The U.S. Treasury on Thursday will auction $15 billion in a reopening of CUSIP 91282CGK1, creating a 9-year, 8-month Treasury Inflation-Protected Security.

Although the Treasury market is filled with uncertainty this month as a debt-limit disaster looms ahead, this TIPS remains an attractive investment. It carries a coupon rate of 1.125%, which was set by the originating auction on Jan. 19, when investors got a real yield to maturity of 1.22%. In its first reopening auction, on March 23, investors got a real yield of 1.182%.

This week’s auction looks likely to get a better result. CUSIP 91282CGK1 trades on the secondary market, and according to Bloomberg’s Treasury Yields listing, it closed Tuesday with a real yield of 1.33% and a price of 99.30 for $100 of value.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

CUSIP 91282CGK1 will have an inflation index of 1.01319 on the settlement date of May 31, so investors at this point would be paying about $100.61 for $101.32 of principal. That’s a rough estimate. The actual yield and cost will be determined by Thursday’s auction.

I was a buyer of this TIPS at the originating auction and I will likely to add to the holding at Thursday’s auction. A real yield around 1.33% — if it holds — will be a decent result. (I won’t make a purchase order until later Wednesday.)

Here’s a chart of the 10-year real yield trend over the last 13 years, showing how aggressive bond-buying by the Federal Reserve suppressed real yields through much of that time:

Click on image for a larger version.

At this point, even though yields are down from their late 2022 highs, 10-year real yields remain near their highest levels in a decade. This looks like a sensible investment.

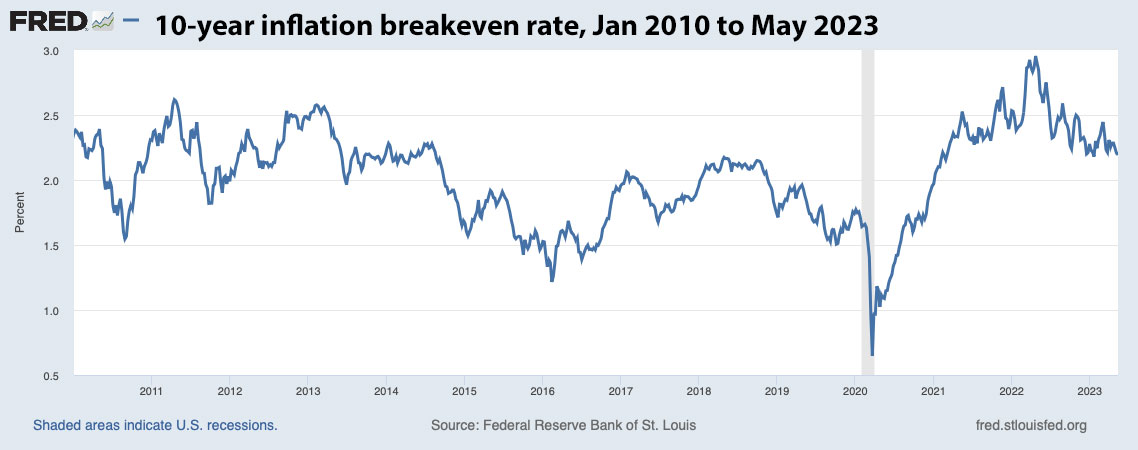

Inflation breakeven rate

With a nominal 10-year Treasury note currently trading at 3.53%, CUSIP 91282CGK1 is trading today with an inflation breakeven rate of 2.20%, which seems reasonable. That means investors are pricing in inflation of 2.2% over the next 9 years, 8 months. If you think inflation will be higher, buy the TIPS. If you think it will be lower, buy the nominal Treasury.

Here is the trend in the 10-year inflation breakeven rate over the last 13 years:

Click on image for a larger version

Inflation expectations have been sliding lower in recent months, making TIPS a more attractive investment versus the nominal Treasury, in my opinion.

Final thoughts

I am writing this Tuesday afternoon from an airport hotel in Quito, Ecuador. In a few hours I will be boarding a redeye flight back to the United States. We’ve been boating, hiking and snorkeling around the Galápagos Islands for the last 8 days. After the first night we had zero internet. Nothing. So I’ll admit I have no idea what is going on in the financial markets.

But it was a relief to see that the TIPS market didn’t go sour in the last week. I am looking forward to Thursday’s auction, which will close at 1 p.m. EDT. If you have updates or opinions on the current financial chaos, post them in the comments section below.

