Oct. 23 update: New 5-year TIPS gets real yield of 1.182%

By David Enna, Tipswatch.com

Auctions for new 5-year Treasury Inflation-Protected Securities happen twice a year, in April and October. Because of the relatively short term, and the different inflationary conditions leading up to each maturity date, the 5-year TIPS auction is hard to predict.

I got caught by this phenomenon in October 2023, when a new 5-year TIPS (CUSIP 91282CJH5) auctioned with a real yield of 2.440%, well below the “market” yield of about 2.55% or higher. I was surprised. But I shouldn’t have been.

I wrote about this in an Oct. 20, 2023, article with the subtitle “There is an explanation for everything, right?” The basic lessons are these: 1) The October TIPS auction will get a real yield less than the apparent market rate, and 2) The April TIPS auction will get a real yield higher than market.

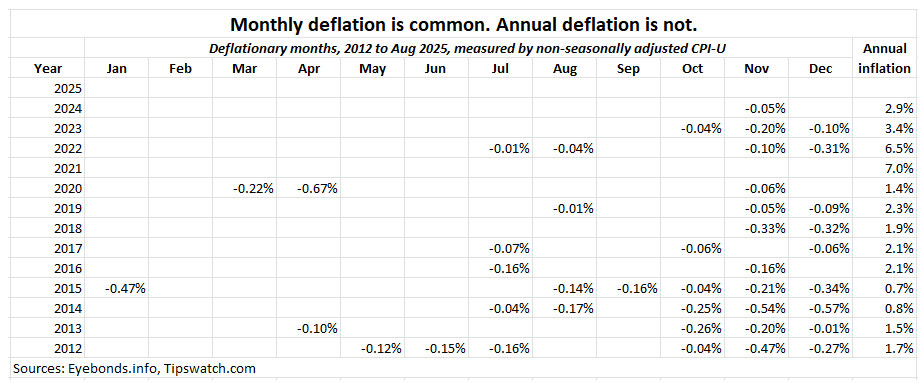

The reason is a bit esoteric: Non-seasonally adjusted inflation has a strong seasonal pattern, generally running higher than headline CPI from January to June and lower from July to December. The closing value of the April TIPS (reflecting inflation through mid-February) is much more likely to be exposed to end-of-the-year deflation, and therefore the April TIPS gets a higher real yield than “market.”

I created a chart last year to prove the point — the April 5-year TIPS gets a higher real yield than the October version:

Also see: ‘Inflation Guy’ explains seasonal adjustment (or lack thereof)

Here’s another chart that shows how deflationary months are quite common in the last three months of the year, which would reduce the maturing value of an April-issued TIPS:

What does this all mean?

On Thursday, Treasury will auction $26 billion in a new 5-year TIPS (CUSIP 91282CPH8). That will be the largest auction-size ever for this term, up from $25 billion in April and $24 billion in October 2024.

You can track the real yield of the April TIPS in real time on Bloomberg’s Current Yields page, which shows a Friday closing real yield of 1.23%. The U.S. Treasury also provides a daily estimate of the real yield of a full-term 5-year TIPS, which closed Friday at 1.30%.

Saturday morning, Vanguard’s bond-trading site was showing an “indicative yield” of 1.235% for the upcoming auction, obviously based on current trading in the April TIPS.

Conclusion: All of these indicators are wrong. At this point in time (things will change by Thursday) I’d predict this TIPS would get a real yield of 1.15% or lower. Past results show us the real yield will be lower than the 1.23% “market” created by the April TIPS. In other words, be prepared to be surprised.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.15% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.15% for 5 years.

Real yields will rise and fall next week in the days leading up to the auction. But it will be interesting to see how close this 5-year TIPS gets to the 1.10% fixed rate on the current Series I Savings Bond, available through the end of this month.

