By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer $19 billion in a reopening auction of CUSIP 91282CGW5, creating a 4-year, 10-month Treasury Inflation-Protected Security.

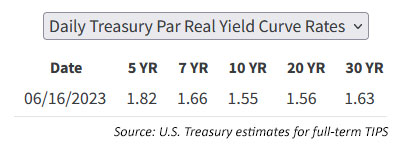

This TIPS had its originating auction on April 20, 2023, when investors got a real yield to maturity of 1.32%. Its coupon rate was set at 1.25%. CUSIP 91282CGW5 now trades on the secondary market and at the close Friday it had a real yield to maturity of 1.81% and a discounted price of $97.43 for $100 of value.

If the real yield holds above 1.8% through Thursday’s auction, it would be the highest auctioned real yield for a TIPS of this term since October 2008.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or below) inflation.

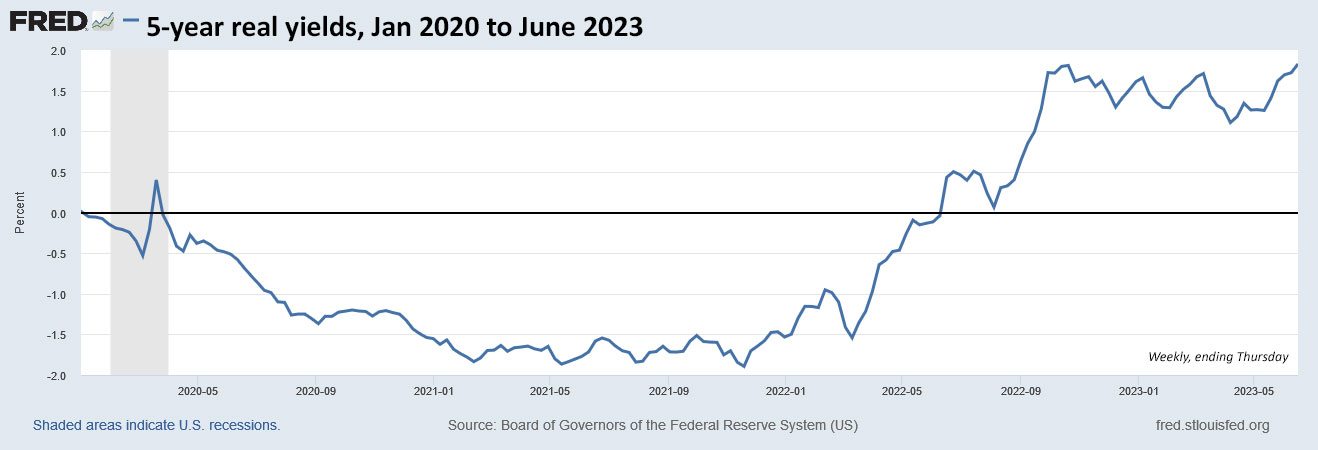

This TIPS looks attractive, in my opinion. I was a buyer at the originating auction and the real yield has risen strongly since then. The 5-year real yield — which is the most sensitive to Federal Reserve rate increases — is now the highest across the TIPS maturity spectrum:

This chart shows how far we have come over the last three years, moving from dreary days of deeply negative real yields to 14-year highs. Just 2 years ago, in June 2021, a similar 5-year TIPS reopening got a real yield of -1.416%.

Pricing: On the settlement date of June 30, this TIPS will have an inflation index ratio of 1.01121, which means an order for $1,000 par would actually be purchasing $1,011.21 of principal. At the discounted price of 97.43, that would mean the investment cost would be $985.22 for $1,011.21 of principal. Plus the investor would pay an additional $2.62 per $1,000 for accrued interest. This will change by Thursday, but it does give you a rough estimate.

