By David Enna, Tipswatch.com

The U.S. Treasury just reported that its offering of $15 billion in a reopened 10-year TIPS — CUSIP 91282CGK1 — generated a real yield to maturity of 1.182%, a bit higher than expected.

This TIPS has a coupon rate of 1.125%, and it was trading on the secondary market with a real yield of 1.15% in the hour before the auction closed. So it looks like demand was weak for this offering. The bid-t0-cover ratio was 2.28, well below the originating auction’s 2.79 on Jan. 19, 2023. That January auction drew high demand; but demand for this reopening looks pretty weak.

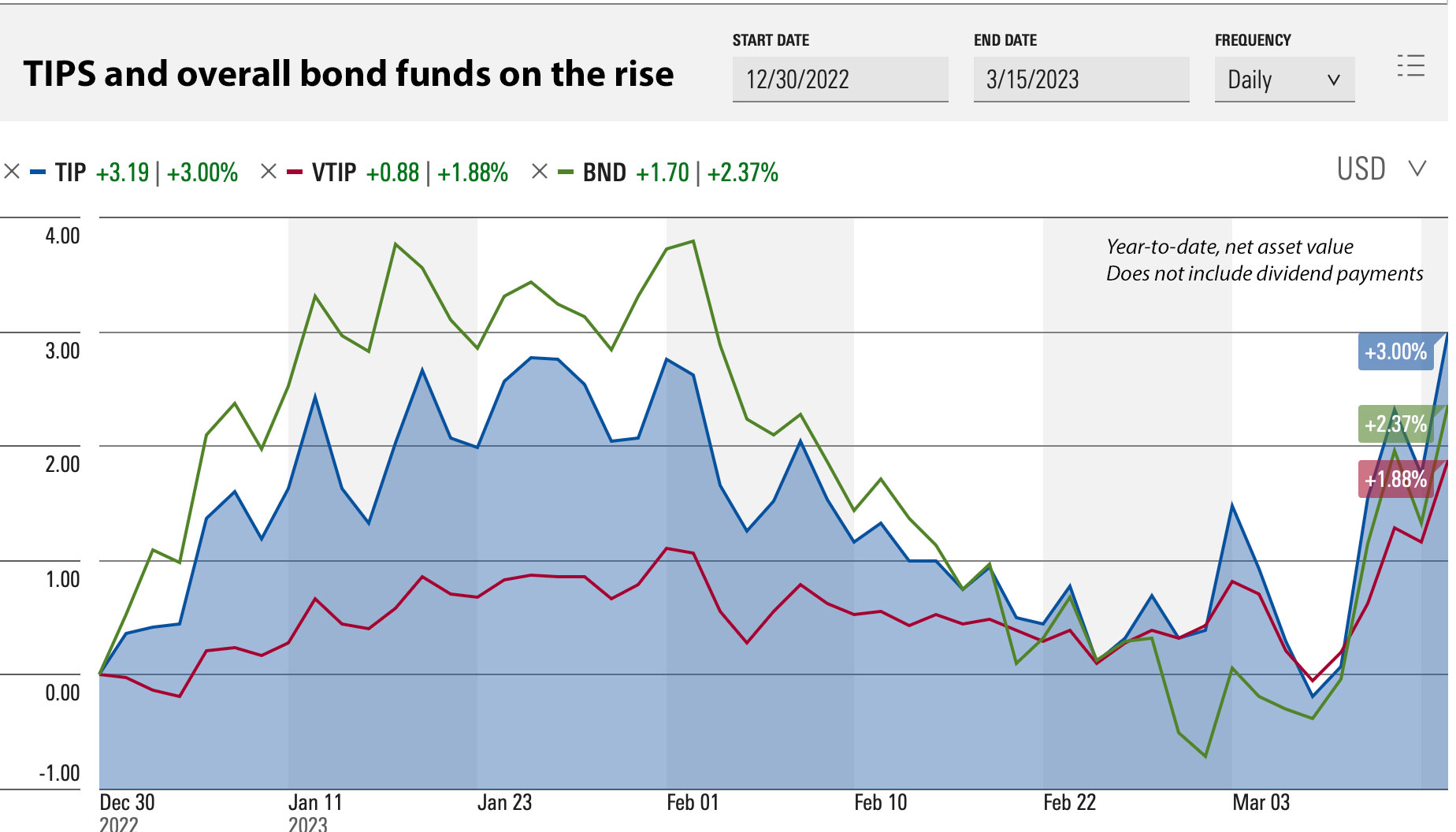

Here is a chart of the 10-year real yield over the last 13 years, showing that today’s yields remain high based on historical trends:

Pricing

This TIPS will have an inflation index of 1.00409 on the settlement date of March 31. Investors paid an unadjusted price of about 99.473545 for $100 of par value. The adjusted price, which includes the inflation accrual, was 99.880392.

This means an $10,000 par investment in this TIPS was actually purchasing $10,040.90 of principal, at a cost of $9,988.04. One positive point is that investors paid below par value for a higher amount of principal. The value of a TIPS investment can never fall below par value at maturity, even in a time of severe deflation.

Plus, this TIPS will pay a coupon rate of 1.125% for the next 10 years.

Inflation breakeven rate

At the auction’s close, a 10-year nominal Treasury note was yielding 3.44%, creating an inflation breakeven rate of 2.26% for this reopened TIPS. This looks like a reasonable number, a bit below most recent auctions of this term.

Here is the trend in the 10-year inflation breakeven rate over the last 13 years, showing the recent decline in inflation expectations as the Federal Reserve continues increasing short-term interest rates:

Final thoughts

I arrived at a hotel in Athens, Greece, about 10 minutes before this auction closed. I am pleased I was able to post this abbreviated version of my usual auction report. Now I am off to dinner (it is 7 p.m. Athens time.) If you invested in this TIPS, please post your reactions and thoughts in the comments section below.

From today’s Reuters report:

The Treasury Department saw slightly soft demand for a $15 billion sale of 10-year Treasury Inflation-Protected Securities (TIPS) on Thursday. The debt sold at a high yield of 1.182%. Demand was below its recent average at 2.28 times the amount on offer.

Here is a recent history of auctions of this term:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…