Caution: Consider carefully the long term and high volatility.

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer at auction $9 billion in a new 30-year Treasury Inflation-Protected Security. For an investor who can handle the long term and high volatility of a 30-year TIPS, this auction deserves a careful look.

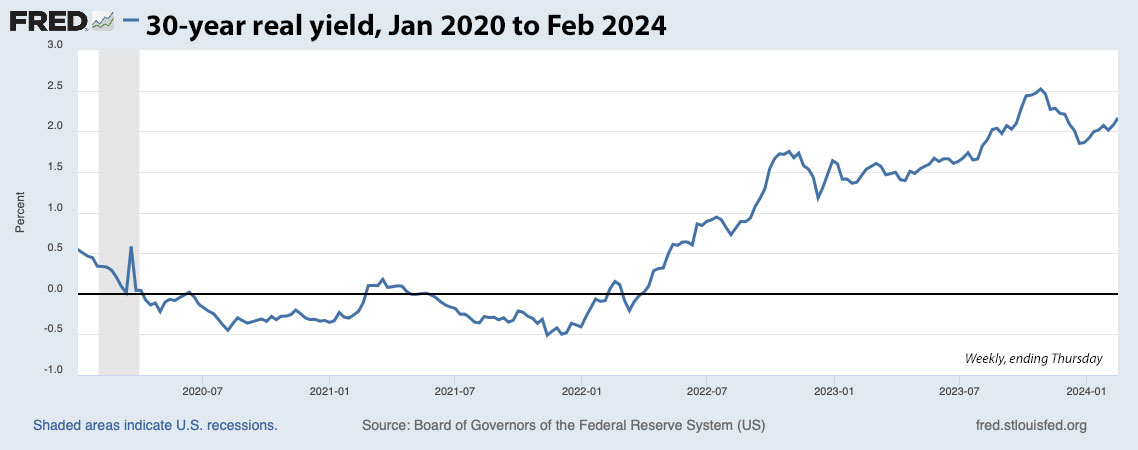

- The Treasury’s real yield estimate for a 30-year TIPS closed Friday at 2.17%, up 26 basis points since February 1. That’s a strong move higher, triggered by elevated inflation fears in the wake of the higher-than-expected January inflation report.

- If the yield holds at 2.17% at Thursday’s auction, it would be the highest auctioned real yield for any 29- to 30-year TIPS since February 2011.

- A yield that high would set its coupon rate at 2.125%, matching the highest coupon rate for any TIPS auction of this term since February 2010.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

So in this case, a real yield to maturity of 2.17% means this TIPS would out-perform U.S. inflation by 2.17% over the next 30 years. That is historically attractive. Getting a coupon rate of over 2.0% is also attractive, in my opinion. It offers a buffer of protection during deflationary periods, plus generates current income that should easily cover the “phantom tax” problem for TIPS in a taxable account.

Here is the trend in the 30-year real yield over the last four years, showing real yields have backed off the highs of late October 2023, but remain historically strong. Obviously, yields could continue rising. Impossible to predict.

There are dangers

There are only two types of investors who should seriously consider buying this TIPS: 1) An investor who is committed to holding to maturity, no matter the ups or downs of market pricing, as part of a structured 30-year plan to set aside inflation-protected cash for the future, and 2) A speculator who believes this TIPS can be sold at a profit in the near- to mid-term future.

