I will admit that back in 2011 I really didn’t know all that much about Treasury Inflation-Protected Securities. I thought I did. But I didn’t. I’ve had a lot of learning experiences over the last 13+ years. Readers often helped me along. A lot of very smart people read this site.

Over these years, I have covered every TIPS auction and every inflation report, so at least I have some institutional memory of truly crazy times — Federal Reserve manipulations, negative real yields, deflationary spells, 40-year high inflation, and boom and bust times for U.S. Treasurys.

On a typical day, this site gets more than 1,500 unique visitors. Last year, users came from, in order of frequency:

United States

United Kingdom

Canada

Germany

Japan

France

India

Singapore

Mexico

China

Obviously, the United States is overwhelmingly the most common source of readership, but I have had questions from all over the world.

These were the most popular articles and pages in 2024:

Notice a trend there? Every article and page is about I Bonds. Even though I try mightily I can’t generate huge interest in TIPS, which are a very attractive investment in 2025. But TIPS are also a lot more complicated and therefore, somewhat shunned.

I was talking with a New York Times reporter this week who asked me: “Are I Bonds still popular?” My answer was, “Yes, with my readers at least. This is high-quality, inflation-protected investment for people who understand the long-term time-frame.” Here is her article.

My best day for readership, WordPress tells me, is Sunday, with 18% of my views last year. I try to publish something every Sunday morning, but yeah, I take some weeks off. Sunday is a notoriously bad day for posting financial news, but my site benefits by the fact no one else is publishing on that day. I get a lot of search engine traffic on Sundays.

In 2024, this site got 932,514 page views, well below my stellar year of 2023, with 1,518,467. This just goes to show you that my site traffic depends less on the quality of my writing, and more on high rates of inflation setting off panic.

I’ll never cheer for high inflation, so I just have to accept getting about 2,555 page views a day, which is actually … incredible.

I thank you, readers. Keep participating and spread the word.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If you are an account holder at TreasuryDirect, one of your “duties” each January is to go on a hunt for your 1099s, the extremely important (and ruthlessly obtuse) tax forms the Treasury hides away deep inside the site.

You will get nothing in the mail, but you will get an email that is easy to miss.

The 2-minute video (which was produced several years ago) is actually helpful, and it plays on YouTube, so you can watch it right here:

Last week I was in TreasuryDirect looking for information and I saw 1099s for the 2024 tax year were now available. (I had not received an email as of yet, but it should be coming soon.)

As the video notes, if you are part of a couple with separate accounts, or if you have linked accounts from converting paper I Bonds, or child accounts, or separate trust or entity accounts, you will need to go to the linked accounts and get separate 1099s. In the case of a spouse, you will need to log out and re-login to that separate account to find the second 1099. Here is what TreasuryDirect says:

It is important to check ALL of your accounts, as a separate Form 1099 will be created for each one. If you have established Custom, Minor-Linked, or Conversion-Linked accounts, you must access each account to print the Form 1099 for that account.

However, if you use your TreasuryDirect account simply to buy savings bonds (I Bonds or EE Bonds) and didn’t redeem any or have any mature in 2024, there will be no taxable transactions and you won’t have 1099s. You will see this on TreasuryDirect’s ManageDirect page:

TreasuryDirect is NOT going to mail you these forms. You need to hunt them down.

Important: Once you are inside the account section of TreasuryDirect, never click on your browser’s back button. If you do, you will be booted out of TreasuryDirect and you will have to log in again. To navigate, either click on the top row of tabs or click “return” at the bottom of most pages.

Here is the basic step-by-step process for finding each set of 1099s:

Log into your TreasuryDirect account on this page. Click “Next.”

Enter your account number and click “Submit.”

After you enter the account number, you will get a message that a verification code has been sent to the associated email address. Open the email, copy the code and paste it in the box. Click “Submit.”

Enter your password and click “Submit.”

