“The Fed is in a real pickle. … Being on the tightening side of monetary policy is no fun.”

Here is this week’s “Cents and Sensibility” podcast from inflation guru Michael Ashton. I am a big fan of this podcast and Ashton’s work because he has deep knowledge of how inflation works, but can explain complex issues in an entertaining way.

His podcast intro: “Inflation continues to show broader and deeper, and now is entering the general business and consumer mindset. In this episode, Inflation Guy talks about the idea that year-over-year inflation may peak soon, but probably won’t go back to the old 2% level. In the long term? Well, that depends on whether the Fed can channel Paul Volcker, and worry less about breaking eggs and more about whether we can afford eggs.”

Have a listen:

You can subscribe to this podcast in all the traditional ways, or find it here.

His audiences know him as the “Inflation Guy.” He is a pioneer in the U.S. inflation derivatives market. Before founding his company, Enduring Investments, Ashton worked in research, sales and trading for several large investment banks including Bankers Trust, Barclays Capital, and J.P. Morgan.

Since 2003, when he traded the first interbank U.S. CPI swaps, and 2004 when he was the lead market maker for the CME’s CPI Futures contract, he has played an integral role in developing new instruments and methods for accessing and hedging various inflation exposures. In 2016, Mr. Ashton published What’s Wrong With Money? The Biggest Bubble of All. He is a graduate of Trinity University and lives in Morristown, New Jersey.

December all-items inflation increased 0.5%, slightly higher than expectations.

By David Enna, Tipswatch.com

This seemed impossible just 12 months ago, when U.S. inflation ran at 1.4% for 2020. But December’s price increases continued an ominous trend in 2021, with annual inflation ending the year at 7.0%, the highest rate in 40 years.

For December, the Consumer Price Index for All Urban Consumers increased 0.5% on a seasonally adjusted basis, the Bureau of Labor Statistics reported. That was slightly higher than the consensus estimate of 0.4%. Year-over-year inflation ran at 7.0%, the BLS said, slightly below the consensus.

This is the final inflation report of 2021, and the 7.0% increase for the year is the largest since 1981, when inflation ran at 8.9%. In the 40 years following 1981, end-of-the-year annual inflation has never exceeded 6.1%, until 2021.

Core inflation, which removes food and energy, rose 0.6% for December, following a 0.5% increase in November. Year-over-year core inflation was 5.5%, the highest annual increase since 1991. Inflation for both the month and the year were higher than expected.

Gasoline prices, usually a trigger for higher U.S. inflation, actually fell 0.5% in December, but are up 48.9% for the year. (Before seasonal adjustment, gasoline prices fell 2.2% in December.) When inflation rises without a boost from energy prices, you know it is surging across the economy. For example:

Food prices were up 0.5% for the month, and increased 6.3% for the year.

The index for fruits and vegetables increased rose 0.9% over the month.

On the other hand, the index for meats, poultry, fish, and eggs declined in December, falling 0.4% after rising at least 0.7% in each of the last seven months.

Shelter costs increased 0.4% for the month and 4.1% for the year.

Costs of used cars and trucks continued surging, rising 3.5% for the month and 37.3% for the year.

New vehicle prices rose 1.0% for the month and were up 11.8% for the year.

The apparel index rose 1.7% for the month, following a 1.3% increase in November.

To sum things up for 2021, The BLS stated:

“Major contributors to this increase include shelter (+4.1 percent) and used cars and trucks (+37.3 percent). However, the increase is broad-based, with virtually all component indexes showing increases over the past 12 months.”

Here is the U.S. inflation trend over the last year, showing the strong move higher for both all-items and core inflation since September:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For December, the BLS set the inflation index at 278.802, an increase of 0.31% over the November number.

Note that the non-seasonally adjusted increase of 0.31% lagged behind the adjusted inflation number of 0.5% for the month, most likely caused by the dip in gasoline prices, a decline of 2.1% before adjustment, but 0.5% after. These types of variations will balance out over a year.

For TIPS. The December inflation report means that principal balances for all TIPS will increase 0.31% in February, following a 0.49% increase in January. In February, balances for the year will be up 7.0%. Here are the new February Inflation Index Ratios for all TIPS.

