By David Enna, Tipswatch.com

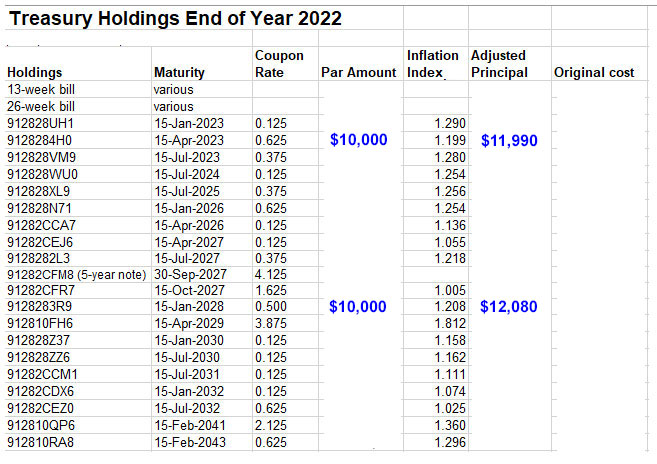

A lot of readers ask about the ladder of TIPS investments I have built over the years. Yes, I do have a ladder, and it does hit every year from 2023 to 2032, and then jumps forward to 2041 and 2042.

Notice the gap? That’s because there are no TIPS issues that mature from 2033 to 2039. Why? Because the Treasury no longer issues 20-year TIPS, leaving a gap in maturities. So I will need to pick up those missing years, one at a time, beginning with this month’s auction of a 10-year TIPS, maturing in 2033.

While it might sound like my ladder was well planned, honestly it was built haphazardly, from purchases of 5- and 10-year TIPS, mostly at auction, and only when I judged real yields to be “attractive.” So the ladder has a lot of maturities this year, in 2023, and then in 2027, because of my purchases of 5-year TIPS in 2018 and 2022, the only two years in the last decade when real yields moved well above zero.

Here is what my ladder looks like, with a few nominals thrown in and actual investment amounts removed. I use an Excel spreadsheet to update the inflation indexes (drawn from the Wall Street Journal) and adjust my principal amounts a few times a year:

Now here we are in 2023, and again real yields are well above zero across the entire TIPS yield spectrum, with the 5-year at 1.68% and the 30-year at 1.55%. If you are interested in building a TIPS ladder, this is a great time to begin.

Why is a TIPS ladder attractive?

I recently read a well-thought out article titled, “TIPS Funds Vs. A Ladder,” on the SeekingAlpha site. The author is Ralph Wakerly, an investor, entrepreneur and consultant with over 35 years of investment experience. Wakerly argues that historical inflation data suggest the next decade of inflation “may run considerably above the ~3% that consumers and investors expect,” making TIPS a highly attractive investment.

I suggest that you read his entire article, but here are some of his major points:

“For investors at or near retirement, a TIPS ladder is an effective means of generating reliable, predictable income. …TIPS are most effective and reliable if held to maturity. This argues in favor of buying individual bonds via a ladder, not a mutual fund or ETF. …

“You can build an effective TIPS ladder that is relatively simple, with a manageable number of holdings via a mix of auction buys and via the secondary market. …

“A bond ladder via a brokerage account like Fidelity or Vanguard costs nothing. There are no transaction costs and no annual expenses.”

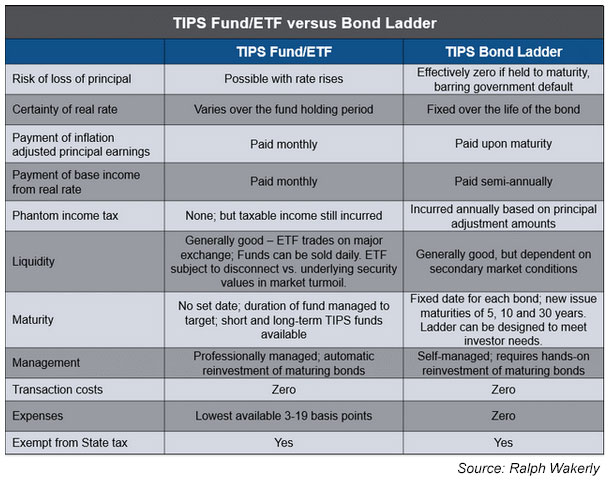

TIPS funds versus a ladder

You can find many smart investors (Bogleheads, especially) who argue that a TIPS fund or ETF is no more risky that holding individual TIPS to maturity. While there may be some logic to this argument (duration matching often comes up as a reason) you have to recognize that the biggest TIPS fund, the TIP ETF, had a total return of -12.24% last year, even as inflation soared to a 40-year high. If you own individual TIPS and are holding to maturity, you can ignore these market swings and just rake in the inflation accruals. At maturity, you are going to get par value x inflation accrual.

