Everything you are about to read is based on facts … and plain old guesswork.

By David Enna, Tipswatch.com

Update, April 28, 2023: Treasury raises I Bond’s fixed rate to 0.9%; new composite rate is 4.30%

Note, March 13: It has been 5 days since I wrote this article, and while I think it presents a reasonable theoretical way to look at the I Bond’s fixed rate, these predictions are totally shot, at least for now. The 10-year real yield is currently trading around 1.22%, down about 44 basis points in the last 5 days. So … in this troubling environment of bank bailouts, the Fed and markets are likely to change course. Yields leading up to the May 1 decision are likely to be very volatile. (But I think this all still makes a strong case for investing in inflation protection.)

Read this article knowing that it is almost impossible to predict what the I Bond’s fixed rate reset will be on May 1. There are simply too many unpredictable factors.

And now, the original article:

I’ve been getting a lot of questions from readers asking: “Do you think the Treasury will raise the I Bond’s fixed rate on May 1? And what should we do about it?”

It’s still too early to speculate (a lot happens in the bond market every week), but I do think the fixed rate is probably going up on May 1. But by how much? No one can say. The Treasury has no announced formula for setting the I Bond’s rate. It seems to be set based on “whim.” But maybe not totally whim.

First, here are some details about the U.S. Series I Savings Bond, a security that earns interest based on combining a fixed rate and an inflation rate.

- The fixed rate will never change. Purchases through April 30, 2023, will have a fixed rate of 0.4%. The fixed rate is essentially the “real yield” of an I Bond, the amount its return will exceed future inflation.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 6.48% annualized. It will adjust again on May 1, 2023, for all I Bonds, no matter when they were purchased. The starting month of the new rate depends on the month you purchased an I Bond.

- The combination of these two rates creates the I Bond’s six-month composite rate, which is currently 6.89% annualized for I Bonds purchased through April 30.

The fixed rate is extremely important for an I Bond investor, especially a long-term investor, because it stays with the I Bond for 30 years, or until the I Bond is redeemed. A higher fixed rate is very desirable.

But even if the fixed rate rises on May 1, if the increase is small — say from 0.4% to 0.6% — an investor still might want to buy in April to lock in the 6.89% interest rate for a full six months. On a $10,000 investment, that equals $344.50 in interest. A 0.2% increase in the fixed rate only adds $20 a year.

It looks likely that the I Bond’s variable rate will fall on May 1. This is uncertain, with two months of inflation unreported, but the variable rate could fall to something like 3.50%. If the fixed rate rises to 0.6%, the new composite rate would be around 4.12%.

So the investment equation is: 6.89% before May 1 and something like 4.12% after May 1. For a short-term investor, buying before May 1 will make more sense. For the long-term holder of I Bonds, buying after May 1 may be wiser. But of course if you wait, you won’t know if the fixed rate is actually going higher. It’s a risk. Or … it could rise somewhere much higher, like 0.8% or 1.0% and you’d be very happy.

Alternatives. Buy half your $10,000 I Bond allocation in April and the other half in May. Or, some investors — those with spouses and two separate TreasuryDirect accounts — could use the “gift box” strategy. Buy your full allocation in April and then, if the fixed rate rises dramatically, use the gift box in May to invest another $10,000 each.

