These new funds offer simplicity, but with some drawbacks.

By David Enna, Tipswatch.com

Back in late September, financial adviser/author Allan Roth sent me an email pointing out BlackRock’s new offering of 10 defined-maturity TIPS ETFs. Roth, who has been pushing for more useful TIPS ETFs, called this “a step in the right direction.”

I was traveling in Greece at the time and couldn’t take a careful look. But after a quick glance, I decided that yes, these ETFs looked reasonable both in theory and in cost. The expense ratios are only 0.10%.

But I had questions: Who is the target market for an ETF that will be holding only two to six bonds until maturity? Why not just buy and hold the individual TIPS? Would these ETFs provide tax-reporting benefits in a taxable account? Are these ETFs targeted at customers of assets-under-management financial advisers (which would dramatically increase the cost to investors)?

A few weeks later, Roth wrote an article for ETF.com on the BlackRock offerings, with the subhead: “Here is why I bought all 10 of them.” From the article:

I spoke with Karen Veraa, head of U.S. iShares Fixed Income Strategy at BlackRock, about these new ETFs. She confirmed that the purpose of the new ETFs is for the investor to buy and hold until maturity. She noted that buying the individual TIPS directly can be complex with large bid-ask spreads. She also said the tax reporting is simplified with annual 1099s issued. …

I like these ETFs and asked John Rekenthaler at Morningstar to give me his views. He responded: “I highly approve of these new funds.”

By the way, Allan Roth is not an assets-under-management financial adviser. He charges an hourly fee and would not benefit financially if his clients used these iShares ETFs.

A contrary view was offered by financial author and adviser Dr. William Bernstein on a recent “Bogleheads on Investing” podcast. Host Rick Ferri asked him about the new “bullet” iShares TIPS ETFs, and after praising TIPS as an investment, he said:

The bullet shares, unless I misunderstand them, don’t make a bit of sense to me. … Why would you buy one or two bonds that mature in any given year. … when you can buy the bond yourself for zero expense? That doesn’t make any sense.

Bernstein’s reaction (which I think is sound) set off a debate in the Bogleheads forum, with contributors weighing in on both sides.

Let’s take a look

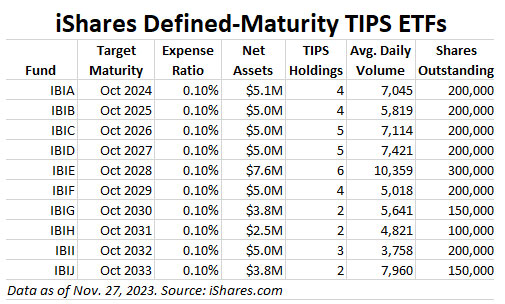

The iShares suite of defined-maturity TIPS funds offers maturities for 2024 to 2033. In other words, you buy the ETF — probably intending to hold to maturity — and then after a defined period, it distributes all proceeds and closes down.

A few things to notice right away: 1) These are extremely small funds with only about $5 million in net assets, versus $19.7 billion for the giant TIP ETF, also from iShares. 2) The number of bonds in each fund is also tiny, ranging from 2 to 6. And 3) The average daily volume is minuscule, which could create bid/ask spread problems. The TIP ETF, by contrast, trades 2.8 million shares a day.

Why do the offerings end in October 2033? Because there are no TIPS maturing from years 2034 to 2039, and then from 2040 to 2053 only a single TIPS per year trades on the secondary market. It’s likely iShares will create a 2034 ETF next year, possibly at first holding only one TIPS (issued in January) and then a second one when a new 10-year TIPS is auctioned in July.

The limited span of maturities means these ETFs aren’t the total solution for building an inflation-protected ladder of investments to cover 20 to 30 years. Roth notes:

Though these new ETFs don’t solve a 30-year safe withdrawal rate, they could be perfect for uses such as bridging the gap while delaying Social Security by building an eight-year ladder at age 62 and waiting to age 70 to begin distributions.

What is the investment objective?

Let’s look at one of these investments, IBIE, which has a target maturity date of Oct. 15, 2028. It holds six TIPS, the most of any of these defined-maturity funds.

This ETF was launched on Sept. 13, 2023, so it has very little performance history. At this point, Morningstar has no performance data on its IBIE page. The ETF launched with a price of $25.22 and now trades at about $25.29.

iShares says the ETF is designed to mature like a bond, trade like a stock. It says: “Combine the defined maturity and regular income distribution characteristics of a bond with the transparency and tradability of a stock.”

