This article is the second in a series looking at how my three favorite bond funds — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed after 2013, when the Fed signaled it would back off on bond purchases and eventually raise short-term interest rates.

Why do this? Because we may be heading into a similar scenario in 2022 and beyond, with the Fed tapering off bond purchases and eventually (and gradually) raising short-term interest rates. The performance after 2013 could tell us a lot about what’s ahead.

None of this happened in 2013, but the Federal Reserve issued enough signals that the bond market reacted with a “taper tantrum,” sending both real and nominal yields sharply higher. Read about what happened in 2013 here.

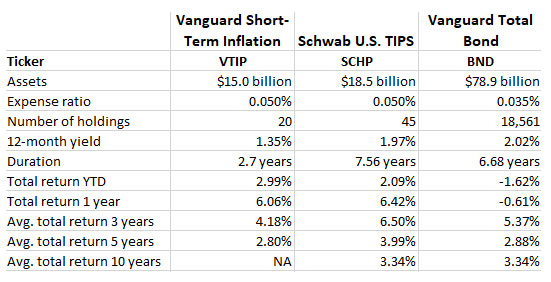

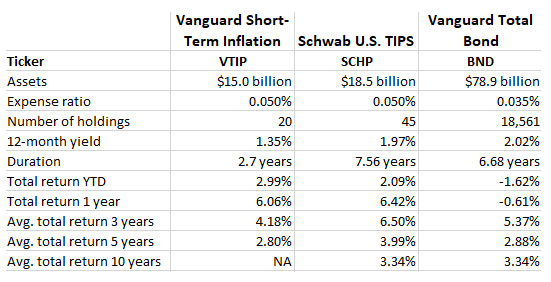

To recap, here are the three bond funds I am tracking; they are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a summary of their basic statistics and performance:

2014: The deck was stacked against TIPS funds

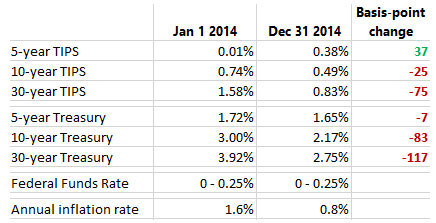

Even though real and nominal interest rates declined in 2014 — reversing the overreaction of 2013 — this wasn’t a good year for TIPS and TIPS funds. Why? Because the yield curve began flattening (with shorter-term yields rising and longer-term yields falling) and inflation slumped to 0.8% year-over-year. Here are the 2014 statistics:

Again, note that the Federal Reserve did not raise interest rates in 2014. But it did taper away from its bond purchases, gradually tightening the money supply. This raised recessionary fears, and longer-term interest rates declined. But there was one exception: Real yields rose for shorter-term TIPS, in reaction to short-term deflationary fears. The annual inflation rate came in at 0.8%, so those fears were justified. TIPS perform best when interest rates decline or stay stable, and inflation rises. The opposite was happening in 2014. The overall TIPS market is heavily skewed toward the shorter-term, with about 20 of 44 total issues maturing in the next five years. This yield flattening trend was not good for a short-term TIPS fund like VTIP, or even a broad-based TIPS fund like SCHP.