Now you are on your MyAccount page on TreasuryDirect. From here you can click on your Investor InBox in the upper navigation to see further instructions. The message will be titled “Tax Statement Notification.”

Important tax information for the recently concluded tax year is now available. The Form 1099 may be accessed through the ManageDirect tab in your TreasuryDirect account. A Form 1099 will NOT be mailed to you.

Next, click on the “ManageDirect” link in the upper navigation. Under the heading, Manage My Taxes, select the link for the 2024 tax year. Then click the link: “View your 1099 for tax year 2024.” (Make sure to select 2024, not 2025.)

At this point, you may get a huge listing of all of your interest payments, savings bond redemptions, potential capital gains and original issue discount accruals for Treasury Inflation-Protected Securities.

TreasuryDirect does not offer an easily printable .pdf version of this form. To print it, click anywhere on the browser page and hit CONTROL P on a PC or COMMAND P on a Mac. This should open up a dialog to print the pages. (Mine was 12 pages long.)

Print the 1099. (Your computer may also give you the option to “print to .pdf” which will allow you to save the document before printing.)

Don’t have a printer? You can copy the entire text of the 1099 and paste it into a text or Word document. Save that file for reference when you fill out your tax return.

At the bottom of the page, click on “Return.” Repeat the process for any additional spousal or linked accounts.

One bit of comedy from TreasuryDirect: Once you open your 1099 page, there will be no top tabs and you will need to scroll all the way to the bottom (12 pages!) to get to the “Return” button. Do not click on the back arrow or you will get logged out of TreasuryDirect.

Examine the 1099

There is a lot to see here, and you don’t want to miss anything that needs reporting to the IRS. On a 1099 from any brokerage or bank, everything is nicely organized and summed up, with clear references to the proper boxes on your tax filing. Not so with TreasuryDirect. In fact, this 1099 is actually a collection of 1099 forms, each with special purposes.

Form 1099-INT Interest Income

If you invested in any T-bills, Treasury notes or bonds, TIPS or redeemed savings bonds in 2023, you are going to see all interest-paying transactions listed here. In 2024 I was rolling over staggered 13- and 26-week T-bills at TreasuryDirect, plus had a collection of TIPS, plus redeemed a couple 0.0% I Bonds, so my list was enormous: 33 items. Example:

At the bottom of this long list, way at the bottom, is the total. Scroll all the way back up to the top to see that this total is Interest On U.S. Savings BondsAnd Treas.Obligations and it goes in Ref. Box 3 on the federal tax form when you are filling out the section for 1099-INT. Here is the definition of Box 3:

Shows interest on U.S. Savings Bonds, Treasury Bills, Treasury Notes, Treasury Bonds and Treasury Inflation-Protected Securities (TIPS). … This interest is exempt from state and local income taxes.

You want to make sure the interest gets recognized as coming from U.S. Treasurys, because it will be free of state income taxes.

If you had any proceeds withheld for tax purposes (highly unlikely) those totals will be listed in column 5 of this section.

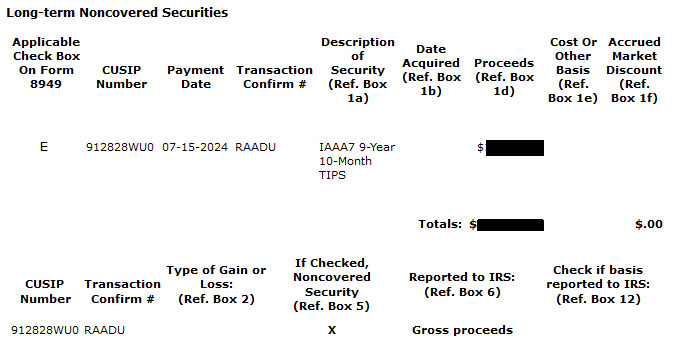

Form 1099-B Proceeds from Broker and Barter Exchange Transactions

There are several sections to form 1099-B and I generally have just a few transactions listed here. This seems like a relatively new part of TreasuryDirect reporting, which shows an Accrued MarketDiscount on longer-term investments that matured in 2024.