As for investment objectives, iShares notes it could be used to achieve multiple objectives. “Use to seek inflation protection with U.S. TIPS, build a bond ladder, and manage interest rate risk.”

Is there a required minimum investment?

No. The minimum investment would be the cost of one share (around $25.29 for IBIE) plus any possible brokerage commission. There are no limits on redemptions. iShares notes there can be a bid/ask spread on purchases and sales. That seems especially likely for an ETF that trades at such a low volume. The iShares prospectus notes:

When the Fund’s size is small, the Fund may experience low trading

volume and wide bid/ask spreads. In addition, the Fund may face the risk of being delisted if the Fund does not meet certain conditions of the listing exchange.

However, even with the small volume for the IBIE ETF, iShares reports that the premium or discount to net asset value has been small, about 6 cents per share. And the median bid/ask spread has been just 0.08%.

Traders in individual TIPS face these same bid-ask issues and at times can have trouble buying or selling TIPS in small numbers. This new ETF resolves the small-lot issue, at least. You can buy as little as one share.

Income and inflation accrual distributions

One of the advantages of owning a TIPS to maturity is that inflation accruals continue to build over time, increasing the amount of principal and also increasing the semi-annual coupon payment as the principal increases. An individual TIPS gets the benefit of compounding, even though the coupon is distributed twice a year.

But one of the disadvantages of a TIPS is that if held in a taxable account, those inflation accruals are subject to “phantom” federal income taxes in the current year, even though they are not paid out. Plus, if your account is at TreasuryDirect, you will face the “dreaded 1099-OID,” the cryptic form reporting your taxable accruals.

In the past, I have written about holding individual TIPS in a taxable account. I am actually OK with that, but after retirement I switched to using a traditional IRA, where money can be raised without tax consequences. See this: “Frightened by a phantom? TIPS are fine in a taxable account, until …“

The ETF plus. These defined-maturity ETFs “fix” the OID issue because inflation accruals will be paid out in the current year, along with the coupon interest. (This is the same way traditional TIPS funds work). That distribution makes these iShares TIPS ETFs more attractive for holding in a taxable account, because it eliminates the phantom income problem.

I assume this also means your broker will provide a single 1099-DIV tax form covering both coupon payments and inflation accruals.

The ETF minus. Distributing the inflation accruals in the current year means that at maturity you will be receiving only the original par value and final coupon payment, since all the inflation accruals would have been distributed.

So to get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs or another similar product.

That could be a problem. I am not confident it would be wise to try to create a reinvestment strategy for ETFs with extremely small average daily volumes. I expect that Vanguard, for one, would refuse to do those reinvestments automatically.

For example, Allan Roth ran into a low-volume problem while building his ladder of these defined maturity ETFs:

I thought it would be a piece of cake to buy these, but I was wrong—at least on two of them. Using the Fidelity retail website, all went through except two. For IBIC and IBIF, I got error notifications that the share quantity I entered was greater than the maximum allowed.

How could buying fewer than 25 shares for about $900 be too high? I followed up with Fidelity and eventually found out I was violating Market Access Rules. Fidelity explained that the quantity I was buying was too high relative to the average volume over the past 90 days. They were eventually able to solve it for me, but I couldn’t buy the exact dollar amount I wanted.

Final thoughts: Simplicity is good

These defined-maturity ETFs look good, maybe not for me, but for other investors looking for a simpler way to invest in TIPS, especially in a taxable account. The iShares pitch is “matures like a bond, trades like a stock” and that is appealing.

In just an hour, an investor could conceivably build a “diversified” exposure to TIPS spanning 10 years, with maturities in each year. This isn’t the solution to building a long-term TIPS ladder to last through retirement, but could be used as a bridge to taking Social Security at age 70 or other specific needs lasting 10 years.

The expense ratio of 0.1% is very good, especially if you can make your trades commission-free. But I do warn against using these ETFs in an assets-under-management account, which could wipe out 1% to 2% of your annual earnings.

One other issue is the fact that these funds don’t offer true inflation protection over the long term, since they pay out the inflation accruals in the current year. That is great for people seeking cash flow. But an investor seeking inflation protection would need to figure out a way to reinvest distributions.

Reinvesting is quite simple for traditional high-volume TIPS funds like TIP, SCHP or VTIP. But the very small volumes of these iShares funds could cause problems. iShares notes: “No dividend reinvestment service is provided by the Trust” and it suggests contacting your broker to see if it can be done on the secondary market.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The wait is over...one of the missing ingredients is the benefit of starting the minimum one year old for maximum…