For I Bonds. The December report is the third in a six-month series that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset May 2 based on inflation from September 2021 to March 2022. After three months, inflation has been running at 1.64%, which translates to an I Bond variable rate of 3.28%. Keep in mind that three months remain, and also that lagging non-seasonally adjusted inflation in November and December should reverse in coming months.

Here are the relevant numbers:

What this means for future interest rates

In congressional testimony this week, Federal Reserve Board Chairman Jerome Powell signaled strongly that the Fed is prepared to raise short-term interest rates in 2022, beginning as soon as March. It looks like three rate increases in 2022 are a sure thing, and if inflation continues at a high rate into the summer, four increases are likely. That would bring the Federal Funds Rate up to a range of 1.00% to 1.25% by the end of the year.

Today’s inflation report reinforces the need for Fed action. There were few surprises in this report, but it is clear that the inflationary surge is continuing. That could be a hard trend to break. The stock market is opening higher this morning, indicating that this report was “digestible,” at least.

Inflation is likely to continue at a very high rate at least through March, which more or less ensures that the Fed will need to make that initial rate hike. The markets seem prepared for it. It needs to happen.

Inflation guru Michael Ashton posted this today on his E-piphany site, which includes a ton of analysis of today’s report:

“The Fed is talking tough, but talk is cheap. They’re still easing at this hour! Eventually they’ll stop digging the hole. When will they start filling it in – not by raising rates which has small effect if any on inflation, but by selling bonds? Don’t hold your breath. …

“This was, sadly, not a very surprising report. Inflationary pressures remain broad and deep, and the Fed today is still purchasing bonds and adding more reserves to the system. … So now, they’re behind the curve and really need to catch up and get ahead of this process.”

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

In one week, real yields have increased as much as 30 basis points. Will this trend continue? Yes, if the Fed continues on its current course.

By David Enna, Tipswatch.com

In the last week, the U.S. bond market seems to have finally faced up to reality: There is no longer any reason for interest rates — both real and nominal — to continue at ridiculously low levels. This could either be the beginning of a months-long trend higher, or just another bond market head fake.

Several news events and trends have combined to bring us to this point, including continued very high U.S. inflation, research showing that the Omicron Covid variant is less lethal, and several positive jobs reports. But the key event seems to have been the release of the Dec. 14-15 minutes of the Federal Reserve’s Open Committee Meeting. This is how the Wall Street Journal summarized those minutes:

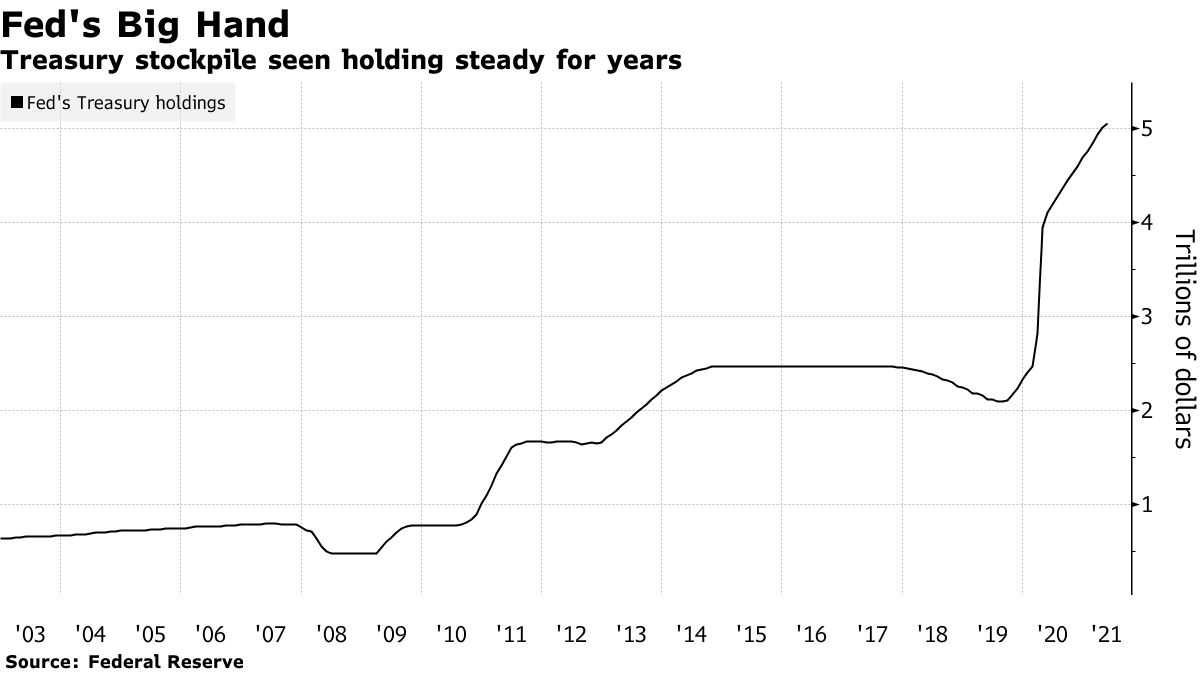

“Federal Reserve officials at their meeting last month eyed a faster timetable for raising interest rates this year, potentially as soon as in March, amid greater discomfort with high inflation. … Some officials also thought the Fed should start shrinking its $8.76 trillion portfolio of bonds and other assets relatively soon after beginning to raise rates, the minutes said.”

Obviously, inflation is a huge concern for the Fed, because in the opening months of 2022 it is now considering: 1) ending its quantitative easing bond-buying by March, 2) also in March, beginning to increase short-term interest rates, and 3) then quickly transitioning to reducing its massive balance sheet of Treasury holdings and mortgage-backed securities.

Nos. 1 and 2 mean the end of an accommodative Fed policy, and markets have been reacting to those expected (but accelerated) actions with a yawn. But No. 3 — reducing the Fed’s balance sheet — means actual tightening of the U.S. money supply, and the market wasn’t prepared to hear that.

This Bloomberg chart was from a May 20, 2021, article with the now-ironic headline “Don’t Fear the Taper: Fed to Dominate Treasury Market for Years.” The point of the article was that even after the Fed completes its tapering of bond buying, it would continue rolling over its massive holdings of Treasurys and continue surpressing longer-term interest rates.

In this chart, you can spot the last time the Fed began tapering an earlier quantitative easing, at the beginning of 2014. Note that the Fed’s balance sheet remained stable after the tapering for nearly four years. Actual reduction of the balance sheet began in 2018, and it wasn’t extreme, but it resulted in chaos in the bond and stock markets at the close of 2018, a year when the Fed also increased its federal funds rate four times. The S&P 500 fell nearly 15% from Dec. 1 to Dec. 24, 2018, and ended the month down nearly 10%.

So while Bloomberg was advising investors to not fear the Fed in May 2021, conditions are changing dramatically in 2022. And things could escalate this week with the release of the December 2021 inflation report, due out on Jan. 12 at 8:30 a.m. EST. Will the U.S. annual inflation rate rise to exceed 7.0%? It’s possible. (The consensus estimate is 7.1%, but these estimates have been very unreliable over the last 12 months.)

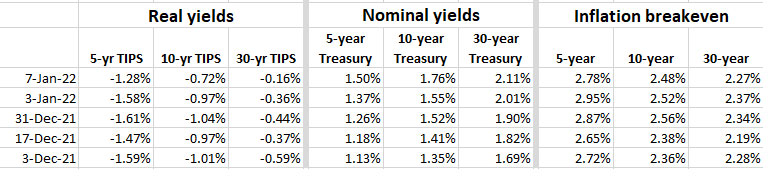

Here is how real and nominal interest rates have reacted over the last month:

Note that the real yield (meaning the yield compared to inflation) of a 5-year TIPS increased 30 basis points in a single week and the real yield of a 30-year TIPS could soon break through the zero barrier for the first time since May 2021. The real yield of a 10-year TIPS rose 25 basis points last week. These are significant moves higher.

But also notice that inflation breakeven rates have held fairly stable. The market is now pricing in future Fed actions to tamp down inflation, with a view that future inflation will average around 2.5% over the next decade.

What this means for TIPS and I Bonds

As real and nominal yields rise, you can expect the values of funds investing in TIPS and Treasurys to take a hit. Here are year-to-date total returns for three key funds (and realize that the year is only 5 market days old at this point):

Vanguard Total Bond Market ETF (BND): Total return of -1.40%.

Schwab’s U.S. TIPS ETF (SCHP): Total return of -2.23%.

Vanguard’s Short-Term TIPS (VTIP): Total return of -0.66%.