This is my only 1099-B item for 2024, and it is a doozy:

This is all for a single 10-year TIPS, CUSIP 912828WU0, that matured on July 15, 2014. The Treasury calls this a “noncovered security,” which I translate to mean, “We have no idea how much you paid for this.” The 1099 instructions note: “Generally, a noncovered security means: debt instruments acquired before 2014.” But I bought it in 2014!

The problem is that Treasury is reporting the “gross proceeds” to the IRS and so I will have to try to figure out a way to keep from paying taxes on that total amount, much of which was my cost basis. The 1099 instructions are not particularly helpful. My records show my initial discount at purchase was about $400, and that is probably what will end up being taxable.

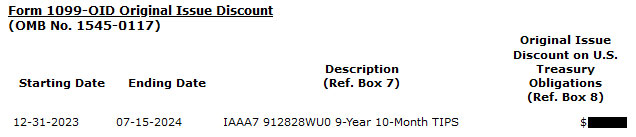

Form 1099-OID Original Issue Discount

This is a very important section for investors who hold TIPS at TreasuryDirect. The 1099-OID lists annual inflation accruals for every TIPS held in the TreasuryDirect account in 2024. These inflation accruals are federally taxable in the year they were earned, even though they were not paid out but just added to principal.

Long-time investors in TIPS are familiar with the 1099-OID, but new investors at TreasuryDirect need to pay heed to this section and report it on their federal tax return.

At the bottom of the list will be the total for all your TIPS holdings. TreasuryDirect notes:

Report this amount as interest income on your federal income tax return. … This OID is exempt from state and local income taxes.

Final thoughts

I am no tax expert, so nothing you just read should be considered tax advice. Still, getting these 1099s from TreasuryDirect is EXTREMELY IMPORTANT. And make sure you do this for every account where you had taxable activity (such as maturing short-term T-bills or redemptions of I Bonds).

You are going to get one email with a fairly cryptic message. That’s it. Nothing in the mail. Nothing you can download to Quicken. No .pdf. No easy-to-read tax summary like you receive from your broker. It’s up to you to go to TreasuryDirect, find the 1099s, print them, decipher them and report them on your tax return for 2024.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The Treasury’s auction of $20 billion in a new 10-year Treasury Inflation-Protected Security — CUSIP 91282CML2 — generated a real yield to maturity of 2.243%, the highest for this term at auction since January 2009.

The auction appeared to generate “okay” demand, with a bid-to-cover ratio of 2.48, fairly standard for this term of TIPS. The “when-issued” auction prediction was for a real yield of 2.232%, so the result of 2.243% indicated less-than-stellar demand.

Nevertheless, this is a very good auction result for investors. The real yield to maturity was the highest for this term since a new 10-year TIPS was auctioned in January 2009 with a real yield of 2.245%. Just like that 2009 auction, CUSIP 91282CML2 gets a coupon rate of 2.125%, also the highest in 16 years.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.243% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.243% for 10 years.

Here is the trend in the 10-year real yield over the last five years, showing that today’s real yield is approaching secondary-market highs of October 2023:

Click on image for larger version.

Obviously, real yields have moved dramatically higher since the Federal Reserve’s aggressive pandemic-era quantitative easing programs ended in early 2022. Today’s 10-year real yield is again historically attractive.

Pricing

Because the coupon rate was set at 2.125%, below the auctioned real yield, investors got CUSIP 91282CML2 at a discounted unadjusted price of 98.951405. On the settlement date of Jan. 31, it will carry an inflation index of 0.99972. With that information, we can calculate the investment cost of $10,000 par at today’s auction.

Par value: $10,000.

Actual principal purchased: $10,000 x 0.99972 = $9,997.20

Cost of investment: $9,997.20 x 0.98951405 = $9,892.37

+ Accrued interest of $9.39

In summary, an investor at today’s auction is paying $9,892.37 for $9,997.20 of principal on the settlement date of Jan. 31. After that, the investor will receive inflation accruals plus an annual coupon rate of 2.125% until maturity. The accrued interest of $9.39 will be returned at the first coupon payment in July.