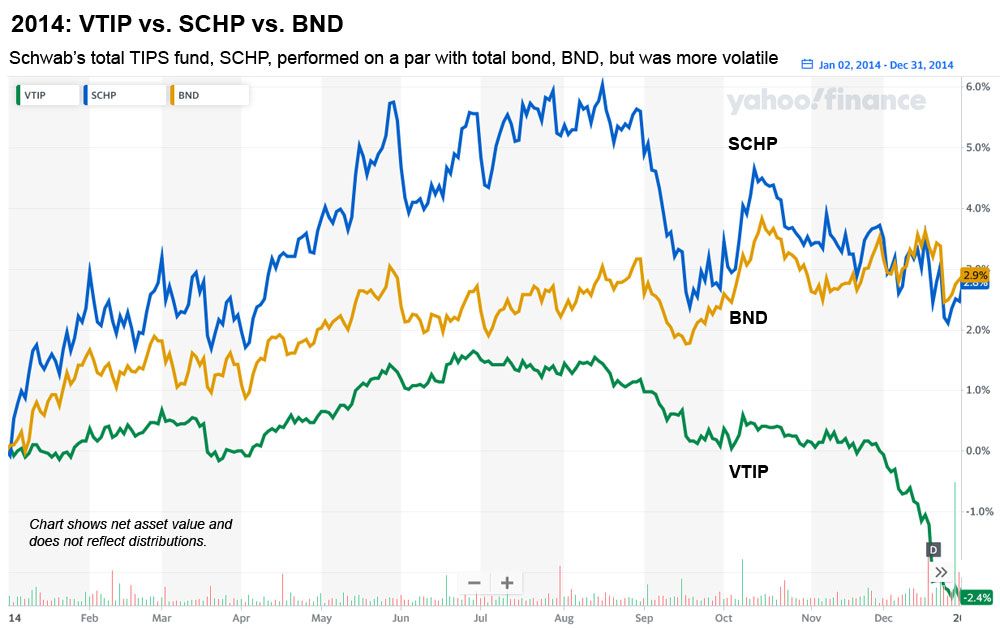

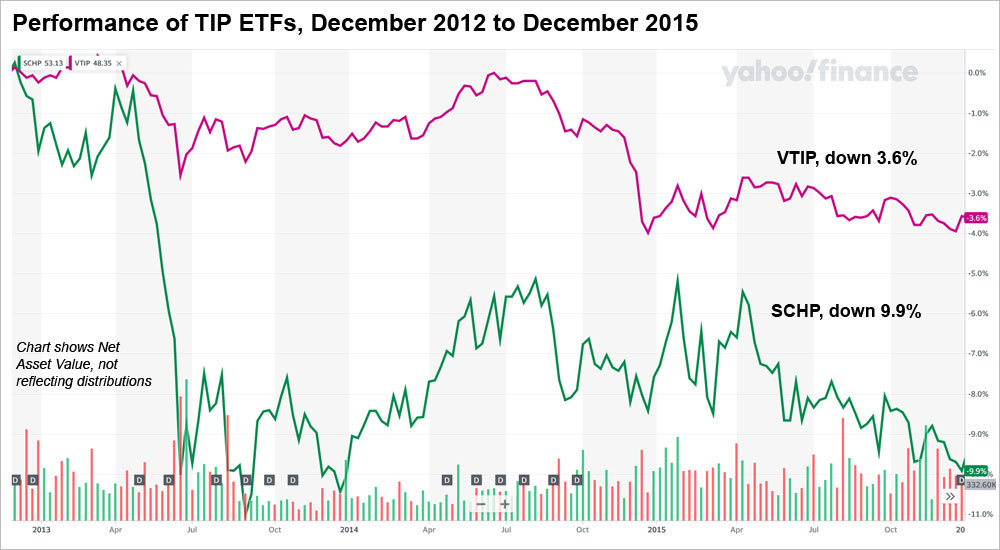

Here is how these funds performed in 2014, with the chart showing changes in net asset value and not reflecting distributions:

The TIPS market took a deep dive beginning in September 2014, an issue I addressed back then in this article. The trigger was the Sept. 17 release of minutes from a July Federal Reserve meeting. In those minutes, the Fed said:

In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions since the inception of the current asset purchase program, the Committee decided to make a further measured reduction in the pace of its asset purchases. …

If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will end its current program of asset purchases at its next meeting.

The Fed, in essence, said it was preparing to end its asset purchases within a few months. Purchases were eventually halted two months later, in October. But the Fed did not change its policy on near-zero short-term interest rates. The first rate increase didn’t come until Dec. 16, 2015.

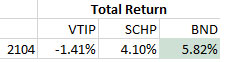

Those Fed meeting minutes halted the rally in longer-term TIPS, and sent shorter-term TIPS yields higher. For the year, VTIP was the worst-performing fund of the three, hit by a combination of higher real yields and very low inflation. BND’s total return out-performed SCHP’s, mainly because the inflation gains for TIPS were too weak to match the higher nominal yields of the overall bond market.

BND was the winner in 2014. SCHP took a volatile course toward a fairly good year. VTIP was the loser.

Conclusion

It’s highly likely that after the Fed acts to halt bond purchases and — eventually — raise short-term interest rates, we will see the yield curve flattening, which will benefit longer-term issues. VTIP could do fine in that scenario, as long as U.S. inflation remains rather high. SCHP would do even better, most likely.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Let’s take a deep-dive look at my three favorite bond funds: VTIP, SCHP and BND

By David Enna, Tipswatch.com

A couple weeks ago I wrote an article on the possible path of TIPS and TIPS funds as the Federal Reserve begins considering, then eventually implementing, a tapering of its $120 billion a month in bond purchases, followed by gradual increases in short-term interest rates.

You can read that here: When the Fed begins tapering, what will happen to TIPS? So far, the Fed’s “talking about talking about” statement has had only a minimal effect on the TIPS market. It triggered a nice result for the June 17 reopening auction of a five-year TIPS, which produced a real yield to maturity of -1.416%. The yield on that TIPS has now fallen to -1.70%, so in reality, the bond market is reacting to the Fed’s statements with a yawn.

But I still believe that unless the pandemic strikes again with a vengeance, the U.S. economy will continue to improve and the Fed will have to carry through with tapering of its bond purchases and eventually — maybe 18 months from now — will begin increasing short-term interest rates. U.S. inflation will be a key factor. If it continues to run anywhere near the current rate of 5.0% later in the year, the Fed will have to speed up the process.

And that means the bond market patterns of 2013 to 2016 and beyond could be duplicated as the Fed unwinds its easy money policy. I thought it would be worth taking a year-by-year look at how my three favorite bond ETFs — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed over the last decade.

These are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a recap of their basic statistics and performance:

Note that the Total Bond Fund is much more diversified than the TIPS funds, which are focused on a single, esoteric type of Treasury investment. For that reason, I consider it a better “core” bond fund. The Schwab TIPS fund has the longest duration, and is therefore going to be the most volatile in times of interest rate shifts. VTIP lessens that risk (and potential gain) by focusing on TIPS maturing in 0 to 5 years. It launched in mid-2012 and therefore does not yet have a 10-year average return.

