A predictable result in unpredictable times.

By David Enna, Tipswatch.com

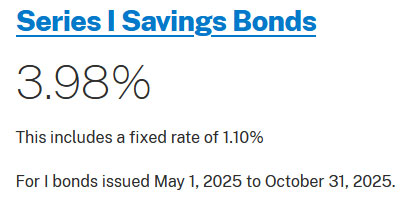

The U.S. Treasury held to past practices today, setting the new fixed rate for the U.S. Series I Savings Bond at 1.10%, as expected, and the new composite rate at 3.98%, also expected.

This was welcome news, indicating the new administration will maintain consistent support for the savings bond program.

No news release has yet been posted; that should come tomorrow. Bizarrely, just a few minutes after the new rate was posted at 8:30 a.m. on TreasuryDirect, it was taken down and the site was again showing the 3.11% composite rate in effect through April 30.

At 10:10 a.m., the site went live again with the new rate, 3.98%.

In recent years, TreasuryDirect has posted the new rate a day early. Even though the rate change officially takes effect May 1, any purchases today at TreasuryDirect will get the new rates. I confirmed this with a test order this morning:

For the time being, I am going to ignore this flip-flop and assume the fixed rate was set at 1.10%, variable rate at 2.86% and composite rate at 3.98%. And that is what an investor will get with a purchase today through late October.

Update: Here is TreasuryDirect’s news release on the new rates.

What is an I Bond?

The U.S. Series I Savings Bond is a U.S. Treasury security that protects the investor against increases in inflation:

- The fixed rate will never change. Purchases through Oct. 31, 2025, will have a fixed rate of 1.10%, down from the previous rate of 1.20% in effect through April.

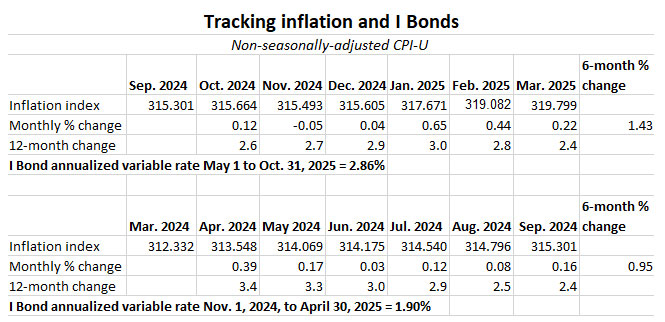

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is now set at 2.86%, based on inflation of 1.43% from October 2024 to March 2025. This new rate applies to all I Bonds, no matter when they were issued. (However, the effective start date of the new interest rate will vary depending on the month you bought the I Bond.)

- The I Bond’s current composite rate is now 3.98%, annualized, for a full six months for any bond purchased from May to October 2025. That is an increase from 3.11% for I Bonds purchased in April.

