TIPS remained rather unappealing the entire year, while I Bonds became a superstar investment.

By David Enna, Tipswatch.com

Here is how I can sum up this monumental year of change:

January 2021: “Inflation will never be a problem again.”

December 2021: “We are heading toward inflation Armageddon!“

In January 2021, U.S. inflation was running at an annual rate of 1.4%, continuing an 11-month string with annual inflation under 2.0%. But 11 months later, by November 2021, annual inflation had soared to 6.8%, the highest rate in 39 years. And it shows no sign of waning anytime soon. Here is the trend in annual inflation over the last year:

And yet, even with that shocking surge in inflation, U.S. interest rates continue at extremely low levels. Here are some key data points from 2021:

- The 4-week Treasury began the year yielding 0.09% and is now at 0.01%.

- The 30-year Treasury began the year at 1.66% and is now at 1.96%.

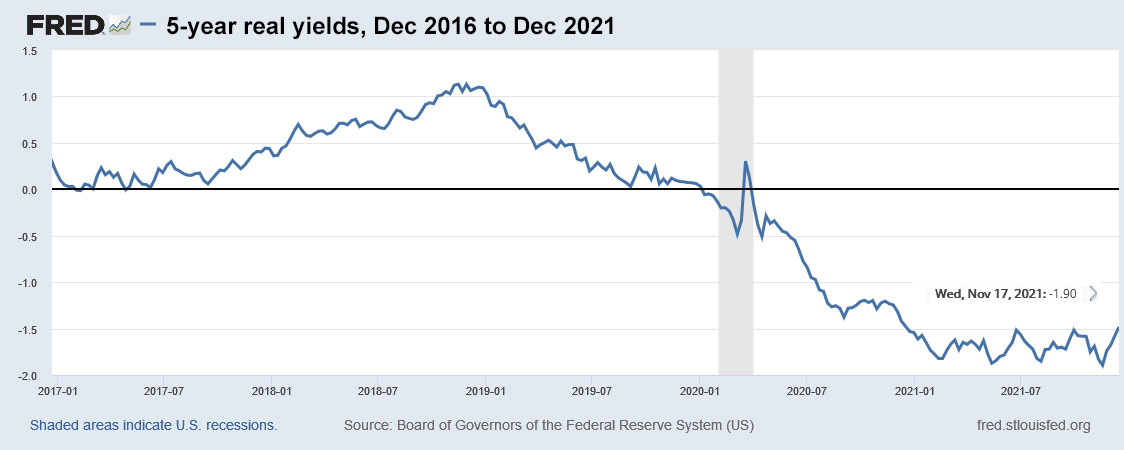

- The real yield (meaning the yield above inflation) of a 5-year Treasury Inflation-Protected Security started the year at -1.62% and is now at -1.54%.

- The real yield of a 10-year TIPS started the year at -1.08% and is now at -0.98%.

- The real yield of a 30-year TIPS started the year at -0.39% and is now at -0.38%.

- The SPY ETF (S&P 500) has had a total return of 29.4% year to date.

- VTIP, Vanguard’s short-term TIPS ETF, has had a total return of 5.25% year to date.

- SCHP, Schwab’s total TIPS fund, has had a total return of 5.48% year to date.