I’ll be posting an article a day in the coming week focusing on each year, 2013 to 2021. Today we’ll start with 2013, an epic year in recent bond-fund history.

2013: A year of surging real and nominal yields

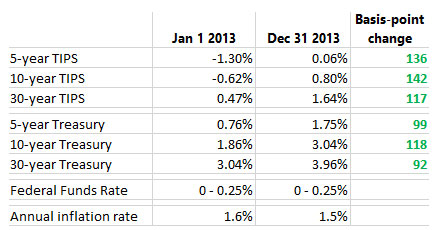

The year 2013 was crucial in the unwinding of the Federal Reserve’s earlier-era quantitative easing efforts. In June 2013, Fed Chairman Ben Bernanke announced an upcoming “tapering” of some of the Fed’s QE policies, but because of ensuing market turmoil the tapering was pushed back to January 2014. But for the market, the path was clear … interest rates were going to rise. The result was a “taper tantrum” that pushed both real and nominal interests rates substantially higher throughout 2013.

Note that the Federal Funds Rate — the Fed’s key short-term interest rate — remained at nearly zero throughout the year, but both real and nominal interest rates rose 100 basis points or more … substantially more for TIPS. This is the “nightmare” scenario for TIPS: Sharply higher interest rates combined with subdued inflation. Here is the result for the three ETFs:

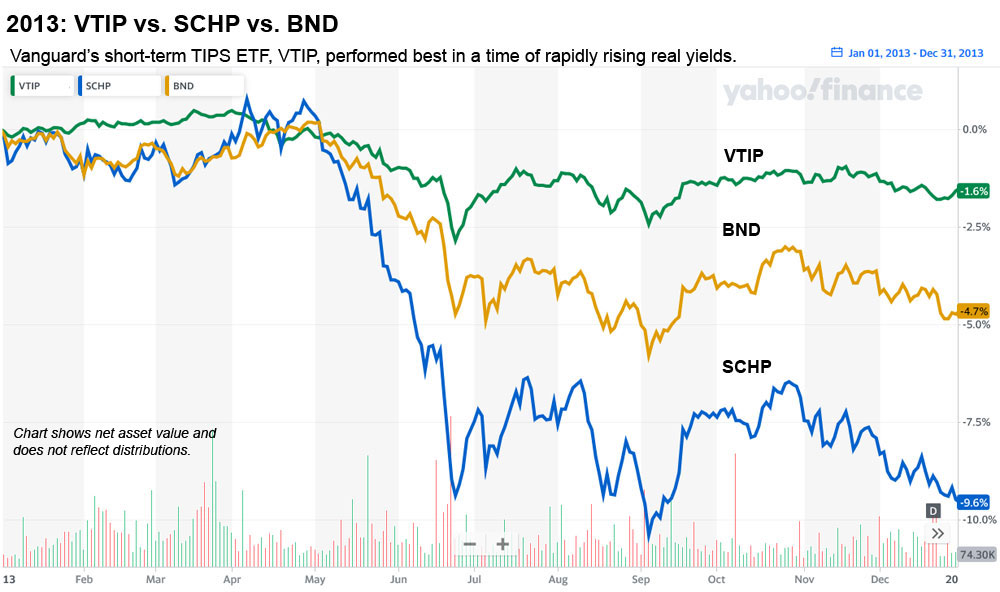

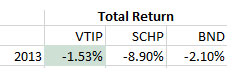

Because of its shorter duration, VTIP held up the best in 2013, while the SCHP’s net asset value plummeted 9.6% before distributions. The chart at the right shows total return, which includes distributions. VTIP was a good performer in a very bad year for bonds.

Conclusion

In a time of rapidly rising interest rates, a shorter duration lessens a bond fund’s interest rate risk. VTIP did reasonably well (meaning not horribly) in 2013 even though Treasury yields surged more than 100 basis points higher. We could be facing a similar scenario in 2022, so VTIP looks like a solid investment in the near term, especially with inflation surging.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

‘Talking about talking about’ is a signal that real yields could be rising

By David Enna, Tipswatch.com

Jerome Powell, chairman of the U.S. Federal Reserve, made some significant statements last week with the potential to shake up both the stock and bond markets. But one response to a question at Wednesday’s news conference rang alarm bells for me:

“But you can think of this meeting that we had as the talking about talking about meeting, if you like. And I now suggest that we retire that term, which has served its purpose well, I think.”

Translation: Powell said, in essence, that the Fed is now willing to talk about future tapering of its aggressive program of buying U.S. Treasurys and mortgage-based securities in support of the U.S. economy. We don’t know when the bond buying will end, or how quickly it will end, but it is now on the table. In addition, increases in short term interest rates could begin in late 2022 or 2023, a year earlier than had been expected.

