Real yield to maturity could be the highest in 12 years.

By David Enna, Tipswatch.com

The Treasury on Thursday will offer $9 billion at auction for a new 30-year TIPS, CUSIP 912810TP3. The real yield to maturity and coupon rate will be determined by the auction results, but it’s looking like this TIPS will get the highest real yield at auction for this term since at least 2014, possibly back to 2011.

The U.S. Treasury on Friday was estimating the real yield of a 30-year TIPS at 1.53%, up 20 basis points since the beginning of February. If that real yield holds through the auction on Thursday, this new TIPS would get a coupon rate of 1.5%, the highest since an originating auction in February 2011.

Oh no, nostalgia!

Ah, 2011 … that was the year I created Tipswatch.com, with the first post on April 10, 2011. A couple months later I weighed in on a 30-year TIPS reopening auction, for CUSIP 912810QP6. My preview was fairly negative. In the last few months, a few readers have quoted that article back to me to demonstrate how unpredictable the Treasury market can be. (Oh yes, I am fully aware of that.)

That 30-year TIPS auction on April 10,2011, ended up getting a real yield to maturity of 1.744%, which looks outstanding today, but was rather disappointing at the time. Hard to believe, isn’t it? Here is what I said in my preview article:

The auction yield should be around 1.8%, probably a bit higher. This is 110 basis points higher than the going rate on a 10-year TIPS, and a whopping 230 basis points higher than a 5-year TIPS. You will get that yield for 30 years, on a principal base that is constantly increasing with inflation. …

That yield is not great. In fact, this TIPS was first issued four months ago with a base rate of 2.19%. It is likely that the TIPS rates will begin – eventually – moving more toward ‘normal’ levels, and for a 30-year that would be nearly 3%. However, I have been saying that for quite awhile, and I have been wrong.

Why did I say a real yield of 3% was “more normal”? That was based on data available in 2011. The Treasury had stopped issuing 30-year TIPS from October 2001 to February 2010. So this was the total history of 30-year TIPS auctions at the time:

Still, I did invest in CUSIP 912810QP6, which ended up getting a real yield to maturity of 1.744% (a record-low for this term at the time). In 2011, I was disappointed. Today, I am quite happy and I am still holding that TIPS, which has a solid coupon rate of 2.125% and an inflation index of 1.357.

Point of this history lesson: We can’t accurately predict where interest rates are headed. What looked disappointing in 2011 ended up being a prize investment in my TIPS portfolio.

Back to this week’s auction!

For two kinds of investors, a 30-year TIPS with a real yield of 1.50% could be attractive: 1) a buy-and-hold-to-maturity investor who is young enough to survive 30 years, and 2) a TIPS trader who believes that real yields are likely to fall in the relatively near future, which would bring capital gains on a trade.

I am neither 1 nor 2, so I am no longer interested in investing in 30-year TIPS. These TIPS are highly volatile investments and require discipline to hold through wild swings higher or lower in market value.

Although real yields on the secondary market for this term were higher in October 2022, 1.53% remains attractive. Just a year ago, in February 2022, a new 30-year TIPS auctioned with a real yield of 0.195%.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.53% means an investment in this TIPS will exceed U.S. inflation by 1.53% for 30 years. If inflation averages 2.3%, you’d get a nominal return of 3.83%, on par with a nominal 30-year U.S. Treasury. But if inflation averages 4.5%, you’d get a nominal return of 6.03%.

