Troubling conclusion: U.S. inflation is no longer slowing and remains too high.

By David Enna, Tipswatch.com

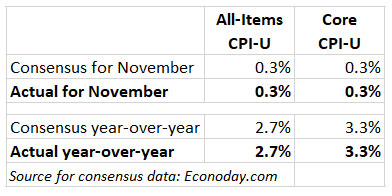

Although annual U.S. inflation rose from 2.6% in October to 2.7% in November, financial markets are likely to view today’s report as a positive, because it matched expectations.

The U.S. Bureau of Labor Statistics reported this morning that both all-items inflation and core (which excludes food and energy) rose 0.3% in November. Those increases matched economist expectations, which – surprisingly – have been fairly accurate recently.

This isn’t exactly cause for celebration, as annual inflation remains too high and seems to be drifting higher. Core inflation has increased 0.3% in each of the last three months. But the stock and bond markets like predictable results. Stocks were up in premarket trading.

The BLS again pointed to shelter costs as a primary inflationary factor, with costs rising 0.3% for the month and 4.7% for the year. That increase, the BLS said, accounted for about 40% of the overall all-items increase. Also, gasoline prices increased 0.6% for the month, but have fallen 8.1% over the last year. The November increase broke a seven-month trend of declining gas prices. More from the report:

- The costs of food at home increased 0.4% for the month and are up only 1.6% for the year. But the costs of dining out — food away from home — have increased 3.6% year over year.

- Apparel costs were up 0.2% after falling 1.5% in October.

- Costs of new vehicles rose 0.6% but are down 0.7% for the year.

- Used car and truck prices rose a sharp 2.0% in November after rising 2.7% in October. But they are still down 3.4% year over year.

- Airline fares rose 0.4% for the month and 4.7% for the year.

- Costs of medical care services rose 0.4% in November and 3.7% for the year.

- Motor vehicle insurance costs rose only 0.1% for the month but remain 12.7% higher for the year.

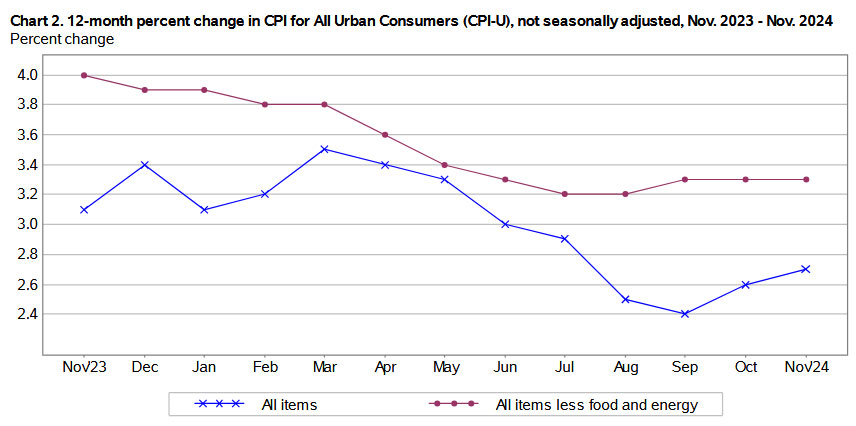

The BLS noted that price increases were widely spread across all major categories. Here is the trend for annual all-items and core inflation over the last 12 months:

This chart presents strong evidence that declines in U.S. inflation have ended, for the time being.

What this means for TIPS and I Bonds

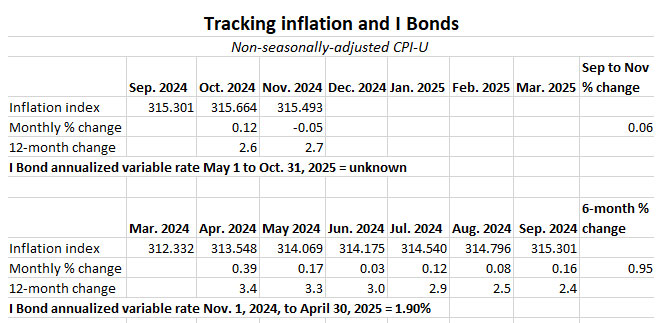

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For November, the BLS set the CPI-U index at 315.493, a decrease of 0.05% from the October number.

For TIPS. The November inflation report means that principal balances for all TIPS will decline by 0.05% in January, after rising 0.12% in November. It is normal to see deflationary non-seasonal numbers in November and December. For example, in 2023, non-seasonal inflation declined 0.2% in November and 0.1% in December.