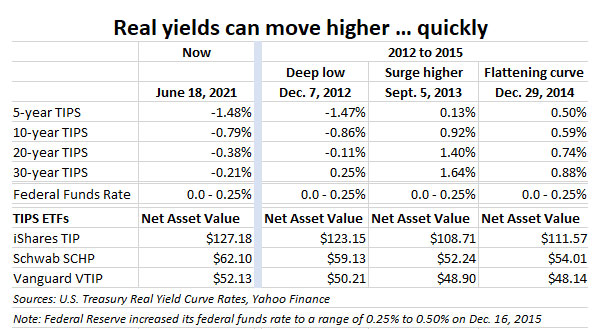

I’ve been thinking about how this “tapering” could affect the real yields and values of Treasury Inflation-Protected Securities. And I think the model to look at is a similar “talking about talking about” period from December 2012 to December 2014, when TIPS yields rose quickly from ultra-low levels. And all of this happened well before the Federal Reserve actually began tapering its bond buying or increasing short-term interest rates. We could be heading into a similar market trend for the remainder of 2021 and into 2022.

Here’s a look at our current market for TIPS compared with the December 2012 to 2014 period, showing that real yields today are very close to those of early December 2012:

Here’s the important historical context to this chart: Ben Bernanke, then the Fed chairman, had hinted vaguely that tapering of bond buying could begin in 2013, but there was no official announcement until June 19, 2013. By that time, the real yield of a 10-year TIPS had already surged from -0.86% on Dec. 7, 2012, to 0.29% on June 19, 2013, an increase of 115 basis points in only 7 months.

Here is information from Wikipedia on this tapering decision:

On 19 June 2013, Ben Bernanke announced a “tapering” of some of the Fed’s QE policies contingent upon continued positive economic data. Specifically, he said that the Fed could scale back its bond purchases from $85 billion to $65 billion a month during the upcoming September 2013 policy meeting. He also suggested that the bond-buying program could wrap up by mid-2014.

The stock markets dropped by approximately 4.3% over the three trading days following Bernanke’s announcement, with the Dow Jones dropping 659 points between 19 and 24 June. … On 18 September 2013, the Fed decided to hold off on scaling back its bond-buying program, and announced in December 2013 that it would begin to taper its purchases in January 2014. Purchases were halted on 29 October 2014 after accumulating $4.5 trillion in assets.

By September 5, 2013, the 10-year TIPS real yield had soared to 0.92%, a remarkable increase of 178 basis points in less than 10 months. But the actual tapering didn’t begin until December 2013. The psychology of tapering moved the bond markets, not the actual deed. And throughout this entire time of surging real yields, the Federal Reserve held its federal funds rate in a range of 0.0% to 0.25%. The first rate increase didn’t come until Dec. 16, 2015.

