By David Enna, Tipswatch.com

Last week I wrote about my recent buying spree of medium- to longer-term Treasury Inflation Protected Securities, combined with some shorter-term nominal Treasurys and bank CDs. My goal is to take advantage of current high real yields to fill my fixed-income ladder out to 2043.

In the feedback I got to that article, several readers asked about the attractiveness of very short-term TIPS, which appear to have above-inflation yields higher than 3.6%. For example, at Friday’s close:

In general, I have recently preferred to use T-bills, bank CDs, and short-term Treasury notes for investments of less than 5 years, and TIPS for investments of 5 years or more more. That’s mainly because short-term nominal rates have been so appealing. But I decided to take a look at CUSIP 912828B25, the TIPS maturing January 15, 2024.

The goal: To set aside $15,000 for a January 2024 purchase of a new 10-year TIPS, which will mature in 2034. At this point, there no TIPS that mature in 2034 and I want to add this one to my investment ladder. I’ll probably buy it at the originating auction on January 18, 2024.

The account: Traditional IRA at Vanguard. Money for this purchase is being withdrawn from my holdings in Vanguard’s Short-Term TIPS ETF (VTIP).

The question: How would investing in CUSIP 912828B25 — maturing Jan 15 2024 — compare with investing in a 17-week T-bill, maturing Jan 2 2024?

So last week, as an experiment, I bought $12,000 par value of CUSIP 912828B25 after doing a quick analysis of the likely results. Nothing is certain, of course. But let’s take a look.

Note that to come up with proceeds of $15,000+ in January, I needed to purchase $12,000 par value of this TIPS. That is because it carries a lofty inflation index of 1.30749, meaning my $12,000 par would actually purchase $15,689.88 of principal. The coupon rate is only 0.625%, so this TIPS sold at a discounted price of 98.73.

The end result was that I paid $15,490.62 for $15,689.88 of principal. That is an immediate gain of 1.29%, or an annualized return of about 3.92% if nothing else happened until maturity. But … two things will happen: 1) The principal balance will continue growing (or possibly falling) along with U.S. inflation from August to November, and 2) there will be a final coupon payment of 0.312% on Jan. 15 based on the ending inflation-adjusted principal.

Also, remember that inflation accruals for TIPS are based on inflation two months earlier. The September inflation accruals have already been set by the 0.19% non-seasonally adjusted inflation reported for July. We already know the inflation index for this TIPS on Sept. 30. What we don’t know are the indexes for October (based on August inflation), November (September), December (October) and half of January (November).

My scenarios look at how this TIPS would perform if non-seasonally adjusted inflation runs at 0.2%, 0.1% or 0.0% for the months of August to November.

Based on this analysis, CUSIP 912828B25 could create a nominal annualized return of nearly 7.5% if inflation runs at 0.2% a month from August to November. That number drops to about 6.4% if inflation runs at 0.1% and 5.1% if inflation remains flat throughout those months.

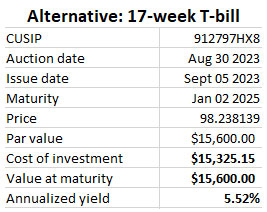

Compare that to the return of a 17-week Treasury bill sold at auction last week:

The TIPS is the clear winner if inflation runs at a monthly average of 0.1% or 0.2% through November. But the T-bill is the winner if inflation is flat or declines in those months.

Where could this go wrong?

I do think deflation risk is higher for a very short-term TIPS (especially one with a high inflation accrual) than for a longer-term TIPS. The long-term investment has time to make up for a few deflationary months. The short-term investment takes an immediate hit.

In the closing months of the year, non-seasonally adjusted inflation tends to run lower than the official seasonally-adjusted CPI number you see reported each month. Last year, for example, non-seasonal inflation came in at -0.10% in November and -0.31% in December. So it is possible we could see a deflationary month before the end of the year, which would likely make the 17-week T-bill the winner.

I’d say that deflation seems less likely in 2023, with the Cleveland Fed currently forecasting a rate of 0.79% for August. That’s probably an over-shoot, but it definitely indicates August wasn’t a deflationary month.

Conclusion

No one knows where inflation is heading, even a few months into the future. But my judgment was that CUSIP 912828B25 is likely to out-perform the 17-week T-bill, so it was worth an experimental purchase to set aside money in January 2024.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: A 10-year TIPS matured Jan. 15. How did it do as an investment? | Treasury Inflation-Protected Securities

Pingback: Here are results of my short-term TIPS experiment | Treasury Inflation-Protected Securities

Hi David, thanks for the helpful information on TIPS. I’ve got a question about the maturity of bond 912828B25. I recently invested in these T-Bills on Vanguard’s secondary market and I’m unclear about the payout at maturity.

As of 11/26/23, the Bond factor stands at 1.31857. I bought 26,000 shares worth $35,306.23, likely adjusted for inflation/bond factor.

When this bond matures on 01/15/24, will the already adjusted $35,306.23 be multiplied by the Bond factor of 1.31857 (assuming it remains unchanged)? I’m a bit confused—some clarity would be appreciated.

I’ve been trying to understand this online but couldn’t find a clear answer. Your insights would be valuable, as always. Thanks!