Inflation breakeven rate

With the nominal 5-year Treasury note trading with a yield of 3.98%, this TIPS currently has an inflation breakeven rate of 2.17%, a number I consider stunning. Investors are saying that inflation over the next 4 years, 10 months will average 2.17%? Seems mighty optimistic. If you think inflation will be higher, this TIPS is attractive, at least versus a nominal Treasury of the same term.

U.S. inflation is currently running at an annual rate of 4.0% and has averaged 3.9% over the last five years. Here is the trend in the 5-year inflation breakeven rate over the last three years:

What about bank CDs?

You can still find best-in-nation 5-year bank CDs paying 4.5% or even a bit higher. That stretches out the breakeven rate to about 2.7%, which seems more plausible. If you don’t care about inflation protection, bank CDs remain an attractive option.

What about I Bonds?

U.S. Series I Savings Bonds currently have a fixed rate of 0.9% for purchases through October. That fixed rate is equivalent to the real yield of a TIPS, and the 5-year term is an option for redemption without penalty. But a 5-year TIPS with a real yield of 1.81% is more attractive than an I Bond at 0.9%, looking purely at investment returns. I Bonds have other factors — simplicity, better deflation protection and flexible maturity date — that make them attractive. I invest in both.

Final thoughts

My TIPS ladder is already loaded with maturities in 2028. but I think I will add another purchase of CUSIP 91282CGW5, if real yields hold up next week. (Financial markets will be closed Monday for the Juneteenth holiday.) Most likely I will buy at the auction, but if I see a good price mid-week on the secondary market, I might grab it.

Keep in mind that a new 10-year TIPS will be auctioned July 20, and that one also looks like it will be worth strong consideration.

Thursday’s auction will close at 1 p.m. EDT and I will post results soon after. If you are considering bidding at Thursday’s auction, I suggest you keep an eye on Bloomberg’s Current Yields to track the yield trend. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

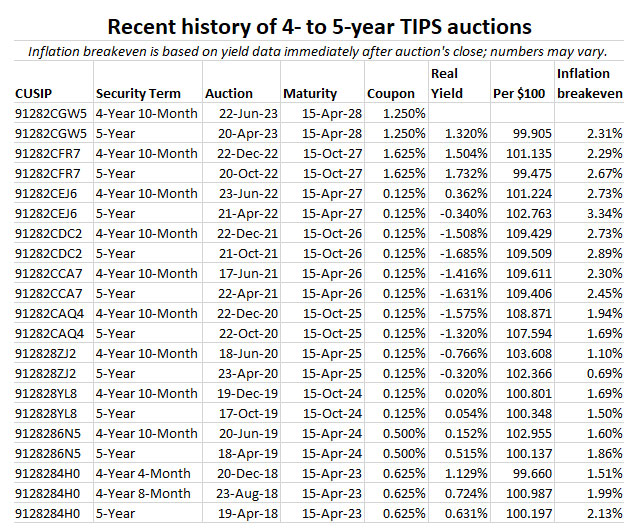

Here is the recent history of 4- to 5-year TIPS auctions, showing the transition from deeply negative real yields, beginning just a year ago:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I was on the treasury direct website and trying to figure out what the penalty would be if I redeemed I Bonds I purchased in November 2021 and January 2022. If the penalty is the last 3 months of interest, if held less than 5 years, is there a way I can be assured of the penalty being the 3.38% rate – I need to know when the rate dropped and then wait 3 full months? The lower rate of 3.38% is being displayed for the November 2021s, but on the January 2022s. it’s still 6.48%. I was hoping that when I clicked the “Redeem” button it would show me a preview of the penalty, but it didn’t. Is there a tool somewhere or method that can be used to calculate the penalty?

A few things:

Each individual bond changes rates every six months from when you got it. So the 11/21 bond changes rates every November and May; the 1/22 changes in January and July.

The value displayed for the bonds on TD includes the penalty where appropriate.

The website eyebonds.info has very useful tables showing the value of any given bond in any month. These tables DON’T include the penalty, so if you’re redeeming a bond early, just back up three months (i.e. right now, you would look at the March value).

