The I Bond’s fixed rate could rise to 0.6% or higher on May 1. Should you wait? Or look at alternatives?

By David Enna, Tipswatch.com

Update, April 28, 2023: Treasury raises I Bond’s fixed rate to 0.9%; new composite rate is 4.30%

So here we are, in April’s magical two-week period where we can make a somewhat informed decision about buying U.S. Series I Savings Bonds in 2023.

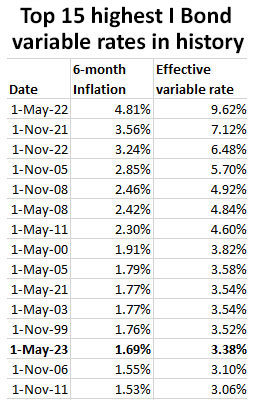

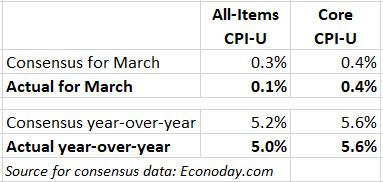

We learned a key piece of information Wednesday with the release of the March inflation report, which set the I Bond’s new variable rate at 3.38%, down dramatically from the current 6.48%. But this drop in yield was expected. U.S. inflation has fallen from a high of 9.1% in June 2022 to the current rate of 5.0%, the lowest since May 2021.

A key thing to understand is that 5.0% is still unacceptably high inflation, reinforcing the importance of long-term inflation protection, which is exactly what the I Bond provides.

But the big difference today versus the last decade is that investors now have equally safe nominal investments with attractively high yields — insured bank CDs, online savings accounts, Treasury money market funds, along with U.S. Treasury bills, notes and bonds.

In addition, there is this obvious alternative: Treasury Inflation-Protected Securities, a more complicated investment that currently offers superior above-inflation returns.

One year ago, in April 2022, you could invest in an I Bond with a yield of 7.12% for six months, then 9.62% for six months. At that time, a 1-year Treasury bill was paying 1.84%. A 5-year TIPS had a real yield of -0.54%. I Bonds were a massively attractive investment in April 2022. Things aren’t so clear today.

So what is an investor to do? First, let’s look at some I Bond basics:

What is an I Bond?

An I Bond is a U.S. government security that earns interest based on combining a fixed rate and an inflation rate.

- The fixed rate will never change. Purchases through April 30, 2023, will have a fixed rate of 0.4%. That could change on May 1, when the Treasury resets the rate. It’s possible that rate could go higher, which would benefit people buying after May 1.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 6.48% annualized. It will adjust on May 1 to 3.38% annualized, based on U.S. inflation from September 2022 to March 2023. The new variable rate will eventually roll out to all I Bonds, depending on the original month of purchase.

- The combination of these two creates the I Bond’s composite rate, which is currently 6.89%. The rate after May 1 will depend on how the Treasury sets the fixed rate. If it remains at 0.4%, then the new composite rate will be 3.79%. But remember it could be higher, but only for I Bonds purchased after May 1.

When you purchase an I Bond, you get the current composite/variable rate for a full six months, and then you transition to the next variable rate for a full six months.

Buying in April. April buyers know both the current composite rate (6.89%) and the next one (3.79%), locking in a compounded return of about 5.4% over the next year.

Buying in May. For a May purchase, investors only know the first six-month variable rate of 3.38%. The new fixed rate won’t be announced until May 1.

One key “negative” of I Bonds is that the Treasury limits purchases to $10,000 per person per calendar year. For this reason, I advise people interested in inflation protection to invest in I Bonds up to the limit each year, and continue holding until they really need the money.

Also, I Bonds cannot be redeemed until you own them 12 months. If you redeem them after 1 year but before 5 years, you will lose the last three months of interest. After five years, you can redeem any amount at any time with no penalty.

Is the fixed rate heading higher?

