Update: 30-year TIPS auction gets real yield of 2.473%, second highest in 16 years

By David Enna, Tipswatch.com

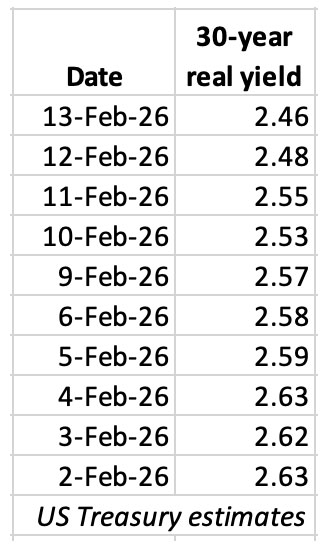

The Treasury on Thursday will offer $9 billion in a new 30-year Treasury Inflation-Protected Security, CUSIP 912810US5. The real yield to maturity and coupon rate will be determined by the auction results, but it looks likely this TIPS will get an attractive real yield, possibly close to 2.5%.

The 30-year real yield has been sinking a bit through the month of February, down about 17 basis points since February 2. But the current Treasury estimate of 2.46% remains historically attractive. In the last 16 years, only one TIPS auction of this term — last year’s August reopening — has generated a real yield that high.

Definition: The “real yield to maturity” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.46% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.46% for 30 years.

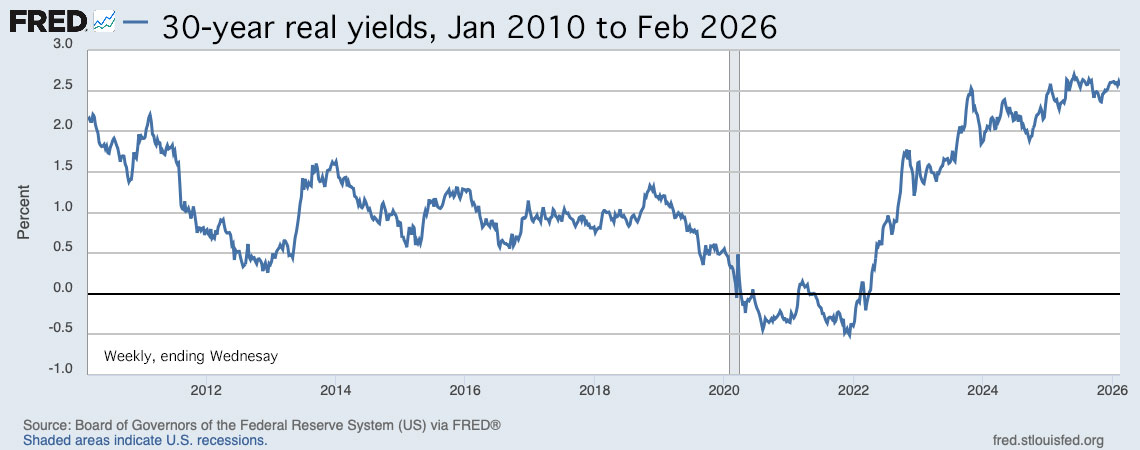

Here is the trend in the 30-year real yield over the last 16 years, showing the massive move higher since the Federal Reserve ended quantitative easing in 2022 and began raising short-term interest rates. During that time, federal deficits have also increased substantially.

A ‘peculiar’ investment

Investors need to realize that any 30-year bond — even a Treasury issue — is going to be highly volatile, rising and falling with changes in market interest rates. My advice has always been to buy TIPS with the intention to hold to maturity. That’s even more important with a 30-year TIPS, which will see values swing mightily while also having somewhat limited appeal on the secondary market.

For example, a 30-year TIPS issued in February 2022 got an auctioned real yield of just 0.195%. Today, four years later, that TIPS is trading with a market price of about 55.05, meaning the investor has now lost nearly 45% of the original purchase price. I wouldn’t have recommended buying that Feb 2022 TIPS, but today’s version with a real yield of 2.46% looks a lot more attractive.