Thank you. That makes sense now, and I believe the interest displayed on the TD site is delayed by 3 months….recall looking at it and not noticing an interest for 3 months. I’ll bookmark the eyebonds.info. Thanks again!

If you purchased in November 2021, the new 3.38% variable rate went into effect on May 1 this year. But since the penalty is the most recent 3 months of interest, you will want to wait until August 1, 2023 to redeem. I Bonds purchased in January 2022 are still paying the 6.48% variable rate through July 1, so wait until October 1 to reduce the interest penalty.

TreasuryDirect always includes the 3-month interest penalty in the current value of the bonds for the first 5 years. Use this link (http://eyebonds.info/ibonds/index.html) to see the current value of your I Bonds based on amount and purchase date. The actual redemption value (with interest penalty) will be the value of the I Bond 3 months prior to the current month for I Bonds redeemed before 5 years.

Thank you, that website is helpful, and sounds like I’m looking at Aug 1 and Oct 1 for the lesser penalty. And yes, I’m seeing the Mar 1 value currently on the TD site, so it’s reflecting the penalty. Thanks!

I wrote on this topic back in March: https://tipswatch.com/2023/03/29/want-to-exit-your-i-bond-investment-youd-better-have-a-plan/ That article summarizes ways to tell the optimal month to redeem I Bonds, especially if you face a 3-month interest penalty. You are correct that TreasuryDirect will not show you the last three months of interest until you have held the I Bond 5 years.

I remember that now, and was trying to find it. Thank you, and it even has the “Ideally, the earliest time to redeem will be Aug. 1, 2023.” for the Nov 2021 buyers. As to the rest of the article, I’ve got to think about whether I truly want to sell, but I’m attracted to the higher rates on other treasuries (6 month – 2 year, maybe 5). Maybe I’ll compromise and sell half.

I enjoy your site and look at it frequently. It’s a great resource for me. Thanks again.

Buying Thursday . Should return 5-6 %.

Mr. Enna, my wife and I are big TIPs investors, but have recently gifted about $133,000 in 0.9% I Bonds to cover our bets for unknown yields for the current gap of 2035-2039 maturing TIPs, and we can sell them and buy the TIPs of that period if the yields turn out okay then. We still have around $188,000 in shorter term TIPs to sell to finish out our I bond ladder with gifting up through 2039 on Treasury Direct. Do you foresee a possibility of even higher I Bond yields in November, and possibly a heads up before the October purchase deadline of the new yield for November (like they did in April), to justify us holding out and not selling our TIPs and gifting the rest of the I Bonds until then, with a new, higher yield?

At this point, I’d say the fixed rate should at least hold at 0.9%, but we are a long way off from November 1. I’ll be using the gift-box strategy later this year, too, but probably in October. Whatever fixed rate we get in November can be purchased in January in the traditional way. My strategy with I Bonds: I won’t hold all of them to maturity, and will begin using some of them eventually for cash needs. My first paper I Bonds, purchased in 2001, will mature in 2031 so there will be a flood of taxable cash in that year to deal with. After that the next maturity is 2043, when I will be 90 years old. So some of the 0.0% fixed rates will be redeemed early.

Thank you for your quick response. Those 2001-2003 era I Bonds were the good old days, were they not? I have $58,000 of 2001 I Bonds at 3.4%, and $225,000 in 2-3% 2001-02 I Bonds that mature then. I redeemed my earlier 0% ones to bankroll the 0.9% giftings originally. I Bonds do make a nice use of emergency cash that keeps up with inflation and not subject to interest rate discounting when selling anytime, as that is an issue with my 2026-2028 TIPs that I want to sell to finance the rest of the gifting (if it is as you think and the November yield will at least hold steady, there isn’t much risk in waiting, even until next April!). I think its a great way to provide an inflation-protected staging area to later sell and buy later 2035-2039 TIPs which have a hole currently, and to keep if their TIPs yield drops like a rock by then. As people become “normalized” to higher inflation and fed reserve rates and mortgage rates (which the fed does not want to set in), maybe the era of 1%+ I Bonds will return (probably not). One thing that probably won’t come back is that earlier era of $60K/person I Bond purchases per year!