The price you paid on the secondary market was set by 3 factors: 1) the amount of par, which was $26,000, 2) the inflation factor on the day you purchased, and 3) the current market price of 912828B25. As of this weekend, that TIPS has a discounted price of about 99.28. It isn’t clear for me what you actually paid for this TIPS, was the $35,306.23 the adjusted principal or the actual cost of the investment?

On December 31, that TIPS will have an inflation factor of 1.31862, so if it matured on that day, you would receive 26,000 x 1.31862 = $34,284. (In other words, at maturity you get par value x inflation factor.) In addition, you would get the last coupon payment of about $214.

But 15 days remain in January until maturity, and we don’t know what the inflation factors will be for that month. That will be revealed with the release of the November inflation report on Dec. 12.

Thanks for your quick reply!

Yes, The price at the time of purchase, with everything you’ve described included, was $35,306.23 for the 26,000 shares of this bond.

My TIPS appears to alreadyy adjusted for the bond factor and will not hypothetically change dramatically on the maturity date.

One of the representatives at the Firm told me that the amount it’s currently worth in my account ($35,306.23) would be multiplied by the bond factor, bringing it to approximately $46,000. this seemed inaccurate and didn’t make sense since it was already adjusted when I purchased the 26,000 shares.

I apologize if this explanation isn’t clear.

Yes, market value has nothing to do with the final payout, which is always (par value x inflation factor) + last coupon payment. Very few investment advisers seem to understand how TIPS work.

Enjoyed your analysis. I’ll find the results interesting, as I purchased that 17 week T-bill…

The great thing about the 17-week T-bill is that it provides an absolutely certain nominal return: 5.52% annualized. The TIPS provides an uncertain nominal return; could be better, could be worse.

Lot of work for little gain. Not a bad bet but, depending on one’s level of of confidence, you have to do it in size to wring out any significant money out of it. If the tips offer was available in size, a dealer would likely be willing to bet the arb and short at the bill rate or better in order to fund purchase of the tips.

No worries here about “significant money,” just enough to buy that TIPS being auctioned in January. A lot of readers were asking about these very-short-term TIPS, so it was worth a look.

I’ve often wondered myself about these high-yielding short-term TIPS. Looking forward to your post-maturity comparison in January, to see which will one comes out ahead.

Do you plan to sell the Jan 2024 a couple of days early so you those funds are available as cash to place an order for the Jan 2034 auction? I use Fidelity for placing auction orders and all funds must be available in cash before I can submit an order.

Good question, but no, I won’t be selling early. I am not sure how Vanguard will handle this. Obviously the cash will be there on the settlement date of Jan. 31. I’ll have to find a work around if the auction purchase isn’t possible, or wait for a chance at the secondary market.

I have a margin account at Schwab partly for this reason. It shows me having negative cash between purchase and settlement if I don’t have the cash available, but so far has not charged me any interest if the funds appear on settlement day. It’s rather annoying having to keep track of things and jump through the hoop of selling my money market fund if necessary, as Schwab does not do that automatically. However, maturing securities are credited immediately.

Even without a margin account (i.e., in my IRA accounts), I’ve been doing the same thing — a lot, in the past year — at Schwab. Yes, I see the negative cash balance and the “money due” banner on the balances page, and even get the occasional urgent email, but when I’ve called and explained that I plan to sell shares of my Value Advantage money fund (recently yielding close to 5% better than cash balances) in time to match up with the end-of-month issuance date of a TIPS bought at a mid-month auction, or the issuance date of a new, not-yet-issued CD, the rep has always responded “OK, I understand, that’s fine.”

Okay to do just for fun, but you are looking at 5 months interest on $12k. Even a 2% annual interest rate difference over 5 months would be only a difference of $100. so if you guess right or wrong shouldn’t hurt or help much. If you had millions to invest for a few months it would be a bigger deal although guessing inflation over a few months seems more like gambling or speculating.

I suspect the tips will do better due to the illiquidity premium — not as easier to sell early for the expected price as a t bill. I have found hard to buy secondary tips for the same as the wsj price or sometimes have to put in the order several times before it’s executed but buying a newly issued t bill is super easy.

Sure, the amounts are small and someone could scale up if they wanted. My article explains the specific purpose to set aside $15,000 into January 2024. It notes the actual gain at 0.2% inflation would be $377 in 4.5 months (but that is uncertain) and the gain with the 17-week Treasury would be $275 (which is certain). So, the upside is probably about $100, or maybe more, and the downside is negligible, probably. I am sure there is an liquidity premium on TIPS, but I have never sold one, so I can’t say from experience.

I am trying to understand the calculation for the final coupon payment. You write, “there will be a final coupon payment of 0.312% on Jan. 15 based on the ending inflation-adjusted principal.” Based on the middle assumption the final principal would be $15,775.57. If you multiply that by the coupon rate of .3125 that equals $49.30. You show $36.70 as a final payment. What am I doing incorrectly?

As the chart explains, I subtracted the $12.52 of prepaid interest which came along with the purchase. So when I get that money back on Jan. 15, 2024, it isn’t really a gain.

Thanks David for this analysis. Just be aware that the Cleveland Fed forecast figure of 0.79% inflation is “inflated” by a seasonal adjustment. I use their year-over-year forecast to derive an unadjusted figure potentially applicable to TIPs. For August that would be 0.59%.

I have wondered about that. Thanks.

As usual, an excellent analysis I think. Doing approximately the same myself.