Of course, real yields could continue rising higher. That’s the risk. But an investor committed to holding to maturity will have principal growing with inflation for 30 years, plus a coupon rate of maybe 2.375% paid out each year on rising principal.

Pricing

This is a new TIPS, so an investor will pay less than par value on the auction’s settlement date of Feb. 27. The inflation index on that date will be 0.99991, meaning the investment price will be slightly discounted. In addition, the coupon rate will be set to the 1/8th percentage point below the auctioned real yield.

So … in conclusion … the cost of this TIPS will be a bit below par value.

Inflation breakeven rate

The 30-year Treasury bond closed Friday with an estimated nominal yield of 4.69%. If this new TIPS gets a real yield of 2.46%, the 30-year inflation breakeven rate would be 2.23%, which means the TIPS will outperform the bond if inflation averages more than 2.23% over the next 30 years.

That’s a fairly high breakeven rate, but consistent with recent trends. Inflation over the last 30 years, ending in January, has averaged 2.5%.

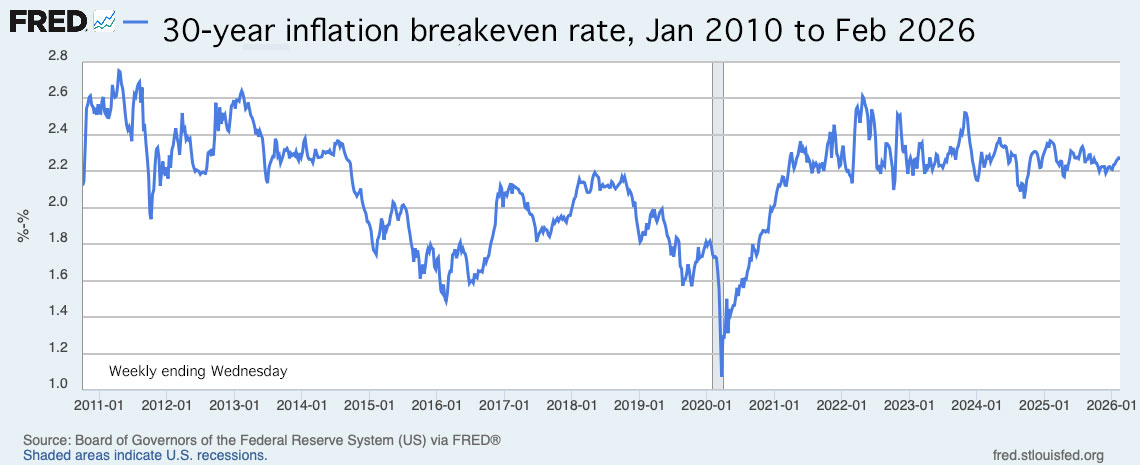

Here is the trend in the 30-year inflation breakeven rate over the last 16 years, showing the remarkably stable inflation expectations since 2021:

Thoughts

I think this TIPS is most appropriate for an investor with an expectation to live through the maturity date of Feb. 15, 2056. It would be an excellent addition, in my opinion, to a 30-year ladder of TIPS investments — for the person who can confidently hold to maturity.

Opinion: I like the idea of having principal growing with inflation, while also collecting a coupon rate of nearly 2.5% along the way. I recommend using a tax-deferred account because of the long years to the eventual payout of principal.

But I won’t be a buyer. My TIPS ladder, primarily in a tax-deffered account, extends to 2043 when I will be 90 years old. I might live longer, but probably not.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

Because I am currently traveling in Australia — 14 1/2 hours ahead of EST at the moment — I can’t say when I will be able to post results of the auction , which will close around 3:30 a.m. Friday in central Australia. I am going to be late with the news, but you can find results on this page after the close.