If you are considering bidding at Thursday’s auction, I suggest you keep an eye on Bloomberg’s Current Yields to track the yield trend. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

Here’s a history of 9- to 10-year TIPS auctions back to 2019:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

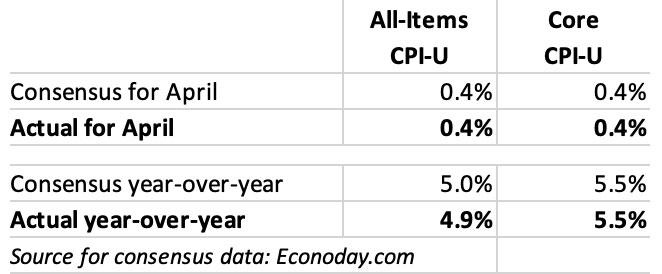

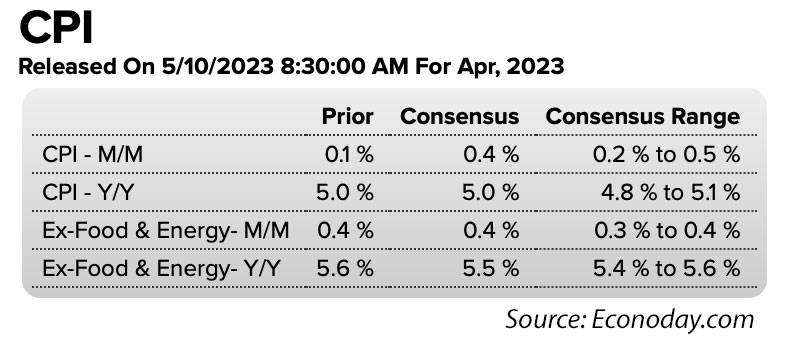

Here’s a quick overview of today’s inflation report:

The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.4% in April on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 4.9%.

Core inflation, which removes food and energy, increased 0.4% for the month and 5.5% year over year.

All of these numbers either matched or came close to economist estimates, so no surprises. Although inflation increased 0.4% in April, up from 0.1% in March, the annual all-items number declined from 5.0% to 4.9%, a slight bit of good news. The annual inflation rate has now fallen 11 months in a row. More worrisome is the fact that core inflation is holding steady around 5.5%. Here is a look at all-items and core inflation over the last year:

The BLS noted that the index for shelter (up 0.4% for the month and 8.1% for the year) was the largest contributor to the monthly all items increase, followed by increases in the index for used cars and trucks (up 4.4% for the month) and the index for gasoline (up 3.0%). Food prices, which have been moderating in recent months were up 0.4% for the month and 4.9% year over year. The BLS said the cost of food at home showed no change in April.

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For April, the BLS set the inflation index at 303.363, an increase of 0.51% over the March number.

For TIPS. The April inflation report means that principal balances for all TIPS will increase 0.51% in June, after increasing 0.33% in May. For the 12 months ending in June, principal balances will have increased 4.9%. Here are the new June inflation indexes for all TIPS.

For I Bonds. The April inflation report is the first of a six-month string that will determine the I Bond’s new variable rate, which will be reset Nov. 1, 2023. So far, one month in, inflation has been running at 0.51%.

One thing to keep in mind as we continue into summer is that non-seasonally adjusted inflation tends to run higher than seasonally-adjusted from January to June, and then lower from July to December. So the next couple months could indicate a higher number than reality. Here are the data:

There’s nothing in this April inflation report that would take the Federal Reserve off its course to hold the federal funds rate in the range of 5.00% to 5.25%. The April numbers matched expectations, and even though annual all-items inflation is gradually declining, inflation remains unacceptably high.

Final thoughts

I am writing this on board a 16-passenger ship moored just off of the town of Puerto Villamil on Gallapagos’s Ilsa Isabela. Today I was lucky enough to have a very slight internet connection; enough to get this posted. But first, I went snorkeling in a pretty area accompanied by four or five friendly and curious sea lions. It’s been a good trip so far.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’ve just returned to Quito, Ecuador’s capital city, after spending five days in the Amazon jungle at a surprisingly pleasant eco lodge on a tributary of the Napo River.

My favorite sighting so far: the Hoatzin (a lot of them).

The good news: We saw four different types of monkeys, 40+ species of colorful birds, gorgeous wild plants, a bunch of giant rodents and two tarantulas. The bad news: My internet access was extremely limited and even now is quite slow. Next week will probably get much worse, so I thought I’d better take the time now to catch up on financial events of the last week.

The Fed

I haven’t been able to closely follow the Fed’s actions or listen to Powell’s press conference. But from what I can gather, the Fed decided to raise its federal funds rate 25 basis points, to a range of 5.00% – 5.25% and then call a halt, at least temporarily.