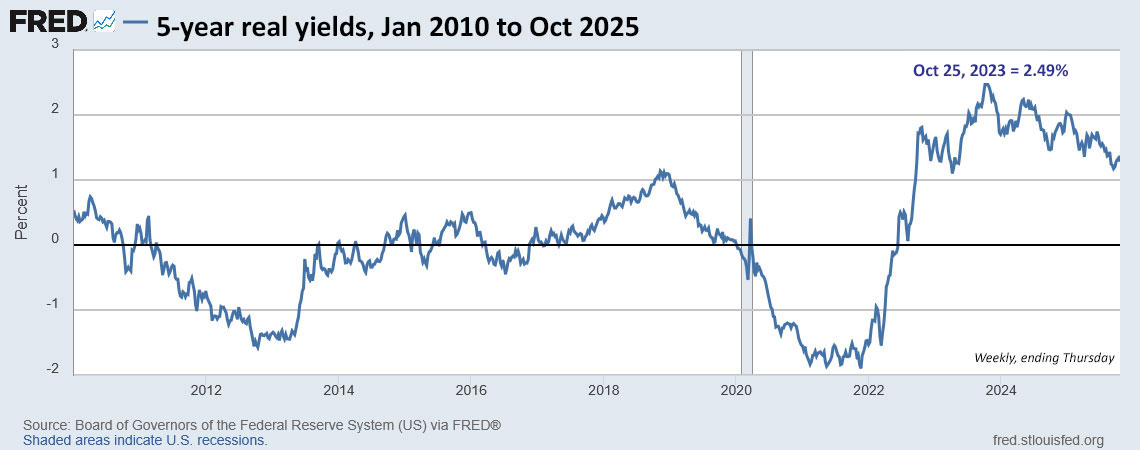

Here is the trend in the 5-year real yield over the last 15 years:

Side note: Remember that 5-year TIPS auction of Oct. 19, 2023, when the real yield was a “disappointing” 2.440%? Turns out that the auction came within a whisker of the 15-year high real yield of 2.49%, set a few days later.

Pricing

Because this is a new TIPS, the coupon rate will be set to the 1/8th percentage point below the auctioned real yield. That means the TIPS will have an unadjusted price slightly below par value. It will carry a minimal inflation index of 1.00148 on the settlement date of Oct. 31. The end result will be a price slightly below par. In other words, a $10,000 investment in this TIPS should cost very close to $10,000.

Inflation breakeven rate

Using the U.S. Treasury estimates of 1.30% for a five-year TIPS (probably too high) and 3.59% for a 5-year Treasury note (probably accurate) you get an inflation breakeven rate of 2.29%, a bit below recent trends. If you adjust the likely yield to 1.15% the breakeven rate rises to 2.44%, higher than recent trends. My conclusion: Who knows?

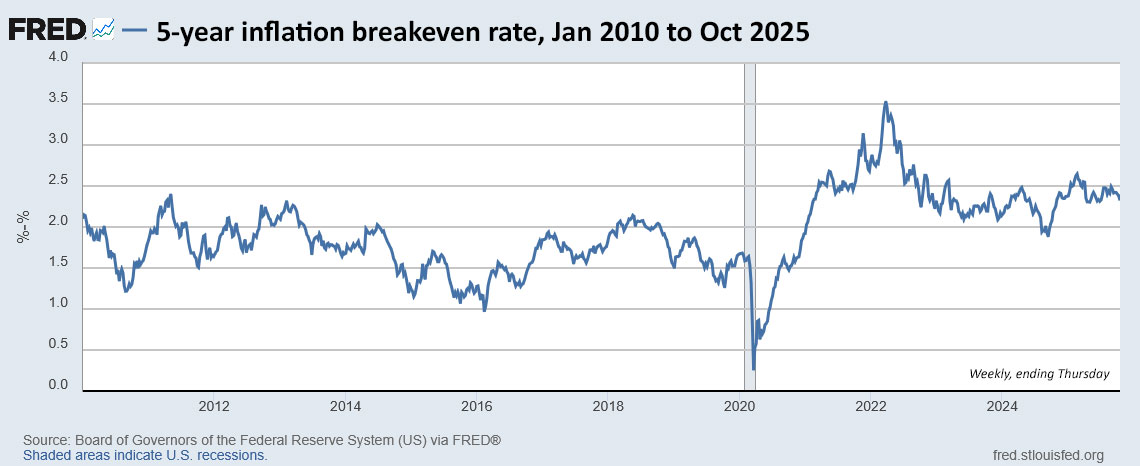

Here is the trend in the 5-year inflation breakeven rate over the last 15 years:

Thoughts

I often note that the 5-year TIPS is most sensitive to the Fed’s short-term rate cuts, and that has proven accurate in 2025. The 5-year real yield has fallen about 67 basis points since January 1, compared to 48 for the 10-year and only 8 for the 30 year.

Is a real yield around 1.15% to 1.20% still attractive for a 5-year TIPS? Yes, but it depends on your investment needs. As the yield approaches the now-current 1.10% fixed rate on the I Bond, the savings bond becomes more attractive, given its tax-deferral, deflation protection and flexible maturity. (The I Bond’s fixed rate is likely to fall to 0.9% at the November 1 reset, but 1.10% is available through the month of October.)

I suspect their won’t be much demand for this auction from small-scale investors. If you are jumping aboard, let me know your thoughts in the comments section.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

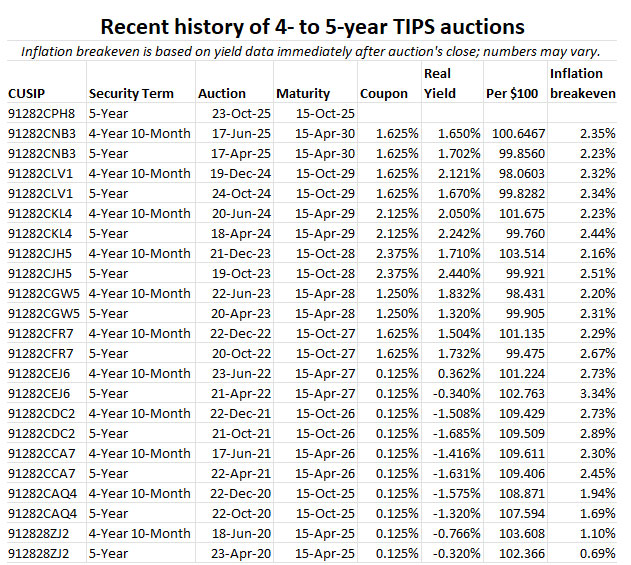

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Anyone else unable to log in to Treasury Direct today due to misconfigured security on their website?

I was able to log in earlier today.

Hi- A bit off topic, but do you have any inputs on the recent email from Treasury Direct stating that I should revisit my COI account and move my funds out and change my redemption route because big changes are coming to the COI aspect of my account?

I received the same email. But I have no funds in the COI. Nor have I ever used the COI. I always transfer directly to/from my bank. Anywho, seems more changes are on the way.

I didn’t get the email, but other readers have notified me about it. Readers can get the full details here: https://www.treasurydirect.gov/savings-bonds/emailcofi/

“Zero-Percent C of I is designed to temporarily hold funds for purchasing other securities. It does not earn interest, so leaving money in this account limits its growth potential … By cashing your C of I or using it to purchase interest-bearing securities, you can put your funds to work immediately!”

This is very good advice. No one should use COI for more than a day or two. It your account gets locked or you face other problems, that money could get stuck earning zero interest for weeks.

“Please note, there may be changes to Zero-Percent C of I to help streamline the process of investing with the Treasury, so cashing your C of I now will help you prepare. Stay tuned as more information becomes available on how we’re enhancing the TreasuryDirect customer experience.”

Changes are coming, that is clear. I hope to post something brief on this Sunday or Monday, but first we have a TIPS auction today and a huge inflation report tomorrow.