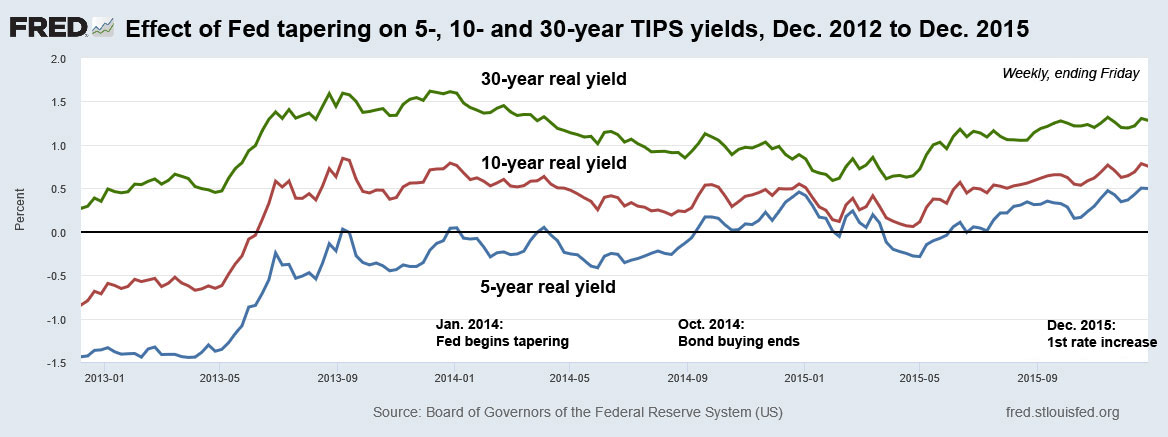

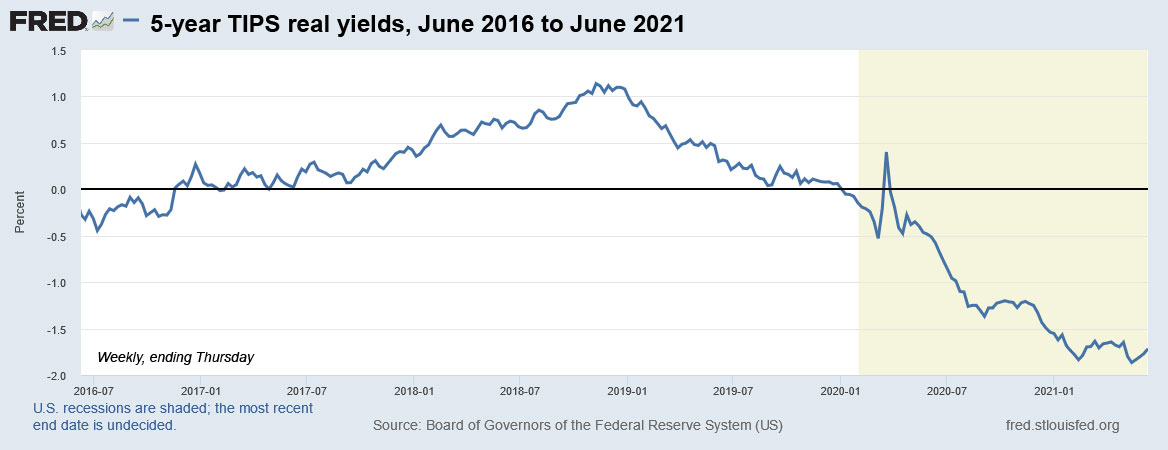

And that is why Chairman Powell’s “talking about talking about” statement is so significant: It is setting in motion a psychology of increasing interest rates, even if the Fed does nothing in coming months. Here is a chart showing TIPS real yields from December 2012 to December 2015, showing that the strong surge higher happened well before the Fed actually began tapering, and nearly 2 years before the first increase in short-term interest rates:

Notice that by December 2014, after the bond buying had ended but a year before short-term interest rates began increasing, the yield curve was flattening in anticipation of future rate increases.

What did that mean for TIPS and TIPS funds?

When real yields rise (or fall) more than 100 basis points, that will have a significant effect on the value of individual TIPS and TIPS ETFs and mutual funds. For a fund like the TIP ETF, which has a duration of 7.53 years, you can expect the net asset value to fall (or rise) by 7.5%, independent of any inflation adjustments.

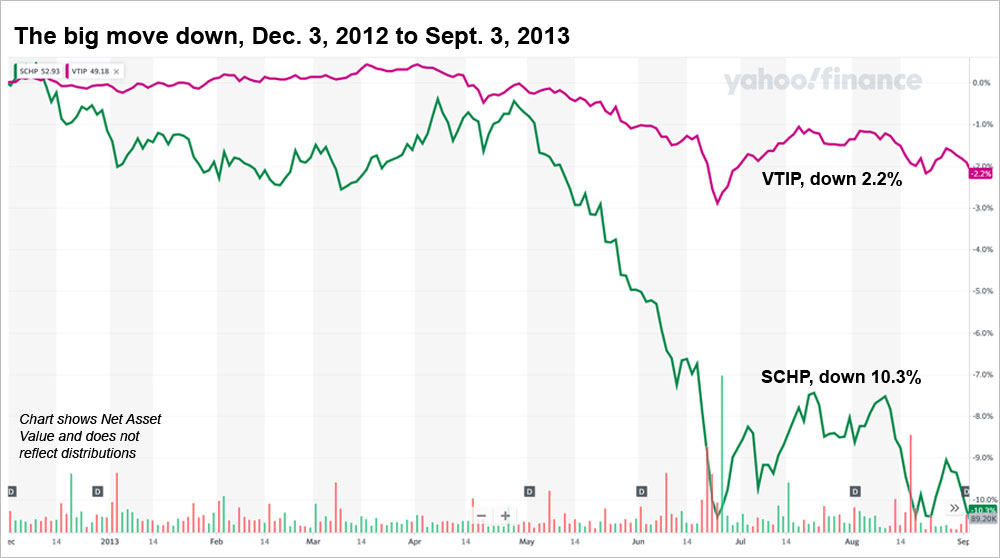

And that is what happened. Here is a chart showing the how the net asset values of my preferred TIPS funds — Schwab’s full-maturity SCHP ETF (duration of 7.4 years) and Vanguard’s VTIP, which invests in 0- to 5-year TIPS (duration of 2.6 years) — performed during the surge in real yields from December 2012 to September 2013:

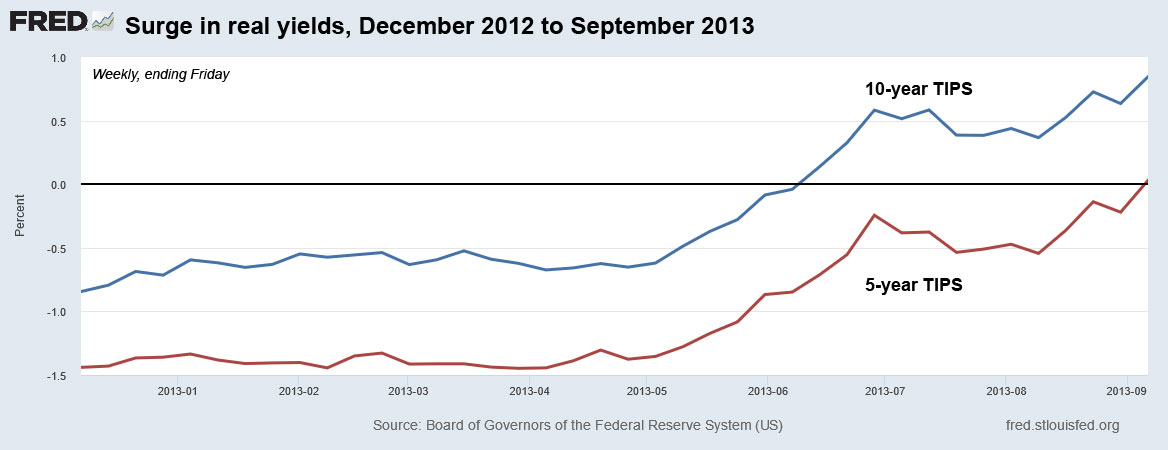

For context, here is how 5- and 10-year real yields surged higher during this period, with the obvious correlation being that higher yields create lower bond values:

After the Fed acted, the yield curve flattened …

This next chart shows the extended period of December 2012 to December 2015, which captures the Fed’s end to bond buying in October 2014 and the first interest rate increase in December 2015. VTIP, the shorter-term TIPS fund, had been performing well for most of 2012-13 and into 2014, but the signaling of higher short-term interest rates started flattening the yield curve, hurting VTIP’s performance. In other words, shorter-term TIPS yields began rising faster than longer-term real yields, and so VTIP took a bigger hit in late 2014, relatively speaking.

Nevertheless, it is clear that VTIP is the preferred TIPS investment in times of rising real yields, because the shorter duration holds down potential losses.

Should you sell out of your TIPS funds?

I can understand the question. TIPS mutual funds and ETFs are a bit more volatile than your typical broad-based intermediate bond fund. They are focused on one esoteric security and hold fewer than 45 issues, generally. Real yields can often move in the opposite direction as nominal yields, at least for short periods of time.

But the key advantage of TIPS and TIPS funds is that they offer a return that is adjusted for official U.S. inflation. That means even if the net asset value declines in coming months, surging inflation could balance off that decline. The outlook isn’t as bad as it might look, assuming inflation continues at a pace of 2.5% or higher.

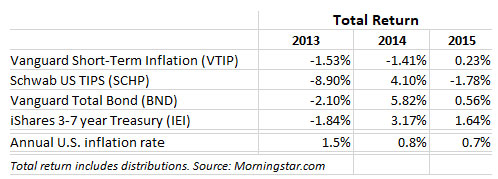

Here’s a look at the total return (including distributions) for four big intermediate term bond funds for the years 2013 to 2015:

Schwab’s broad-based TIPS fund, SCHP, did take a hard hit in 2013, but recovered well in 2014. VTIP also stumbled, but not too badly because of its short duration. But here is the key: Notice the very low inflation rates of those years, averaging 1.0% a year. Our near-term future, transitioning into tapering, could see higher inflation rates, maybe much higher. So TIPS funds seem like a “hold.” My personal preference (for what that’s worth) is to overweight VTIP vs. SCHP, but I will continue to own both.

(If the yield curve seriously flattens over time, longer-term TIPS could end up out-performing shorter-term TIPS, so that would benefit SCHP over VTIP. That is what happened in 2014, after Fed tapering was in progress.)

One other thing: I’d be willing to see some of my fixed-rate investments lose some value, if that meant interest rates would “normalize,” having nominal rates above the rate of inflation. So maybe a 5-year CD would pay a paltry 3.0% again and a 10-year TIPS could get a real yield of 1.0%.

Conclusions

My gut feeling is that the Fed will soon start “backing off” on its tapering hints, especially if the U.S. stock market declines sharply. (The backing-off phase is totally predictable, and expected.) Tapering is coming, but it could be as long as a year away. The Fed seems to like to make “big decisions” at its December meeting, so that will be one to watch.

Powell’s statements this week have already had the effect of strengthening the U.S. dollar, which will in turn help hold down surging inflation. If inflation cools off dramatically later this year, that will take pressure off the Fed. It will not need to move quickly.

But Powell was clearly setting the stage for higher inflation expectations at his Wednesday news conference:

“Inflation has increased notably in recent months. The 12 month change in PCE prices was 3.6% in April and will likely remain elevated in coming months before moderating. Part of the increase reflects the very low readings from early in the pandemic falling out of the calculation, as well as the pass through of past increases in oil prices to consumer energy prices.

“Beyond these effects, we are also seeing upward pressure on prices from the rebound in spending, as the economy continues to reopen … raising the possibility that inflation could turn out to be higher and more persistent than we expect.”

We are entering an uncertain period for investors in Treasury Inflation-Protected Securities. Real yields could be rising. That will be great for future investors; not so great for TIPS traders and holders of TIPS mutual funds.

But … We have to admit that the economic environment of 2021 is “different” from 2013, and this Fed is much more willing to accommodate economic growth and the wealth effect from stock market gains. It will take months of sustained, higher-than-expected inflation — as we saw in February, March, April and May — to force Fed action. Inflation will be the key.

The key point is: It isn’t the Fed actions that drive the markets. Instead, it is the Fed’s signals. And this week we got a huge signal that tapering is coming.

Take a look at the 2013 ‘taper tantrum,’ and what followed …

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The Treasury’s reopening auction of CUSIP 91282CCA7 — creating a 4-year, 10 month Treasury Inflation-Protected Security — went off today with a real yield to maturity of -1.416%, about 31 basis points higher than where this TIPS was trading yesterday morning.

The yield got a boost Wednesday afternoon after the close of the Federal Reserve’s Open Market Committee meeting, which appeared to open the door to future tapering of the Fed’s aggressive bond-buying programs. The Fed also indicated it could begin increasing short-term interest rates in 2023, instead of 2024.