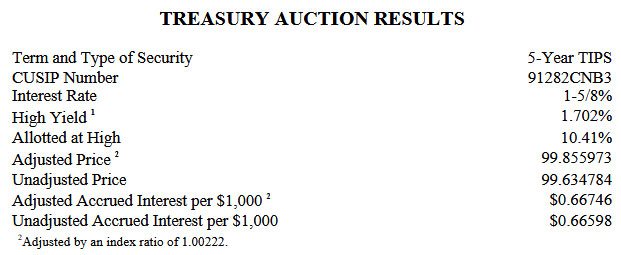

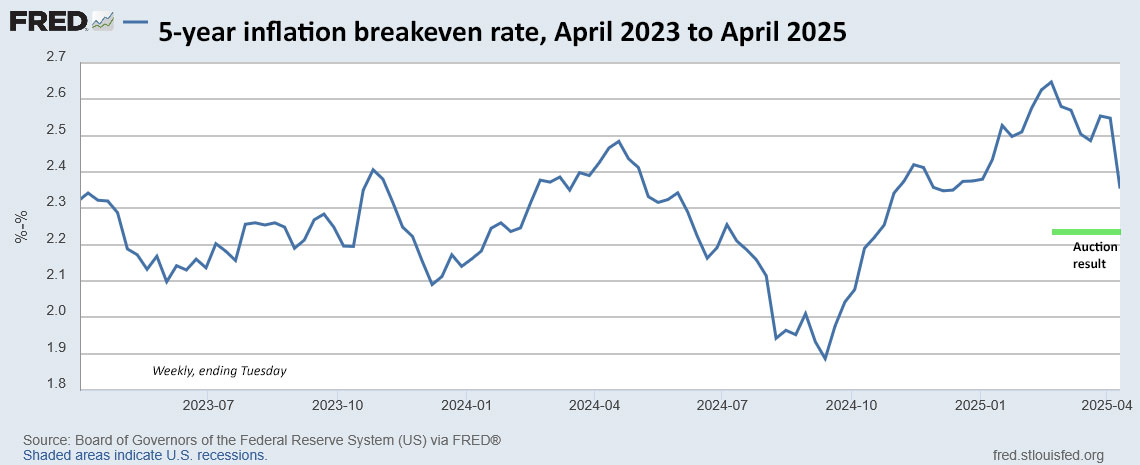

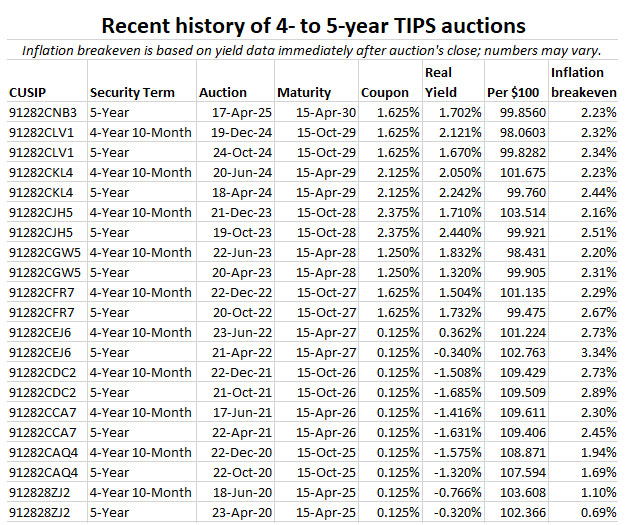

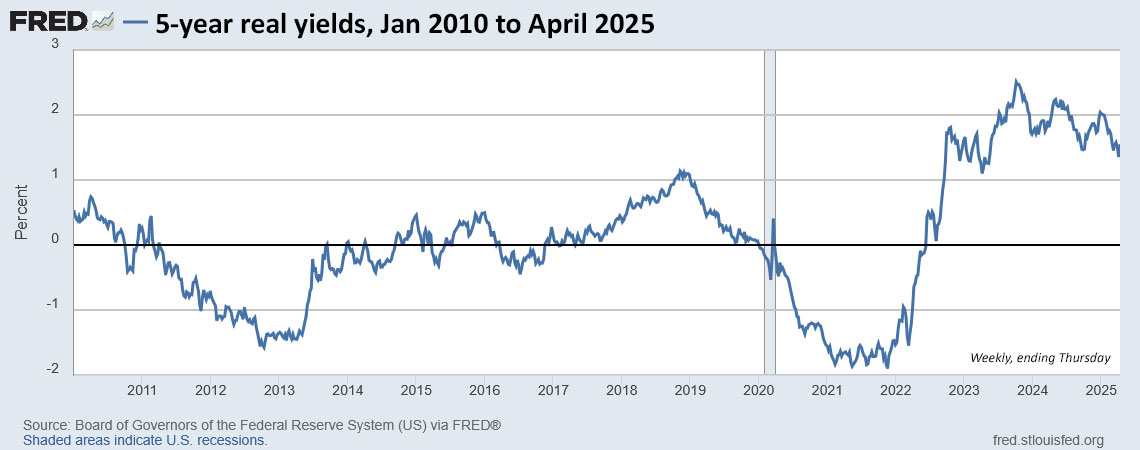

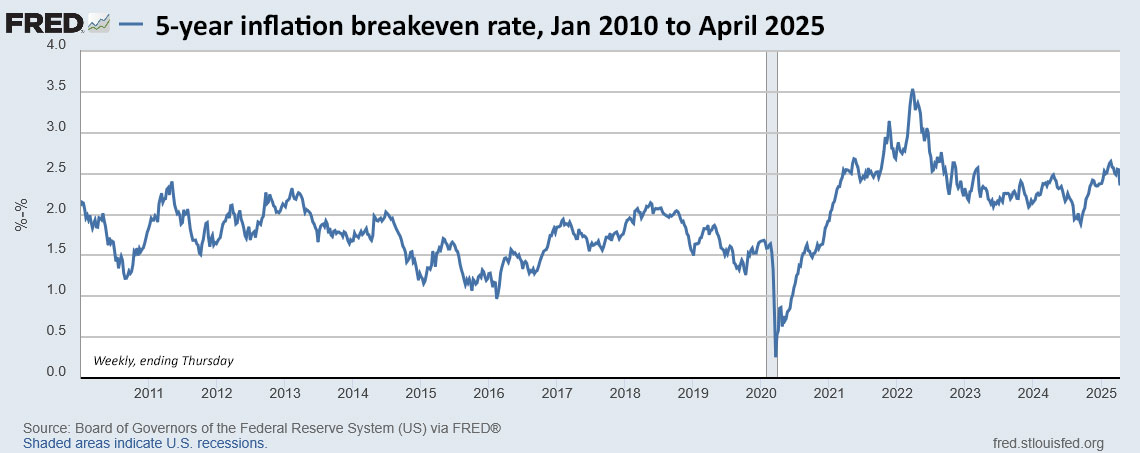

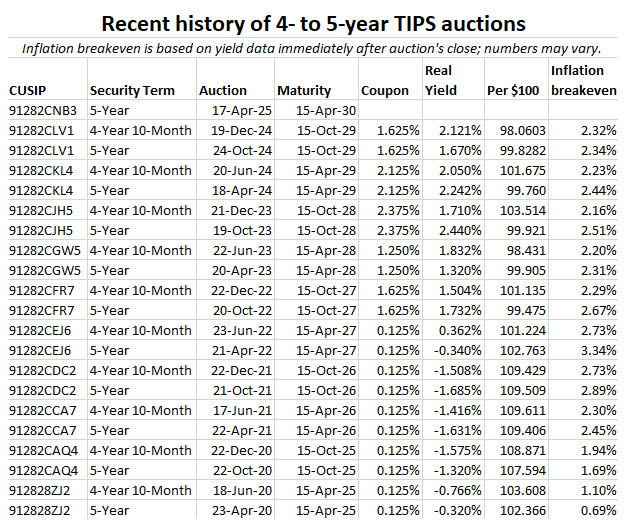

The fixed rate. The Treasury has not revealed a method for setting the I Bond’s fixed rate. But over the last decade, it appears to have leaned heavily on this formula for setting the I Bond’s new fixed rate: Apply a ratio of 0.65 to the average 5-year TIPS real yield over the preceding six months. It seems to have held to that formula for this reset:

This was one area that concerned me in the new administration, because changes in policy are always possible. But today’s decision is reassuring that we can expect Treasury to follow predictable policies of the past.

The variable rate. This component of the I Bond’s composite rate wasn’t in doubt. It is based on six months of inflation, in this case 1.43% from October 2024 to March 2025. Double that rate and you get the annualized variable rate, 2.86%.

Again, it is worth noting that this new variable rate will go into effect for all I Bonds, no matter when they were issued. So if you are holding 0.0% fixed rate I Bonds, you will get 2.86% interest for six months. The starting month of the new rate depends on when you initially purchased the I Bond.

The composite rate. The I Bond’s composite rate isn’t calculated by simply adding the variable and fixed rates. The Treasury uses a formula that adjusts for compounding factors of the fixed rate:

[Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

So with a fixed rate of 1.10% and inflation rate of 1.43%, the new composite rate calculation looks like this:

0.011 + (0.0286) + (0.0001573) = 0.0397573

Rounding gives you 0.03976. Turning the decimal number to a percentage gives a composite rate of 3.98%. This rate is in effect for six months for I Bonds purchased from May to October 2025. I Bonds purchased in the November 2024 to April 2025 period will eventually get a composite rate of 4.08% for six months.

What this all means

Let’s assume the posting, then pull-down, then re-posting of the new composite rate was an accident and not the result of some Treasury official running down a hall screaming, “We can’t do that!” The fixed rate is the key to an attractive I Bond, and a rate of 1.10% above inflation remains appealing.

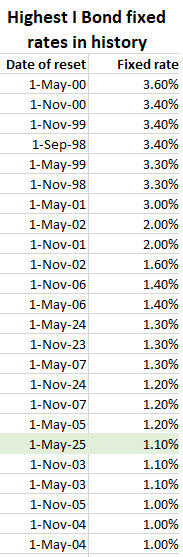

