By David Enna, Tipswatch.com

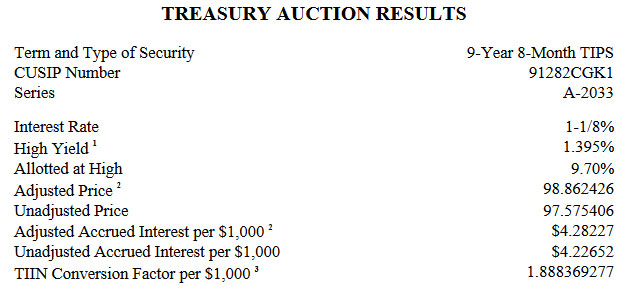

The Treasury’s auction today of CUSIP 91282CGK1 — a 9-year, 8-month Treasury Inflation Protected Security — generated a real yield to maturity of 1.395%, a good result for investors but just slightly below market trends.

Earlier in the day, this TIPS was trading on the secondary market with a real yield to maturity of 1.41%, so the auction result came in slightly lower. Pretty close. The bid-to-cover ratio was a middle-of-the-road 2.31, indicating acceptable but not stellar demand.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

On the positive side, the real yield of 1.395% was the 2nd highest for any TIPS auction of this 9- to 10-year term dating back to a reopening auction in April 2010. The only auction with a higher result came in November 2022 at 1.485%.

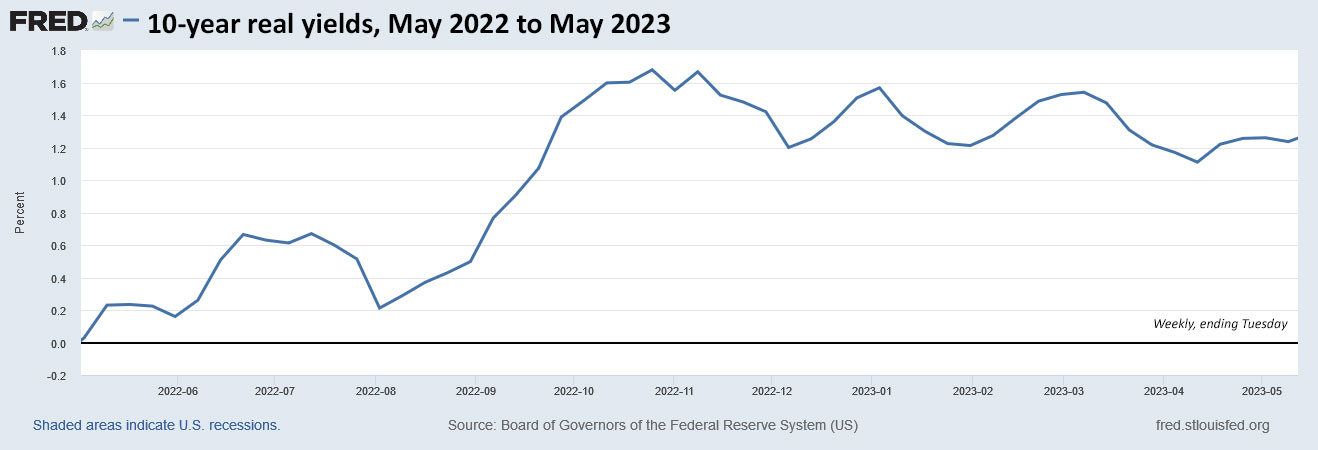

Here is the trend in the 10-year real yield over the last 12 months, a remarkable period when we have seen real yields rise from 0.0% to today’s 1.395%:

Pricing

CUSIP 91282CGK1 has a coupon rate of 1.125%, which was set by the originating auction on January 19. Because the auctioned real yield was higher, this TIPS sold at a discount, with an unadjusted price of 97.575406. It will have an inflation index of 1.01319 on the settlement date of May 31.

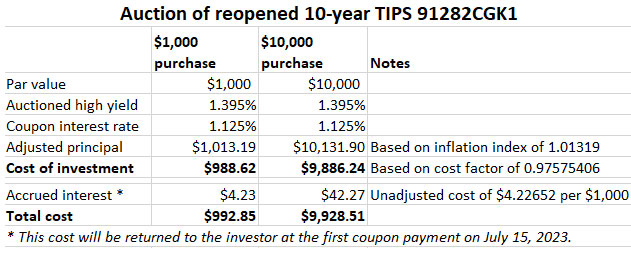

Here is how the pricing works out for today’s investors:

Note that the cost of investment came in lower than the par value, even with the addition of the 1.01319 inflation index. This is because of the 27-basis-point spread between the real yield and coupon rate, which was large enough to cover the inflation accrual. It’s not a big deal, but remember that with any TIPS par value is guaranteed to be returned at maturity, even after a long period of deflation.