I have been theorizing that the Fed had to put tapering and interest rate increases “on the table” months before it takes those actions. And yesterday, Fed Chairman Jay Powell explicitly (and almost comically) opened that door, saying in his news conference:

But you can think of this meeting that we had as the talking about talking about meeting, if you like. And I now suggest that we retire that term, which has served its purpose well, I think.

With Wednesday’s meeting, the Fed indicated it understands that the surging inflation we have seen in recent months is a threat to be watched, and the Fed will be willing to take steps necessary to control an overheating U.S. economy. The result was: 1) to give the market a breather on inflation fears, and 2) to begin flattening the yield curve, with shorter-term rates rising and longer-term rates holding stable.

And so, just 16 hours later, we get to the Treasury’s reopening auction of $16 billion of a 5-year TIPS. CUSIP 91282CCA7 was trading on the secondary market with a real yield of -1.73% Wednesday morning, but by Thursday morning the yield had jumped to -1.49% and the eventual auction result was -1.416%. For investors, this went well. Send a thank you card to Chairman Powell.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

CUSIP 91282CCA7 has a coupon rate of 0.125%, so investors had to pay a sizable premium to make up for the -1.416% real yield. The adjusted price was about $109.61 for about $102.05 of value, after accrued inflation and interest were added in. This TIPS will have an inflation index of 1.01804 on the settlement date of April 30.

In essence, investors paid about a 7.4% upfront premium to collect an annual coupon payment of 0.125%, plus accruals matching U.S. inflation over the next 4 years, 10 months. Was that a bad deal? Probably not, as I explained in my preview article: “This TIPS might be the prettiest ugly duckling in a pond of extremely ugly ducks.” There are no safe options that will match U.S. inflation in the near- and medium-term, other than U.S. Series I Savings Bonds, which have a purchase cap of $10,000 per person per year.

A week ago, it looked highly likely that today’s auction would set a record low yield for any TIPS auction of any term. But the Fed came to the rescue, and today’s yield remained 21 basis points above the record, -1.631%, set in the originating auction for this TIPS on April 15, 2021.

Here is the trend for 5-year real yields over the last two years, showing the strong move downward after Federal Reserve’s intervention in the bond market, which began in March 2020:

Obviously, it will be a long climb higher toward positive real yields, and I expect we won’t reach those levels until well into 2013, or later. But … you never know.

Inflation breakeven rate

With a nominal 5-year Treasury note trading at 0.88% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.30%, a bit lower than recent trends. This means it will out-perform a nominal Treasury of the same term if inflation averages more than 2.3% over the next 4 years, 10 months.

A week ago, this TIPS had a breakeven rate of 2.49%. But the Federal Reserve’s “wink” toward future tapering of bond purchases and potential increases in short-term rates eased inflation fears. At least a little. So the inflation breakeven rate fell.

Here is the trend in the 5-year inflation breakeven rate over the last two years, showing the surge higher after March 2020, and gradual easing in recent weeks:

Reaction to the auction

The TIP ETF (which holds the full range of TIPS maturities) had been trading slightly down all morning Thursday — indicating higher yields — but then moved positive after the auction’s close at 1 p.m. EDT. This signals a positive reaction to this auction. The bid-to-cover ratio was 2.67, also an indication of solid demand.

Oddly, by 4 p.m., the real yield on this TIPS had slid back down to -1.56%, lower than it was trading in the morning and 14 basis points lower than the auction result. Go figure.

The big “surprise” — which should have surprised no one — was the Fed’s wink and nod Wednesday toward a gradual end of its bond buying and a gradual increase in short-term interest rates. Over time, if this happens, you can expect 5-year TIPS yields to begin rising off these ultra-low levels, even though longer-term yields may remain stable. Inflation breakeven rates should also begin declining.

A lot will depend on how high inflation runs in the next six to nine months. If it begins cooling, then the Fed can hold off on tapering. If it runs hot, the Fed may be forced to step through the door it just opened.

Disclosure: I made a small investment in this TIPS, mainly to test Vanguard’s bond-trading platform. I was unsure until today if I would do it, but the rising yield settled that issue.

Today’s auction closes the history on CUSIP 91282CCA7. The Treasury will launch a new 5-year TIPS in October.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Can anyone make the case that a 5-year Treasury Inflation-Protected Security with a yield lagging inflation by 1.73% and an upfront premium cost of nearly 10% makes sense as an investment?

Hey, I can.

But that doesn’t mean I will be investing in Thursday’s $16 billion reopening auction of CUSIP 91282CCA7, creating a 4-year, 10-month TIPS. I probably won’t. Nevertheless, in today’s low-interest-rate environment — accompanied simultaneously by surging inflation — this TIPS reopening remains an intriguing investment, “relatively speaking.”

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

CUSIP 91282CCA7 was created in an originating auction on April 22, 2021, when it generated a real yield to maturity of -1.631%, the lowest in history for any TIPS auction of any term. The Treasury set its coupon rate at 0.125%, the lowest it will go for a TIPS. Investors had to pay a sizable premium, about about $109.41 for about $100.32 of value, after accrued inflation and interest were added in.