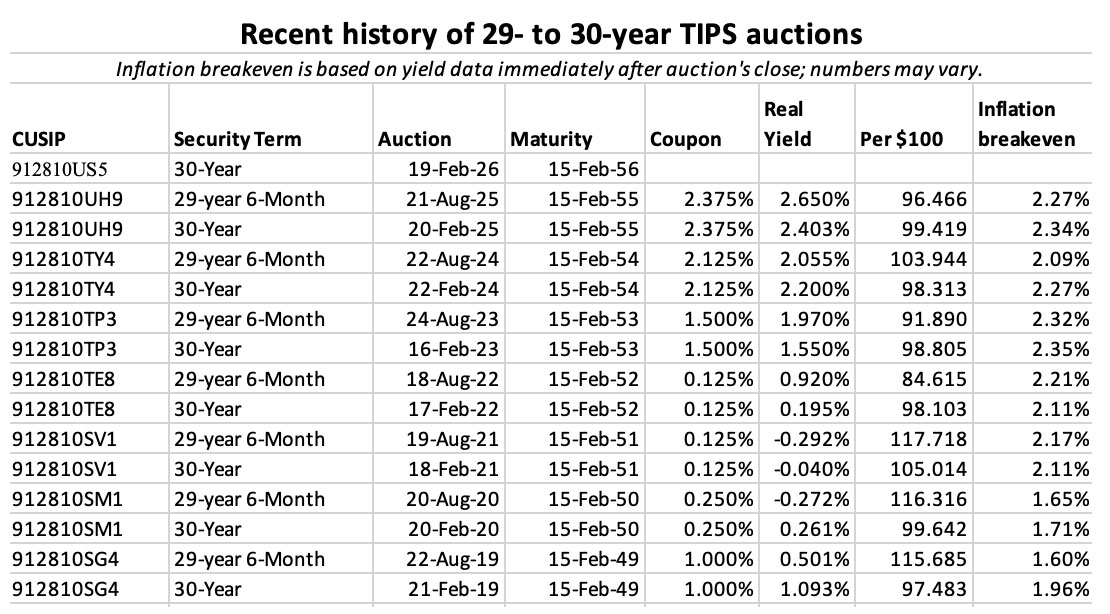

Here are auction results for the 29- to 30-year term over the last seven years.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I recall reading in an investor education piece that one is best served by pitching the duration of your bond holdings to when you will need the money. This allows you to ride out any ups and downs in interest rates and come out ahead. I would surmise that long dated bonds sport attractive yields today due to the lingering memory of 2022, “the worst bond market year in history,” when interest rates rose sharply. Investors have hesitated to jump back in. At the beginning of 2022, I held a position in the Vanguard Long Term Investment Grade fund, which is still under water by about 13% from the beginning of that year.

If you buy a bond of 30 years duration, you will likely be leaving the principle to your heirs, unless you have the wherewithal to sell it on the secondary market. I would say that during a bear market in stocks, which shouldn’t be too far off, that long dated high quality bonds are usually a good place to be.

Looks like another good opportunity to build on the bond ladder portion of a portfolio for the middle-aged and trust funds… more than double the fixed interest payout of new I-bonds.

Picking up some at auction for helping build my son’s retirement bond ladder portion of his IRA and some for a long-term trust to insure some future liabilities.

It wasn’t very long ago these 30-years TIP bonds weren’t yielding so much real yield.

30 years is a long time, certainly beyond my imagined life expectancy. My impression is most of the people who visit this site are in retirement or close to it, so a 30 year bond would be a gamble. If you have a 30 year time horizon, equities would be the way to go. I will say however that in the years soon after the launch of I-bonds, I was an enthusiastic buyer. I intend to hold them until maturity (30 years) and they have been a terrific investment (with a commensurate tax liability coming up). Time and compounding have always been an investor’s friend.

Just keep in mind that redeeming those early-year I Bonds will trigger a surprising tax hit. You may want to stagger redemptions over several years. See this: https://tipswatch.com/2024/02/04/long-time-i-bond-investors-face-a-tax-time-bomb/

In upcoming posts, please consider commenting on the buzz about Truflation and its potential risks to our TIPS ladders. Thank you David.

