By David Enna, Tipswatch.com

With all the attention being drawn to U.S. Series I Savings Bonds these days, the Treasury’s other inflation-protected investment, the Treasury Inflation-Protected Security, seems to be flying under the radar. And that’s probably right. For a small-scale investor, in October 2021, an I Bond makes a heck of a lot more sense than a comparable TIPS.

Because an I Bond can be redeemed after five years with no penalty, it is directly comparable to a 5-year TIPS. An I Bond offers a real return that will match official U.S. inflation over five years. A 5-year TIPS currently has a real yield of about -1.58%, meaning it will under-perform official inflation (and the I Bond) by 158 basis points. The clear winner is the I Bond.

At auction this Thursday, the Treasury will offer $19 billion in a new 5-year TIPS, CUSIP 91282CDC2. It can’t compare with its little brother — the I Bond — but is it an attractive option for investors seeking inflation protection after reaching the I Bond’s $10,000 per person per year purchase cap? Let’s take a look.

A 5-year TIPS has two advantages over an I Bond: 1) there isn’t a purchase cap, and 2) a TIPS can be purchased in a tax-deferred account, allowing an investor to use tax-deferred money to make the purchase. (Although an I Bond is a tax-deferred investment, it can’t be purchased inside a tax-deferred account.) Keeping the transaction inside a tax-deferred account means no immediate tax liability caused by raising money for the purchase.

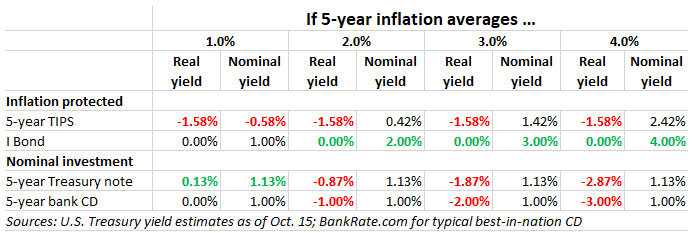

As I noted above, the U.S. Treasury on Friday estimated a full-term 5-year TIPS would have a real yield of -1.58%. While that sounds miserable, it is in line with other high-safety nominal investments, for example the 5-year Treasury note or an insured 5-year bank CD. Here’s a comparison, showing how a 5-year TIPS will under-perform a nominal Treasury under low inflation scenarios, but easily out-perform the Treasury note if inflation averages 3.0% to 4.0% or higher in the next five years:

This chart shows the clear superiority of the Series I Savings Bond, which will out-perform the other safe investments under any inflation scenario higher than 1%. The I Bond is the only truly attractive investment on the chart. But once inflation rises above 2.5%, the 5-year TIPS begins to out-perform the nominal investments. If you believe inflation is likely to run higher than 3.0% over the next five years, the TIPS is the better investment — versus a nominal Treasury or bank CD.

Here is the trend in 5-year real yields over the last three years, showing the deep dive into negative yields after the Federal Reserve began aggressive bond-buying in March 2020. Next month, in November, the Fed intends to begin tapering away from that bond buying, a many-months process that should cause real yields to climb. But so far, the 5-year real yield has stabilized in a range of about -1.50% to -1.60%.

Thursday’s auction results will set the real yield to maturity for CUSIP 91282CDC2, and its coupon rate will be set at 0.125%, the lowest the Treasury will go for a TIPS. That means investors will be paying a hefty premium for the coupon rate, probably somewhere around $108.25 for $100 of par value, assuming the auctioned real yield comes in at about -1.58%.

In addition, this TIPS will have an inflation index of 1.00093 on the settlement date of Oct. 29, which will push the adjusted price up slightly, but investors will receive a matching amount of accrued principal.

Inflation breakeven rate

With a nominal 5-year Treasury note trading at 1.13%, this new TIPS would have a 5-year inflation breakeven rate of 2.71%, which seems like a reasonable estimate of U.S. inflation in the near-term future. Inflation is currently running at an annual rate of 5.4%, but inflation over the last 5 years has averaged only 1.9%. Investors see inflation trending higher than recent trends, and that looks like a reasonable assumption.

However, a caution: 2.71% is exceptionally high by historic standards. The Treasury provides 5-year inflation breakeven data back to 2003, and you have to go back to May 2006 to see inflation expectations that high. A high inflation breakeven rate makes a TIPS “pricey” versus a nominal Treasury. But will investors care when U.S. inflation is running at a decades-high level of 5.4%?

