Did it work out well? Yes. But is it worth the risks?

By David Enna, Tipswatch.com

For a few years now, I’ve been getting questions about seemingly lavish high real yields on Treasury Inflation-Protected Securities that are nearing maturity. My usual response is that these real yields — while technically accurate — get exaggerated as maturity nears and only one coupon payment remains.

See this from Sept. 2, 2022: “What’s up with those crazy real yields on ultra-short-term TIPS?“

For example, in late August 2023 readers spotted this TIPS, CUSIP 912828B25, maturing Jan 15 2024, just 4 1/2 months later.

Its quoted real yield was 4.080%, and at the time U.S. inflation was running at 3.7%, so some readers extrapolated a gorgeous return of 7.7% on this TIPS, in just 4 1/2 months. At the time, a 17-week T-bill was yielding about 5.5%.

But that isn’t the way it works. Only 4 1/2 months of inflation accruals remained so the end result for the TIPS was highly likely to be somewhere close to the 17-week T-bill, I figured. Time for an experiment! My thinking: I could get a better understanding of these short-term TIPS by investing in one.

My mind game resulted in this Sept. 3, 2023, article: “Experiment: Let’s try out a very short-term TIPS“.

The investment

To test the theory, on Aug. 30, 2023, I purchased $12,000 par of CUSIP 912828B25 on the secondary market at a real yield of 4.07% and a price of 98.73437. Because this TIPS had a high inflation index of 1.30749, the investment cost me $15,491.30 after the price discount, plus $12.52 in accrued interest.

Because this purchase was starting out with principal of $15,689.88, I was getting an immediate gain of 1.28%, plus I knew I would get 0.3125% interest at final maturity, for a total of 1.59%, which translates to an annual return of about 4.2% before any inflation accruals.

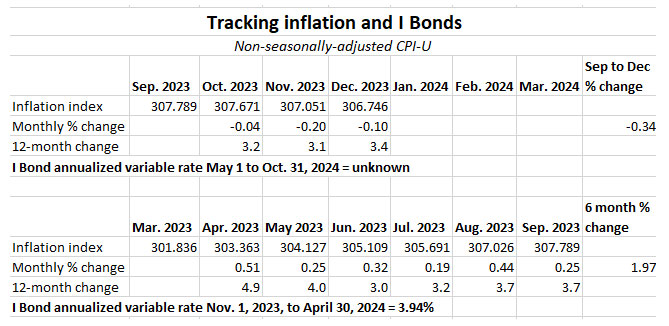

And there was the key to this whole investment: How much non-seasonally adjusted inflation (or very possibly, deflation) would we see before the January 15, 2024, maturity? Inflation accruals for TIPS are set by non-seasonally adjusted inflation two months earlier. So I already knew one month of accruals, for September:

- September: accruals of 0.19%, based on July inflation.

- October: ???, ended up being 0.44% based on August inflation

- November: ???, ended up being 0.25% based on September inflation

- December: ???, ended up being -0.04% based on October deflation

- January: ???, ended up being -0.10% based on half of November deflation

In this case, the first three months added 0.88% to my principal and things were looking good. But the next 1 1/2 months subtracted 0.14% from my principal. I expected this to happen, because non-seasonally adjusted inflation often goes negative in November and December.

Verdict: This time, it worked.

My goal was to use this investment maturing Jan. 15, 2024, to help fund my next TIPS purchase … the new 10-year TIPS that was auctioned last week with a real yield of 1.81%. Would I end up doing better buying this TIPS, or just investing in the 17-week Treasury that would mature on Jan. 2, 2024?

Here is the result:

I adjusted the investment totals to come up with a similar ending number around $15,850. The TIPS ended up being the winner in this contest, with a nominal annualized yield of 6.21% versus 5.52% for the 17-week T-bill. That’s 69-basis-point bonus, but in actual dollars it amounts to about $75, or about one-third the cost of one trip to Costco.

This TIPS had an ending inflation index of 1.31741, 0.759% higher than the starting index of 1.30749. That is annualized inflation of about 2.02%. And remember, I figured with the final coupon payment the annualized nominal yield would be 4.2% before inflation or deflation. The actual return was 6.21%. Do the math: 4.2% + 2.02% = 6.22%, so you can see roughly how the real yield actually topped 4.0%, as advertised.

Final point: Is it worth it?

Any time you buy a TIPS with just a few months to maturity, you will be highly likely to be buying a large amount of additional principal that is not guaranteed to be returned at maturity. In this case, I was buying 30.7% extra principal at a cost of about $3,504. If deflation had struck in August and September, I would have gotten a lousy return versus the 17-week T-bill.

Deflation is more of a risk in the short-term (especially nearing the end the year) than the long term. In the future, I would be a lot more likely to buy the 17-week T-bill, which involves zero risk and a certain return at maturity.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’d wait until October to make a decision. The difference between keeping the cash in a 3% HYSA and buying…