By David Enna, Tipswatch.com

For the third month in a row, U.S. inflation surged to higher-than-expected levels in May, reaching the highest annual level in nearly 13 years, the Bureau of Labor Statistics reported today.

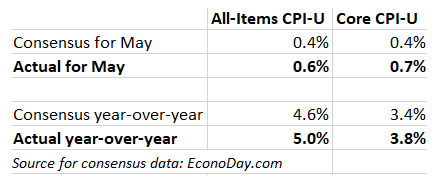

The Consumer Price Index for All Urban Consumers increased 0.6% in May on a seasonally adjusted basis, the BLS said. Over the last 12 months, the all-items index increased 5.0%; this was the largest 12-month increase since a 5.4% increase for the period ending in August 2008. The May numbers were well above the consensus forecasts of 0.4% for the month and 4.6% for the year.

Core inflation, which removes food and energy, rose 0.7% in May and 3.8% over the last 12 months, also racing well ahead of the consensus forecasts of 0.4% and 3.4%. That was the highest increase in core inflation since June 1992.

One amazing aspect of this report was that seasonally-adjusted gasoline prices actually fell in May, down 0.7% for the month but still up 56.2% over the last 12 months. I expected to see higher gas prices, caused by shortages throughout the Southeast thanks to the Colonial Pipeline shutdown. (Gasoline prices in the Southeast have definitely not fallen. Before seasonal adjustment, gasoline prices rose 4.2% in May, the BLS said.)

The index for used cars and trucks continued to rise sharply, the BLS said, increasing 7.3% in May. This increase accounted for about one-third of the all-items increase. Here are other highlights from the report:

- Food prices increased 0.4% in May, the same increase as in April, but are up only 2.2% over the last year.

- The May increase for food was mostly due to the index for meats, poultry, fish, and eggs, which increased 1.3% over the month. The beef index rose 2.3 percent in May.

- The energy index was unchanged in May after declining slightly in April, but is up 28.5% over the last year.

- Apparel prices rose 1.2% in May and are up 5.6% over the last 12 months.

- The household furnishings and operations index increased 1.3% in May, its largest monthly increase since January 1976. Widespread shortages are being reported in furnishings.

- The index for car and truck rentals continued to rise, increasing 12.1% after rising 16.2% the prior month.

- The medical care index declined 0.1% in May after rising in each of the four previous months.

- The costs of shelter rose 0.3% in May, and are up 2.2% over the last 12 months.