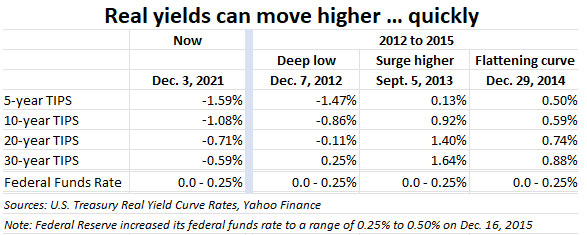

It looks likely that the 30-year TIPS real yield will rise above zero relatively soon, and that is also possible for the 5- and 10-year TIPS, but most likely much later in the year, if at all. Then again, look at the rate history of 2013, when real and nominal yields rose dramatically, even though the Fed took no actions that year except to say it planned to taper quantitative easing:

I created this chart for an article last month, speculating on the possibility of 10-year real yields rising above zero, which could cause the Treasury to increase the I Bond’s fixed rate at the May or November resets. I think that looks unlikely for May, but is a possibility in November, depending on how things play out.

If inflation eases, the pressure will be off the Fed to reduce its Treasury horde, and real yields could continue below zero for much of the year. However, if the Fed does increase its federal funds rate four times in 2022, I think it is likely that the 5-year TIPS yield could rise above zero.

If the 10-year nominal Treasury rises to a level near 2.50% (still relatively low by historic standards), the real yield of a 10-year TIPS should rise to close to zero, or above. Anything much higher and you could see the I Bond’s fixed rate rise, at some point in the future.

However, keep in mind that if the real yields of TIPS rise above zero, and the I Bond’s fixed rate remains at zero, then TIPS will again, finally, be a very competitive investment.

At any rate, my personal plan is to buy my I Bond 2022 allocation this month, to capture the current 7.12% variable rate for six months, and then the next rate, also likely to remain high, for another six months. That’s what I recommend, but many people will disagree, hoping for a higher fixed rate. I don’t think that will happen in May, at least. November could be interesting.

For TIPS investors looking to build out ladders into the future, an increase in real yields will make TIPS much more attractive. If you want to be a net buyer of TIPS, you want real yields to increase.

The Fed can change course

If the stock and bond markets take a frightening turn downward, expect the Fed to back off on a 4th interest rate increase this year, and a reduction in its Treasury balance sheet could be put off for months, maybe years. But the bond buying will end, either way. And short-term interest rates will go higher, either way.

The key will be the rate of U.S. inflation over coming months. It looks likely that high inflation will continue through March at least, before easing off to something closer to 4% for the rest of 2022. But inflation is impossible to predict. The Fed brought us this current surge in inflation. Will it have the courage to bring it under control?

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

My usual beginning-of-the-year buying guide for U.S. Series I Savings Bonds has a lot of qualifications and “what ifs,” making this a complicated and much-debated decision. Is the I Bond’s fixed rate likely to rise during the year? Should I space my purchases out over the year? Will the inflation-adjusted variable rate rise dramatically at the resets in May and November?

I Bonds are issued by and guaranteed by the U.S. Treasury

I’m telling you: All of that really doesn’t matter in 2022. It looks like the wise course will be to buy I Bonds anytime from January to April, but before the May 1 rate reset. Before we get into why, here’s a quick primer for investors who are new to I Bonds:

An I Bond is a U.S. government security that earns interest based on combining a fixed rate and an inflation-adjusted rate.

The fixed rate will never change. Purchases through April 30, 2022, will have a fixed rate of 0.0%, which means they will simply track official U.S. inflation over time.

The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 7.12%, annualized, for six months. It will adjust again on May 1, 2022, for all I Bonds, no matter when they were purchased. (However, the effective start date of the new interest rate will vary depending on the month you bought the I Bond.)

Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also the option to get $5,000 a year in paper I Bonds in lieu of a federal tax refund. The purchase limit is the reason people ponder timing their I Bond purchases; once you hit $10,000 per person per year, you can’t purchase more, at least in the traditional way.

The value of building and holding a stockpile of I Bonds was demonstrated in 2021, with inflation surging to an annual rate of 6.8% in November. As U.S. inflation rises, the return on I Bonds increases, and the money compounds tax deferred until you redeem the I Bonds. For more detailed information, read my Q&A on I Bonds and the I Bond Manifesto.

The case for buying in January

I Bonds purchased through April 2022 will earn 7.12% interest, annualized, for a full six months. That is an exceptionally high return, and blows away other safe alternatives. With a $10,000 investment:

I Bond: You will earn $356 in 6 months.