Hi David,

As always THANK YOU! Could you tell me how much it would cost to buy 15k of the 5 year reopening?

Take care

Looking at your post:

$985/$1011.21 x $15000 + $2.62 x 15 = $14653.77

Yes?

At this moment that TIPS is trading at 97.27, but that could change tomorrow. So right now, at least, you’d be buying $15,168 of principal x .9727 = $14,754 + $39.30 accrued interest = $14,793.30. That’s the estimate, but the auction won’t have that exact result.

And if held in a taxable account, that would be an OID of $414, to be included on this year’s tax return? Sorry, still trying to get my head around this!

No, the inflation accruals from the settlement date on would be reported on your tax return.

Thanks! I can see why many folks prefer to hold these in tax-deferred accounts.

David, thanks for the helpful post. Do you think this week’s attractive yield is the highest we’ll see on the 5-year TIPS this year? I definitely plan to buy, but am debating whether to hold back some funds in case the October or December auctions climb higher. On the other hand if yields start to fall, I think bank CDs will remain competitive for a while longer. I agree that even a 2.7% inflation breakeven with CDs is low (and expect inflation to average at least 3% over the next five years).

No way to know. If the Fed raises short-term rates two more times, we could go higher. But real yields have been volatile all year.

Just wondering because i am a novice, but what happens to the value of the 5 year tips if inflation drops from the current 4% to 3%? Does the value decrease or increase?

If inflation falls, the nominal return you receive will go down, but you are still getting 1.8% above inflation until maturity. If real yields start falling, then the value of the TIPS will increase, but that won’t matter if you are holding to maturity.

Tuesday update: Unfortunately, on Vanguard’s platform today secondary market purchases of 91282CGW5 require a $100,000 minimum investment. (Current real yield is 1.81%.) This seems to happen often with newly issued TIPS.

At Fidelity:

Min 10

1.774%

97.586

1.00968

And at Schwab

Min 5 (3,000 available)

1.781%

97.558

1.00968

For those folks (myself included) who bought their annual allocation of I Bonds early in 2023, only to experience buyer’s remorse upon missing out on the 0.9% fixed rate that started May 1, this week’s reopening auction of the 5-year TIPS is indeed very attractive: high real yield, low breakeven. Moreover, it offers the chance to correct that “mistake” — while getting a real yield that’s twice as high, and without having to resort to the gift box strategy or other workarounds for I Bonds. I plan to buy my first TIPS at the Thursday auction. Many thanks to David and other readers’ comments for teaching me how to evaluate TIPS and their auctions.

You can always buy additional Ibonds in October for the 0.9% fixed rate in your/your spouse’s gift boxes.

Of course, not everyone has a spouse or a trusted partner to do the gift-box swap.

Thanks for these enlightening posts! I’ve had way too much cash sitting around for several years waiting for the next bear market, which I thought was imminent. When inflation picked up I realized I should put it to work. I always thought fixed income investments were boring, but this world is amazingly complex. I have a T-bill maturing next week that I was going to invest 1/3 in TIPS and 2/3 in another short term T-bill, but now I am thinking I should put 2/3 in TIPS.

I was in the same state of mind until last year when the yields bacame interesting. Luckily, I got into buying US Tresuries at auction and took all my cash out of banks. TIPS is a step higher in complexity but manageable. Real yields will not last for long so TIPS represent a good diversification in addition to nominal Treasuries.

So does the coupon rate of a TIPS represent profit in a sense? That is, will the TIPS eventually return a gain generated by inflation, or a loss from deflation, and then added to that is the coupon rate?