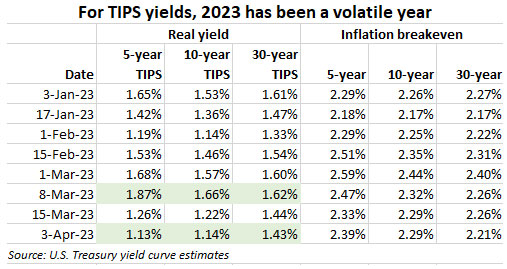

Back on March 9, I wrote an analysis suggesting that Treasury would be likely to raise the I Bond’s fixed rate to somewhere around 0.6% to 1.0% — leading to a guess of 0.8%. But on that very day, Silicon Valley Bank collapsed and we began weeks of financial turmoil, forcing real yields down dramatically. The equation of my highly-thought-out “guess” has changed.

The Treasury has no announced formula for setting the I Bond’s fixed rate, so that means anything I am saying is pure speculation. But my observations — and those of many savvy Bogleheads — indicate that the fixed rate tends to track higher when the real yield of a 10-year TIPS tracks higher. In other words, there is a correlation, but it is not a set formula. It appears to be a formula combined with the whim of the Treasury Department.

The fixed rate is extremely important for an I Bond investor, especially a long-term investor, because it stays with the I Bond for 30 years, or until the I Bond is redeemed. A higher fixed rate is very desirable.

In recent days, without giving this a lot of thought, I have been saying I think the May 1 reset of the fixed rate will fall into a range of 0.4% to 0.6%, but I’d lean more toward 0.6%. Here is an updated chart of the information I am using to make my “guess”:

Most recent real yield theory. On the right side is the equation I have used for years, comparing the potential fixed rate with the most recent real yield of a 10-year TIPS. This technique is hugely inconsistent, but it does a good job of predicting a rise or fall in the fixed rate.

In November 2022, the Treasury set the fixed rate at 0.4%, creating a spread of 118 basis points with the 10-year TIPS. The typical spread in recent years was around 50 basis points, so that 0.4% fixed rate was too low, in my opinion.

But note that since November 2022, the 10-year TIPS real yield has fallen from 1.58% to 1.14%. If you take 50 basis points from 1.14% you get 0.64%, so using this method I think we could see a new fixed rate of 0.6%.

Half-year average theory. On the left hand side of the chart is my newer theory, suggested by readers. To apply this theory, I determined the average 10-year real yield over the rate-setting periods — May to October and November to April for each period the fixed rate was set above 0.0%. Then I calculated the ratio of the new fixed rate to the six-month average.

In the most recent rate reset in November 2022, the fixed rate of 0.40% was 56% of the 0.72% six-month average for the 10-year real yield. If you applied that ratio to current 10-year real yield average of 1.37%, you get a fixed rate of 0.80%, rounded to the tenth decimal point. (Fixed rates are always set to the tenth decimal point, such as 0.40% currently.)

This method lessens the importance of the recent fall in 10-year real yields and points to a new fixed rate of 0.8%, which would be highly attractive.

Conclusion. I’m now guessing a fixed rate of 0.6% to 0.8%. But remember, this is a guess backed up by data, but still a guess.

Higher yield vs. higher fixed rate

Investors buying I Bonds in April get the advantage of locking in a 6.89% composite rate for six months and then 3.79% for six months. So even if the fixed rate rises, buyers in May will need several years to catch up. One of my readers, an Excel whiz who goes by “hoyawildcat,” came up with this explanation of the breakeven periods:

Here are the breakeven dates for I Bonds bought in May (at the new 3.38% variable rate and different fixed rates) vs. I Bonds bought this month (at the current 6.48% variable rate and 0.4% fixed rate).