Wakerly came up with this comparison of TIPS funds vs. individual TIPS, an excellent summation:

Consider interest rate risk

As Wakerly notes. “This was painfully evident this year. Fund investors have been punished as the 10 year real TIPS rate went from -1% to the current 1.6%. … However, individual TIPS bonds held to maturity protect against principal loss in the event of rising real rates.”

At a time of rising real yields, TIPS funds are going to suffer. But an individual TIPS will stay on its course to maturity, where it will pay par value + inflation accrual (or at the very least, par value). If you hold a TIPS in a brokerage account, it can be painful to see the loss in “market value” because that is how the broker will report it each day. But in reality, your TIPS is actually holding its principal value (unless deflation strikes), and rising with future inflation. Wakerly says:

In my opinion, this is the most important advantage of buying individual bonds in a ladder versus a fund. This is especially important for retirement investors who want predictable income and cash flow.

Is a ladder really diversified?

Of course it is, if you do a decent job of spacing out maturities and the amounts invested. The TIP ETF only has about 48 holdings — that is all the TIPS trading on secondary markets. A ladder with a few holdings with attractive real yields, maturing at a date to match your needs, is well diversified. Wakerly notes:

From a bond diversification standpoint there isn’t a need to buy a fund. Unlike corporate or muni bonds where you want to diversify default risk across issuers, TIPS are effectively riskless assets backed by the full faith and credit of the US government.

On the other hand, keep in mind that TIPS are a highly specialized investment, designed to protect assets against future inflation. Most people would want to pair their TIPS holdings with low-cost stock index funds, traditional bond funds and some nominal fixed income, such as bank CDs or Treasurys.

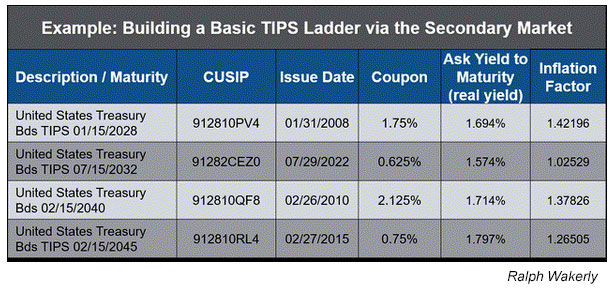

Building a ladder

Wakerly says he is building a ladder with an eye on future income needs, so he is focusing on TIPS with a weighted maturity of 18 years. You’d need to consider your future needs. In my case, I am already retired and just trying to protect capital against future inflation, so my ladder focuses more on the near term. Here is Wakerly’s sample ladder:

Another strategy: I have heard from many readers who say they have built a TIPS ladder in their traditional IRA account to account for future required minimum distributions long into the future.

Conclusion

I highly recommend reading Wakerly’s complete article, which goes into greater detail, and another he recently wrote on TIPS titled, “TIPS Performance Could Rival That Of The S&P 500 Over The Next Decade“. (I’m not endorsing that opinion, but after the highly volatile 2022, anything could happen.)

But I do agree with his closing opinion:

“A TIPS ladder is an effective way to invest, especially for those in or near retirement who are comfortable creating their own do-it-yourself annuity. The ladder is currently generating one of the highest yields in the past 14 years with higher certainty of returns, and better principal protection than a mutual fund or ETF.”

One more thing …

For another interesting read on TIPS ladders, check out financial adviser Allan Roth’s October article, “The 4% Rule Just Became a Whole Lot Easier” in which he describes how he painstakingly built a TIPS ladder that will allow 4.36% inflation-adjusted withdrawals over 30 years. He notes, “This is a very attractive strategy for someone wanting a guaranteed inflation-adjusted cash flow in addition to Social Security.”

Roth built this ladder with the help of a Bogleheads contributor, Bob Hinkley, and his article set off a lively — and helpful — discussion in the Bogleheads forum. The article was also referenced in a December Morningstar article titled, “How to Build a TIPS Ladder“.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’m about to take the plunge on a ladder. If I buy on the secondary market (e.g. Vanguard) do I really need to care which TIPS I buy as long as I pay attention to the maturity date? In other words can I assume that the market takes care of pricing each bond appropriately or are some bonds with similar maturity dates better deals than others?

