By David Enna, Tipswatch.com

U.S. Series I Savings Bonds are one of the nation’s most talked-about investments of 2021, especially now that their inflation-adjusted interest rate has surged to 7.12% at the November 1 reset. Glowing articles have been popping up in Barron’s, Bloomberg, the Wall Street Journal, CNBC, USA Today, and on and on.

And now, as the year draws to a close, there is a possibility to lock down — in a two-week period — $20,000 in I Bonds (or $40,000 for a couple) and get 7.12% annualized for a full six months on the entire investment. The Treasury sets a $10,000 per person per calendar year limit on I Bond purchases, but the 2021 purchase cap ends on Dec. 31 and the 2022 cap launches on Jan. 1.

So here you go, a chance to double up on a very attractive interest rate. But you will need to act fast.

What is an I Bond?

If you are totally new to I Bonds, you can read my “Q&A on I Bonds,” which covers all of the pluses and minuses of this investment. But briefly … An I Bond is a U.S. government security that earns interest based on combining a fixed rate and an inflation-adjusted rate.

- The fixed rate will never change. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through April 30, 2022, will have a fixed rate of 0.0%, which means they will simply track official U.S. inflation over time.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 7.12%, annualized, for six months. It will adjust again on May 1, 2022, for all I Bonds, no matter when they were purchased. (However, the effective start date of the new interest rate will vary depending on the month you bought the I Bond.)

I Bonds are the most conservative and most safe of all investments. Your principal is 99.9999999% safe and it will never decline, ever. If inflation falls to below zero, the inflation-adjusted rate will fall to zero, but not below zero.

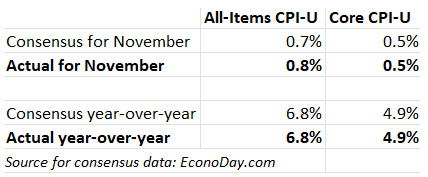

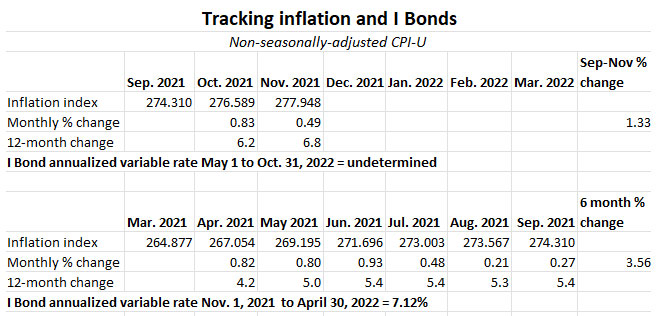

The value of building and holding a stockpile of I Bonds has been demonstrated in 2021, with inflation surging to an annual rate of 6.8% in November. As U.S. inflation rises, the return on I Bonds increases, and the money compounds tax deferred until you redeem the I Bonds.

The purchase limit

Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also the option to get $5,000 a year in paper I Bonds in lieu of a federal tax refund. Some investors find this amount too small to make a difference in their asset allocation. However, an investor using multi-year purchases can build a substantial stake in I Bonds.

And that’s why this last week in December is so important. This week, you can lock down $10,000 with a 7.12% return for the first six months and then next week, do it again. That is a total of $20,000 for a single person, and $40,000 for a couple. For most people, that is a significant investment, especially for use as part of an emergency fund.

After six months for each investment, on June 1 for the I Bonds bought in December and July 1 for the I Bonds bought in January, the inflation-adjusted variable rate will be reset. It’s impossible to say what that new rate will be, but I think it’s likely to be in a range of anywhere from 4% to 7% … also very attractive.

I Bonds have to be held a year before they can be redeemed and there is a penalty of the last three months of interest for I Bonds held less than 5 years. But even with that penalty, any purchase of I Bonds in December and January will be guaranteed to return at least 3.56% over one year. Compare that to an insured bank CD paying 0.60%, or the 1-year Treasury paying 0.33%. It’s no wonder I Bonds are a very popular investment at the moment.

Want to do this? Get started TODAY

To buy I Bonds, you need to have an account at TreasuryDirect. If you already have an account, no problem. Just log in and make the purchase. But if you don’t have an account, time is running out. You need to place your I Bond order today, Dec. 28 (preferably) or tomorrow (last shot), to ensure that your purchase will be registered in December 2021. A purchase made Thursday might be OK, but it’s getting risky.

A lot of readers don’t like TreasuryDirect, which can be a bit clunky. But the process of buying and redeeming I Bonds at TreasuryDirect works well. First you need to open an account, and I wrote a guide to walk you through the basics: Ready to open a TreasuryDirect account? Here are some tips.

When you set up the account, you will be linking a bank or brokerage account to TreasuryDirect. Then to buy I Bonds, you simply log into TreasuryDirect, set the purchase amount and date, and the purchase will be made. You can purchase I Bonds near the end of a month and get credit for a full month of interest. TreasuryDirect makes timing the purchase easy.

Couples need two separate TreasuryDirect accounts, so allow time for that if you are using this strategy.

Then … buy in January? Or later?

I’ll be writing a guide to I Bond purchases in 2022 next month, but right now I am thinking that a purchase in January will be fine. In reality purchasing any time through April 30, 2022, will ensure six months of the 7.12% rate. So there won’t be a similar rush to buy in January.

But if the idea of a “double dip” purchase of I Bonds appeals to you — along with a super-attractive interest rate over the next year — you need to get the 2021 purchase done … RIGHT NOW.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I'm already familiar with the product and was curious if Tipswatch had ever done any rate predictions for it, like…