David’s prediction of somewhere around 1.15% real yield for the 5-year TIPS auction is looking to be pretty spot on with real yields dropping slightly the past couple of days. I think I will pass on this auction in my taxable account, stock up on 1.1% fixed rate I Bonds this month (due to their flexibility and current fixed rate) before the fixed rate drops, and see what happens over the next 6 months. I might buy some 5-year TIPS on the secondary market if real yields increase and likely buy some 10-year TIPS at auction in January.

Thanks for all you do. I have been following you since early this year and learned a lot.

Could you at some point address the issue of why bonds with very little time remaining seem to be priced way lower than one might expect?

eg this am those expiring 1/2026 were appearing with YTM of 1.6% – attached.

Thank you,

Diane

I have written about this several times in the past. The real yield gets skewed as the maturity date gets closer. The threat of some monthly deflation is always there for TIPS maturing in January, February or April. Typically, the actual short-term nominal yield is very close to that of T-bills.

Thank you, David, for your great insights.

In my tips ladder the bonds I purchased in 2021 that mature in 2031 have market values less than their purchase price. Is there anything wrong with selling these securities for the tax loss and reinvesting the proceeds for similar securities, but not the same to avoid the wash rule?

Interesting question. The market real yield of those 2031 TIPS (1.28%) is the same as any other 2031 TIPS, but you have a loss. If you buy a Jan 2032 TIPS (real yield 1.40%, same coupon rate), you will be buying it a slightly bigger discount. The net result might be close to the same. I can’t really say if this is a good move, but since this is in a taxable account, I assume you might get a tax loss, which would help.

Is the decision to buy the five year TIPS at auction simpler if looking to purchase in a Roth IRA?

I wouldn’t say simpler, but there would be no tax consequences in the future.

David, Thank you for this info., so helpful , as usual. Do you have an estimate of what the interest rate will be for the semi-annual payments?

Regardless of that I will buy at this auction in the inflation adjusted amount of my just matured 5 yr TIPS. For many years I have bought some TIPS and max amount of I Bonds for inflation protection for safe money and now I maintain both at the adjusted amounts to be able to supplement retirement income if needed for LTC for this ~80 yr old couple.

I would guess the coupon rate will be 1.125%, but real yields can move around this week.

TIPS v I-Bond. As an example of circumstances, by the time the I-Bond hits its no penalty point (5 years) I’ll be past the magic 59.5 year old point. I’d be buying the TIPS inside an IRA, and thus if the main need for it is the emergency case such as being laid-off then it’d be accessible to me without penalty. Thus I’m thinking that the TIPS is the better choice, but I’d be very interested in people’s opinions that might contradict that.

I think the interest TIPS earn in a traditional IRA is both federal and state taxable at the time money is withdrawn, as opposed to only federally taxable (with phantom income) in a non-IRA account. I would be very interested to hear from others if this is correct. Maybe IRA keep separate records of treasuries and no state taxes are paid on that interest when funds are withdrawn. Since I am in a high tax state, buying TIPS in a regular IRA may mean paying state taxes at a future withdrawal date, which I would try to avoid.

You’re right that I do lose the protection from state taxes in the IRA which is worth considering – and would be even more in some states than others. That’s a good point.

In states with an income tax, and also that tax withdrawals from traditional IRAs, any money drawn from that account will be taxable at the state level, in addition to federal level.

Check your state law, there are 4 states with a state income tax that exempt IRA withdrawals from state income tax. There are also 3 states that Partially exempt IRA withdrawals.

But even if the earnings in an IRA are taxable, you can still time somewhat when you take the withdrawals. And in the case of the Roth you might not have to withdraw at all during your lifetime. In an ordinary account you have to pay the federal taxes whenever the instrument matures.

Actually, in a taxable account you pay taxes every year on the “phantom” gain even though it’s not realized. That’s the bad news. The good news is that taxes due on maturity are only based on the current year’s gain.

It seems to me if the real yield of TIPS and I bonds are close, it’s very tough to beat the I bond in taxable, due to it’s many advantages, especially tax efficiency, flexible redemption, etc. Conventional asset location says bonds may go in tax-deferred, due to tax drag, but there’s no tax drag with I bonds.