I like this move and it is what I expected as the United States continues slogging through a slow-motion banking crisis. It does mean that short-term interest rates will be slightly higher than current U.S. inflation (now at 5.0% annually). Of course, this week’s April inflation report could change that equation. I think the Fed knows troubled times are coming, because of …

The debt-limit crisis

I saw that the Treasury Secretary Janet Yellen theorized that the x-date for hitting a hard debt limit could come as soon as June 1, or possibly early July. That was earlier than expected and not good news. Congress remains deadlocked and no compromise looks possible. A more likely result will be a temporary extension of the debt limit, possibly through September, to allow more time for serious talks.

This debt limit fiasco seems to have had little effect — so far — on the U.S. stock market, which finished last week down about 0.8%. Not bad. Of course, the Fed decision to halt interest rate increases was a counter-balancing positive for the market.

T-bill yields

I have written about how similar debt-ceiling events in 2011 and 2013 caused brief disruptions in short-term Treasury yields, with investors demanding higher yields because of the potential turmoil. In recent weeks, we saw this brewing right before our eyes with investors pouring into 4-week T-bills (in theory maturing before the crisis) and demanding higher yields on 8-, 13- and 26-week T-bills, which looked likely to get caught in the political mess.

Now, with Yellen announcing a potential x-date of June 1, that situation has reversed, and the 4-week T-bill is now most at risk. The result: Last week’s 4-week Treasury auction got an investment rate of 5.964%, up an incredible 206 basis points from 3.905% the week before.

Click on image for larger version.

This trend is likely to continue — and worsen — as a true hard debt limit looms over the market in coming weeks.

Real yields

I’m pleased to see that nothing “major” has been happening with real yields of Treasury Inflation-Protected Securities as we approach the next TIPS auction, the May 18 reopening auction of CUSIP 91282CGK1, a 10-year TIPS.

The 10-year real yield is holding at 1.23%, down about 13 basis points since the beginning of May. At this point, that auction still looks attractive, but it also makes the current I Bond with a fixed rate of 0.9% look very competitive.

Click on image for larger version.

The most interesting trend from February to May 2023 has been the widening of the long end of the TIPS yield curve. I have been expecting that to happen as the Fed begins winding down this tightening cycle. But I am not expecting yields to decline much on the short end. We’ll see.

Wednesday’s inflation report

Consensus estimates are pointing toward April inflation coming in at 0.4% for the month and 5.0% for the year, which would hold steady with the March number. Core inflation is expected come in at 0.4% for the month and 5.5% year-over-year. None of this can be viewed as “good news,” and if inflation comes in higher than expected, it could rile financial markets.

The U.S. dollar

In Ecuador, the official currency is the U.S. dollar for all transactions. This country widely uses the U.S. $1 coin, which you rarely see in the United States. The U.S. dollar gives this nation a stable economic base for foreign investment, as long as exports are strong. Oil is the largest export at 32% of all exports, and yes, drilling is expanding in the Amazon region.

One predictable side effect of the combination of the Fed rate-hike halt and looming debt crisis is a decline in the value of the U.S. dollar, which has lost 2.3% of its value year to date. A weaker dollar creates an inflationary trend, which could counteract some of the Fed’s attempts to slow inflation. This is a trend to watch.

My schedule

By Wednesday morning I will be in the Galapagos Islands and facing highly uncertain internet connections and shifting schedules for activities. I am not sure when I will be able to post an analysis on the CPI report or preview article on the May 18 TIPS auction. In addition, I may have trouble approving and responding to your comments. Be patient!

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

For most of last week, I was stressing out about today, when I will be leaving for South America for a tw0-week-plus trip. It wasn’t the travel that had me stressed. It was the fact that on May 1 the Treasury would announce the I Bond’s new fixed/composite rate and I’d be away from internet for hours.

My hoped-for sighting.

Well, that worked out. The Treasury — for the first time ever — announced the new rates early, on Friday, since all purchases from Friday through October will be receiving the new fixed rate of 0.9% and composite rate of 4.3%. Thank you, Treasury, for the early announcement.

I am expecting to have very little internet access for much of this trip — which includes high mountains, Amazon jungle and remote islands. And that means I will be late posting news, approving comments and answering questions. There will be some news that needs covering before I get back, and I hope to get to it when the internet gods allow it.

What’s ahead

May 2. TreasuryDirect is going down for maintenance from about 6:30 to 8:30 am EDT. Don’t be surprised if it lasts longer. This shouldn’t be a big deal; there are no Treasury auctions scheduled for Tuesday.

May 3. At about 2:15 pm EDT, the Federal Reserve will announce its latest interest rate decision. Everyone expects a 25-basis-point increase in the federal funds rate, putting the rate in the range of 5.00% to 5.25%, slightly above the current U.S. inflation rate of 5.0%.