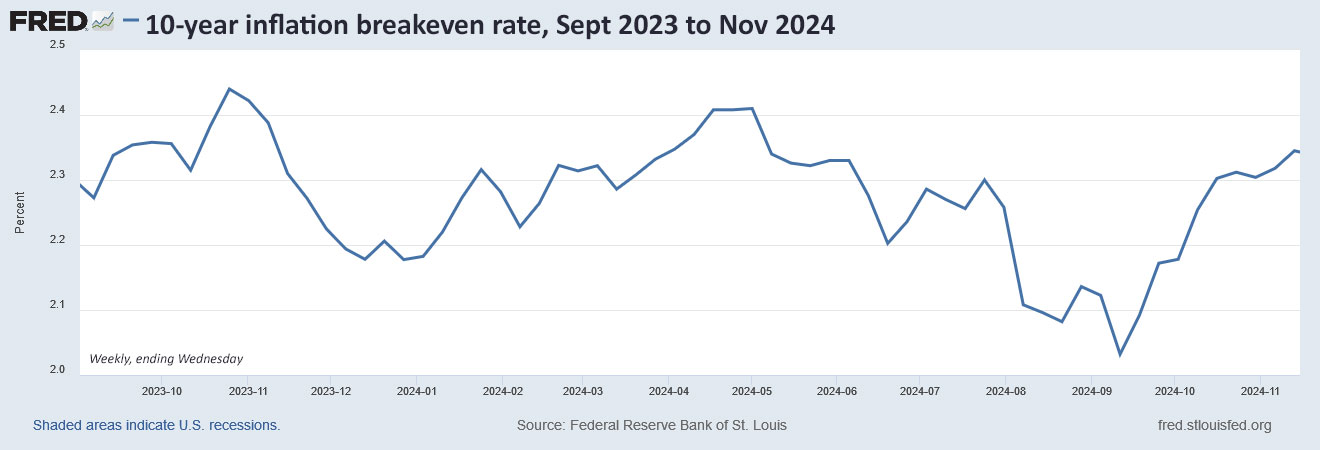

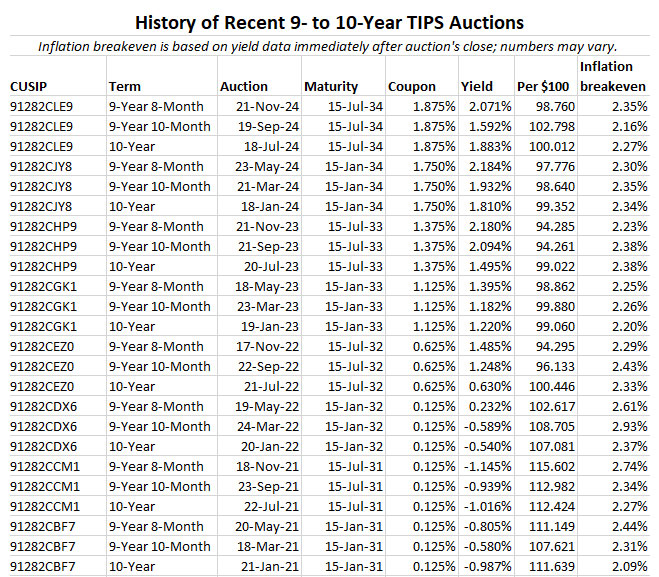

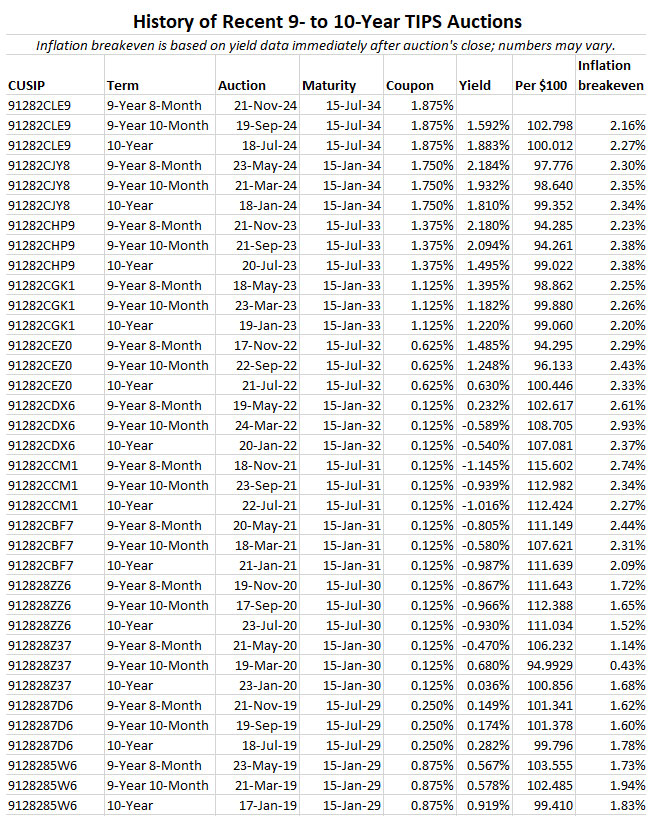

This is likely to reverse course in January. Earlier this year, for example, non-seasonal inflation rose 0.54% January while adjusted CPI-U increased 0.3%. Here are the January inflation indexes for all TIPS.

For I Bonds. The November inflation report is the second in a six-month string that will determine the I Bond’s new variable rate, which will be reset May 1. So far, after two months, inflation has increased just 0.06%, which would translate to a variable rate of just 0.12%. This is meaningless. It’s too early to make any assumptions. Here are the data:

What this means for future interest rates

Clearly, inflation remains too high and is not showing signs of falling. But the Federal Reserve has been signaling it is likely to go ahead with a 25-basis-point decrease in the federal funds rate next week. This report seems unlikely to change that plan.

This morning’s Bloomberg headline is right on target: “US CPI Brings No Surprises, Firming Up Fed Rate-Cut Bets.” From the coverage:

The report suggested that disinflation has essentially stalled in recent months. Headline CPI notched the first back-to-back annual acceleration since March, while core has been stuck at 3.3% — well above a figure consistent with the Fed’s 2% target for a separate price gauge, the PCE – for three months now. …

Shelter costs as usual made up the main portion of the rise in CPI, at almost 40%, although they did slow from the previous month. …

“Especially given the slowing in shelter, this should be very comfortable for the Fed to lower policy rates 25 basis points in December and continue cutting in 2025,” Citigroup Inc. economists Veronica Clark and Andrew Hollenhorst said in a note.

I agree that a 25-basis-point decrease seems likely next week, which would put the federal funds rate in the range of 4.25% to 4.50%, still comfortably higher than the annual U.S. inflation rate of 2.7%.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

What a bonanza they've been! I am fortunate to have had the instinct and the money to have purchased large…