By David Enna, Tipswatch.com

After a week of declining yields in the Treasury market, a new 10-year TIPS auctioned Thursday with a real yield to maturity of 1.22%, a bit lower than looked likely just before the auction’s close.

This is CUSIP 91282CGK1, and its coupon rate was set at 1.125%, the highest coupon rate for any new 10-year TIPS since an auction in January 2011, which had a surprisingly similar result: real yield of 1.17% and coupon rate of 1.125%. A few months after that 2011 auction, 10-year real yields fell sharply, hitting -0.13% by August 10.

All morning, CUSIP 91282CGK1 looked likely to get a real yield of about 1.24%, and the “when issued” premarket was set at 1.26%. So the result of 1.22% appears to have been caused by high investor demand. The bid-to-cover ratio was set at 2.79, well above any recent auction of this term.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.22% means an investment in this TIPS will exceed U.S. inflation by 1.22% for 10 years. If inflation averages 2.2%, you’d get a nominal return of 3.42%, on par with a nominal 10-year U.S. Treasury, currently 3.42%. But if inflation averages 4.5%, you’d get a nominal return of 5.72%.

Pricing

This new 10-year TIPS is a bit unique because it auctioned with an adjusted price below par value, which is fairly rare for a new offering. The details:

The key factors here are that the unadjusted price was $99.11 for $100 of value and the inflation index on the settlement date of Jan. 31 will be 0.99948. Accrued interest will be about 49.6 cents per $1,000 investment. Here is how the pricing works out:

Inflation breakeven rate

With a 10-year nominal Treasury note trading with a yield of 3.42% at the auction’s 1 p.m. close, this TIPS gets an inflation breakeven rate of 2.20%, just slightly higher than the market rate earlier in the day. This is the lowest auctioned breakeven rate for this term since January 2021. I’d say this is an attractive rate, making this TIPS appealing versus a nominal Treasury.

Reaction to the auction

This one was a bit ill-fated, with a slew of economic reports arriving this week pointing to a downturn in the economy. That is putting more pressure on the Federal Reserve to call a halt to its current hawkish interest rate increases. But a lot of this sentiment is cyclical. We could see rates rising next week. Or maybe falling.

As I have noted before, this is only the fifth TIPS auction of this term since January 2011 to get a real yield to maturity higher than 1%. There have been 72 auctions of this term over that time span, so today’s result is welcome, even if real yields dipped a bit in the closing hours.

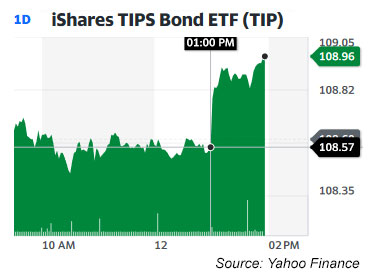

This chart shows the market’s quick reaction to the auction’s close at 1 p.m. ET, with the broad-based TIP ETF surging higher in reaction to the apparently strong demand.

I know a lot of new TIPS investors jumped aboard this auction, and I want to reinforce my view that the result was positive for investors: A rare real return on your money surpassing 1.2%, over 10 years, while also priced slightly below par value. Of course, there will be two more reopening auctions of this issue — in March and May — and then a new 10-year TIPS will be auctioned in July. So more opportunities to come.

Here are auction results for this term over the last five years:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi Dave, Thanks for the great Blog. You are a gifted writer and excellent financial quantifier. Follows is a link to a financial blog that posted an article on TIPS vs Gold you will find interesting:

https://scottgrannis.blogspot.com/2023/08/tips-vs-gold-which-is-better-inflation.html

Best Regards, BoomRBust29 – protect my email address for privacy

Pingback: 10-year TIPS reopening auction gets a real yield of 1.395%, 2nd highest in 12 years | Treasury Inflation-Protected Securities

Pingback: Thursday’s 10-year TIPS reopening auction looks attractive; ignore the Treasury turmoil | Treasury Inflation-Protected Securities

Pingback: 10-year TIPS reopening auction gets real yield of 1.182% | Treasury Inflation-Protected Securities

Pingback: This week’s 10-year TIPS reopening auction still looks attractive | Treasury Inflation-Protected Securities

Pingback: Bond market shakeup: Where we stand today | Treasury Inflation-Protected Securities

I have been buying TIPS on the secondary market at my E-trade brokerage account for years. Over the last few days, when I try to put in an order for the Jan 15 2033 TIP I am informed that the minimum size is 100 (Roughly $100,000). In the past, I have purchased as few as 5 at a time with no problem. The E-trade bond desk just tells me that they don’t set the market so nothing they can do. I’m wondering what has changed?

That new TIPS had a settlement date of Jan 31, so its possible it wasn’t available for purchase until Feb 1. Since it is so new, possibly there are limited sellers? You might want to just keep checking.

