5-year real yields have increased 88 basis points in the last two months. This TIPS looks attractive, even though real yields could keep climbing.

By David Enna, Tipswatch.com

In the nine days that have followed the release of the somewhat-disturbing May inflation report, the Treasury market has been rocked by aftershocks of volatility.

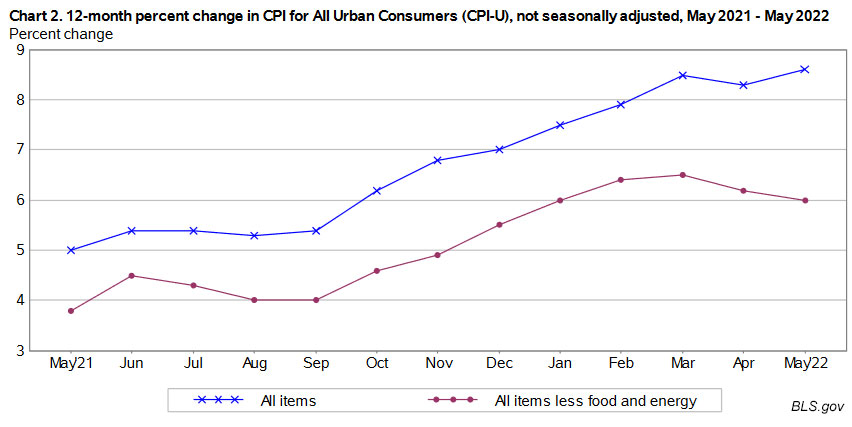

In that nine-day span, the Federal Reserve opted to raise short-term interest rates by 75 basis points, no doubt triggered by the May report, with all-items inflation rising 1.0% and hitting an annual rate of 8.6%. The report showed substantial price increases in every main sector tracked by the Bureau of Labor Statistics. The average American is feeling the pain: Food prices were up 1.2% in the month, and gas prices were up 4.1%.

The May inflation report was issued on June 10, into an environment of already-rising real and nominal interest rates. It set off a wave of uncertainty in the Treasury market.

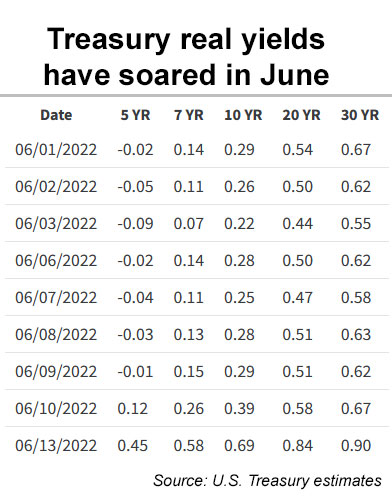

Nominal Treasurys. On June 9, the 5-year Treasury note was yielding 3.07%. It surged to 3.61% on June 14, before closing at 3.34% on Friday.

Treasury Inflation-Protected Securities. Real yields on TIPS were even more volatile, with the 5-year TIPS yielding -0.1% on June 9, rising to 0.73% on June 14 before falling to 0.54% at Friday’s close.

I’ve noted in the past that as the Federal Reserve increases short-term interest rates, the 5-year TIPS will be the auction term most likely to track higher with Fed rate increases, especially as fears of economic decline flatten the yield curve. Right now the Treasury estimates that a full-term 5-year TIPS would yield 0.54%, just 13 basis points below the 10-year TIPS.

Coming Thursday: 5-year TIPS reopening auction

The Treasury will offer $18 billion in a reopening auction of CUSIP 91282CEJ6, creating a 4-year, 10-month TIPS. This issue was originated in an auction on April 21 with a real yield to maturity of -0.34% and a coupon rate of 0.125%. It had an adjusted price of $102.76 for about $100.42 of principal. In my preview article for that auction, I noted:

If the history of the last tightening cycle repeats itself, we should see 5-year TIPS real yields rise at least another 100 basis points. But that forecast is highly uncertain ….

Two months later, the 5-year real yield has already increased 88 basis points. This TIPS, which trades on the secondary market, closed Friday with a real yield of 0.51% and an unadjusted price of $98.17, a decline of about 4% since the originating auction.

Although real yields are likely to continue climbing, I consider a real yield of 0.51% on a 4-year, 10-month TIPS to be attractive. That is a 51-basis point advantage over the U.S. Series I Savings Bond. This auction is worth a serious look.