The coupon rate is part of the equation that determines the real yield to maturity, so in non-deflationary times it is just part of the total return. But if severe deflation set in for years, the TIPS is guaranteed to return par value at maturity, so the coupon rate will be on top of that and it does provide additional income (but this is a highly unlikely case).

Thanks. I have a small order for the Thursday reopening for my Rollover IRA. That seems to be a good place to hold some TIPS.

At the time of posting this, the 5 yeas TIPS 92182CGW5 on Schwab is available in the secondary market with the following terms:

Price — 97.617

Current Yield — 1.281%

Yield To Maturity — 1.768%

Inflation Factor — 1.00968

Inflation-Adjusted Price 0 98.561933

It is David’s fault in helping me start getting the hang of TIPS.. before you know it, I may even start picking good deals…..thanks!!!..:)

For the same above, Vanguard has the real yield of 1.81% while Fidelity has 1.788%…..interesting, Schwab is the worst of the three.

I doubt there is much TIPS trading going on because of the Federal holiday. Tomorrow should provide a better update.

I was thinking the same. Also, different platforms, perhaps, update their systems at different times. However, I am going to monitor if there is a hint of different markups, afterall it is a secondary market.

Hi David Thanks for your posts.

Perhaps you have explained this before but I can’t find it. If you own a S1000 5-yr TIPS bought 04/2023 it pays interest on 10/2023 on a principal on $1000? So what happens with the reissue of June 2023 of the same TIPS? Does it pay interest in December? or in June 2023?

The coupon payments stay on the existing schedule. So if the TIPS was originally issued in April, the coupon payments will be Oct 15 and Apr 15 of each year. When you buy a reissue or a TIPS on the secondary market, you prepay the interest earned up to that point of the six-month period, and then the money is returned to you on the next coupon payment date.

Joing the wishful thinking celebration, I believe the days/years/decades of ultra low inflation where the fed failed to reach even 2% inflation in the recent past are behind us. With globalization (cheap labor) delivering deflation gone, high US debt, continued sporadic supply chain interuptions due to Ukraine war, etc. will make 3-4% inflation as the new normal. Fed just needs to accept that in 2024 or 2025. So, for the next 4-5 years, 5 year TIPS should do just fine, worst case, we will at least get ouf principal back. Every wishful thinking has some (il)logical narrative to support it…. :0)

Hi David, what is the best process, at a high level, to find TIPS in the secondary market. Since I am relatively new to your blog, you may have already covered this. I may not be even asking the right question. I have accounts with Schwab, Fidelity & Vanguard. For exmple, I do know how to get available TIPS listing on Schwab. I can sort the list by increasing or decreasing YTM, etc. not sure how best to identify a good opportunity because there is no real yield listed…thanks!!!

Each platform is different. I have never used Schwab, so I can’t say anything about that. I do use Fidelity & Vanguard, but the account where I buy TIPS is at Vanguard. (Fidelity has better information on its site, in my opinion.) I’d suggest clicking around. You definitely should be seeing real yields, but they are probably called “yield to worst” or “yield to maturity.” Vanguard disables a lot of the functionality when the market is closed.

Schwab is better than Fidelity IMHO

On Schwab.com, the number listed in the YTM column is the real yield. If you open the detailed quote page for any listed bond (by clicking on the name of the bond in the “Description” column of the search page), at the bottom of the Quote Details on the right side you will see “YTM values displayed include the inflation index factor and assume a zero future rate of inflation.” I.e., the YTM is the yield to maturity if there is no further inflation after the date of the quote. This is real yield.

Thanks to you & David…..I agree that Schwab platform is better than Fidelity which is better than Vamguard. With the aquisition of Ameritrate by Schwab and adding Think or Swim platform capabilities should make the Schwab platform closer to the Bloomberg terminal, in terms of financial data access. Looking forward to playing with it…..best!!!