1 year Treasury: You will earn $40 in 1 year.

1 year bank CD: You will earn $65 in 1 year.

2 year Treasury: You will earn $156 in 2 years.

3 year Treasury: You will earn $312 in 3 years.

A lot of people are looking at that 7.12% six-month return and deciding to invest in I Bonds for the short-term, planning to redeem after the one-year holding period. (I recommend hanging on to I Bonds for the long term, but I understand the strategy in this low-interest-rate environment.)

Short-term investment? One quirk of U.S. Savings Bonds is that if you purchase near the end of a month, you get credit for a full month of interest and ownership. So for a person viewing I Bonds as a short-term investment, placing an order at TreasuryDirect to buy on Jan. 26 or 27 makes sense. That starts the clock ticking on the one-year holding period. You will be able to redeem in early January 2023, but you will lose the last three months of interest. Still, you will earn at least $356 interest (probably more) even with the three-month interest penalty. A couple could double up on that purchase.

Long-term investment? Long-term holders of I Bonds are my favorite people, and my recommendation for them is to buy up to the full purchase cap anytime between January and April. Got the money available now? Do it in January. Need time to raise the money? Get it done before April. Any purchase of I Bonds through April will earn the 7.12% annualized rate for a full six months.

So … Buy before May. It is that simple. But you didn’t think I’d leave it at that did you?

What if the I Bond’s fixed rate increases in 2022?

I wrote an article recently speculating on the slight possibility that the I Bond’s fixed rate could rise in 2022. My conclusion was that it could happen, but it would require a massive increase in real interest rates. For example, the 10-year TIPS now has a real yield of -0.97%. That yield would need to rise 125 basis points, or more, for the Treasury to even consider raising the I Bond’s fixed rate, especially when the variable rate is already so attractive.

So, would it make sense to hold off on purchases in 2022 to see if the fixed rate rises? Nope.

Yes, I know, a higher fixed rate is always preferable. That’s the first rule of I Bond investing, since the fixed rate stays with that I Bond for the entire 30-year term, while the variable component changes every six months. But in this case, waiting beyond May 1 means missing out on a massively attractive 7.12% annualized rate for six months. That’s $356 interest in six months, equivalent to more than a decade of interest from a fixed rate of 0.2%. And that $356 initial interest will give your investment a nice boost to future returns, because it will grow with future inflation.

Sorry, but here comes a huge 19-year chart, showing how semi-annual interest earned on an I Bond purchased before May 1 will compare to a purchase after May 1 with a fixed rate of 0.2% (which is very unlikely). This chart assumes that the inflation-adjusted variable rate will remain high at the May 1 reset, and then gradually begin tapering down to an annual inflation rate of 2.2%.

This is a corrected version of a chart originally published with this story.

The key takeaway from this chart is that buying I Bonds before May 1 gives your investment a $356 head start, and that head start will continue to grow with inflation over 30 years. So even though the semi-annual accrued interest would be higher with the 0.2% fixed rate, it would take until year 13 for the 0.2% fixed rate (which is highly unlikely, remember) to catch up to the I Bond purchased before May. And if the fixed rate stays at 0.0% in May (much more likely), the investment would trail the return of the pre-May I Bond through the entire 30 years.

Is it reasonable to wait until April to see if the fixed rate is likely to rise in May? Sure, and it does no harm to your investment. But it’s still highly likely that investors will want to buy before May. Even if the fixed rate does rise in May, the investment return will lag the before-May purchase for 13 years.

But one final point, which I often say: “The Treasury does weird things.” We’ll see.

Key dates for the curious

Both the I Bond’s inflation-adjusted variable rate and the fixed rate will be reset on May 1 (actually May 2 since the 1st is a Sunday) and November 1. Investors will know the new variable rate a couple of weeks before the official reset, because it is based on six-month inflation rates.

At 8:30 a.m. EDT on April 12, 2022, the Bureau of Labor Statistics will release the March inflation report, which will set in stone the I Bond’s new inflation-adjusted variable rate, based on non-seasonally adjusted inflation from September 2021 to March 2022.

So an investor who opts to wait will have from April 12 to April 28 (a Thursday) to decide on buying before May 1, or after. But remember, the only way the I Bond’s fixed rate will rise above zero is if 10-year real yields rise about 125 basis points in the next four months.