This TIP CUSIP 91282CGK1 has been available at Schwab’s website since the settlement date (Jan 31). The Schwab website clearly lists the “Min” (i.e., minimum) purchase amount for each seller. Most of the listed sellers have a high minimum purchase amount (such as 100 to 150 x $1,000), but often one or two sellers show up with “Min” of 1 x $1,000 par value. So i think David is correct: You need to keep checking back for a seller(s) on your platform with smaller minimum purchase amounts. I’ve been watching this CUSIP also, and unfortunately (for me) it was selling at YTM 1.255% (min purchase $1,000) up until the FOMC announcement, and then tumbled after the announcement to 1.15 YTM. I guessed wrong on that move, and i’m going to keep checking back in the days/weeks to come for a higher YTM (lower price).

Hey DT, if you’re watching, today is a good day to snatch CUSIP 91282CGK1 on the secondary market. I just bought on Schwab website at YTM 1.276%, price 98.591 (minimum $1,000 par)

Thanks toms — I check several times a day at E-trade, and the Jan 15 2033 TIPs depth of market always has a minimum purchase of 100 $1,000 face value bonds or more so far. All the other bonds are available with as few as 1 bond. Don’t know enough about the bond market to know why Schwab would be different than E-trade. It may be a blessing in disguise, though. I notice that the ask price is down to $97.53 today.

Fidelity has min purchase of 1 but the price is higher. For min 1 qty the current ask price is 97.834 (1.359ytm) vs 97.791 for 150 qty (1.363ytm)

Depth of market finally eased and I was able to purchase my shares at E-trade today at a price of $97.28 with YTM of 1.42%. Not bad. That fills in the rung on my ladder. Just required some patience…..

Good job of being vigilant!

I usually buy at auction, but as mentioned by some others above, I refrained from buying this 10-year at auction because yields had fallen and were fluctuating rather wildly pre-auction and it seemed (to me) at the time that real yield would bounce back up (at least temporarily) and i could buy later on the secondary market at better real yield. This CUSIP 91282CGK1 settled today (1/31) and it is now on the secondary market (at Schwab) at YTM 1.255, price 98.78947. Isn’t that already better than the auction price?

I plan to wait another day or two, anticipating real yield may rise further after FOMC (tomorrow) tamps down expectations for rate cuts in the foreseeable future. Yes, it’s a guess, but it’s an educated guess.

Have you ever done an article specifically about what to look for when purchasing TIPS on the secondary market? (I’m doing this all within IRA accounts at Schwab (no fees for online purchase), so i’m not concerned about fees or tax issues, just optimizing price of “wealth preservation” as portion of fixed-income allocation in our IRAs.)

I have dealt with this secondary-market issue in several articles, but have an idea I am working on for a future article, looking at the key factors to consider. We’ll see if I succeed.

Your posts are much appreciated. Question (or maybe request for a post topic): could you discuss how to compare TIPS on secondary market related to different inflation factor amounts and if there is any advantage or disadvantage to purchasing an individual TIP with significantly higher or lower inflation factor, beyond higher initial cash outlay for the TIP with high inflation factor. Does the real yield quote even out the inflation factor and keep the comparison with widely divergent inflation factors still an “apples to apples” comparison? Thanks much in advance.

IRA RMDs are calculated based on the IRA balance at the end of the previous year. How will the value of the TIPS held in the IRA account be calculated? Based on the market value of the TIPS at the end of the year or the index ratio?

Market value.

That’s okay with me but it’s not what I expected.

If the TIPS were held in a taxable account, then I would expect the IRS to use the inflation-index ratio to calculate the taxes due on the “phantom” income. What am I missing here?

The Lord, and the IRS, move in mysterious ways.

Correct in a taxable account you pay taxes on the accruals every year. But in a traditional IRA, the only factor that matters for RMDs on Dec 31 is market value of the entire account.

David,

Thanks so much for your work on this website!

I am building a TIPS ladder starting in 2032 when I will be 71. I have already purchased TIPS maturing in each of years 2032, 2033, 2040-2049. Like other TIPS ladder investors, I need to figure out how to fill those years 2034-2039. I had been planning to just buy one 10 year TIPS every year from 2024-2029, but with TIPS yields so high now, would you recommend people consider buying all of those years’ TIPS in March 2023, if the yield remains high?

Thanks,

Steve

This seems to make sense, if you will want access to the money in those years 2033 to 2040. After 2033 you could shift to shorter-term nominals to cover those years, or even I Bonds. Real yields could continue to climb in the short term, but now is an attractive time for ladder-building. Take a look at Allan Roth’s widely discussed article: https://www.advisorperspectives.com/articles/2022/10/24/the-4-rule-just-became-a-whole-lot-easier … And then the Bogleheads discussion: https://www.bogleheads.org/forum/viewtopic.php?t=388845

Thanks, it was actually this article and the Boglehead discussion that led me to build my TIPS ladder and then discover your very helpful website.