Things to consider: 1) the maturity date for the ladder and 2) the real yield to maturity (which you’d like to be as high as possible). When you go to purchase, several things will affect the price for the par value you enter: 1) the market price, which could be above or below $100 and 2) the inflation index, which will tell you the amount of principal you will actually be purchasing. Also, if you are placing a small order you may not find a seller or you may get a slightly lower real yield. I do think the market is fairly priced … some of the very short-term TIPS may look to have huge real yields but in reality they would pay about the same as a nominal Treasury.

Hypothetical (unrealistic) example but will help me understand:

2 TIPS than mature on the same date 10 years ahead so principal gain though indexing is equal.

a) Price is $110 with a coupon of 2%. Excluding increase in principal through indexing, this has a 10% premium and will deliver 20% interest over 10 years to net 10%

b) Price is $95 with a coupon of 1%. Excluding increase in principal through indexing, this has a 5% discount and will deliver 10% over 10 years to net 15%

Is this right?

Thanks!

Buffethead, two TIPS maturing the same year could have very different inflation indexes because one might have been a 20-year TIPS and the other a 10-year TIPS. You’ll see that often. The ones with high premiums have high coupon rates and also could have much higher inflation indexes. The coupon rate will set the price per $100 you will pay, but the real yield to maturity is the key factor: If it is close then the two TIPS will have very similar performance, despite the different coupon rates.

I invested about 20 %of my portfolio in SCHP ,a medium term tips ETF and saw my principal drop quite a bit. Should I wait for it to come back up in value before building a tips ladder? What would you recommend for someone in my situation?

SCHP is a good fund, but because it holds the full range of maturities in TIPS it got hit hard when real yields soared higher last year. It had a total return of -12.7% last year, but is up about 1.7% so far this year. I am not a financial adviser, so I can just give my personal opinion: Last year, starting in the summer, I was selling SCHP in my tax-deferred brokerage account and using the proceeds to buy individual TIPS. Now the only TIPS fund I own is the shorter-term VTIP, and I am still using that to buy individual TIPS when the real yields look good. I’d rather own individual TIPS and hold to maturity, but … just my opinion.

Let’s say I’m setting up a TIPS ladder and I want to buy some TIPS on the secondary market that mature in 2026. When I check on Fidelity, I see 5 possible options. I don’t really care about the maturity date as long as it is in 2026, so how do I know which one to choose? Do I simply pick the one with the highest yield to maturity? Do I pick the one with the lowest adjusted price to protect myself from possible losses during a deflationary period? Or do I look for something else? I couldn’t find any information about this on your Web site, but my apologies if I missed it. Thanks.

This is a hard call. Real yield to maturity is the primary factor, but you’d also want to look at the coupon rate and accrued principal, which will affect the price you pay. TIPS with a large amount of accrued principal and a premium price often have a higher real yield, and that is the case with 912810FS2 that matures Jan 15 2026. It was originally issued in 2006 and has an inflation accrual of 50%, plus a slightly premium price. So you are taking on the risk of buying a lot of additional principal at a premium price. And that is reflected in the real yield.

Is Wakerly buying bonds on the secondary market?

Yes, those are secondary market purchases and the real yields shown were from a week or more ago.

I guess I tend towards a contrarian at heart… I own TIPS and I-bonds but worry about returns on the TIPS in real yields in the event of extended deflation? It appears that I would be, in that event, watching the accrued principle going down and only receiving a low fixed interest rate on that depreciating principle. It also appears that on the other hand my I-bonds accrued principle would not go down in any deflationary period.

If you are worried about deflation, I Bonds are a better investment. With an I Bond, the accrued principal never goes down. But realize that extended deflation will wipe out the fixed rate of the I Bond and you will get 0.0%. Another option would be longer-term nominal Treasurys, because they will far exceed inflation by paying more than 0.0%.

Good to know! It then appears that I-bonds are good protection of any accrued principle against either inflation or deflationary periods.

I have been building a TIPS ladder for retirement with the desire of receiving $50k per year in current dollars, so I’ve been buying $50k per year at recent 5 and 10 year auctions. With real yields where they are today, I’d like to buy out further years, beyond the “gap.” If I’m looking at the years of 2040 to 2045, for example, how do I figure out how much in par value I should be buying today?

The real yield of those 2040 to 2045 TIPS issues right now is just under 1.5%, so do you want to figure out the current value of the future $50,000 at a real growth rate of 1.5%? In other words, how much to invest today to have $50,000 in real, after-inflation terms? I don’t know the formula to use but maybe one of my readers has a solution.

If you want to have TIP bonds mature in a specific year provide you with $50k in current dollars, then all you need to do is buy those TIP bonds in the secondary market with an adjusted price today of $50k. Take for example 2040. The TIP maturing on 2/15/2040 has an index ratio today of 1.37835 so you divide your $50k by that ratio and you get 36,275. Let’s call that $36k, so you need to purchase $36k in par value of this TIP. With today’s asking price of 109.0625 that will cost you about $54,117 plus about $427 in accrued interest for a total of $54,544.