At age 62, a 30 year commitment seems a bit optimistic. I’m currently planning my demise for age 90 ;).

With Google Gemini, I did some math wondering what the pros and cons are of a 20 year TIPS at 2.24 and a 30 year TIPS at 2.48%.

The Scenario: Rates Rise to 4.00%

In this scenario, you buy at 2.48% and sell 20 years later when the prevailing 10-year real rate is 4.00%.

The answer is about 2.0% and you’d be better off buying the actual 20 year TIPS. While I would make the commitment “til death do us part” my heirs including charitable organizations may think or require otherwise.

I think instead I will likely put a bit more weight on my 20-25 year TIPS – I’m primarily trying to insure against high medical inflation and end of life care expenses, and a 2.25% real return just about matches medical inflation.

I’m curious at what age others’ ladders run to.

My impression is that the “best” strategy is to plan on a final SPIA bought at age 85, if you live that long and seem in good-ish health. 85 is the oldest you can get a SPIA I believe. For this reason, many folks have a TIPS ladder with even rungs through age 84 and then a “balloon rung” for age 85 what will be used to pay the SPIA premium when/if the time comes. I’ve “split the difference” with a ladder of even rungs through age 91. If I’m in good-ish health at 85, the plan is to sell the remaining rungs to buy the SPIA. If not in good health, then just keep spending them down until the end. I’m not saying this is ideal but it’s where I’ve ended it up and I’m comfortable with it.

Sally – that strikes me as a good plan. I’ve considered charitable remainder trusts depending on my mix of deferred and non-deferred funds, rules in 20 years, …

I segregate my holdings into a ladder and a remainder. The principal of the ladder is intended to be spent upon maturity. The remainder is intended to be kept indefinitely, perhaps exchanged or sold and invested elsewhere or even converted into a new ladder sometime along the way if and when it makes sense to do so, but never otherwise. I agree that it makes little sense to build a ladder more than a few years beyond one’s life expectancy.

However, very long-duration bonds, perpetual bonds, perpetual preferred stocks, and common stocks have a place in the remainder portion of a portfolio constructed in this manner. If you’re willing to hold common stocks which never have any maturity, you should also be willing to own bonds that are unlikely to mature in your lifetime. Such assets may not be for every plan, but I find it unreasonable to reject 30-year bonds because they will not mature during your expected lifetime while happily allocating 30, 40, or even 60% of your portfolio to common stocks that will never mature at all. Would you buy a common stock that pays a 2.5% dividend against its current price, which you expect will grow with the company’s earnings at a rate roughly comparable to the increase in the CPI-U? There are probably 100-200 such stocks traded on the public markets in the US alone. Most people, even already retired, are very happy to hold much lower-yielding common stocks despite the complete lack of any guarantee of future income growth or ability to redeem at par. Many people are happy to own assets that yield NOTHING AT ALL with no guarantee that they ever will (or, to put it more finely, that are unlikely to yield anything within their lifetime).

Suffice it to say, I disagree with the rejection of long-dated bonds if they don’t fit into a lifetime ladder. Long-duration bonds should be evaluated against equities and other securities that offer no plausible near-term redemption opportunity, as well as monetary metals and other tangible stores of value. They may or may not be good investments in that context, but they should not be rejected out of hand unless it is simply all you can do to build a ladder and hope you don’t outlive it. A few years ago, we were looking at negative ‘real’ TIPS yields, obviously a terrible investment and at best a speculative holding. At 2.5% (you could get 2.68% a couple weeks ago!), long-dated TIPS yield well over twice the S&P 500, which is heavily weighted toward overvalued speculative stocks that pay very little or nothing. That is not to be ignored in the perpetual portion of your portfolio, regardless of age.

I can’t disagree with your premise. My traditional IRA includes backup holdings in Vanguard Wellington and Total Bond Fund. Those investments are “perpetual”, but can easily be sold at any time.