By David Enna, Tipswatch.com

One of the year’s most interesting TIPS auctions is coming Thursday, the reopening of CUSIP 912810TP3, creating a 29-year, 6-month Treasury Inflation-Protected Security. Like many of you, I won’t be a buyer at this $8 billion offering. But for some, this TIPS offers a unique investment opportunity.

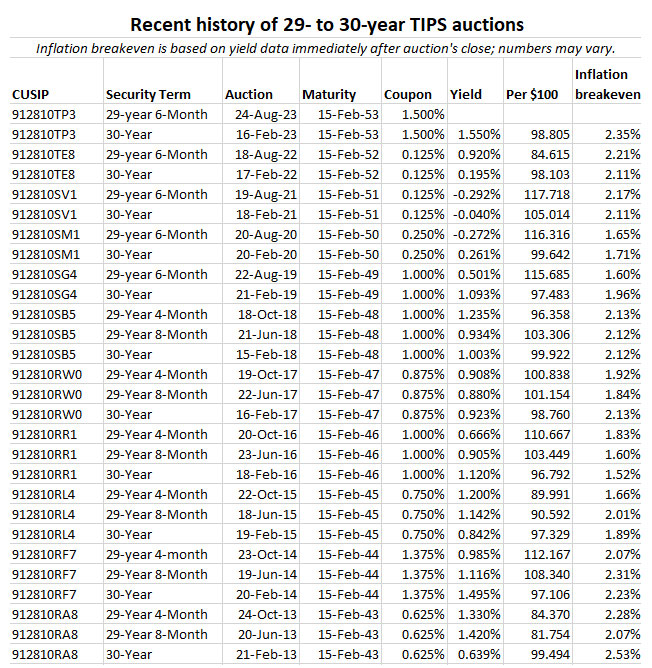

I say unique, but that could mean uniquely positive (a good possibility) or uniquely awful (there’s always that chance). But either way, this auction will be unique because it is likely to generate a real yield to maturity of close to 2.0%, or higher. No TIPS auction of the 29- to 30-year term has nabbed a real yield that high since February 2011, when a new issue got a real yield of 2.190%. Just two years ago, a similar August auction got a real yield of -0.292%.

CUSIP 912810TP3 trades on the secondary market, and Bloomberg’s U.S. Yields page shows it closed Friday with a real yield of 2.08%. If that holds on Monday, an investor could bypass Thursday’s auction and lock in a 2% yield over inflation. Or … just wait for the auction and get its result.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

Here is the trend in the 30-year real yield going all the way back to February 2010, when the Treasury restarted the 30-year maturity after an 8 1/2-year pause:

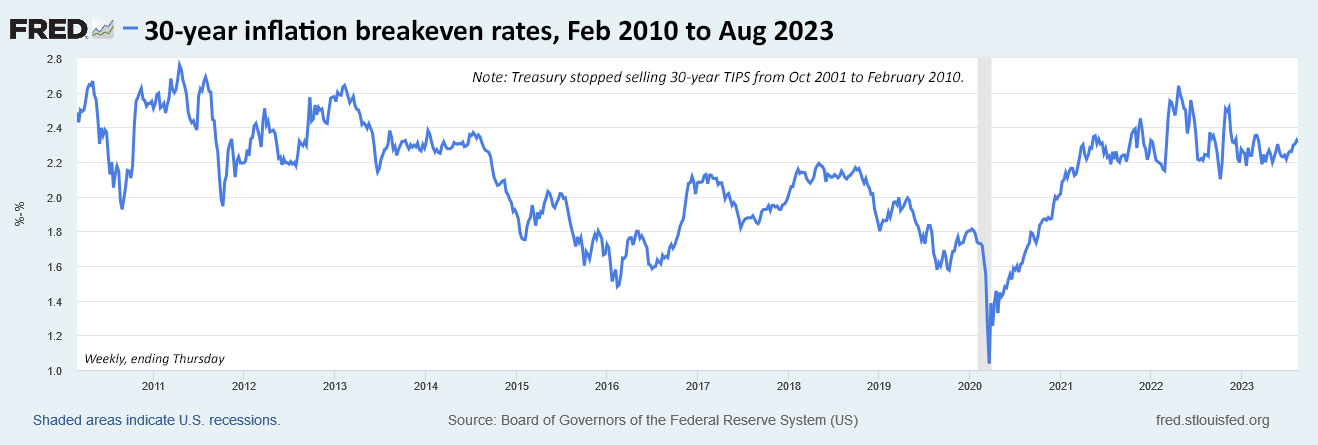

The chart show the 30-year real yield only briefly topped 2% during this entire period, in 2010 and early 2011, and again in August 2023.