Now with that said, you should NOT be buying $50k per year in your bond ladder to ensure that you get $50k per year in current income. To better understand why this is read the Allan Roth article.

Thanks, Jim. That’s what I’d thought, but appreciate the confirmation. Are you referring to the Allan Roth article “The 4% Rule Just Became a Whole Lot Easier” or something else? I didn’t see anything in that one that would convince me not to do so. Many thanks.

Yes that is the article. When you build a ladder of TIPS to provide a constant annual amount of real income you have to account for interest payments from the bonds that don’t mature in a particular year of your ladder. The spreadsheet that Allan refers to in his article does this for you.

Here is an example. Using that spreadsheet, I just setup a 29-year ladder that pays $50k in current dollars every year starting in 2024 and goes through 2052. In order to get $50k in current dollars in 2024 you will only need to buy $25K in par value of the TIP that matures in 2024. That TIP has an adjusted cost today of $28,695K. In 2024 you will also get about $20k in interest from the TIP’s that mature in 2025 through 2052 which when combined with the maturing TIP gives you your $50k in current dollars.

i think it would be really difficult to do that calculation with a high degree of accuracy because TIPS doesn’t reinvest interest and principal is lost during anytime CPI-U goes into deflation. much easier to do with I Bonds.

Assuming 30 year holding period with reinvested interest payments every 6 months, desired real $10K at maturity, and 0.4% fixed rate, I think the calculation in a spreadsheet would be:

PV(0.002,60,,10000,0) which comes out to $8870 invested now to get $10000 of real buying power later

The TIPS ladder is appealing but does it work in a non-qualified account given the tax implications of the phantom income. You are paying some tax on that thirtieth rung thirty years early. I have not done the math but the value of that tax payment compounding in an I bond seems relevant. If the ladder is built in a qualified account you are giving away the state tax exemption and in my case my qualified accounts are filled with equities. I would need to put fixed income into my qualified account and take the appreciation of equities in my non-qualified account. I can run the numbers but wonder if anyone has done this analysis with something like a real TIPS yield of 1.2% and a real yield on an I bond of 0.4%.

It’s better to build a TIPS ladder in a tax-deferred account, especially after retirement, when you might not want to raise money to pay the income tax (or to buy the TIPS). The one negative is that Treasurys in a traditional tax-deferred account lose the state income tax exclusion. I have some TIPS in a taxable account and I am letting them mature — all my new purchases are in a traditional IRA. When these taxable-account TIPS mature, I have already paid the taxes so there is little owed at maturity.

I understand that it’s better but in my case that would mean moving equities to my non qualified account. I’d rather have the growth in the qualified accounts. If the option is a thirty year tips at say 1.2% in a non-qualified account or an I bond at 0.4% RY in a non qualified account which has the better outcome?

Just wondering if these types of numbers have been run.

Thanks

A bit off topic, but another thing to consider: If you hold stock assets in an a taxable account, you can take advantage of lower capital gains tax rates, plus do tax-loss harvesting when the market is down.

I am relatively new to TIPS and this group. Building a TIPS ladder sounds exciting though I need to read all the articles that you have referenced and learn more. As I shared before, buying bond funds has been a big no for me for a long time; my wife and I own none. However, I learnt a few more reasons why not to buy them from the referenced Wakerly article..looking forward to David’s Jan 15th 10-year TIPS preview….thanks!!!

In the linked Q&A you wrote ” If you bought a TIPS and got a real yield to maturity of 0.75%, then you are going to earn 0.75% over inflation for the term of the TIPS, if you hold to maturity.” The seems to imply a future value, that your investment X will grow over n years at at an after-inflation rate of 0.75% compounded annually and be worth (after inflation) 1.0075 raised to the nth power times X.

My understanding has been the YTM calculation does not say anything about reinvesting dividends (see https://www.economics-finance.org/jefe/econ/ForbesHatemPaulpaper.pdf)

So the meaning of “you are going to earn 0.75%” is a bit murky. You only get the expected future value if all the coupons can be reinvested in TIPS at the same 0.75% rate.

I think two problems exist. The first is the uncertainty of the yield at the time you reinvest coupons. As we’ve seen the YTM on TIPS can go up and down. If you reinvest at lower (even negative) rates then you’ll have less money after inflation when the bonds mature than expected when you first purchased the TIPS. Should we say all the actual outcomes earned 0.75% over inflation?

