I could say it’s been a weird week for Treasury Inflation-Protected Securities, but honestly, every week is a weird week for TIPS. The Treasury today will reopen CUSIP 912828N71, a 10-year Treasury Inflation-Protected Security that first auctioned on Jan. 21 with a coupon rate of 0.625%.

In the advance I wrote last week for this auction, this TIPS was trading on the secondary market with a real yield (after inflation) of about 0.36%. But then the market for TIPS weakened, and the yield rose to 0.47% on Tuesday. This TIPS was getting interesting.

In the advance I wrote last week for this auction, this TIPS was trading on the secondary market with a real yield (after inflation) of about 0.36%. But then the market for TIPS weakened, and the yield rose to 0.47% on Tuesday. This TIPS was getting interesting.

But then came Wednesday’s inflation report and Federal Reserve unease about rate hikes, and bam … back down to 0.36%, right were we started. (The chart at the right shows yield estimates for a full-term 10-year TIPS, probably slightly higher than this 9-year, 10-month reopening.)

And the downward trend in yield is continuing today. I’d say alarm bells are ringing against an investment in this auction. Here’s were we stand:

- Bloomberg’s Current Yields page shows this TIPS is trading today on the secondary market with a real yield of 0.29% and a cost of $103.18 for $100 of par value. Buyers will pay a premium because the yield is well below the coupon rate of 0.625%.

- Yesterday’s Closing Price on this TIPS was about $102.78 with a yield to maturity of 0.337%.

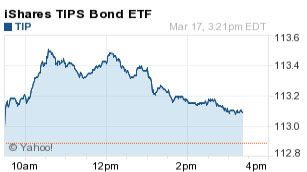

- The TIP ETF is trading sharply higher this morning at $113.41, an increase of nearly 0.5%. That means TIPS yields are declining.

Where will today’s auction yield fall? Hard to say, but it isn’t going to be pretty. It could be somewhere in the 0.25% to 0.29% range, meaning investors will be paying about 3% above par for that 0.625% coupon rate.

Although I was a buyer of this issue back in January, I will pass on this auction. This TIPS will be reopened again in May and the Treasury will issue a new 10-year TIPS in July.

NOTE: I will be tied up this afternoon at the 1 p.m. auction close and I won’t be able to post immediately after the auction. Sorry! I will post results as soon as I can.

TreasuryDirect should be posting results here soon after 1 p.m.

If you redeem anytime before 5 years, you will lose that last three months of interest. But it is possible…