Interesting side note: The coupon rate of this inflation-adjusted TIPS, at 2.125%, is higher than the 10-year Treasury note’s nominal yield of less than 2.0% from August 2019 to March 2022. Things have changed.

Inflation breakeven rate

With the nominal 10-year Treasury note trading with a yield of 4.64% at the auction’s close, CUSIP 91282CML2 gets an inflation breakeven rate of 2.40%, a bit higher than recent results for this term. It means the TIPS will outperform a nominal Treasury if inflation averages more than 2.4% over the next 10 years.

That breakeven rate is high enough to make the nominal 10-year Treasury attractive, but I’d still prefer the inflation protection the TIPS provides. Here is the trend in the 10-year inflation breakeven rate over the last 5 years, showing the fairly stable pattern in the 2.0% to 2.5% range:

Click on image for larger version.

Reaction

As I have been noting for months, I was a buyer at this auction because CUSIP 91282CML2 is the first TIPS in history to mature in 2035, and I wanted to fill that spot on my TIPS ladder. The real yield of 2.243% was a bit of surprise, about 4 basis points higher than I thought looked likely earlier in the morning.

Also, as I predicted (this one was obvious), the TIPS auctioned with an investment cost below par value. This isn’t a huge deal, but a plus. I am pleased. Obviously, real yields could continue to climb higher, but this was a historically attractive mark.

There will be 5 more 10-year TIPS auctions in 2025. CUSIP 91282CML2 will be reopened at auction on March 20, and then again in May. Another new 10-year TIPS will be auctioned in July and then reopened in September and November.

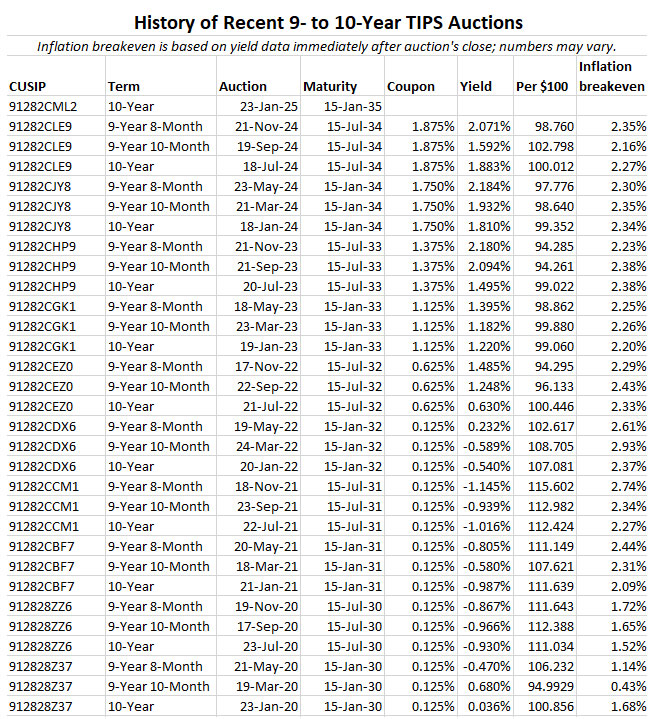

Here is a recent history of TIPS auctions of this term, showing that as recently as three years ago, 10-year TIPS were auctioning with negative real yields:

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

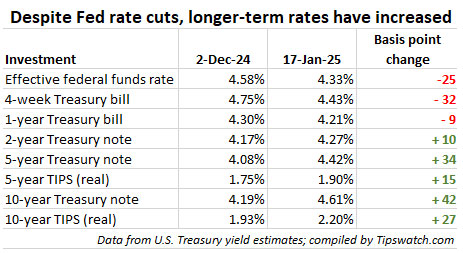

I picked up the December issue of Kiplinger Personal Finance from my nightstand last week and began paging through. And chuckling. Why? Because nearly the entire issue was devoted to investing in a new era of declining interest rates.