Inflation breakeven rate

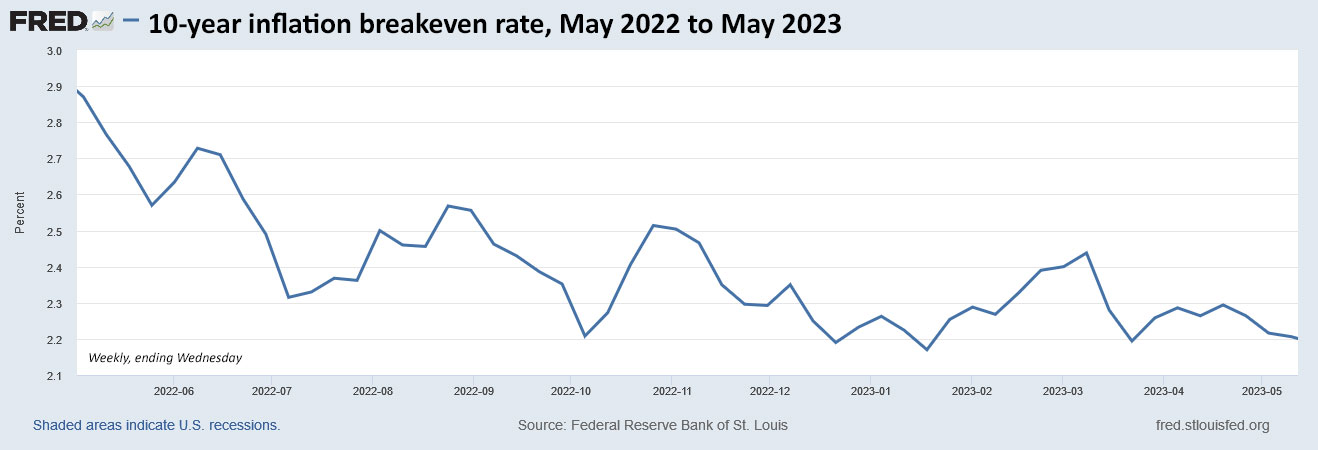

With a 10-year nominal Treasury note trading at 3.64% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.25%, close to recent results for this term. It means that CUSIP 91282CGK1 will outperform a nominal 10-year Treasury if inflation averages more than 2.25% for the next 9 years, 8 months.

Here is the trend in the 10-year inflation breakeven rate over the last year, demonstrating that inflation expectations have been sliding lower as the Fed has raised interest rates and continued quantitative tightening:

Final thoughts

This auction was a good result for investors. Earlier in the morning, it looked like the real yield could end up around 1.41%, but this result was fine — the second highest auctioned real yield in a dozen years. I was a buyer. I’m happy.

It’s impossible to say where real yields will be heading, even in the near-term future. They could certainly go higher, but I think this period of fairly stable high real yields is a good time to continue adding to your hold-to-maturity TIPS investments.

This auction closes the books on CUSIP 91282CGK1. A new 10-year TIPS will be auctioned on July 20 and then reopened in September and November.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I bought this TIPS at the original auction in January through a Fidelity retirement account. Something I’m not getting, and I fear this is a stupid question, as we’ve had inflation – not deflation – since then I would have expected the principal to go up with inflation, but according to Fidelity it has gone down instead, to $96.625 today. The first interest payment isn’t until next month, and it will be interesting to see if it’s based on this reduced principal or not.

Thanks, David

The market value of a TIPS rises and falls as real yields rise and fall. This is how all bonds work — if yields rise, the value of the bond falls. This TIPS had an originating auction on Jan 19 with a real yield to maturity of 1.22%, and it has a coupon rate of 1.125%. When you bought that TIPS at auction, you paid an unadjusted price of about $99.11 for $100 of value. Now the market value — ignoring inflation — has fallen to about $96.25. Why? Because the current real yield is 1.564%, higher than that coupon rate of 1.125%. The inflation accrual — so far since the January origination auction — is about 1.4%.