Definition: The “real yield” of a TIPS is its yield above or below official U.S. inflation, over the term of the TIPS. So a real yield of 0.51% means an investment in this TIPS will exceed U.S. inflation by 0.51% for 4 years, 10 months.

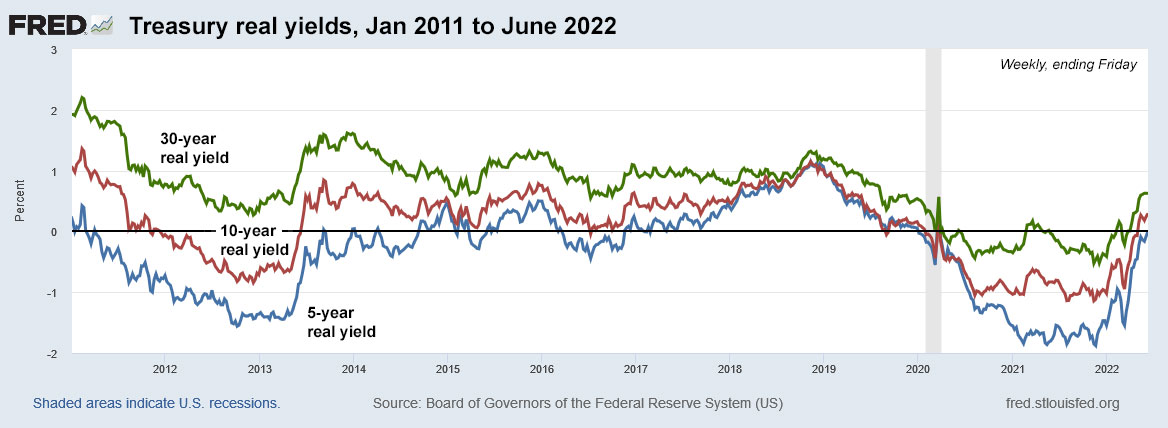

Here’s the trend in the 5-year real yield from 2013 to 2022, showing the potential for the 5-year real yield to continue rising as the Fed continues tightening. At the end of the Fed’s last tightening cycle, the 5-year real yield hit 1.13% in mid-December 2018. I think there is potential for it to go higher this time, unless the U.S. economy drastically worsens:

Pricing. Real yields are in a volatile phase right now, so things could change before Thursday’s auction. (You can track yields in real time on Bloomberg’s Current Yields page.) But let’s say the real yield holds at 0.51% and the price is $98.17 for $100 of par value. Investors will actually be paying more at Thursday’s auction, because this TIPS will carry an inflation index of 1.02376 on the settlement date of June 30. The price should be about for $100.51 for about $102.38 of accrued principal.

That’s a rough estimate, but it means if you put in an order for $10,000 in this TIPS, you will end up paying about $10,051 for $10,238 of principal. From that point on, you will earn 0.125% plus accruals matching official U.S. inflation.

Principal balances for this TIPS will be getting a boost of 1.1% in July, based on May’s rate of non-seasonally adjusted inflation. Investors know this, and it should already be reflected in the pricing.

Inflation breakeven rate

With a 5-year nominal Treasury currently yielding 3.34%, this TIPS has an inflation breakeven rate of about 2.83%, dramatically down from the originating auction when the inflation breakeven rate was 3.34%, probably the highest breakeven ever recorded at auction for any TIPS of any term. While 2.83% is historically high, it seems very reasonable at a time when U.S. inflation is running at 8.6%.

Still, the 5-year nominal Treasury is also getting appealing, especially if you believe the Fed won’t maintain an aggressive course of tightening. I’d probably dabble in the 5-year Treasury note when yields rise above 3.5%. (The next auction of this term is coming Monday, June 27.)

On balance, though, getting a real yield of 0.5%+ makes the 5-year TIPS more appealing, since it provides insurance against unexpectedly high inflation, just like we are suffering today.

Here is the trend in the 5-year inflation breakeven rate from 2013 to 2022, showing that breakevens have slipped lower since the Fed solidly committed to fighting inflation earlier this year:

Conclusion

As long-time readers know, my investing style is to buy TIPS at auction and hold them to maturity. The 5- and 10-year TIPS are perfect for this strategy, and this one will mature in 4 years, 10 months. I’ll be a buyer at Thursday’s auction, as long as real yields hold anywhere near their current levels.