Some sample headlines and topics:

How lower interest rates affect your finances.

Dividend payers are poised to benefit from falling rates.

At long last, rates are dropping.

Rate-cut winners and losers.

Columnist: “I am wary of long-term Treasurys.”

As it turns out, Kiplinger got it wrong. Even though the Federal Reserve continued to cut its federal funds rate by 25 basis points in November and again in December, these cuts had no effect on medium- and longer-term Treasurys. In fact, both nominal and real yields have increased strongly since December 1, 2024.

Let’s give Kiplinger a break, however. I was right with them in expecting to see at least slightly lower medium-term Treasury rates going into 2025. Instead, because of positive economic news and uncertainty about policies of the incoming president, medium- and longer-term rates have been rising.

And this all leads up to Thursday’s auction of a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CML2. This will be the first TIPS in history to mature in 2035, and because of that I have long been targeting a purchase at this auction. I need to fill year 2035 in my TIPS ladder. I am pleased to see the potential real yield hovering around 2.20%, despite slipping a bit last week because of a so-called “soft” December inflation report.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.20% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.20% for 10 years.

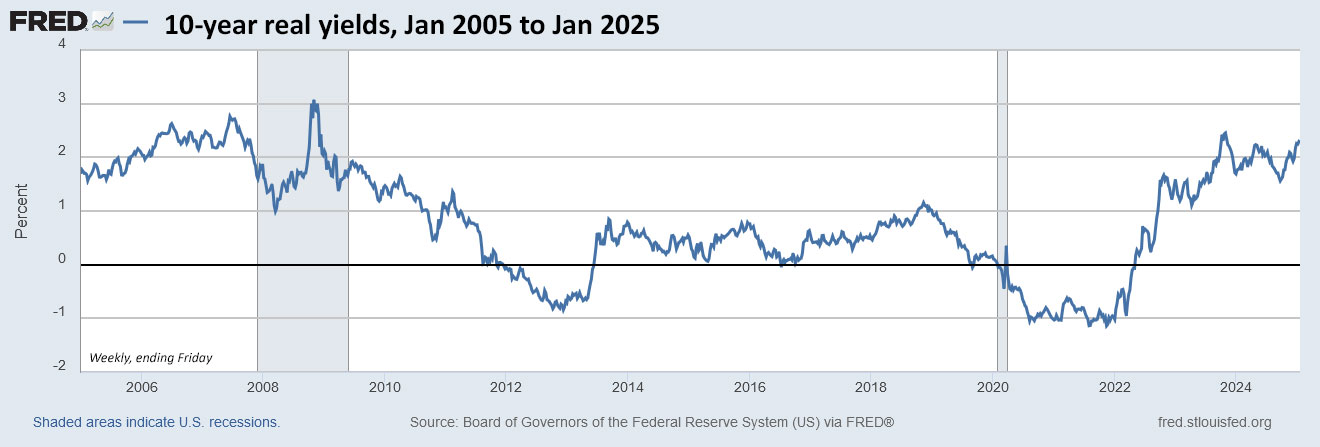

By historical standards, a real yield of 2.20% is attractive. It is actually quite a bit above the historical real return (1.80%) of 10-year Treasurys from 1928 to 2024. Take a look at this chart of the 10-year real yield over the last 20 years:

Click on image for larger version.

The lower yields from 2011 to early 2022 were caused by aggressive bond-buying programs of the Federal Reserve, which kept longer-term interest rates suppressed. Now we are in an era of moderate quantitative tightening and yields have returned to more normal levels.

So for me– if rates hold this week — I am going to jump at Thursday’s chance to lock in a 10-year TIPS with a real yield of around 2.20%. A few more things to consider:

The Treasury is offering $20 billion of this TIPS, the highest ever for an auction of this term. Last year’s January auction was for $18 billion.