If you are holding to maturity, you really don’t need to focus on the constantly changing market value.

I want to share an observation that I just made after reading Nick Timiraos of WSJ article posted at 2:24pm today. Interstingly, post panedemic, well debated, neutral rate, and contrary to my thinking, is expected to stay low. This means the Fed will need to keep rates high until inflation comes down from 4.9% to around 2%. Barring unexpected events, which happens more often than we want to believe, so far, the Fed seems to be quite successful in bringing down inflation from 9.1% to 4.9% by raising interest rates by only 5% (it’s all relative, I have 80s in mind). If the trend of inflation going down remains intact or recession happens (though Q2 GDP growth of 2.2% is looking way better than Q1 1.1% growth), we have a limited time (6-9 months) to get a decent income from current rates. The challenge will be on how to manage when the current nominals, in taxable or non-taxable accounts, mature? I buy TIPS only in our non-taxable accounts and keep them to maturity. Any thoughts?

Based on past experience, I have been preaching a sense of urgency in buying inflation-protected and nominal investments while yields are attractive. I have been buying nearly every 5- and 10-year TIPS auction, while also adding attractive nominal CDs when I see them. I am trying to stretch out maturities to 10 years plus (not realistic for CDs). Longer-maturity TIPS often have huge inflation accruals and that makes them less attractive. So the 10 year is a good middle ground, since we can now buy new and reopening issues that mature in 2033. The 5-year is also attractive. I’m also exclusively buying TIPS in a non-taxable brokerage account and planning to hold to maturity.

The one nagging issue is: What if something fundamental has changed and real and nominal interest rates will continue rising into the future? I could deal with that because I still have room to purchase more.

I too feel a sense of urgency though, as you point out, one never knows. Unfortunately or fortunately (sorry for coping this recently used term in a townhall – you were most likely snorkling and joyfully missed it :)), on the nominal side, most of my buying has been in my taxable accounts and I have been either greedy or fearful of going beyond 3 years maturity. The spread (with the yield curve inverted) makes it hard to go longer. TIPS, in a non-taxable accouns, do provide comfort with the fact that at least the inflation problem is addressed. I have this wishful thinking that with inflation coming in control, Fed pausing followed by cutting, the economy, with infrastructure bill spend, penup demand, etc., will grow fast and longer dated nominals will then provide a better opportunity. In the meantime, the goal is to maximize returns by daily monitoring of nominal and real yields and building a short-term ladder, in other words, I am trying to be a unqualified Money Market manager with zero expense ratio (not counting the bid ask spread :)) There is quite a bit of comfort that we are dealing with, supposedly, zero principal risk asset – notwithstanding unnecessary debt ceiling noise.

Zero risk to principal asset NOT zero principal…

Yep. Zero risk to principal asset but only if you buy it t auction. In the secondary market there can be a loss of principal (moderate loss)

Indeed!!…good point.

I’m a little confused…would it have been better to buy on secondary market since that yield was higher? Sorry, new to this…

There are advantages to buying at auction: You always get the high yield no matter the size of your investment, even a $1,000 investment gets the same yield as someone buying $10 million. That isn’t true on the secondary market. Smaller purchases get a lower yield, and you won’t know how low until you start your order. I doubt an $10,000 investment could have gotten the 1.41% real yield this morning before the auction. The advantage of buying on the secondary market is that the brokerage will show you the yield you are getting, so you know your exact investment. At auction, the yield won’t be determined until the auction closes. The yield could be lower, or it could be higher, than you expect. It works both ways, and more or less balances out.

Thanks…makes sense (cents?)

FYI, the auction results PDF says the accrued interest is $4.226 unadjusted / $4.282 adjusted per THOUSAND, not per ten thousand.

So if I’m doing the math correct, a $1000 par purchase will cost $992.90.

Thanks for catching that. Dumb error (I was rushing to get to a pickleball match). This is now fixed.

Excellent analysis. I thank you for your posts.

I am looking forward to the June 22 4 year 10 month reissue of the 5 year TIPS 91282CGW5 as I already bought some of this same CUSIP last April. I will, of course keep, close tabs with your postings when the time comes

Congrats! Sounds like a good deal to me. I purchased this same CUISP 3 times earlier this year, at a real yield of 1.2%. Each time the yield was near the low point for the year.