The chart shows all the times in history, dating back to September 1998, that the I Bond’s fixed rate was 1.0% or higher. While May 2025 is low on this list, note that only four of these high-level resets happened in the last 17 years.

I Bonds are a unique investment, one of the safest in the world, because they are backed by the U.S. government and provide protection against official U.S. inflation, no matter how high it rises. I Bonds earn tax-deferred interest, are free of state income taxes, can never lose a cent of value and have a flexible maturity date.

Purchases are limited to $10,000 per person per year, unless you add to holdings through gift-box, trusts, or business-owner strategies. So it makes sense to buy nearly every year, but especially when the fixed rate is appealing, as it is today. I consider I Bonds a cash-equivalent investment. Hold them for one year and cash out with a three-month interest penalty, or redeem in five years with no penalty. All the while, there is zero chance your investment will lose value.

Now that we are in the May to October purchase period, you should feel no rush to invest. If you want the I Bond issued in May, wait until late in the month, like May 28, to make the purchase. You earn a full month of interest no matter when you invest.

Another option is to hold tight until mid-October, to see where inflation has been heading and also get a reading on the next fixed rate, to be reset November 1.

I made my I Bond purchases earlier this year, so I am done. Let me know what you are thinking in the comments area below.

Update on EE Bonds

The Treasury set the new fixed rate for EE Bonds at 2.70%, up from the current 2.60%. It also maintained the doubling period of 20 years, meaning that an EE Bond will earn an effective rate of 3.53% if held for 20 years. This compares with a the 20-year Treasury bond, currently yielding 4.66%.

It is hard to make a case for EE Bonds as a short-term investment (especially because of the three-month interest penalty for redemptions before five years) or long-term holding (because you can do much better with a Treasury bond.)

If short-term interest rates fall dramatically before November (unlikely) the EE Bond could begin to look attractive. Otherwise, this savings bond is a non-factor.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

There are about 163 million workers in the US with an average salary of about $70k. About 12 million or…