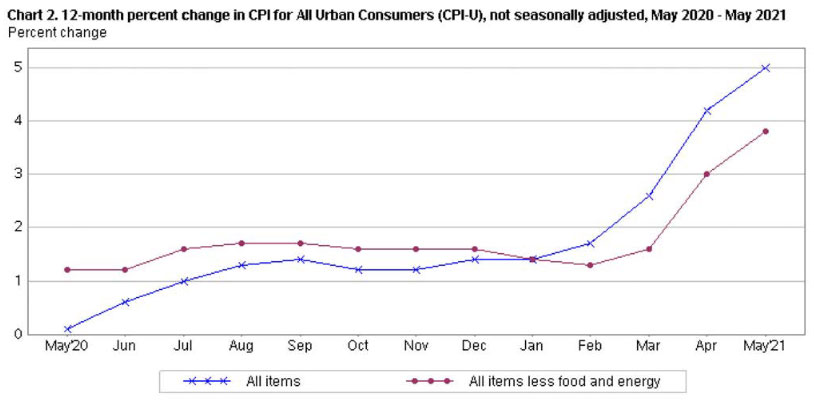

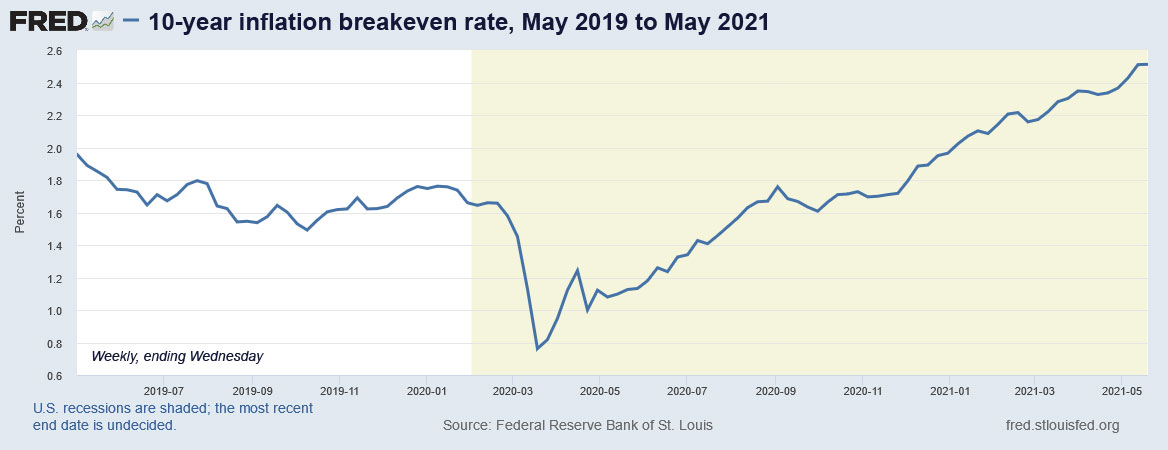

The May report again shows a widespread pattern of unexpectedly high inflation across the U.S. economy, with almost every category except energy showing strong price gains in the month. Here is the 12-month trend for all-items and core inflation, showing the impressive surge higher after the Federal Reserve and congressional stimulus programs stepped up in March 2020:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For May, the BLS set the inflation index at 269.195, an increase of 0.80% over the April number. This follows increases of 0.82% in April, 0.71% in March and 0.55% in February.

For TIPS. The new inflation index means that principal balances for all TIPS will rise 0.80% in July, following the 0.82% increase in June. Because non-seasonally adjusted inflation rose a bit faster than the seasonally adjusted number, you can expect a reversal of that trend in coming months. (Seasonal and non-seasonal numbers balance out over 12 months.) Here are the new July inflation indexes for all TIPS.

For I Bonds. The May inflation report is the second in a string of six months that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on November 1. After two months, inflation is up 1.63%, which translates to a variable rate of 3.26%, already getting close to the current rate of 3.54%. Four months remain, and a lot can happen in four months (especially summer months, when inflation is notoriously volatile.)

Here are the numbers so far:

What this means for future interest rates

The Federal Reserve continues to predict this surge in inflation will be “transitory,” but it’s disturbing that inflation has been running much higher than expectations for three months in a row, even while gas prices were stable. The Fed is hoping to discourage an “inflation psychology” seeping into our consciousness, because it could set off a snowball effect of higher wages and higher raw material costs.

From today’s Wall Street Journal report:

Food makers said their costs are climbing at an alarming rate, prompting them to raise some prices. “The inflation pressure we’re seeing is significant,” General Mills Inc. Chief Executive Jeff Harmening said at a recent investor conference. “It’s probably higher than we’ve seen in the last decade.”

He and his peers point to transportation, commodity and labor costs all increasing at the same time. They expect the trend to continue for at least the rest of this year.

The Federal Reserve tracks a different inflation index — Personal Consumption Expenditures — which was up 3.6% through April and looks likely to top 4.0% for May when that number is released later this month. The Fed wants inflation to “average” above 2.0% for a sustained time. It seems well on its way to reaching that goal.

At some point, probably soon, the Fed will need to begin “talking up” potential plans to taper its bond-buying stimulus programs, which would allow longer-term U.S. rates to begin rising. As of this morning, the stock market is rising nicely despite today’s inflation report. That indicates the financial markets don’t see Fed tapering beginning anytime soon.

But the Fed faces serious challenges if U.S. inflation continues to rise much higher than expectations.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

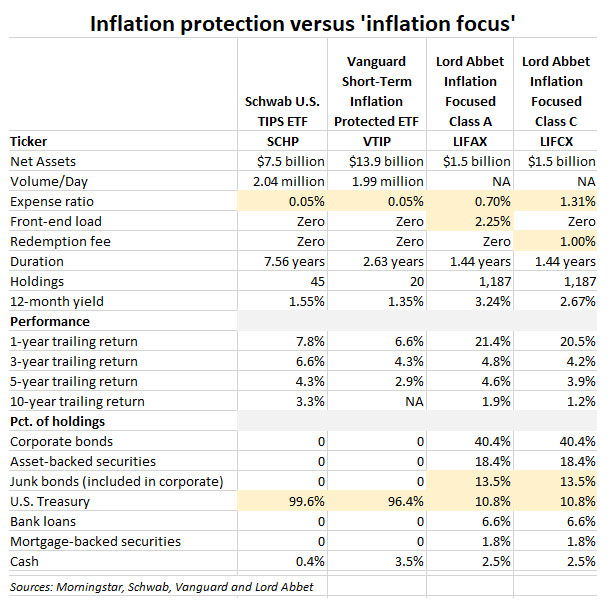

I selfishly request you add the 20-year TIPS to the list.