By David Enna, Tipswatch.com

Vanguard’s lineup of bond exchange-traded funds has long had a missing piece: An ETF that indexes the performance of the full spectrum of maturities for Treasury Inflation-Protected Securities.

Vanguard’s only option was VTIP, its Short-Term Inflation-Protected Securities ETF, which has been around since October 2012. It is based on index that includes all TIPS maturities of less than 5 years.

I like VTIP because volatility is held down by its short duration. For that reason it tends to track changes in inflation better than longer-term funds, which offer more potential for capital gains, or losses. VTIP also has an Admiral Shares mutual fund version, VTAPX.

In addition, since June 2005, Vanguard has offered a mutual fund with the full range of TIPS maturities: VAIPX is the Admiral Shares version. Now it is launching VTP, a new ETF that is similar to, but not a clone of, VAIPX.

In its press release for this ETF (one of several new issues) Vanguard notes:

VTP provides long-term investors with a robust tool designed to protect their portfolios from inflation risk. It offers exposure to the full spectrum of the U.S. TIPS market, complementing our existing Vanguard Short-Term Inflation Protected ETF (VTIP). VTP has a broader investment universe and a longer duration profile, launching with an expense ratio of 0.05%. It could be a valuable addition for those looking to hedge against inflation over extended periods.

If you are interested, here is the prospectus.

In most cases, I’d caution against investing in a brand-new ETF, but Vanguard has a lot of experience in this sort of index investment. Most investors would prefer to go with a similar ETF over the Admiral Shares mutual fund, which requires a minimum investment of $50,000 and actually has a slightly higher expense ratio, 0.10% versus 0.05% for VTP.

The only issues are:

- Would you prefer to invest in a TIPS ETF versus buying individual TIPS and holding to maturity? And then …

- If you want to go the ETF route, would you prefer to go with the lower-volatility shorter duration VTIP versus the longer-range scope of VTP?

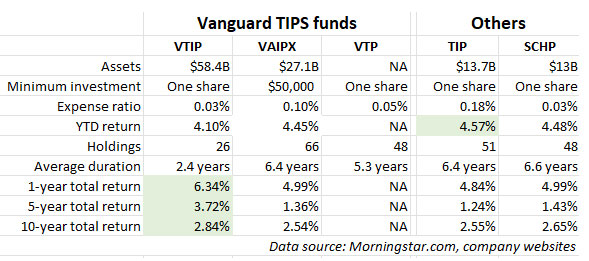

We can’t do a direct comparison of the ETFs yet, but let’s look at how VTIP and VAIPX have performed, with the addition of the full-range iShares TIP and Schwab SCHP ETFs:

This information, gathered from Vanguard’s site, shows that VTP is not an exact duplicate of VAIPX. It is holding fewer issues, and its average duration is shorter. There are 53 TIPS currently trading in the secondary market.

Also, as you can see, VTIP has out-performed the full-maturity VAIPX over 1-year, 5-year and 10-year periods, during a time of high volatility in the Treasury market. However, if we entered another era of quantitative easing, with strongly lower real yields, VAIPX and VTP (along with TIP and SCHP) would likely outperform VTIP.

Thoughts

I don’t currently invest in any TIPS mutual funds or ETFs. I have used VTIP in the past as a holding fund while waiting to make future investments. I favor VTIP because of the lower volatility. The new ETF, VTP, should over time closely track TIP, the biggest TIPS ETF, which has a higher expense ratio of 0.18%.

My preference, as always, is to build a ladder of TIPS investments to be held to maturity, providing inflation-protected cash for future needs.

Now, here is a bonus. Morningstar’s Long View podcast this week featured Salim Ramji, one year into his tenure as CEO at Vanguard. He talks about the firm’s efforts to simplify investing and improve customer service:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for this post, David. Do you have any insight or guesses as to why the mutual fund would have a higher expense ratio than the corresponding ETF version (namely twice as high, and for both the Admiral and non-Admiral variants)?

I think this is a fairly common occurrence for mutual funds vs ETFs. For example, the Vanguard Total Bond Fund ETF has an expense ratio of 0.03% while Vanguard Total Bond Market Index Fund Admiral is at 0.04%. I imagine that ETFs are easier to manage because this is an individual stock instead of a mutual fund.

Great information, thank you! What would you recommend (ladder or fund) for someone who plans to consume the dividends/interest only and not sell/consume the principal? What duration makes the most sense in this case?

I should add that this would be in a qualified plan if I chose a fund or I’d have to roll to an IRA to build a ladder. I do like ERISA protections, though… so that’s a point in favor of a fund right off the bat.

Jess, given your desire to keep the original investment intact, I’d say the idea of total bond fund makes sense for your qualified account, with dividends being paid out. But your account value will fluctuate with changes in market yields. And the payouts will be taxable if you withdraw them.

If you move the money to an IRA, why not simply consider buying a single nominal U.S. Treasury, or a combination, depending on your time-frame? The 10-year note is yielding 4.43% and the 20-year bond is at 4.96%.