The key thing will be the message the Fed sends about rates going forward. I don’t usually write about these Fed announcements, which are covered by 1,000 media outlets. But it will be an important bit of news to watch.

May 7. TreasuryDirect is going to remove its notorious “virtual keyboard” sometime this week to “improve the customer experience.” I actually like that keyboard, but it has very few fans. One problem is that it discourages users from creating complex passwords using a password manager. So it actually lessens security, somewhat.

I have no idea what will replace it. Usually, I would write a guide about the changeover, but that probably won’t be possible, because I will be in an the Amazon jungle about that time.

May 10. The Bureau of Labor Statistics will release its April CPI report. All CPI reports are crucial, but this one is a little less so since the March report set the I Bond’s current variable rate of 3.38%. I will try to post an analysis when I can get connected.

The Cleveland Fed’s inflation nowcasting is predicting all-items inflation of 0.6% for April and 5.2% year over year, putting U.S. inflation back on an upward path. That would be bad news for the markets, but these Cleveland Fed predictions often miss the mark.

May 11. Treasury will announce the May 18 reopening auction of CUSIP 91282CGK1, creating a 9-year, 8-month TIPS. I would normally post a preview article on Sunday morning, May 14. That might (or might not) happen.

May 18. If all goes as planned, I will be home on the day of the 10-year TIPS auction, which closes at 1 p.m. EDT, and things will be returning to normal. I will posting the results and an analysis after the auction.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Composite rate will fall from 6.89% to 4.30%, but the fixed rate of 0.9% is highly attractive for long-term holders.

By David Enna, Tipswatch.com

Surprise! I Bonds purchased from May to October 2023 will get a fixed rate of 0.9% and a composite rate of 4.3%, TreasuryDirect announced this morning, jumping the gun on its expected May 1 press release. It’s all right there on its homepage:

At first, I thought this was posted by mistake, jumping ahead of Monday’s announcement. In the 12 years I have been writing about I Bonds, the new rates have never been announced early.

A few minutes later, the TreasuryDirect site went down, possibly because of the “what the hell?” factor driving traffic. But I was able to return to the site a bit later and it loaded, with the same information.

I had been speculating that the I Bond’s new fixed rate would be about 0.6%, so 0.9% is great news. It is the highest fixed rate since the reset in November 2007. The fixed rate tells you how much the I Bond will earn above official U.S. inflation. It is equivalent to the “real yield to maturity” of a Treasury Inflation-Protected Security.

The site has the full information on the new rate and how it was determined, combining the new inflation-adjusted variable rate of 3.38% with the new fixed rate of 0.9%.

Fixed rate

0.90%

Semiannual (1/2 year) inflation rate

1.69%

Composite rate formula: [Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

[0.0090 + (2 x 0.0169) + (0.0090 x 0.0169)]

Gives a composite rate of

[0.0090 + 0.0338 + 0.0001521]

Adding the parts gives

0.0429521

Rounding gives

0.043

Turning the decimal number to a percentage gives a composite rate of

4.30%

TreasuryDirect’s page listing the history of fixed rates now includes the 0.9% rate, more than doubling the 0.4% fixed rate in effect for purchases through April 30.

The current composite rate for I Bonds purchased through April 30 is 6.89% and that will fall to 4.3% for purchases from May to October 2023. But the fixed rate of 0.9% makes the May-to-October purchases very attractive.

Just as an aside, the new composite rate for I Bonds purchased from November 2022 to April 2023 will be 3.79%, which reflects the fixed rate of 0.4% and inflation-adjusted rate of 3.38%.

TreasuryDirect said this week that the last day to place orders for the 6.89% rate was yesterday, April 27. (I placed my order on April 26.) So I am assuming that any I Bond purchased today will get the new May 1 rate. And that could be why the Treasury decided to post the new rate information, since we can assume it will take effect for purchases today.

EE Bonds

The Treasury also announced that the new fixed rate for EE Bonds will be 2.5% for savings bonds issued from May 1 to Oct. 31, 2023. This is up from the current fixed rate of 2.1%. The Treasury is retaining the policy that EE Bonds are guaranteed to double in value if held for 20 years, creating an effective interest rate of 3.53%.

Gift box strategy?

The Treasury limits purchases of I Bonds to $10,000 per person per year, so investors need to think through a strategy for the best time to invest. If you were planning on holding the I Bonds for less than 2 years, the smart move was to buy in April, locking in an annual return of about 5.4%. For long-term holders, buying in May is preferable, locking in the 0.9% fixed rate for the full 30-year term of the I Bond.