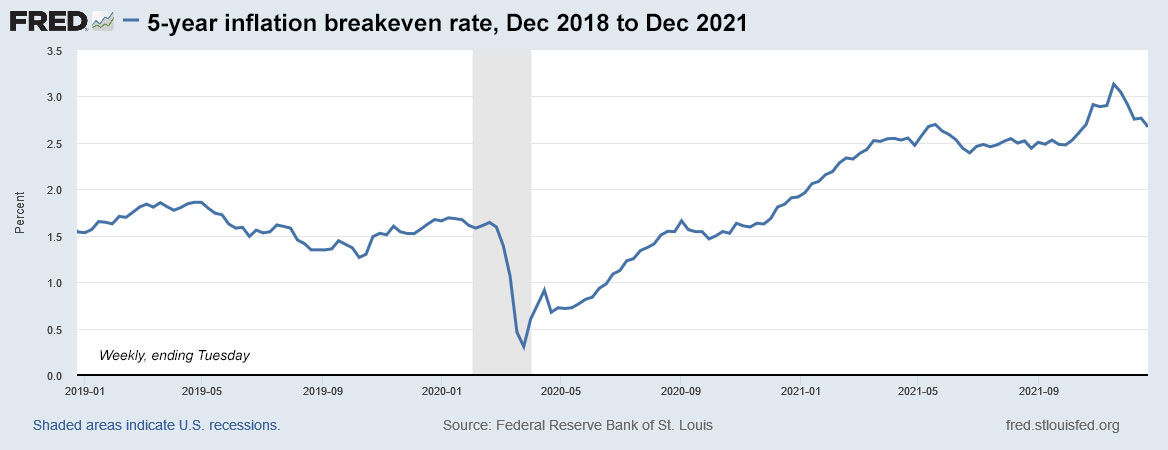

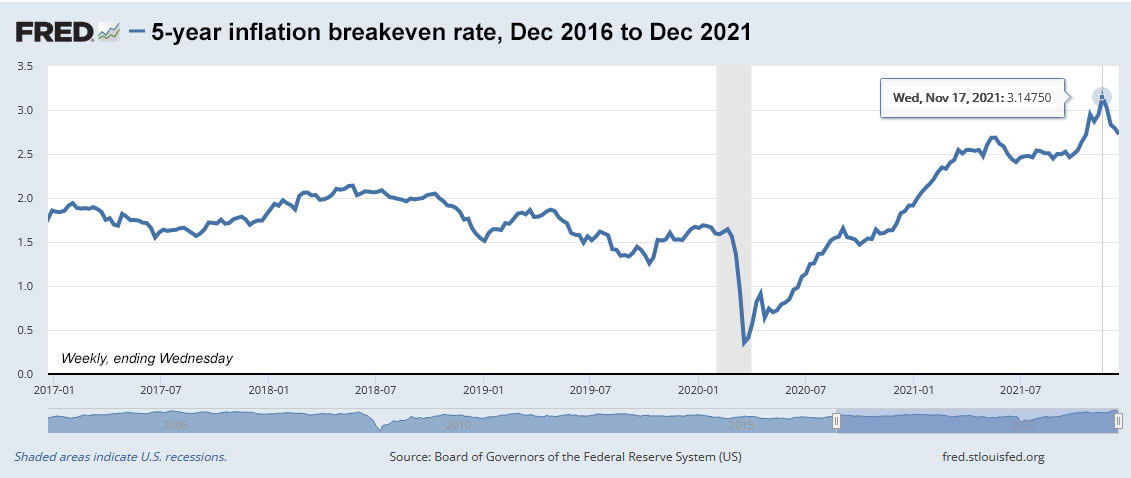

And finally, the 10-year inflation breakeven rate started the year at 2.01% and is now at 2.53%. In other words, investors now sense that inflation might be 52 basis points higher over the next 10 years, even though inflation has soared 540 basis points this year to a 39-year high.

Sometimes I wonder: Am I living in an alternate universe? At some point, and soon: 1) inflation will have to plummet or 2) interest rates will have to rise, dramatically. But for now, all we can do is look back on an eventful year for inflation, and an uneventful year for interest rates.

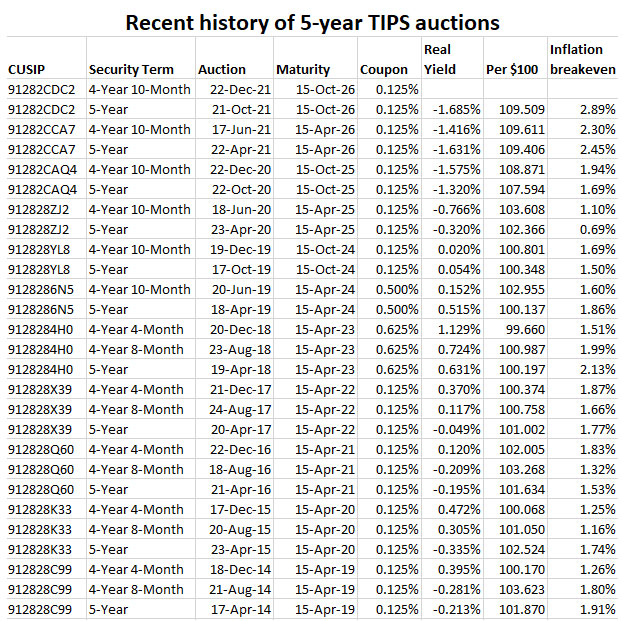

Recapping a year of TIPS auctions

CUSIP 91282CBF7, 10-year TIPS

Original auction, Jan. 21, 2021: Investors got a real yield to maturity of -0.987%, which at the time was the lowest ever for any auction of this term. The inflation breakeven rate was 2.09%, which was the highest for any auction of this term since September 2018. (Just 11 months later, that 2.09% breakeven rate looks almost nostalgic.)

Reopening auction, March 18, 2021: Investors got a much more “attractive” real yield of -0.580%, 38 basis points higher than the originating auction two months earlier. The inflation breakeven rate rose to 2.31%.

Reopening auction, May 20, 2021: The real yield came in at -0.805%, a bit higher than the record low. The inflation breakeven rate continued rising to 2.44%.

CUSIP 912810SV1, 30-year TIPS

Original auction, Feb. 18, 2021: This new 30-year TIPS auctioned with a real yield to maturity just slightly negative to inflation, at -0.04%, to fairly weak investor demand. The coupon rate of 0.125% became the record low for any 30-year TIPS auction in history. The inflation breakeven rate was 2.11%. All in all, this ended up being a fairly attractive auction, especially for TIPS traders.

Reopening auction, Aug. 19, 2021: Six months later, this TIPS reopened with a real yield to maturity of -0.292%, the lowest ever for any TIPS auction of this term. The adjusted price was a hefty $117.72 for about $104.33 of value, after accrued inflation was added in. The inflation breakeven rate was 2.17%, slightly higher than at the originating auction.

