By David Enna, Tipswatch.com

The U.S. Treasury just announced that its auction of a new 10-year Treasury Inflation-Protected Security resulted in a real yield to maturity of 0.045%, the lowest yield in more than three years of auctions.

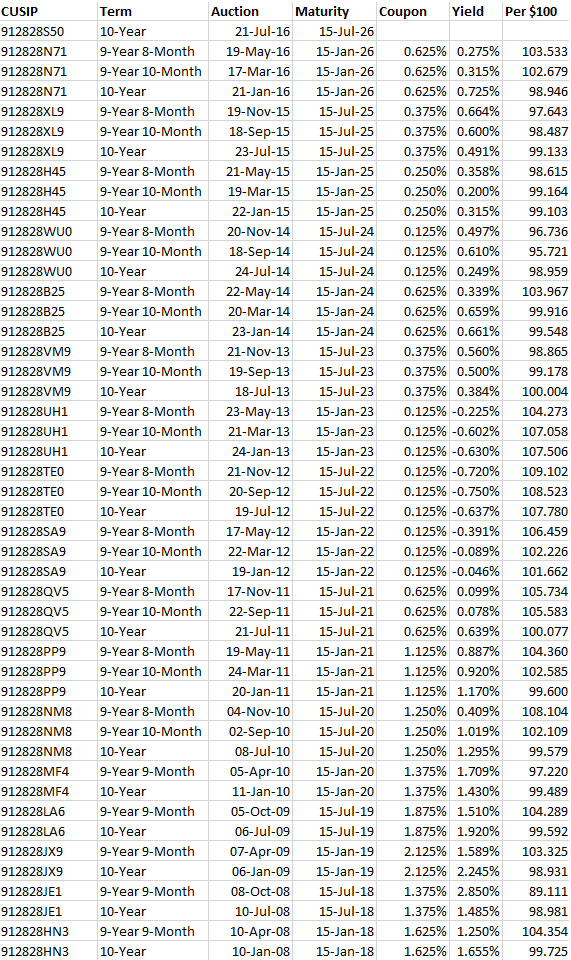

CUSIP 912828S50 gets a coupon rate of 0.125%, the lowest the Treasury will go. And that means investors at today’s auction had to pay a premium – an adjusted price of about $100.98 for $100 of par value. The adjusted price includes an inflation adjustment to principal of about 18 cents per $100 on the settlement day of July 29, when the inflation index will be 1.00184.

The real yield – which means the yield above inflation – of 0.045% was the lowest for any 9- to 10-year TIPS auction since May 2013. There have been 19 auctions of this term since then.

The Treasury had estimated Wednesday that a full-term 10-year TIPS would yield 0.130%, and the TIP ETF had been trading slightly down Thursday morning, indicating slightly higher yields. The auction result of 0.045% ran counter to those numbers, indicating buyer demand must have been strong.

Why would a TIPS barely beating inflation draw strong buyer demand?

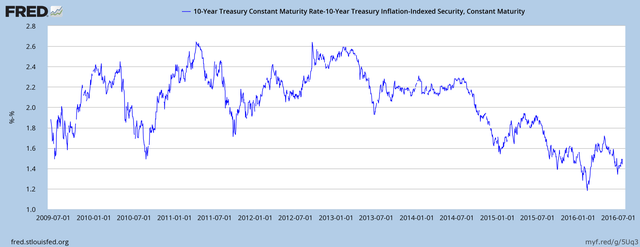

Inflation breakeven rate. One reason TIPS remain a popular investment is that even at a time of very low nominal yields, buyers can be assured with a TIPS of at least keeping pace with inflation. With the 10-year nominal Treasury trading at 1.59%, this TIPS gets an inflation breakeven rate of about 1.54%. That means if inflation averages more than 1.54% over the next 10 years, the TIPS will outperform a nominal Treasury.

Core inflation has increased 2.3% over the last 12 months, which indicates we could be entering a time of slightly higher inflation. TIPS are a good way to protect against that risk. A breakeven rate of 1.54% remains very low historically, as shown in this chart of rates since the deep recession ended in 2009:

While I didn’t find today’s auction attractive, it’s obvious that big money investors found the safety of TIPS attractive. Reuters called the demand ‘solid’ and pointed out:

The ratio of bids to the amount of 10-year TIPS offered was 2.39, up from 2.27 at the prior auction in May and the highest since March 2015.

Well Said, Interest rates are one of the hardest things to predict.