Earnings from the new 0.9% fixed rate create a breakeven period of about 3 years, 8 months. If you plan to hold less than 3 years, 8 months, buying in April works out better. Anything longer will make the May rate more attractive.

The dilemma: Now the fixed rate rises to 0.9%, but you already bought your full allocation this year. (True for me.) What do you do?

If you bought in April, like I did, you can still use the gift box strategy if you have a spouse or a trusted friend or family member with a separate TreasuryDirect account. Using this strategy, anytime before the end of October you can place $10,000 into the TreasuryDirect gift box, assigned to your partner, and your partner would do the same for you.

Some basics of the gift box strategy:

When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

“I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Rolling over 0.0% fixed rates?

If you are holding I Bonds with 0.0% fixed rate — especially those held for five years or more — you can consider redeeming those older I Bonds for new ones with the 0.9% fixed rate. When you redeem, you will owe federal taxes on the interest earned.

I think this is a sound strategy, especially if you don’t want to raise another $20,000 to buy I Bonds this year in two separate accounts.

One key thing to consider is to wait until the current variable rate of 6.48% has completed and the new rate of 3.38% has begun. You have until October to make a purchase of I Bonds with the 0.9% fixed rate. No rush.

If you have held the I Bond less than five years, consider waiting an extra three months to have the three-month interest penalty apply to the lower composite rate.

Projecting the fixed rate

We still don’t know how the Treasury decides on setting the fixed rate of the I Bond, but it’s becoming clear that the rate tracks higher and lower with real yields of Treasury Inflation-Protected Securities. We just don’t know how much. TreasuryDirect recently added this “less vague” statement to its FAQ page on I Bonds, clearly indicating that market real yields are a factor in setting the fixed rate:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

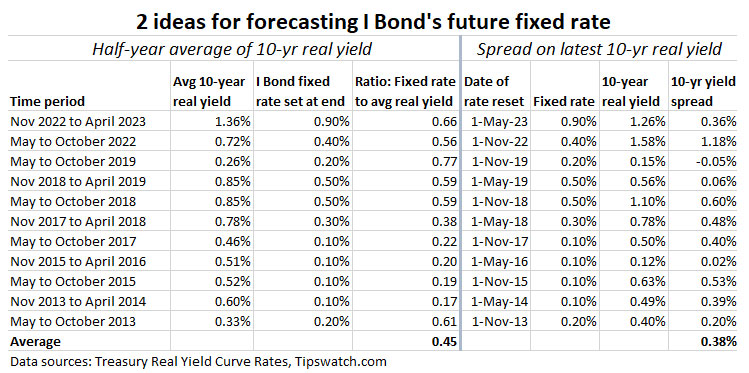

Here is the final version of my two prediction models for the I Bond’s fixed rate. The columns on the left show how the fixed rate compares with the average of the 10-year real yield over the last six-month rate-setting period. The columns on the right show how the fixed rate compares with the latest real yield of the 10-year TIPS.

Click on the image for a larger version.

I have limited these numbers to the times when the Treasury raised the fixed rate above 0.0% going back to November 2013, solidly in the era of Federal Reserve intervention in the U.S. bond market.

If you look at the calculation on the right, the average yield spread between the latest 10-year TIPS and the I Bond fixed rate is 38 basis points. The new fixed rate of 0.9% is 36 basis points below the current 10-year real yield of 1.26%. So that looks good as a predictor, but this calculation isn’t very reliable except to predict if the fixed rate is likely to rise or fall.

The half-year average calculation is more reliable, I think, and in more recent rate changes the ratio has been in the range of 0.59 to 0.77. Today’s fixed rate announcement of 0.9% puts the ratio at 0.66, right in the middle. I think this half-year-average formula is more reliable, but still nowhere near perfect.

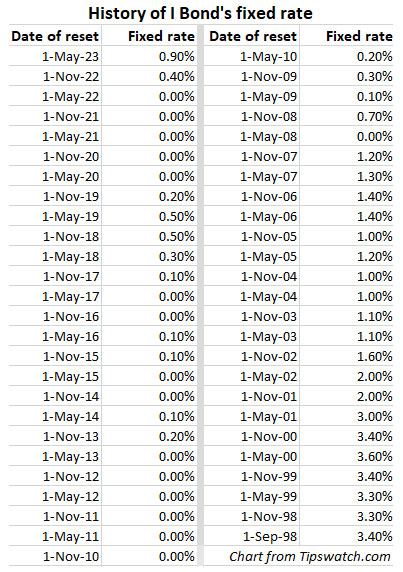

To close, here is the history of all fixed rates for I Bonds back to their inception in September 1998:

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…