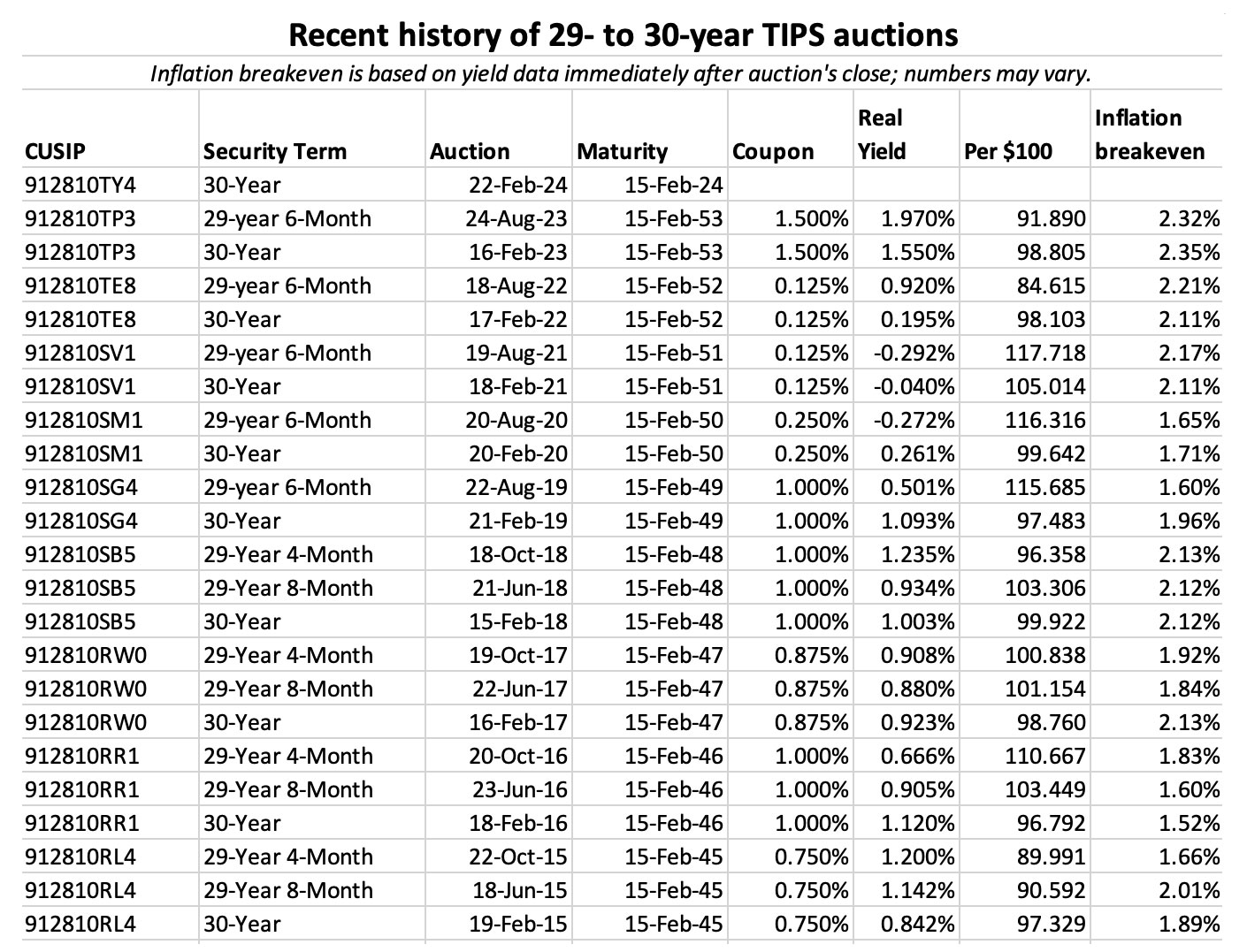

A 30-year TIPS is highly volatile. In 2023, the February 30-year TIPS auction generated a real yield of 1.55%, the highest in 12 years. The coupon rate was set at 1.50%, also a 12-year high. It was an attractive result, at that moment. But … with the 30-year real yield currently at 2.17%, that TIPS (CUSIP 912810TP3) is now trading with a price of 85.96, meaning it has lost about 14% of its value in one year.

The investor in that TIPS who intends to hold to maturity will do fine collecting 1.55% above inflation over 30 years. But an investor who can’t stomach that sort of volatility probably isn’t happy. It takes an iron will to invest in a 30-year TIPS and then hold to maturity.

Pricing

This TIPS will carry an inflation index of 0.99952 on the settlement date of February 29. That means any investment at this auction should result in a cost close to the par value. In other words, an investor placing an order for $10,000 in par value should end up paying slightly less than $10,000. But a small amount of accrued interest will raise the cost slightly.

The par value of a TIPS — $10,000 in the example above — is guaranteed to be returned at maturity if severe deflation sets in. For a 30-year TIPS, this really isn’t an issue. But buying a new TIPS at par value is still “nice,” in my opinion.

Inflation breakeven rate

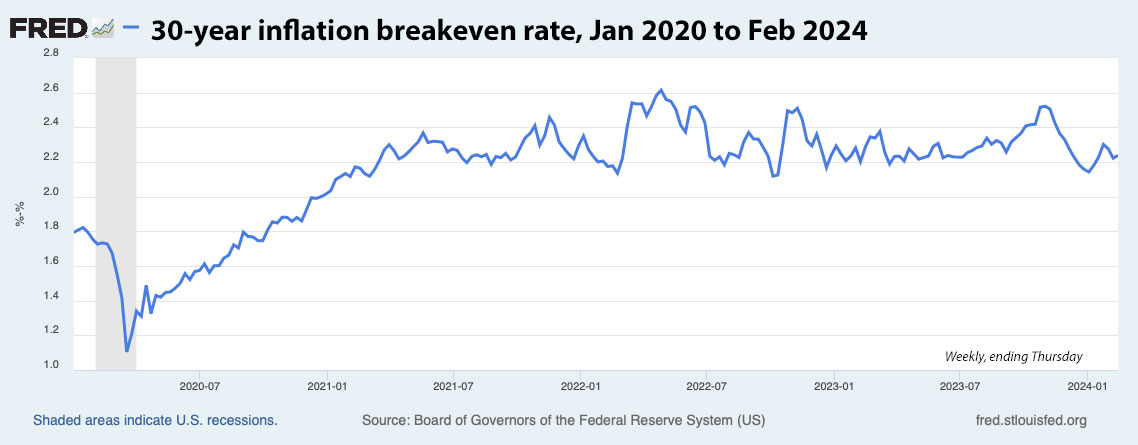

With the nominal 30-year bond closing Friday at 4.45%, this new TIPS currently would get an inflation breakeven rate of about 2.28%, slightly below the rates of the last two auctions of this term. This number seems reasonable. Inflation over the last 30-years, ending in January, has averaged 2.5%.

Here is the trend in the 30-year inflation breakeven rate over the last four years, showing the current rate is close to the typical rate seen since July 2022:

Final thoughts

I won’t be a buyer of this TIPS because its 30-year maturity doesn’t match my probable lifespan for holding to maturity. (My TIPS ladder extends to 2043, when I will be 90. Hope I make it.)

But the auction is intriguing because the real yield is attractive. For an investor who can conceivably hold this TIPS for 30 years, and can tolerate its high volatility, CUSIP 912810TY4 deserves a strong look.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I am writing this from Wellington, New Zealand, where I am 18 hours ahead of Eastern Standard Time. I plan on writing on the auction result after it closes on Thursday, but I can’t say when. The auction closes just at the start of a busy travel day, 7 am on Friday for me. Be patient, but you can check this page for the auction result after 1 p.m EST.

Meanwhile, here are auction results for the 29- to 30-year term over the last eight years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If I had funds at this moment I would buy long dated TIPS instead of iBonds. Those real yields are…