At 8:30 a.m. EDT on Oct. 13, 2022, the BLS will release the September inflation report, which will set the I Bond’s next inflation-adjusted interest rate, based on inflation from March to September 2022.

At about 10 am. EDT on May 2 and November 1, the Treasury will announce the new fixed rate for I Bonds, which seems very likely to remain at 0.0% on May 1 but is more of an open question for November 1. However, if the fixed rate rises in November, investors who capped out purchases earlier in 2022 will have a chance to get the higher fixed rate in January 2023.

Conclusion

People looking at I Bonds as a short-term investment should purchase near the end of January to get the clock started on the one-year holding period. By purchasing near the end of the month, and redeeming near the beginning of January 2023, the holding period can be cut to 11 months and a few days. This strategy is guaranteed to return at least $356 on a $10,000 investment, even with the three-month interest penalty.

Once the year is up, investors would have to look at then-current inflation-adjusted variable rate. If it is high — anywhere above 4% — they will probably want to hold off on redeeming in January to avoid a three-month penalty on an attractive interest rate.

People looking at I Bonds as a long-term investment should plan on completing their purchases — up the full cap of $10,000 per person per year — anytime before May 1. Investors who like to be strategic can wait until mid-April to make the purchase, but most likely, they will want to buy before May 1.

My personal decision: I have placed an order to buy my full allocation on Jan. 26.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

TIPS remained rather unappealing the entire year, while I Bonds became a superstar investment.

By David Enna, Tipswatch.com

Here is how I can sum up this monumental year of change:

January 2021: “Inflation will never be a problem again.”

December 2021: “We are heading toward inflation Armageddon!“

In January 2021, U.S. inflation was running at an annual rate of 1.4%, continuing an 11-month string with annual inflation under 2.0%. But 11 months later, by November 2021, annual inflation had soared to 6.8%, the highest rate in 39 years. And it shows no sign of waning anytime soon. Here is the trend in annual inflation over the last year:

And yet, even with that shocking surge in inflation, U.S. interest rates continue at extremely low levels. Here are some key data points from 2021:

The 4-week Treasury began the year yielding 0.09% and is now at 0.01%.

The 30-year Treasury began the year at 1.66% and is now at 1.96%.

The real yield (meaning the yield above inflation) of a 5-year Treasury Inflation-Protected Security started the year at -1.62% and is now at -1.54%.

The real yield of a 10-year TIPS started the year at -1.08% and is now at -0.98%.

The real yield of a 30-year TIPS started the year at -0.39% and is now at -0.38%.

The SPY ETF (S&P 500) has had a total return of 29.4% year to date.

VTIP, Vanguard’s short-term TIPS ETF, has had a total return of 5.25% year to date.

SCHP, Schwab’s total TIPS fund, has had a total return of 5.48% year to date.

And finally, the 10-year inflation breakeven rate started the year at 2.01% and is now at 2.53%. In other words, investors now sense that inflation might be 52 basis points higher over the next 10 years, even though inflation has soared 540 basis points this year to a 39-year high.

Sometimes I wonder: Am I living in an alternate universe? At some point, and soon: 1) inflation will have to plummet or 2) interest rates will have to rise, dramatically. But for now, all we can do is look back on an eventful year for inflation, and an uneventful year for interest rates.

Recapping a year of TIPS auctions

CUSIP 91282CBF7, 10-year TIPS

Original auction, Jan. 21, 2021: Investors got a real yield to maturity of -0.987%, which at the time was the lowest ever for any auction of this term. The inflation breakeven rate was 2.09%, which was the highest for any auction of this term since September 2018. (Just 11 months later, that 2.09% breakeven rate looks almost nostalgic.)

Reopening auction, March 18, 2021: Investors got a much more “attractive” real yield of -0.580%, 38 basis points higher than the originating auction two months earlier. The inflation breakeven rate rose to 2.31%.

Reopening auction, May 20, 2021: The real yield came in at -0.805%, a bit higher than the record low. The inflation breakeven rate continued rising to 2.44%.

CUSIP 912810SV1, 30-year TIPS

Original auction, Feb. 18, 2021: This new 30-year TIPS auctioned with a real yield to maturity just slightly negative to inflation, at -0.04%, to fairly weak investor demand. The coupon rate of 0.125% became the record low for any 30-year TIPS auction in history. The inflation breakeven rate was 2.11%. All in all, this ended up being a fairly attractive auction, especially for TIPS traders.