I was looking at my TIPS ladder recently and noticed I have a lot of issues maturing in 2023. Why is that? Because I was heavily buying 5-year TIPS in 2018 in the heart of the Fed’s last tightening cycle, when real yields were in a range of 0.631% to 1.129%. So, even though there are probably going to be better buying opportunities in the near future, I am going to hedge my bets by continuing to add to my holdings while real yields are improving.

This auction closes at noon Thursday for non-competitive bids, like those made at TreasuryDirect. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll report the results after the auction closes at 1 p.m. EDT Thursday.

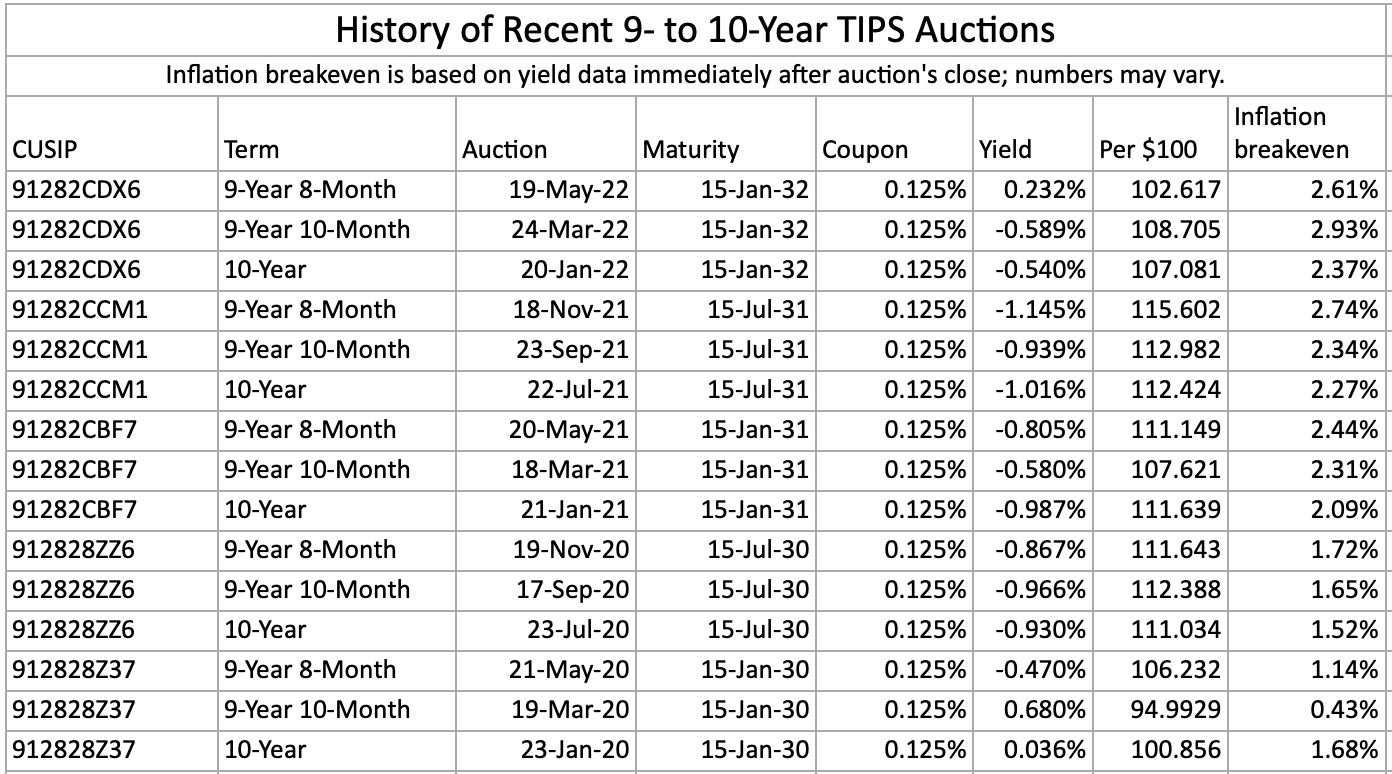

Here is the history of all 4- to 5-year TIPS auctions over the last 9 years, showing the effects of the Fed’s last lukewarm tightening cycle (late 2014 to 2018) and then drastic easing cycle (2020 to 2021):

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…