0.4% — Breakeven: Never

0.5% — Breakeven: April 2040 (16 years 11 months)

0.6% — Breakeven: May 2032 (9 years)

0.7% — Breakeven: June 2029 (6 years 1 month)

0.8% — Breakeven: October 2027 (4 years 5 months)

0.9% — Breakeven: January 2027 (3 years 8 months)

1.0% — Breakeven: May 2026 (3 years)

I’ve seen similar breakeven numbers posted in the Boglehead forum, slightly different, but close enough to get an idea of the April vs. May purchase decision. Most of the Bogleheads seem to be opting for an April purchase.

Remember, you get a ‘mulligan’

While the Treasury limits I Bond purchases to $10,000 per person per year, savvy investors have uncovered a loophole that bypasses that limit: the gift box. This technique works best for spouses or family members, who can each purchase another $10,000 (or more) in I Bonds for each other, deposited in separate gift boxes.

I Bonds placed in the gift box begin earning interest immediately and capture the current fixed rate. When they are delivered in a future year, they apply to that year’s purchase cap for the recipient.

Harry Sit of the TheFinanceBuff.com was the first to write about this strategy on Dec. 27, 2021, in an article titled “Buy I Bonds as a Gift: What Works and What Doesn’t.” When people ask me about the gift box, I point them to this article, which was well researched and thorough. So, go read that article if you don’t know about the strategy.

Some basics of the gift box strategy:

- When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

- The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

- Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

- You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

- “I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

- The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Investment alternatives

A lot of investors have flooded into I Bonds in the last two years, enticed by extremely attractive yields and near-total safety. Those investors were often looking for immediate, short-term returns at a time when savings accounts and money market funds were paying something like 0.05%.

But now, things are totally different. There are many attractive alternatives to I Bonds, such as:

- 1-year insured bank CD paying 5.1%.

- 13-week Treasury bill paying 5.02%.

- 1-year Treasury bill paying 4.64%.

- A 5-year TIPS with a real yield of 1.17%, well above the I Bond’s 0.4%.

- Online savings accounts paying about 4.1%.

- Money market accounts paying more than 4%.

Realistically, I Bonds purchased in April remain competitive, offering a nominal return of 5.4% over one year. But if that I Bond is redeemed in April 2024, the investor loses three months of interest, dropping the yield to about 4.4%. That’s still a good return, but not anything stellar.

I’ve heard from a lot of readers who are planning to bypass buying I Bonds this year and even beginning to redeem I Bonds in coming months as the lower variable rate kicks in. Can’t argue with that, if the investor’s goal is getting the highest near-term yield possible.

I Bonds remain attractive, however, for people seeking to push inflation-protected money into the future, with near-zero risk. I Bonds have better deflation protection than TIPS, have a flexible maturity date and are free of state income taxes. After five years, they become an easily accessible, inflation-protected savings account. You can never lose a penny of principal with an I Bond.

Final thoughts

A month ago, I thought the I Bond’s fixed rate would rise on May 1 to a range of 0.6% to 1.0%. Then came the banking fiasco, and my prediction fell to 0.4% to 0.6%. After writing this article and doing a better analysis, my prediction rises to 0.6% to 0.8%. As I have noted, this is a guess backed up by data.

I am opting to buy our full allocation of I Bonds in April and have set April 26 as the purchase date on TreasuryDirect. If the fixed rate rises dramatically on May 1, I will use the gift-box strategy to add to our holdings. In other words, I can’t lose.

In addition, I most likely will be investing in the new 5-year TIPS going up for auction on April 20. I’ll post a preview article on that April 16.

Later this year, as the lower variable rate kicks in, I may begin redeeming some 0.0% I Bonds that have hit the 5-year mark. Those will become retirement spending money, the reason I bought I Bonds in the first place.

Another viewpoint …

Jennifer Lammer, a YouTube content creator who closely follows I Bonds, just posted this video, reaching a similar conclusion: Buy I Bonds in April, but with a plan to buy more later in the year. There’s a lot of good information here.

What is your strategy? Post your ideas in the comment section below.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…