If the real yield to maturity ends up above 2.20%, it would be the highest real yield for any 9- to 10-year TIPS at auction since January 2009.

If the coupon rate is 2.125% or higher, it would be the highest for this term since January 2009.

Pricing

This is a new TIPS, so its coupon rate will be set at the 1/8th percentage point level below the auctioned real yield (most likely 2.125% or 2.250%). Because of that, this TIPS is going to auction at a slightly discounted price. Plus, its inflation index on the settlement date of Jan. 31 will be 0.99972, providing another very slight discount.

In other words, a purchase of $10,000 par of this TIPS is probably going to cost just a little less than $10,000 or maybe right at $10,000 after you add in a small amount of accrued interest, maybe $10 or so.

Inflation breakeven rate

With the 10-year nominal Treasury note closing Friday at 4.61%, this TIPS currently would have an inflation breakeven rate of 2.41%, higher than any auction of this term since September 2022. However, U.S. inflation has averaged 3.0% over the last 10 years, so the number isn’t unreasonable. (In my opinion, a 10-year nominal Treasury at 5% would start to get interesting.)

Here is the trend in the 10-year inflation breakeven rate over the last 20 years:

Click on image for larger version.

That’s a crazy chart, isn’t it? The shaded areas show the strong effect recessions have on inflation expectations. And yet, over the 20 years, the 10-year inflation breakeven rate never quite reached the 3.0% level of the 2014-to-2024 period. Remember: the inflation breakeven rate is a measure of sentiment, not at all an accurate predictor of future inflation.

Buy now … or wait?

Several readers have asked me why I am going to buy CUSIP 91282CML2 at Thursday’s auction (if yields hold reasonably steady). Why not just wait and buy it later on the secondary market? Waiting could definitely work. … Or not.

Waiting is a bet that real yields will continue to rise, and that definitely could happen. … Or not. My philosophy of TIPS investing is buy a yield you like and don’t look back.

Buying at auction assures me of getting the same high yield as the big-money investors, with no bid-ask spread. Also, because this is a new TIPS, you may not see many small-lot sale offers on the secondary market for several weeks.

The negative of an auction is the uncertainty about the actual yield you will receive. The advantage of the secondary market is that you can see exactly the price and real yield you will get. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference.

So either way is probably fine, auction or secondary market. I am choosing to go with the auction because this is a new TIPS with a good yield and good pricing. Over this week, you can track the Treasury estimate of the 10-year real yield on this page. Financial markets will be closed Monday in honor of Martin Luther King Jr.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

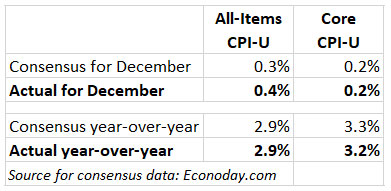

The December inflation report issued this morning by the Bureau of Labor Statistics can be viewed only one way: U.S. inflation is not yet under control.

Seasonally adjusted inflation increased 0.4% in December, higher than expectations. Annual inflation increased from 2.7% to 2.9% in December, which matched expectations but isn’t great news. Core inflation, removing food and energy, increased 0.2% for the month and 3.2% for the year, breaking a three-month string at 3.3%. That’s the one bit of positive news.

So officially, U.S. inflation ran at 2.9% for the year 2024, down from 3.4% in 2023.

Gasoline prices reentered the inflation picture in December, rising 4.4% for the month, but fell 3.4% for the year. Fuel oil prices also rose 4.4% for the month. The BLS said energy prices accounted for about 40% of the overall CPI increase. Also from the report:

Shelter costs showed no sign of abating, rising 0.3% for the month and 4.6% for the year.

Food at home prices rose 0.3% for the month and 1.8% for the year.

Apparel prices rose 0.1% for the month and just 1.2% year over year.

Airline fares rose 3.9% for the month and 7.9% for the year.

Costs of used cars and trucks rose 1.2% for the month but were down 3.3% for the year.

