By David Enna, Tipswatch.com

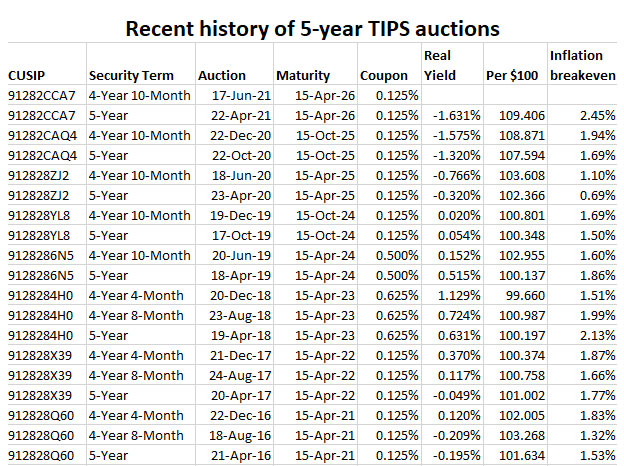

The Treasury’s reopening auction of CUSIP 91282CCA7 — creating a 4-year, 10 month Treasury Inflation-Protected Security — went off today with a real yield to maturity of -1.416%, about 31 basis points higher than where this TIPS was trading yesterday morning.

The yield got a boost Wednesday afternoon after the close of the Federal Reserve’s Open Market Committee meeting, which appeared to open the door to future tapering of the Fed’s aggressive bond-buying programs. The Fed also indicated it could begin increasing short-term interest rates in 2023, instead of 2024.

I have been theorizing that the Fed had to put tapering and interest rate increases “on the table” months before it takes those actions. And yesterday, Fed Chairman Jay Powell explicitly (and almost comically) opened that door, saying in his news conference:

But you can think of this meeting that we had as the talking about talking about meeting, if you like. And I now suggest that we retire that term, which has served its purpose well, I think.

With Wednesday’s meeting, the Fed indicated it understands that the surging inflation we have seen in recent months is a threat to be watched, and the Fed will be willing to take steps necessary to control an overheating U.S. economy. The result was: 1) to give the market a breather on inflation fears, and 2) to begin flattening the yield curve, with shorter-term rates rising and longer-term rates holding stable.

And so, just 16 hours later, we get to the Treasury’s reopening auction of $16 billion of a 5-year TIPS. CUSIP 91282CCA7 was trading on the secondary market with a real yield of -1.73% Wednesday morning, but by Thursday morning the yield had jumped to -1.49% and the eventual auction result was -1.416%. For investors, this went well. Send a thank you card to Chairman Powell.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

CUSIP 91282CCA7 has a coupon rate of 0.125%, so investors had to pay a sizable premium to make up for the -1.416% real yield. The adjusted price was about $109.61 for about $102.05 of value, after accrued inflation and interest were added in. This TIPS will have an inflation index of 1.01804 on the settlement date of April 30.

In essence, investors paid about a 7.4% upfront premium to collect an annual coupon payment of 0.125%, plus accruals matching U.S. inflation over the next 4 years, 10 months. Was that a bad deal? Probably not, as I explained in my preview article: “This TIPS might be the prettiest ugly duckling in a pond of extremely ugly ducks.” There are no safe options that will match U.S. inflation in the near- and medium-term, other than U.S. Series I Savings Bonds, which have a purchase cap of $10,000 per person per year.

A week ago, it looked highly likely that today’s auction would set a record low yield for any TIPS auction of any term. But the Fed came to the rescue, and today’s yield remained 21 basis points above the record, -1.631%, set in the originating auction for this TIPS on April 15, 2021.

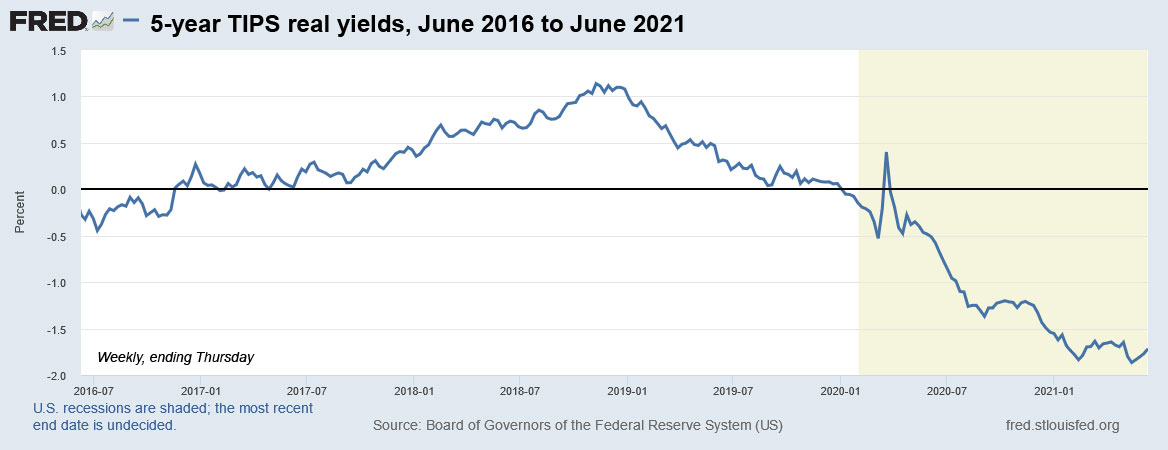

Here is the trend for 5-year real yields over the last two years, showing the strong move downward after Federal Reserve’s intervention in the bond market, which began in March 2020:

Obviously, it will be a long climb higher toward positive real yields, and I expect we won’t reach those levels until well into 2013, or later. But … you never know.

Inflation breakeven rate

With a nominal 5-year Treasury note trading at 0.88% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.30%, a bit lower than recent trends. This means it will out-perform a nominal Treasury of the same term if inflation averages more than 2.3% over the next 4 years, 10 months.

A week ago, this TIPS had a breakeven rate of 2.49%. But the Federal Reserve’s “wink” toward future tapering of bond purchases and potential increases in short-term rates eased inflation fears. At least a little. So the inflation breakeven rate fell.

Here is the trend in the 5-year inflation breakeven rate over the last two years, showing the surge higher after March 2020, and gradual easing in recent weeks:

Reaction to the auction

The TIP ETF (which holds the full range of TIPS maturities) had been trading slightly down all morning Thursday — indicating higher yields — but then moved positive after the auction’s close at 1 p.m. EDT. This signals a positive reaction to this auction. The bid-to-cover ratio was 2.67, also an indication of solid demand.

Oddly, by 4 p.m., the real yield on this TIPS had slid back down to -1.56%, lower than it was trading in the morning and 14 basis points lower than the auction result. Go figure.

The big “surprise” — which should have surprised no one — was the Fed’s wink and nod Wednesday toward a gradual end of its bond buying and a gradual increase in short-term interest rates. Over time, if this happens, you can expect 5-year TIPS yields to begin rising off these ultra-low levels, even though longer-term yields may remain stable. Inflation breakeven rates should also begin declining.

A lot will depend on how high inflation runs in the next six to nine months. If it begins cooling, then the Fed can hold off on tapering. If it runs hot, the Fed may be forced to step through the door it just opened.

Disclosure: I made a small investment in this TIPS, mainly to test Vanguard’s bond-trading platform. I was unsure until today if I would do it, but the rising yield settled that issue.

Today’s auction closes the history on CUSIP 91282CCA7. The Treasury will launch a new 5-year TIPS in October.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If I had funds at this moment I would buy long dated TIPS instead of iBonds. Those real yields are…