composite rate will be 0.0%. But that is only for six months. I Bonds purchased this year, through April, have a fixed rate of 0.4%. So if the variable rate goes to 0.0%, those I Bonds will have a composite rate of 0.4%.

Thank you for all of your posts and insights. I’m also a newbie here, so I wanted to confirm my understanding. If the May variable rate is set at 0%, that I’m guessing for those wanting to redeem before 5 years, it may make sense to hold for long enough such that the last 3 months worth of interest will be 3 months of 0%, depending on which month they were purchased, is that correct?

Correct. I am expecting a lot of the new I Bond investors who came in for the 9.62% rate will be looking for an exit. A low variable rate would give them that opportunity, but it will require holding the I Bond 15 months from the month of purchase. If you bought in October 2022, as many did, the exit month would be January 2024. See this: https://tipswatch.com/2022/11/06/short-term-i-bond-investors-be-patient-with-your-exit-strategy/

If the inflation is negative (deflation), say -0.2%, does that eat into the bonds fixed rate, if it has a fixed rate?

The fixed rate is what it is. The -0.2% variable rate would combine with the fixed rate to get you the composite rate (which can never go below 0). To answer the question I think you meant, a negative variable rate can offset the positive fixed rate to leave you with a composite rate of zero.