The second is that for many investors the coupons can’t be reinvested in TIPS bonds because the bonds sell on the order of $1,000 and the interest payment per bond might be $5-$20 per bond every six months. You need a big investment for that to be enough to buy another TIPS bond every time you receive coupon payments, and if you have can’t reinvest with inflation protection then you’ll have less when the bond matures than the YTM predicts.

I still think buying TIPS bonds is better than a buying a fund since it avoids the risk of the price swings a fund may have. If held to maturity you’ll have something in the neighborhood of what you expected from the YTM when you first purchased the TIPS. It’s unfortunate the Treasury doesn’t offer zero-coupon TIPS which would eliminate the two reinvestment problems above.

I get this “reinvesting dividends” argument often, but most financial research — including the research paper you link to — says you will earn the real yield to maturity, regardless of reinvesting dividends. Your future gains could be higher if you can reinvest the coupons at higher yields. One factor with TIPS — and not with other Treasurys — is that the coupon payment rises with future inflation, so the interest income continues to adjust higher if inflation is higher.

Let me put it this way. Not many people realize that YTM is a technical definition that calculates the IRR for a bond purchase, stream of interest payments, and redemption at maturity. I think they treat it as saying something about the amount of money they’ll have at bond maturity.

Let me give an example. Suppose you buy a $1,000 par value 20-year bond at par with 10% annual interest payments. Any bond calculator will say the YTM of this bond is 10%. Now let’s think about 2 worlds chosen for illustrative purposes. In the first you can reinvest every coupon at 10% so at maturity you’ll have $6,727. In the 2nd world interest rates fall to 0% the day after you buy the bond and stay there for 20 years. You happily collect your $100 annually but unhappily they never grow, so at maturity when your bond is redeemed you’ll have accumulated $3,000.

By the technical definition both outcomes earned a YTM of 10%. An extreme example to illustrate a point, especially in a world where current YTM are around 2% or less.

Still for longer periods of time, like in the question where someone wants to have $50K/year in 2045 which is about 20 years down the road, the reinvestment rate matters. With a compound growth rate of 2% a $1,000 investment grows to $1,486 in 20 years, with it grows to $1,220 or only 82% of $1,486. That could be a big miss for someone expecting $1,486 based on current YTM numbers.

There are 16 different TIPS issues — across a wide variety of maturities — on the secondary market that have 0.125% coupons. Not quite zero-coupon, but very very close.

True, but all those TIPS with the 0.125% coupon are now selling at a discount, creating the higher real yield to maturity. The price discount is what balances out the low coupon rate to create the market yield.

I think you missed the point of my post: By buying near-zero (0.125%) coupon TIPS, you don’t have to be be much concerned with coupon reinvestment rate risk plus you can predictably realize most of the quoted market purchase YTM through the maturity date of the bond; that is attractive to folks who want to defease a real expense in the maturity year of the bond and don’t need or want coupons along the way.

I have a municipal bond ladder (triple tax free), an I Bond ladder (tax deferred), and I am thinking of starting a short-term TIPS ladder to complement the other two. I have never purchased a TIPS and I have been reading your articles to try to simplify this investment instrument enough to feel comfortable with it. I’m getting there. I’m recently retired and do my own taxes. If I proceed, I would have to use money from a taxable account for this purpose. My inclination is to purchase a 5-year TIPS and a 10 year TIPS from TD at auction, hold them to maturity to ignore the constant flux, and fill in from there in between the two.

Question 1: Can I designate a POD upon order like I can with an I Bond and what happens if I pass away before maturity? Does the TIPS simply pass to my beneficiary’s TD account like an I Bond does once a death certificate is provided to TD?

Question 2: My other two bond ladders are simple from a tax reporting perspective. The Munis generate income with no tax consequence and the I Bonds are only federally taxed upon redemption. Easy. Since you have to pay tax along the way with TIPS, can you explain what 1099 forms I would receive from TD each year or point me to an article (either yours or someone else’s) that explains this aspect?

Thank you for all the information you provide here.

1) All the TIPS we own at TreasuryDirect are registered with my wife as the primary owner and me as the WITH owner. I don’t think you can use the POD – payable on death – registration with a TIPS, to designate a beneficiary. Not sure, though. (It can be used on an I Bond.) Of course, in an IRA account, you can name the beneficiary for the account.

2) TreasuryDirect issues 1099s for TIPS, 1099-INT and 1099-OID, in the same form. Those are posted late in January or early February. You need to go looking for them. TD doesn’t make this easy. I plan to write about those forms once they are posted for 2022.

You might find inheritance issues managed more conveniently by using your existing brokerage account for your TIPS bonds.