CUSIP 91282CCA7, 5-year TIPS

Original auction, April 22, 2021: The Treasury’s offering of $18 billion in a new 5-year TIPS generated a real yield to maturity of -1.631%, which at the time was the lowest real yield at auction for any TIPS in history. The inflation breakeven rate was 2.45%.

Reopening auction, June 17, 2021: This was one of the most interesting auctions of the year, and the only TIPS I actually bought in 2021. (It was a small purchase to test a new brokerage account.) This time, the real yield to maturity rose to -1.416%, boosted by the Federal Reserve’s announcement the day before that it was opening the door to tapering its aggressive bond-buying program. The real yield for this TIPS jumped by 31 basis points in a single day. The inflation breakeven rate dipped to 2.30% based on the Fed’s supposed future actions to calm inflation.

CUSIP 91282CCM1, 10-year TIPS

Original auction, July 23, 2021: There had been 110 TIPS auctions of this 9- to 10-year term since 1997 and this auction’s real yield to maturity of -1.016% set the record low yield, by a large margin. But that record wouldn’t last long. The inflation breakeven rate was 2.27%, which seems surprisingly low.

Reopening auction, Sept, 23, 2021: The real yield at this auction bounced higher, to -0.939%, again spurred by Fed statements the day before indicating actions to slow its bond-buying program. The inflation breakeven rate was 2.34%.

Reopening auction, Nov. 18, 2021: This is where things start to get weird. In November 2021, the Federal Reserve actually began tapering its bond-buying and made clear that interest-rate increases could be coming much sooner than the market expected. The market reacted with a yawn and bid the real yield to maturity of this TIPS down to -1.145%, the lowest ever for any TIPS auction of this term. The inflation breakeven rate soared to 2.74%.

91282CDC2, 5-year TIPS

Original auction, Oct. 21, 2021: Another TIPS auction, another record low yield. The Treasury’s offering of $19 billion in a new 5-year TIPS generated a real yield to maturity of -1.685%, which still stands as the lowest ever recorded for any TIPS auction of any term. The 5-year inflation breakeven rate came in at 2.89%, by far the highest rate for any 5-year TIPS auction in more than a decade. The 5-year breakeven rate was last at this level in March 2005.

Reopening auction, Dec. 22, 2021: The last TIPS auction of the year generated a real yield to maturity of -1.508% and an inflation breakeven rate of 2.73%, down from the October number.

All eyes on I Bonds

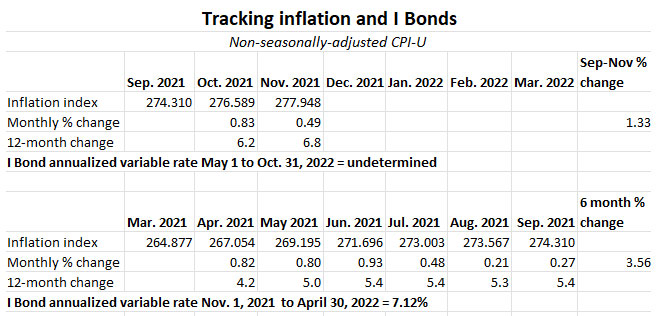

Although the fixed rate for U.S. Series I Savings Bonds stayed steady at 0.0% through 2021, the dramatic surge in U.S. inflation created intense interest in I Bonds as the inflation-adjusted variable rate jumped higher in May, and then even higher in November.

To start the year, through April 2021, I Bonds had a rather mundane six-month inflation-adjusted rate of 1.68%, but that jumped to a much more attractive 3.54% on May 1 and then to the wow-factor rate of 7.12% on November 1. The reason? U.S. inflation rose 3.56% in the six months from March to September 2021, the highest six-month increase in the 23-year history of I Bonds.

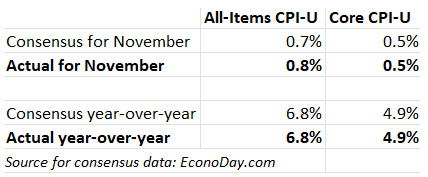

Here are the inflation numbers the Treasury uses to determine the variable rate:

Note that just two months into the next six-month rate setting period, U.S. inflation has been running at 1.33%, which would translate into an annualized six-month variable rate of 2.66%. I Bonds are likely to continue to be a very safe, very attractive investment well into 2022.

TIPS, however, remain rather unattractive, with real yields well below zero. Will 2022 bring dramatically higher real yields? I doubt those will come quickly, but once the market shifts momentum, we could see higher yields, especially for the 5-year TIPS.

At this point, I Bonds remain the most attractive inflation-protected investment in the world. As long as real yields remain depressed, your first $10,000 invested in inflation protection should be allocated to I Bonds. Then consider TIPS.

Happy New Year, everyone.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I meant regarding 'wait it out' on I-bonds... but to me, TIP bonds right now are a horse of a…