As I see it, an I bond in a taxable account performs exactly as it would in a tax-deferred account (TDA), assuming equivalent I bond redemption date and TIPS TDA distribution. There is zero tax drag on the I bond, and the real yield compounds with inflation (not so for TIPS, unless the coupon is somehow reinvested at the same real yield, no guarantees), and redemption/distribution tax rate are the same.

Except…I bond in taxable wins if there is any state tax.

Here are some comparisons:

https://tipswatch.com/2025/09/07/when-rates-decline-i-bonds-get-more-attractive/#comment-41374

Edward McQuarrie did a very informative analysis of TIPS in taxable vs tax-deferred (free download). The tax drag of paying ongoing taxes on the phantom interest in a taxable account can cause significant underperformance in after-tax return. This also takes into account the relative after-tax performance of stocks, say for a 60/40 or 50/50 portfolio.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5146747

Since I will have RMDs, and hold bonds in my TDA, a TIPS ladder for RMDs is my preferred choice, especially if I can lock in historically good real yields.

But reinvesting the coupon is awkward, especially before RMDs start.

Edward McQuarrie (again!) has a thought provoking piece on using TIPS coupons to extend a TIPS ladder beyond 30 years. This helps address the simplistic view that a TIPS ladder initially can’t extend more than 30 years (longevity problem), and perhaps helps in comparisons with immediate payout annuities, which have a higher initial payout and are great for longevity, but terrible for inflation, so may have half (or more or less) actual inflation impacted spending power after 30 years.

https://www.financialplanningassociation.org/learning/publications/journal/APR25-how-clients-can-sustain-real-withdrawals-beyond-30-years-OPEN

Thanks for the insight, David!

These days seem to be strange times for the world in the business of money.

I have been planning to buy a small amount of 5 year TIPS at this auction and also some I Bonds before the end of October. Unless expected real yields for TIPS move up quite a bit in the next few days (seems unlikely) I plan to reduce my TIPS purchase and allocate more to I Bonds at the 1.1% fixed rate.

The I Bond seems to be the superior choice between the two. Plus with the I Bond you know the first six month yield will be 3.98% and on 10/24 you will know the second six month yield after that (likely at or above that same yield depending on September CPI). Knowing the exact yield for year one of a five year investment (20% of the term) that will always outperform inflation by 1.1% defers federal tax, has no state tax, has deflation protection, and you could hold onto beyond five years seems like a no-brainer to me.

If I’ve already purchased my share of I Bonds and TIPS no longer seem attractive, are there other bonds worth considering?

That’s a wide-open question. Would you be interested in a 10-year nominal T-note yielding 4.02%? Seems like a reasonable yield. The 10-year TIPS is at 1.75%, so it would out-perform if inflation averages more than 2.27% over the next 10 years.

Sounds like us small investors are better off waiting to April (or even that June re-opening) as a general rule? Unless that’s washed out in the long run with the inflation adjustments that happen with the TIPS balances.

I’m not clear from the first paragraph under “Thoughts” though – would that argue that if the Fed more aggressively cuts rates between now and April the 5-year then would likely plummet even more?

My opinion is that the April and October returns end up being very similar and the market is adjusting the real yields to make them equal. So there is no advantage, generally, for an April investment over October. The June and December reopenings are easier to estimate because you’d be buying the TIPS currently trading on the secondary market.

I wonder if the annual fluctuation in bond yields is due to tax collections. As one of your other posts noted, in Feb and March of 2026, Americans will get a large refund of taxes paid in 2025. The US Government will need to borrow all of this as they are spending more than every dollar that comes in. In April, receipts will go up as most who pay taxes in, wait until the last minute. I will wait for the Spring auction for my shorter term TIPS investment.

Are TIPS a buying power loser in the long run as inflation is probably understated and taxes have to be paid on the interest and inflation adjustments?

Probably not a loser, depending on what tax bracket you’re in, there might be about 0.90% lost to taxes. The real yield will be is estimated to be around 1.10% to 1.20%