Warmly,

Steve

Hi David, Still trying to get my head around the TIPS specially in the secondary market. I have many dumb questions. Hope you and the community can help in answering these questions.

Trying to understand these two tips:

TIPS#1: 912810PS1

Maturity: 01/15/2027

Coupon: 2.375

Inflation Factor: 1.47651

Ask Price: 103.617

Ask Yield: 1.434

TIPS#2: 91282CFR7

Maturity: 10/15/2027

Coupon: 1.625

Inflation Factor: 1.00517

Ask Price: 101.865

Ask Yield: 1.217

If I buy these from secondary market for $10,000 PAR, I have to pay $15,299 for the first one and $10,239 for the second.

1. As I understand, the PAR value is the only guaranteed amount at maturity, so at least theoretically the first one riskier than the second one, right?

2. How the inflation factor is calculated and why they differ so much between these two TIPS although both of them are maturing in 2027? Are they going to be the similar values at maturity?

3. What does the Ask Yield mean? Do I have to consider this number in buying tips from secondary market? Does higher ask yield mean overall better return by maturity as the first one in this example?

Thanks,

Anurav

Question 1: Yes only par value is guaranteed to be returned at maturity. Another factor with these two TIPS is the widely different coupon rate, which means you are paying a higher premium price for that extra principal.

Question 2: The inflation factor begins at 1.0 on the date of issue. For TIPS 1 the date of issue was Jan. 15, 2007. For TIPS 2 that was October 15, 2022. TIPS 1 has had 15 more years to build up its inflation factor.

Question 3: The ask yield is just the real yield to maturity based on the ask price. It may not be the yield you actually get at the purchase, but it should be close. A higher real yield is attractive, but many investors would prefer TIPS 2 just because its current inflation accrual is small and its ask price is close to par. TIPS selling close to par value will tend to have lower real yields, but may be more attractive to some investors.

Thank you for your quick response. One follow up on question #2. Will the Inflation Factor keep increasing till maturity or it depends on the current inflation/deflation?

It depends on current inflation/deflation. To be accurate, inflation adjustment lags 2 months. So December inflation/deflation takes effect in February.

Thank you.

Hi David: I have been following your very informative posts for some time and I do appreciate the time and effort you put into providing this information. I too own 91282CEJ6 [10,000], maturing on April 15, 2027.

I know that you have never sold a TIPS prior to maturity and recommend against it. But for reasons unique to me, I have been thinking about selling it, even though I know there would be a loss. I just can’t figure out exactly what that might be, given what I paid for it and what it might sell for.

If possible, I would truly appreciate it if, for example, you could calculate what that figure would be if I were to sell it at the price of $94.586, so that I can make an informed decision. Thank you for your consideration.

If you bought $10,000 par …. This TIPS will have an inflation index of 1.05473 as of Monday, so you have $10,547 of accrued principal. It looks like it is now priced at about $94.50, so that means 10,547 x 0.945 = $9,967 market value, plus a very small amount of accrued interest.

Basic question, just trying to understand.

When you buy on the secondary market, what price do you get on when you redeem on maturity?

Let’s say par is 100 and you buy for 95.

Do you get: (IR=index ratio)

100*IR

or

95*IR

At maturity you get par (100) x inflation index. If that calculation is less than par (not likely) you get par.

Thanks.

If a TIPS is auctioned for less than $100 per $100, say $95 for illustration, and we then go through a deflationary period such that the adjusted price is $90 does the investor receive $100 at maturity or just $95? Similary if the auction goes off at $95 and at maturity the adjusted price is $99 does the investor get $99 or $100?

Thanks

The investor is guaranteed to receive the original par value at maturity. So, not matter what you paid, you’d get the par value of $100 at maturity. In the case of this auction, investors paid $99.06 for about $99.85 of principal. But the par value remains $100, and that is guaranteed to be returned at maturity. At an opening auction like this one, that guarantee is practically meaningless because inflation certainly will be enough to push principal over $100 in 10 years.

Thanks. That’s very helpful. In staring at some issuances in the secondary market it seems to me that all else equal it’s lower risk to buy a tips that has an adjusted price below $100 if possible. Eliminates the risk of losing principal from deflation or disinflation.

David, it depends on the TIPS you are looking at, but generally a TIPS with a higher inflation accrual will end up having a slightly higher real yield to maturity. Another factor is the coupon rate. If it is higher than the current market real yield, then the investor is buying additional principal at a premium price. Again, that TIPS would tend to have a higher real yield to maturity.