New vehicle prices rose 0.5% in December but fell 0.4% for the year.

Motor vehicle insurance costs rose 0.4% for the month and 11.3% for the year.

Looking for a bright spot? The costs of alcoholic beverages fell 0.3% for the month and rose just 1.4% for the year.

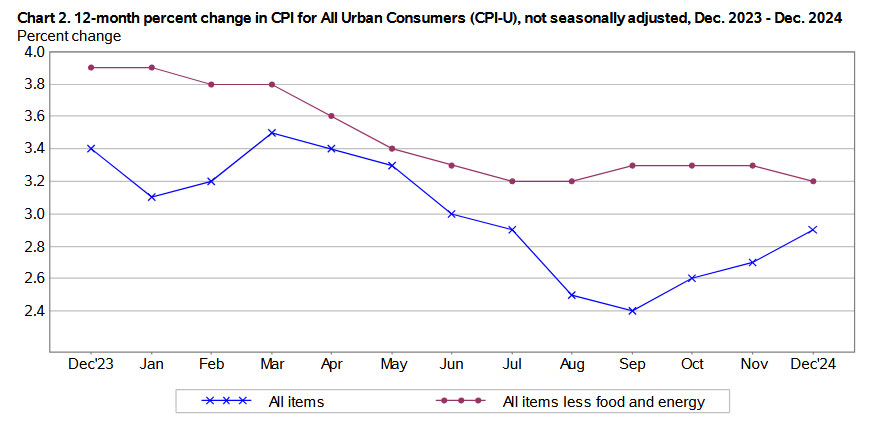

There aren’t a lot of bright spots in this December report, with prices increasing across a broad spectrum of products and services. Here is the trend in annual inflation rates over the last year, showing the clear trend of higher all-items inflation:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For December, the BLS set the inflation index at 315.605, an increase of 0.04% over the November number.

It is normal for non-seasonally adjusted inflation to run lower than official inflation in December. In fact, last month was the first December since 2021 to not record non-seasonally adjusted deflation for the month. The numbers will turn around in January, with non-seasonal running higher than seasonal.

For TIPS. December inflation means that principal balances for all TIPS will increase by 0.04% in February, after falling 0.05% in January. Here are the new February Inflation Indexes for all TIPS.

For I Bonds. The December report is the third of a six-month string that will determine the new variable rate, to be reset as of May 1 and eventually roll into place for all I Bonds. As of December, inflation has increased just 0.1% for the three months, translating to a variable rate of 0.2%.

However, that is pretty meaningless. Non-seasonally adjusted inflation will pick up in January. For example: In 2023, inflation for October to December was -0.34%, but the next three months brought the variable rate up to 2.96%. Here are the data:

What this means for future interest rates

This might not be a “nightmare” inflation report for the Federal Reserve, but it certainly isn’t good news. Annual inflation hit a low of 2.4% in September but now has ticked steadily higher to 2.9%. Core inflation has been steadily above 3.0%, but finally ticked lower in December.

In Bloomberg’s morning report, some analysts are pointing the drop in core inflation has a strong positive. This is from Anna Wong and Stuart Paul of Bloomberg Economics:

We think the Fed will likely view the December CPI report favorably. We still expect officials to hold rates steady in January, but the report bolsters the case for the dot plot’s outlook of 50 basis points of rate cuts this year.

A counter view from Bloomberg’s Molly Smith:

While the easing in the CPI is welcome, Fed officials would need to see a series of subdued readings after months of elevated prints to reassure them that inflation progress has resumed. Lingering price pressures have contributed to a deep selloff in global bond markets and fueled concerns that the Fed eased policy too quickly at the end of last year.

My opinion: For the time being, especially as we enter a period of uncertain government policies, I think the Fed is likely to delay any future cuts in interest rates. Before any change, it will begin sending signals. For now, we are on hold.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am definitely not a fan of purchasing TIPS with negative real yields. My goal is to get a safe…