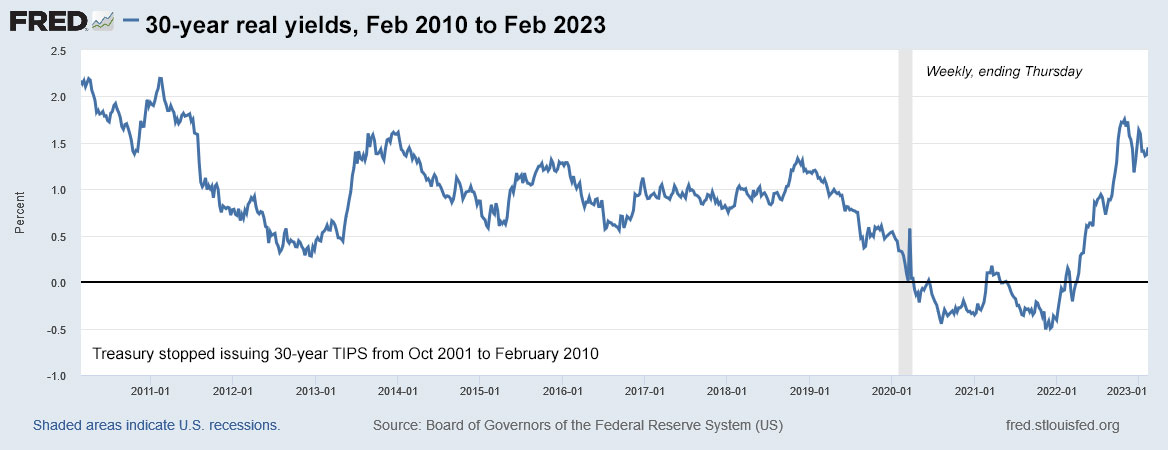

This chart shows the history of 30-year real yields since the Treasury reinstated the 30-year TIPS in February 2010:

For much of this 13-year period, the 30-year real yield lingered in a range around 1.0%, but keep in mind that real yields were suppressed by the Federal Reserve’s quantitative easing. Now we are in a period of quantitative tightening, and there is no way to predict how long that will last or the eventual result on real yields.

For an investor of the right age looking to build a buy-and-hold TIPS ladder, this 30-year TIPS looks like a reasonable investment. As long as that investor can ignore market volatility, which could be extreme in either direction.

Inflation breakeven rate

With the 30-year nominal Treasury bond closing Friday with a real yield of 3.83%, a new 30-year TIPS with a real yield of 1.53% would have an inflation breakeven rate of 2.3%, a bit higher than recent auctions of this term. But 2.3% looks reasonable. Over the last 30 years, inflation has averaged 2.5% a year. For all 30-year periods beginning in 1971, only one period has had inflation lower than 2.3% — 1990 to 2020 at 2.2%.

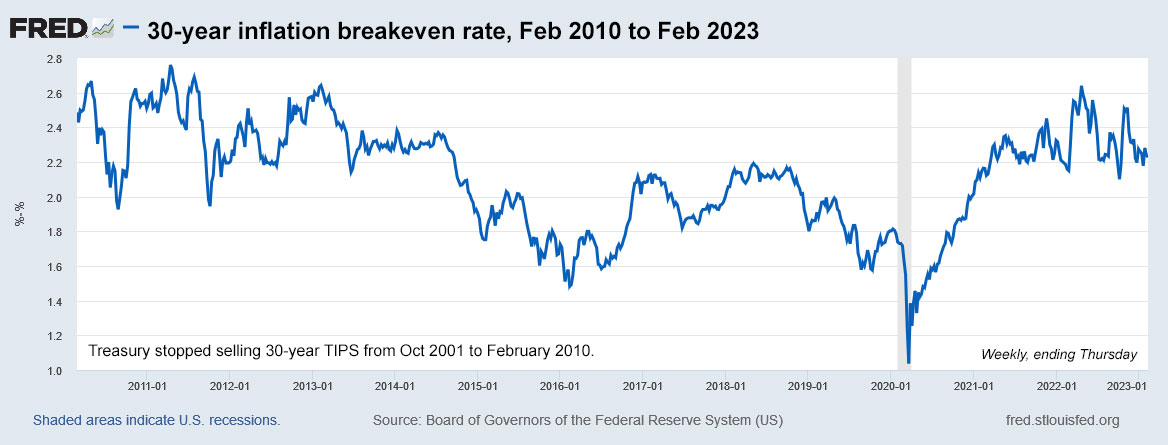

Here is the trend in the 30-year inflation breakeven rate from 2010 to 2023:

Final thoughts

I won’t be a buyer, but that is based on my age and ability to hold to maturity. My current TIPS ladder stretches out to February 2043, when I will be approaching 90. I still have some spots to fill, but I will be focusing on TIPS maturing in 5 to 19 years. For example, next month on March 23 we will have a 10-year TIPS reopening auction, and then on April 20 a new 5-year TIPS will be issued.

Investors looking at this new 30-year TIPS should focus on buying it in a tax-deferred account, but because the coupon rate will be around 1.5%, that should be adequate to cover “phantom income taxes” in a taxable account. Investors in a taxable account have to pay taxes on TIPS inflation accruals in the current year.

You can track the Treasury’s daily Yield Curve updates here. Yields are likely to continue to be volatile into next week. This auction closes at noon Thursday for non-competitive orders at TreasuryDirect. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting results soon after the auction closes at 1 p.m. ET Thursday.

Here is a history of all 29- to 30-year TIPS auctions over the last eight years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I don't know anything about TIAA Traditional, but I see it appears to be an annuity. TIAA is a good…