TOS is great. Worried Schwab will screw it up like they did CyberTrader.

Bird in the hand vs two in the bush?

Given the high real yield, why wait until Thurs’ auction when you can probably buy it close to the Fri. close in the secondary market tomorrow?

Please explain.

You won’t be buying tomorrow, since markets are closed Monday. If you see a yield Tuesday you like on the secondary market, go ahead and buy. The auction could be worse, it could be better. The one big benefit for buying at auction is that you get the same high yield that the million dollar bidders get. That’s not the case in the secondary market. I fine with buying either way and not looking back.

David: How do you get to the $2.95. Sorry if this is stupid question but we are new to TIPS.

I see that you are pointing out a typo, which is corrected. That calculation is done by the Treasury and is shown on the auction announcement: https://www.treasurydirect.gov/instit/annceresult/press/preanre/2023/A_20230615_4.pdf

Will the Sep 21th 10YR TIPS (reopening) be the Jul 20th 10YR TIPS?

Thanks

Check the Cusip number: it should be the same,

but this should make it clear. ….”10-year TIPS are usually announced mid-month in January and July. The reopenings of 10-year TIPS are usually announced mid-month in March, May, September and November”

Yes, the new TIPS being auctioned in July will be reopened in September and November.

I am buying a substantial amount, for me!(5-6K ) this Thursday and to simplify things I will use a non-taxable account.

David, there’s a small typo in the first sentence of the second paragraph: the originating auction date is stated as April 20, 2022, but should be 2023. The spreadsheet at the bottom of the article correctly gives the auction date as 2023 (but for some reason says 4/28, rather than 4/20; the April 2022 auction date is also given there as 4/29, rather than 4/21.)

Thanks for catching this. I have made repairs.

Sure would be helpful if someone could quote an equivalent YTM at least historically to date of these kind of issues. I must be too stupid to comprehend how to compare these apples to the oranges of other Treasuries. Interesting that people are willing to take the risk of deflation in buying this product.

I track performance of matured 5- and 10-year TIPS on this page: https://tipswatch.com/tips-vs-nominal-treasurys/ …. In general, you want nominal investments at good yields in a time of deflation and you want inflation protection with good real yields at a time of high inflation.

Thanks

Also you can find YTM data for all matured TIPS on eyebonds.info. For example, here are data for the 10-year TIPS that matured July 15, 2022, which ended up having a nominal YTM of 1.719%. However, a 10-year Treasury note issued the same month had a return of 1.54%. http://eyebonds.info/tips/hist/tips46hista.html

“Interesting that people are willing to take the risk of deflation in buying this product.” Every investment has some type of risk; every single one. Not investing has risk too. Since no one knows what lies ahead, I believe the best approach is to be diversified (holding a variety of assets that should do well under different conditions) in the hope that at least some of your assets will do well enough so that you can get by.

Of course there is a risk of deflation, but the breakeven inflation point of 2.17% look profitable (to me at least). I mean, inflation might get down for a while to 2% eventually yes, but along 4 years and 10 month as average seems…

And even in the worst case, some part of your portfolio has to be inflation protected to be truly diversified. (IMO)

Yup. I agree. Just hard to get my head around it. Plus who knows what the idiots in charge will do. You’d think they will inflate their way out if this but who knows.

The average inflation rate (Sept 98-Today) for the Ibond including the negative values and the most recent highs was 1.23%. The number of times that the Ibond 6 month inflation rate was below 1 is 20/50.

Who knows where we are heading, but the three highest 6-month I Bond inflation rates have all been since 2022. The current rate of 1.69% ranks 13th highest of the 50 in history.

I plan to buy as well. What is the use of break even rates if they mostly seem so far from reality? May be my mind is mostly on the wrong side..:)

I am with David. This TIPS doesn’t precisely fit in my ladder but is too tasty to pass up. I seriously doubt future inflation will be as low as it seems most expect. A great deal of wishful thinking involved.