If the real yield holds above zero, this will be the most attractive TIPS auction in more than 2 years.

By David Enna, Tipswatch.com

Something great and unfortunately rarely seen could happen this Thursday, when the Treasury holds a $14 billion auction reopening CUSIP 91282CDX6, creating a 9-year, 8-month Treasury Inflation-Protected Security.

This reopened TIPS could 1) get a real yield positive to inflation, and 2) an auction price at a discount to par value. We haven’t seen either of these things for the last 12 TIPS auctions of this term, dating back to the wildly chaotic auction on March 19, 2020, when the financial markets were roiled by the pandemic outbreak.

CUSIP 91282CDX6 trades on the secondary market, and you can track its real yield to maturity and price on Bloomberg’s Current Yields page. As of Friday’s market close, it had a real yield of 0.18% and a price of $99.45 for $100 of par value. This TIPS is trading at a discount because its real yield now surpasses the coupon rate of 0.125%.

The price investors actually pay at Thursday’s auction will look a little different, however. This TIPS will carry an inflation index of 1.03672 on the settlement date of May 31. That means an investor will pay roughly $103.10 for $103.67 of value, after accrued inflation is added in. In other words, you’ll pay more, but get a matching amount of additional principal.

Side note 1: Note the significance of that 1.03672 inflation index. It means that non-seasonally adjusted inflation will have increased 3.67% in just four and a half months, ending on May 31. That’s amazing.

Side note 2: Ponder just how fast real yields have increased as the Fed began reversing its aggressive quantitative easing of the last two years. On November 18, 2021, a reopened 10-year TIPS auctioned with a real yield to maturity of -.1.145%, the lowest in history for this term. Thursday’s auction looks likely to be about 135 basis points higher … in just six months.

Definition: The “real yield” of a TIPS is its yield above or below official U.S. inflation, over the term of the TIPS. So a real yield of 0.20% means an investment in this TIPS will exceed U.S. inflation by 0.20% for 9 years, 8 months.

Of course, we can’t know what Thursday’s auction price and real yield will be. The Treasury market is experiencing strong volatility. But the trend is definitely higher for real yields, as shown in these Treasury estimates for a full-term 10-year TIPS:

- March 1, 2022: -0.90%

- April 1, 2022: -0.41%

- April 18, 2022: -0.07%

- May 2, 2022: 0.18%

- May 13, 2022: 0.24%

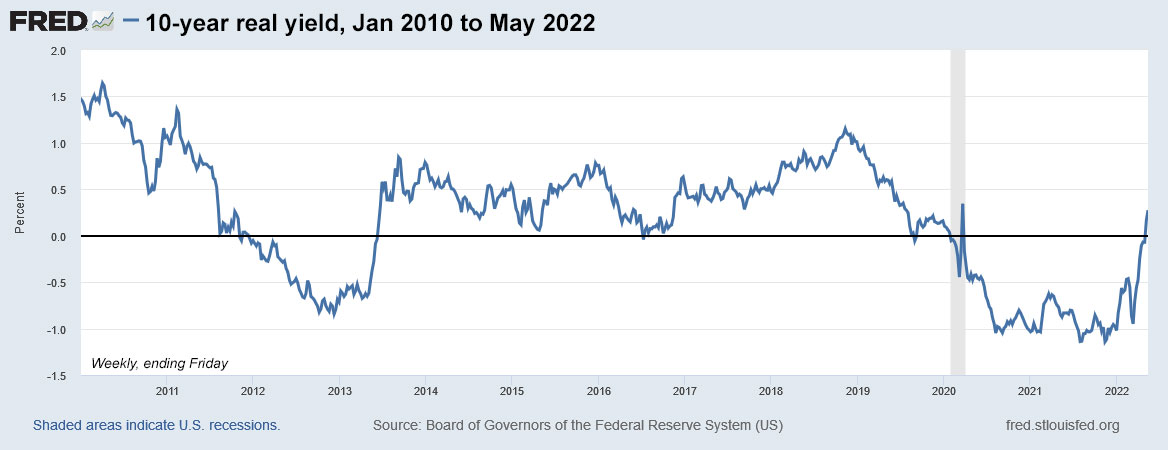

Now let’s take a look at the big picture, with this chart of 10-year real yields over the last 12 years:

This chart shows two full Fed easing cycles: 2011 to 2014 and then 2019 to 2022. The middle section, where real yields are positive, shows what happens when the Fed sustains tightening. In the last tightening cycle beginning in 2014, the Fed gradually increased short-term interest rates and then later began reducing its balance sheet of Treasurys, but even then only made half-hearted reductions.