Some cautions

As I noted, I won’t be a buyer of this TIPS because it will mature when I am 99 1/2 years old. It doesn’t fit into my hold-to-maturity strategy. For others — age 60 or younger — it could fit as the top piece of a multi-year TIPS ladder.

It’s important to recognize the volatility of any 30-year Treasury investment. Even small swings in market real yields can cause substantial changes in the market value of a TIPS. For example, CUSIP 912810TP3 originally auctioned on Feb. 16, 2023, with a real yield of 1.55%, which at the time was the highest auction result in nearly 12 years. That set the coupon rate at 1.5% and the adjusted price was about 98.66 for $100 of value.

Fast forward six months and today that same TIPS has a real yield of 2.08% on the secondary market and its market price has dropped to about 87.34. So this TIPS has lost about 11.5% of its value in only six months. The lesson here is that long-maturity Treasurys are highly volatile; an investor has to recognize that going in. However, if the plan is to hold to maturity and collect 2.0% above inflation, market values aren’t much of a concern. Focus on the plan.

Also, I highly recommend purchasing any long-term TIPS in a tax-deferred account. In a taxable account, yearly inflation accruals of a TIPS (which are added to the principal balance) will be taxed each year as interest income. You won’t recoup that money until the TIPS is sold or matures after 29 1/2 years.

Pricing

On the auction’s settlement date of Aug. 31, CUSIP 912810TP3 will have an inflation index of 1.02632, which means auction investors will be buying about 2.6% additional principal. So an investor purchasing $10,000 par of this TIPS would actually be purchasing $10,263.20 of principal. At Friday’s closing price of 87.34, that principal would cost $8,963.88. Add in about $6.66 of accrued interest and you get to $8,970.54 total cost.

In essence, the investor is paying about $8,964 for $10,263 in principal, plus getting accruals to principal matching inflation for 29 1/2 years, plus collecting a 1.5% coupon along the way. This is a rough estimate based on Friday’s closing market value.

An inflation index of only 1.026 is another reason this long-term TIPS is unique. Because of very high recent inflation, the TIPS maturing in Feb 2052 has an inflation index of 1.094 (9.4% above par) and the one in Feb 2051 is at 1.170 (17% above par). Both of those TIPS also have coupon rates of just 0.125%, the lowest the Treasury will go, compared to 1.5% for CUSIP 912810TP3.

Inflation breakeven rate

With the nominal 30-year bond closing Friday at 4.38%, a 30-year TIPS yielding 2.08% would get an inflation breakeven rate of 2.3%, which is historically high but in line with February’s originating auction. Would I rather invest in a 30-year nominal paying 4.38%? Probably not, but for some this could be a toss up.

Here’s the trend in the 30-year inflation breakeven rate over the last 13 years, showing the range-bound pattern over recent months:

Final thoughts

I found an interesting article this week posted by Bloomberg on Yahoo Finance. The headline was: “Inflation-Protected Bond Bulls’ Pain Thresholds Get Tested.” It told how market strategists from TD Securities made a bet on 5-year real yields declining in the near future, hoping for a quick capital gain.

They targeted an improvement to 1.25%, expecting no further Federal Reserve interest-rate hikes and deceleration in US growth and inflation. Three weeks later, the stop-loss threshold of 2.20% was reached as those assumptions came under assault. …

Still, there’s scope for losses to deepen before support emerges, Dominic Konstam, head of macro strategy at Mizuho Securities, said in a Thursday interview on Bloomberg Television.

“There’s a limit to how far you can sell off,” he said. “Five-year real rates are pretty chunky at the moment, and if they go up another 20, 30 basis points that’s going to be quite attractive I imagine for a lot of investors.”

Why is that interesting? Because savvy market strategists got burned by betting on 5-year TIPS, the least volatile of the TIPS issues. Any bet on 30-year TIPS would have been hugely magnified, and hugely unwise.

I am not a TIPS trader and I don’t theorize on TIPS trades. It is possible that CUSIP 912810TP3 could end up being a big winner for traders, or a big loser. The only way I advise investing in CUSIP 912810TP3 is in a hold-to-maturity strategy, with full awareness of the potential losses (or possible gains) if you need to exit early.

An investor in CUSIP 912810TP3 this week can very likely lock in a 2.0% yield above official U.S. inflation for the next 29 1/2 years. And that is unique.

If you are pondering an investment at Thursday’s auction, keep an eye on Bloomberg’s U.S. Yields page, which updates in real time. It is accurate, but any auction result can bring surprises.

Thursday’s auction will close at 1 pm ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

Here is a history of recent TIPS auctions of the 29- to 30-year term:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…