It now trades on the secondary market, and you can follow its current real yield and price in real time on Bloomberg’s Current Yields page. As of Friday’s market close, it was trading with a real yield of -1.73% and a price of $110.30.

If that yield holds through Thursday’s auction, it would set a new auction low for any TIPS of any term. Investors at this week’s auction will actually pay a higher price than Bloomberg indicates, while getting additional principal. Accrued inflation and interest will put the price at about $111.45 for $102 of adjusted value. This TIPS will have an inflation index of 1.01804 as of the June 30 settlement date.

(Just for nerds: As an aside, it’s remarkable that this TIPS was originated on April 15 and non-seasonally adjusted inflation has increased 1.8% since then. The inflation accrual on a TIPS is applied two months after each monthly inflation report. So the calculation for this TIPS is half of February’s rate of 0.547, which is 0.274%, plus 0.71% in March and 0.82% in April. It adds up to 1.804%, and that’s how you get an inflation index of 1.01804).

Here is the trend in the 5-year TIPS real yield over the last five years, showing the remarkable move lower after the market mania of February 2020, which triggered aggressive moves by the Federal Reserve to suppress interest rates and by Congress to stimulate the U.S. economy:

So, how could this TIPS look attractive?

Thursday’s auction could result in a record low real yield for any TIPS in history, of any term. And investors will have to pay a large premium, just to under-perform inflation by about 1.73% over the next 4 years, 10 months. How could that look appealing? It can, because this TIPS might be the prettiest ugly duckling in a pond of extremely ugly ducks.

There is only one U.S. dollar investment that is both very safe and guaranteed to match official U.S. inflation over the next five years. That is the U.S. Series I Savings Bond, which carries a real yield of 0.0%, a whopping 173 basis points better than CUSIP 91282CCA7’s current return. But I Bonds come with a purchase cap of $10,000 per person per calendar year. Once you’ve made that purchase, where do you look for a very safe 5-year investment? Five-year Treasury notes? A 5-year bank CD? Both of those options are safe, but look very likely to severely lag inflation over the next five years.

If you think we are likely to have a run of higher-than-typical inflation over the next five years, this TIPS becomes a logical investment amid a bunch of disastrous choices. Here are the numbers under varying inflation scenarios:

Once inflation averages more than 2.53% a year, this TIPS will out-perform a 5-year Treasury note at 0.76% or a 5-year bank CD at 0.80%, currently among the best in the nation. But the Treasury note and bank CD have no upside potential; they are both going to return well below 1% for five years. The TIPS has unlimited upside potential once inflation averages higher than 2.53% a year.

For that reason, I think this 5-year TIPS is an attractive alternative to other safe 5-year investments.

Inflation breakeven rate

With a 5-year Treasury note currently yielding 0.76%, this TIPS would get an inflation breakeven rate of 2.49% if it auctions with a real yield of -1.73%. That means it will out-perform a U.S. Treasury note if inflation averages more than 2.49% over the next 4 years, 10 months. That’s high, but this breakeven rate has actually dipped a bit in the last two weeks.

Here is the trend in the 5-year inflation breakeven rate over the last five years, showing the remarkable surge in inflation expectations after Federal Reserve and congressional stimulus kicked in in March 2020:

A year ago, I would have said 2.49% is a ridiculously high breakeven rate for a 5 year TIPS. A year ago, in May 2020, inflation had averaged only 1.5% in the previous 5 years. This year, after an impressive surge in inflation, that average has risen to 2.3%. I have no idea what the “new normal” is going to look like, but an inflation rate of 2.5% (or higher) in coming years looks like a reasonable bet.

Conclusion

The key question for investors is: When do you think nominal and real yields will begin rising? If you think higher rates are coming soon, waiting to invest makes sense. If you think rates will remain stable or decline further, and you want to lock in inflation protection, an investment in this TIPS is reasonable. I expect demand to be pretty strong under these market conditions.

If you are planning to invest, keep an eye on that Bloomberg Current Yields page until the morning of the auction. Real yields have been volatile in the last week. This auction closes at noon EDT Thursday for non-competitive bids and finalizes at 1 p.m. I will post the auction results soon after the auction closes.

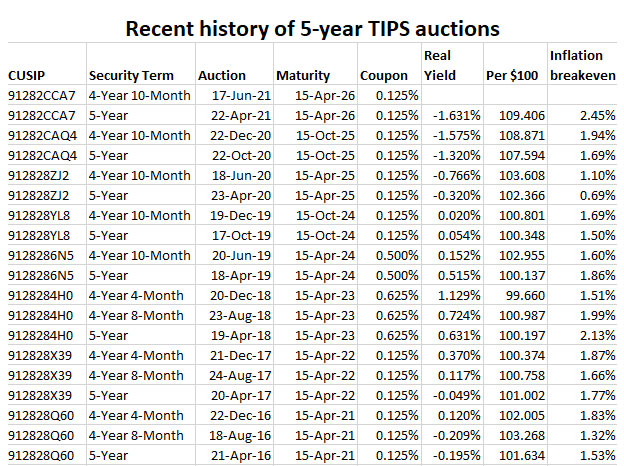

Here’s a chart of recent auction results for 4- to 5-year TIPS:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I selfishly request you add the 20-year TIPS to the list.