Handicapping the fixed rate

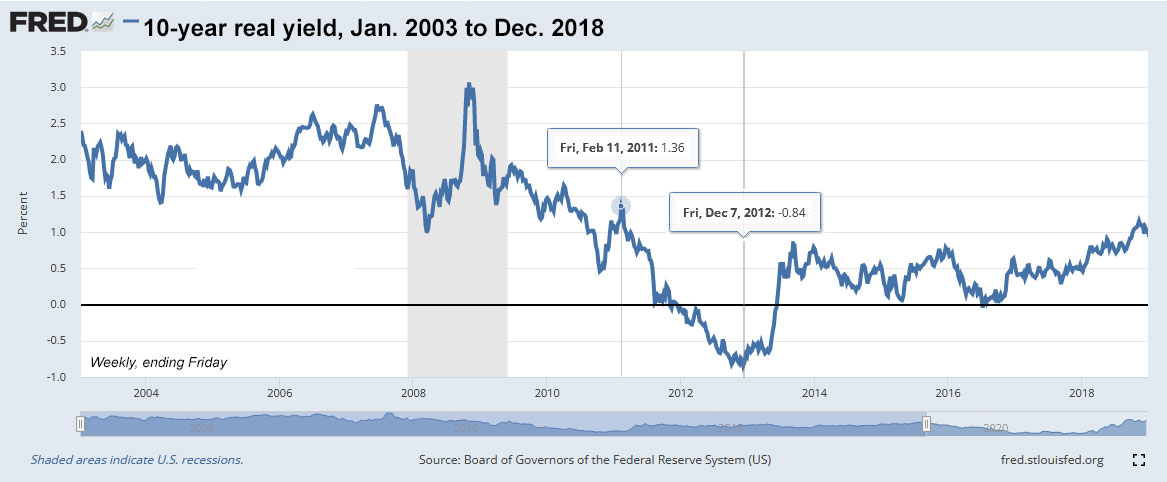

Although the Treasury has no public formula for setting the I Bond’s fixed rate, I have long speculated that the fixed rate will tend to track (although lower) with the real yield of a 10-year Treasury Inflation-Protected Security. Last October, I suggested that the fixed rate was likely to rise to a range of 0.3% to 0.5%, even though a higher fixed rate was justified. The Treasury settled on 0.4%. I got lucky on that prediction.

On October 31, 2022, the 10-year TIPS was yielding 1.58%. The I Bond’s fixed rate generally lags 50 to 75 basis points lower than the 10-year real yield, so a higher fixed rate was justified, in my opinion. But real yields at that point had just recently surged higher. It was hard to forecast a longer-term trend.

Several readers have suggested that the Treasury may take an average of the 10-year real yield over the previous six months and then apply a ratio to that yield to set the I Bond’s fixed rate. I liked that idea, at least in theory. So I took a look at recent rate-setting periods where the fixed rate was set higher than 0.0% to compare the six-month-average theory against the most-recent-yield theory:

OK, to be honest, neither theory works well enough to be relied on as a predictor and that puts us back to the “whim of the Treasury” theory for setting the I Bond’s fixed rate. It says so right in the Federal Register:

The Secretary of the Treasury determines the fixed rate of return. The fixed rate is established for the life of the bond. This amendment clarifies that the fixed rate of return will always be greater than or equal to 0%.

Still, I think market real yields do play a role in this rate-setting exercise.

Half-year average theory. To apply this theory, I determined the average 10-year real yield over the rate-setting periods — May to October and November to April for each period the fixed rate was set above 0.0%. Then I calculated the ratio of the new fixed rate to the six-month average.

In the most recent rate reset in November 2022, the fixed rate of 0.40% was 56% of the 0.72% six-month average for the 10-year real yield. If you applied that ratio to current 10-year real yield average of 1.41%, you get a fixed rate of 0.80%, rounded to the tenth decimal point. (Fixed rates are always set to the tenth decimal point, such as 0.40% currently.)

But … this history of rate resets is highly inconsistent, with the ratio averaging just 34%. If you apply that to the current average of 1.41%, you get a fixed rate of 0.50% (rounded), still higher than the current 0.40%.

The more-recent ratios have tended to fall around 60%, which would give you a fixed rate of 0.80%.

Most recent real yield theory. This theory — which looks at the yield spread between the I Bond’s new fixed rate and the most recent 10-year TIPS yield — is also hugely inconsistent, but it generally does a good job of predicting when the fixed rate is likely to rise or fall.

The fixed rate of 0.4% in November resulted in a yield spread of 118 basis points, the highest margin going back 13 years. It’s possible the Treasury saw the then-recent surge in real yields as temporary, so it held the fixed rate lower than it might have otherwise.

If you apply a spread of 50 to 75 basis points (the average is 67 bps) you get a fixed rate of 0.90% to 1.20%, based on the current real yield of 1.66%.

Conclusion

I think the fixed rate is heading higher, possibly to around 0.6% on the low end and 1.0% on the high end. Let’s just say –er, guess — 0.8%. Feel free to crowdsource your own ideas and theories in the comments sections below.

Plus, remember that a lot can change before May 1, and the Treasury can do anything on a “whim.”

I’ll be taking another look at this issue — and potential I Bond investing strategies — after we learn the new variable rate, which will be set by the March inflation report released on April 12, 2023.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…