This is a complex issue and depends on your personal needs. I am not a financial adviser. Do you want to roll out of your qualified plan? If so, and if the money goes into a traditional tax-deferred account, that is an excellent basis for building a ladder. But if you want to stay in the qualified plan (which might have only a few investment choices) then a good total bond fund might be a good choice. Again, I am not a financial adviser.

Sorry, that did sound too close to advice-seeking. I was hoping you’d comment if philosophically there’s a case where a fund makes more sense than a ladder… since the return of principal is a big selling point of a ladder, but not relevant in this situation.

FYI, in 2025, I purchased 10,000 I-bonds in my account, then purchased 3,000 more in wife’s gift box. Just successfully delivered the 3,000 I-bonds from the gift box to my account with no issue. Apparently that “loophole”. Is still there? That October 2024 e-mail from the treasury telling people to deliver I bonds from the giftbox as soon as possible is standard procedure going forward??

We don’t know anything more this year. It still appears if you buy the cap amount first, then you can then receive more sets of gift-box I Bonds after that purchase, in the same year. If you receive gift deliveries first, they will fill the cap amount and you won’t be able to make a traditional purchase in that year. I haven’t heard anyone contradict this.

VAIPX is “actively managed,” which explains the higher fee and the different composition of holdings. I doubt the extra fee for VAIPX is worth it. It would be interesting to compare VTIP to SCHP, which is also indexed and has a slightly lower fee, I believe (.03%?)

Good information, thanks. I added data on TIP and SCHP to the chart for comparisons. I suspect VAIPX is most widely held in defined benefit plans like 401(k)s, which usually do not offer access to ETFs.

David, with individual TIPS one has the option to make purchase decisions based in part upon the (expected) real yield of the bonds.

In your opinion, does the idea of purchasing a TIPS fund or ETF inherently mean that one is indifferent to the real yield of the bonds held in the fund/ETF?

Is this another distinguishing feature between purchase of individual TIPS vs a fund or ETF?

No, I think you should pay attention to the current “market” real yields of the TIPS held in a fund, meaning how they are priced today. My thinking is that TIPS funds are fairly attractive today because real yields have increased to historically normal levels. See this posting. But when you buy an individual TIPS to hold to maturity, you are locking in your real yield at purchase. That is the approach I prefer.

Do you know how these funds are taxed, if held in a taxable brokerage account? I hold individual TIPS in an IRA to avoid the tax issues but I’m wondering if these funds would be suitable for a taxable account.

With a TIPS fund or ETF, inflation accruals are paid out as current income, along with the coupon rate, so holding these funds in a taxable account is very similar to holding any bond fund in a taxable account. If you reinvest dividends, you will pay tax on the dividends in the current year but your basis will increase, lowering your taxes owed in the future, potentially.

Could you elaborate (or point to a past post?) on your preference for holding a ladder vs one of these funds? Obviously the expense ratio saps yields. But it is convenient to just hold a fund and never worry about it. I suppose an expert (or his readers? 🙂 can optimize which TIPS you purchase over time to try to out perform the index. Have you ever analyzed the performance of your ladder vs an index?

On a completely different note, an idea / question: Government employees have access to the “G Fund”, which is the weighted average of all treasuries with maturities four years or more. Some (e.g. here) argue that it has a measure of inflation protection. I would love to hear your thoughts on that.

The idea of a ladder, preferably in a tax-deferred account, is to have guaranteed inflation-protected cash flow for each year in the future. Set aside $20,000 for 2035 and in 2035 you will withdraw $20,000, adjusted for inflation, plus collect a coupon rate along the way. There are many articles on this site:

One / Two / Three

I don’t know much about the G fund. It looks risk-free, which is good.

Thanks. The third link gets to my question. I’m generally convinced on the value of the ladder (certainty of returns, no expenses), but remain confused by the emphasis #3 has on principle loss in rising rate environment. Obviously this doesn’t impact TIPS held to maturity. But while the bond fund will lose principle, if you hold it longer than the duration of the constituent bonds you should make up the principle loss with higher returns, right?

So for “long-term” (e.g. much longer than the average duration), is there really more risk of principle loss in the ETF than the ladder? I would also be able to claim a capital loss I think, realize some tax advantage.

A lot of Bogleheads (very smart people) point to duration-matching as a way to reduce risk. And for a portfolio that keeps rolling forward, it’s probably true. My problem with that strategy is that it could backfire if you need to withdraw the money in the midst of a very bad year, for example 2022, when the TIP ETF’s net asset value fell 12.2%. Even with dividends reinvested TIP hasn’t quite regained the value of its high in late 2021.

The “G Fund”. is an excellent fund not available to the public. It provides the weighted average return of all treasuries like you said, but there is NO interest rate risk. The fund never goes down, it does not hold marketable securities. The securities are specifically issued to the TSP.