91282CEJ6 is interesting to me. It matures in 5 years (4/15/27) price $94.586, adj price $99.77215, .125% coupon, with a ytm of 1.404%. That ytm is about 14bps better than the 5 yr tips real yeild listed on bloomberg. And of the 5 tips maturities in 2027 it’s the only one with an adjusted price below $100 so there’s no capital loss risk. Am I off in my thinking?

I’d agree that as of today’s close, it looks good. I actually own that TIPS, and it is looking better now than when I bought it.

Appreciate the thoughts. It’s funny, I’m an investment professional and generally understood the key concepts around how TIPS work, but didn’t realize just how complex they were until going down the rabbit hole a bit.

TIPS newbie here. The current price of 91282CEJ6 being $94.586 means for $10,000 Par I am paying $9,458.60.. At maturity I am guaranteed $10,000. right?

Assuming inflation averages 2.2% and the coupon rate being 0.125%, nominal return will be 2.325% till maturity.. Am I interpreting it right? Thanks

Anurav, your analysis looks right. That TIPS has an inflation index of about 1.054, so if you buy $10,000 par you will actually be receiving $10,504 of principal. If the price is 94.586, then you will be paying about $9,935 for $10,504 of principal, plus a very small amount for accrued interest. From that point on, you will be earning 0.125% on $10,504, and the coupon payment will grow with inflation, as long as there is inflation.

Thank you David. I got my first TIPS (91282CEJ6) in the secondary market today. Your posts are a huge.

I’m one of the newbies buying TIPS at today’s auction. Thanks for your great explanation giving me the confidence to jump in and get my feet wet. I’m feeling pretty confident we won’t see inflation below 2.2% again anytime soon.

Same for me, Cynthia, and from the sounds of it here, I’m wishing I would have purchased more. Big thanks to Mr. Enna and his wonderful website that thoroughly explains the often nebulous world of Treasurys. I recently watched some videos on YouTube from Diamond NestEgg who gives a shout out to David Enna also. I look forward to reading more of David’s articles on TIPS & I-Bonds.

Thank you so much for all of your information! I have wanted to get buy some TIPs at auction & finally took the plunge with December 5-year 91282CRF7 with an inflation breakeven point of 2.26% and this week’s 10-year 91282CGK1 with a breakeven point of 2.2%

I am still having some difficulties understanding how the inflation factor works.

91282CRF7 Index ratio as of 12/30/22 of 1.00576

91282CGK1 Index ratio as of 1/31/23 of 0.99948

Any help explaining this would be greatly appreciated! Thank you!

The inflation index each month is based on non-seasonally adjusted inflation two months earlier. But the December issue was a reopening and carried inflation since it was originated in October. The January issue was a new TIPS and so it got an index based on a half a month of November’s -0.1%.

I chickened out on this auction today as yields continued to fall

. I’m curious to know when this offering be available on the secondary market. Any idea on this David?

I am assuming (but not sure) that the auction transactions have to settle first, and that happens on Jan. 31.

What is bid-to-cover ratio and what is its significance when purchasing TIPS at an auction?

It is basically the amount of bids received by the Treasury versus the amount sold. For TIPS auctions, the typical bid to cover ratio is about 2.5.

I hear rumors that this will be the last Treasury auction of any kind this year until the Debt Ceiling has been raised. Is that true?

I can’t find any evidence to support this (right now), but at times in the past some Treasury auctions were canceled over this issue. The Treasury is still showing auctions on its schedule and has no alert on either the Treasury site or TreasuryDirect.

Slightly off topic but I recently had a terrible experience with Treasury Direct.

I tried adding a bank account, verified all the information was correct, and it said it could not verify the account. I clicked a few times and then it placed a hold on that account! Then I tried using the contact form and it logged me out before I could send it! So now I have to call them and wait just to sort out this mess. Who knows how many hours that will take.

It remains, to this day, a nightmare website. It only works if you never have to change anything again, if everything is perfect. The moment you actually try to change something or get support, it collapses into one of the worst places to deal with. And you can’t click back on your browser, you have to use their buttons. And therefore it doesn’t really fit in to how most of us live our life or use the internet.

What’s my point? My point guys is that you yourself have to decide if dealing with them is worth the I bonds. All of you will proclaim the wonderfulness of I bonds until you actually have problems with the site, and then you will understand everything I have written.

This is a major negative against I bonds. It’s not minor. It’s major, like, be aware of this before getting yourself into this mess, be prepared for headache after headache just to get that precious interest rate.

May just go with tips or tips etf from broker from now on. I will allow myself time to recover and possible liquidate my I bonds, we’ll see.

Sorry to hear that- adding a bank account to my I bond account was easy peasy.

I also recently added a bank to my T-Direct account without any problem.

Treasury Direct does eventually answer the phone… their folks we’ve spoken to are polite, knowledgeable, helpful.