Here is that big-picture trend in the 5-year inflation breakeven rate, dating back to 2003. During much of the time since the 2008 recession, this rate has lingered at or below 2.0%:

Inflation is currently running at the highest level in 31 years, with 5.4% annual inflation recorded in September, the highest September-to-September rate since 6.2% in 1990. After that peak in 1990, inflation continue to run at or above 2.5% for the next six years. Conclusion: An inflation breakeven rate of 2.7% looks reasonable.

Thoughts on this auction

It’s not attractive, but the real yield doesn’t look likely to set a record low, which was -1.631% for a new 5-year TIPS auctioned on April 15, 2021. With the Fed launching its tapering efforts in a month (or so they say) real yields should begin inching higher. Are more attractive auctions ahead?

One risk-reduction strategy I have been considering: If you own a broad-based TIPS fund (such as TIP or SCHP) in a tax-deferred account, you could sell a small portion and invest it gradually into 5-year TIPS auctions. That way you will be lowering your duration risk and know that in 5 years (or less for reopenings) you will get your money back. But remember that any premium price over par is not guaranteed to be returned at maturity. This strategy retains inflation protection with a little less risk. Just a thought. Let me know if you see flaws.

CUSIP 91282CDC2 will get a reopening auction on Dec. 16. Will the Fed’s actions in the next two months make that future auction more attractive? Could be.

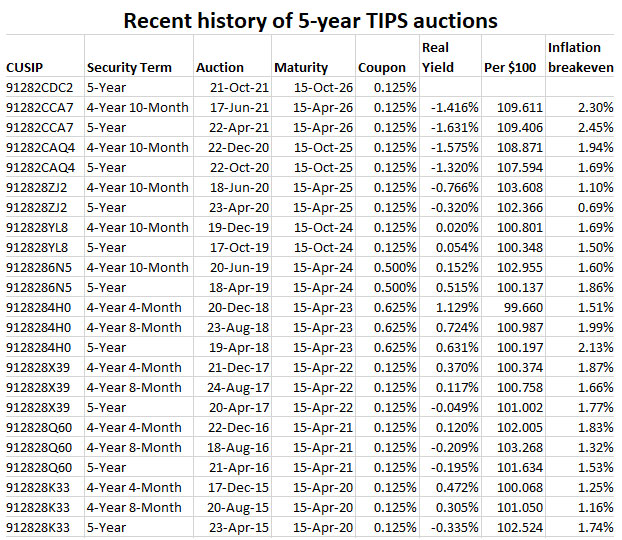

I will be reporting the auction results soon after the close at 1 p.m. Thursday. Non-competitive bids have to be placed by noon. Here’s a listing of recent TIPS auctions of this term, showing the six consecutive auctions with negative real yields, starting in April 2020, as the Fed began aggressively buying Treasurys.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hello, I purchased TIPS: 91282CDC2 on the day it was issued on 10/15/2026 (settlement 10/21/21). Looks like I paid a hefty premium of 1.0951. I will be paid 1/8% interest but lets say inflation stays zero till maturity will I ever recover the premium I paid on maturity?

Thank you

In theory, if inflation stayed at zero throughout the five years, you would get back only the par value, not the premium you paid (plus 0.125% paid out as current interest per year). So if you bought $10,000 of this TIPS and paid about $10,951 for it, only the $10,000 is guaranteed to be returned at maturity. At this point, that TIPS has an inflation index of 1.019, meaning the $10,000 is now worth $10,190 in accrued principal. Its market value is now about $10,823, less than you paid because real yields have declined.

On the positive side, you will be getting a 0.84% boost in March based on January inflation.

Hello I just listened to your podcast about i bonds and have purchased a few whenever my ee bonds mature. What would your thoughts be on cashing low yielding ee bonds early to purchase an i bond? I enjoyed your podcast and also would like to mention I find treasury direct user friendly after using it a few times . Than you for your response.

Judy K

Hi Judy, if you are well into the 20-year holding period for EE Bonds — like close to 10 years in or more — I’d definitely keep the EE Bonds, which will double in value in 20 years. Since you mentioned you have EE Bonds that are now maturing, they could be paying 4% a year right now, until maturity. Keep those! If you recently purchased EE Bonds, they are probably paying a fixed rate of 0.1% and you could redeem them with very little tax consequence. I am a fan of EE Bonds for anyone who feels comfortable they can hold them for 20 years.

Thanks for the pertinent analysis as always David. Wish I could argue a point here but I can’t, in agreement.