Reopening auction, Aug. 19, 2021: Six months later, this TIPS reopened with a real yield to maturity of -0.292%, the lowest ever for any TIPS auction of this term. The adjusted price was a hefty $117.72 for about $104.33 of value, after accrued inflation was added in. The inflation breakeven rate was 2.17%, slightly higher than at the originating auction.

CUSIP 91282CCA7, 5-year TIPS

Original auction, April 22, 2021: The Treasury’s offering of $18 billion in a new 5-year TIPS generated a real yield to maturity of -1.631%, which at the time was the lowest real yield at auction for any TIPS in history. The inflation breakeven rate was 2.45%.

Reopening auction, June 17, 2021: This was one of the most interesting auctions of the year, and the only TIPS I actually bought in 2021. (It was a small purchase to test a new brokerage account.) This time, the real yield to maturity rose to -1.416%, boosted by the Federal Reserve’s announcement the day before that it was opening the door to tapering its aggressive bond-buying program. The real yield for this TIPS jumped by 31 basis points in a single day. The inflation breakeven rate dipped to 2.30% based on the Fed’s supposed future actions to calm inflation.

CUSIP 91282CCM1, 10-year TIPS

Original auction, July 23, 2021: There had been 110 TIPS auctions of this 9- to 10-year term since 1997 and this auction’s real yield to maturity of -1.016% set the record low yield, by a large margin. But that record wouldn’t last long. The inflation breakeven rate was 2.27%, which seems surprisingly low.

Reopening auction, Sept, 23, 2021: The real yield at this auction bounced higher, to -0.939%, again spurred by Fed statements the day before indicating actions to slow its bond-buying program. The inflation breakeven rate was 2.34%.

Reopening auction, Nov. 18, 2021: This is where things start to get weird. In November 2021, the Federal Reserve actually began tapering its bond-buying and made clear that interest-rate increases could be coming much sooner than the market expected. The market reacted with a yawn and bid the real yield to maturity of this TIPS down to -1.145%, the lowest ever for any TIPS auction of this term. The inflation breakeven rate soared to 2.74%.

91282CDC2, 5-year TIPS

Original auction, Oct. 21, 2021: Another TIPS auction, another record low yield. The Treasury’s offering of $19 billion in a new 5-year TIPS generated a real yield to maturity of -1.685%, which still stands as the lowest ever recorded for any TIPS auction of any term. The 5-year inflation breakeven rate came in at 2.89%, by far the highest rate for any 5-year TIPS auction in more than a decade. The 5-year breakeven rate was last at this level in March 2005.

Reopening auction, Dec. 22, 2021: The last TIPS auction of the year generated a real yield to maturity of -1.508% and an inflation breakeven rate of 2.73%, down from the October number.

All eyes on I Bonds

Although the fixed rate for U.S. Series I Savings Bonds stayed steady at 0.0% through 2021, the dramatic surge in U.S. inflation created intense interest in I Bonds as the inflation-adjusted variable rate jumped higher in May, and then even higher in November.

To start the year, through April 2021, I Bonds had a rather mundane six-month inflation-adjusted rate of 1.68%, but that jumped to a much more attractive 3.54% on May 1 and then to the wow-factor rate of 7.12% on November 1. The reason? U.S. inflation rose 3.56% in the six months from March to September 2021, the highest six-month increase in the 23-year history of I Bonds.

Here are the inflation numbers the Treasury uses to determine the variable rate:

Note that just two months into the next six-month rate setting period, U.S. inflation has been running at 1.33%, which would translate into an annualized six-month variable rate of 2.66%. I Bonds are likely to continue to be a very safe, very attractive investment well into 2022.

TIPS, however, remain rather unattractive, with real yields well below zero. Will 2022 bring dramatically higher real yields? I doubt those will come quickly, but once the market shifts momentum, we could see higher yields, especially for the 5-year TIPS.

At this point, I Bonds remain the most attractive inflation-protected investment in the world. As long as real yields remain depressed, your first $10,000 invested in inflation protection should be allocated to I Bonds. Then consider TIPS.

Happy New Year, everyone.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I'm already familiar with the product and was curious if Tipswatch had ever done any rate predictions for it, like…