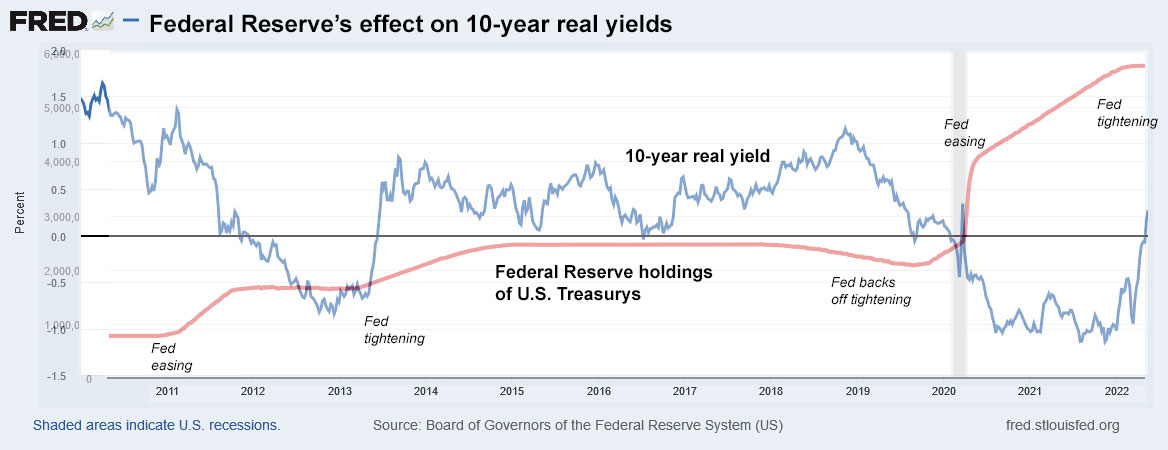

Here is that same chart with the Federal Reserve’s balance sheet of Treasurys overlaid on the 10-year real yield. Notice that when the Fed increases its balance sheet, it does so aggressively. When it reduces it, as in 2019, it does it very gradually (at least in the past):

When the Fed eases — lowering short-term rates and adding to its Treasury holdings — real yields dip well below zero. When the Fed backs off, real yields normalize, above zero. That is where we are today. Except the huge difference in 2022 is that U.S. inflation is running at 8.3% and the Fed knows it has to act aggressively to raise rates and lower its balance sheet. We are only a small step along that process, in my opinion, but the bond market is already pricing in some of the future Fed actions.

Inflation breakeven rate

With a nominal 10-year Treasury trading Friday with a yield of 2.92%, CUSIP 91282CDX6 currently has an inflation breakeven rate of 2.74%, an entirely reasonable number with U.S. inflation running at 8.3%. But as I noted, the bond market has been pricing in future Fed actions, and the market believes inflation can be held in check. In normal times, I’d consider 2.74% a high breakeven rate, but these aren’t normal times.

Here is the trend in the 10-year inflation breakeven rate over the last 12 years, showing that by historical standards, these breakeven rates have tended to top off around 2.6%:

Some thoughts on the auction

If the real yield can hold above zero, CUSIP 91282CDX6 would mark a milestone for TIPS investors, with the first positive real yield after 12 consecutive 10-year auction offerings yielding negative to inflation. I’m calling this attractive. Better yields could be coming, but this one is worth a look.

TIPS vs I Bonds. With a real yield of 0.20%, is a 10-year TIPS more appealing than an I Bond with a real yield of 0.0%, based on the current fixed rate? I’d say no, but things are getting close. The I Bond has advantages because of its flexible maturity date, better deflation protection and built-in deferred federal taxes. The TIPS can be traded on the secondary market, which can be a positive or a negative. I’d still prefer I Bonds for my first $10,000 a year in inflation protection. But this 10-year TIPS looks like a good alternative, if the yield can sustain above zero.

Another advantage for TIPS is that investors can use retirement account money to buy a TIPS in an IRA brokerage account. That means there is no consequence in raising money for the purchase. Sell something, buy something, all in the same account. I Bonds can’t be held in an IRA account, so investors can face tax consequences in raising cash for an investment.

Reader alert: I will be traveling again

I’ll be a buyer of this TIPS, adding to my recent “nibble” purchases as real yields have been rising. This should be the most attractive auction in more than two years.

This auction closes for non-competitive bids at TreasuryDirect at noon EDT on Thursday. If you are buying through a brokerage account, you should make your purchase either Wednesday evening or early Thursday, because auction orders close early at brokerages.

I will attempt to post the auction result soon after it closes at 1 p.m. EDT Thursday. However, I will be out of the country (again), and I can’t be certain of my schedule Thursday. Where am I going? The photo at the right provides a hint.

Until then, here is a history of recent 9- to 10-year TIPS auctions, going back five years. It’s hard to remember, but as recently as November 2018, a 10-year TIPS auctioned with a real yield of 1.109%. Soon after, the stock market tanked and the Fed backed off. A year later, the global pandemic hit. Such interesting times:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…