By David Enna, Tipswatch.com

I’ve been writing about inflation and inflation-protected investments for 10 years, and most of that time, actual U.S. inflation has been sleepy and dull. Suddenly, but not too surprisingly, that has changed.

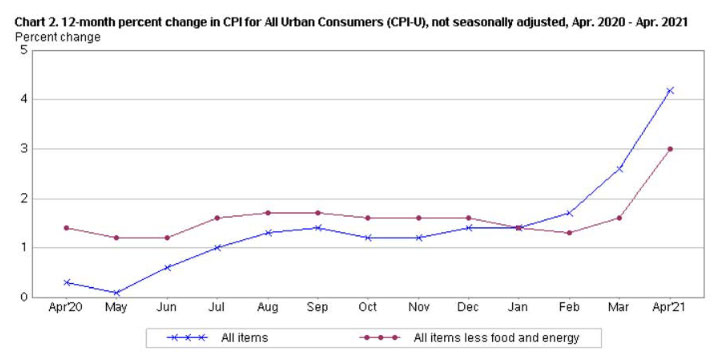

Official U.S. inflation — measured by CPI-U, the Consumer Price Index for All Urban Consumers — rose at unexpectedly high rates in March and April, well above consensus forecasts. And it looks like this could continue for several months. The result: Inflation is suddenly a very hot topic. And that actually is worrisome, because when workers begin “accepting” that future inflation will be high … wages will rise and accelerate the trend.

Google emails me a daily search alert for “Treasury Inflation-Protected Securities,” and most days in the past there would be no email at all, or an email with one or two slightly-related stories. Now, that list is booming to 12 to 15 stories a day.

So let’s take a look at what media are saying about inflation.

Wall Street Journal, May 23

The stakes are high for investors. Inflation dents the value of traditional government and corporate bonds because it reduces the purchasing power of their fixed interest payments. But it can also hurt stocks, analysts say, by pushing up interest rates and increasing input costs for companies. …

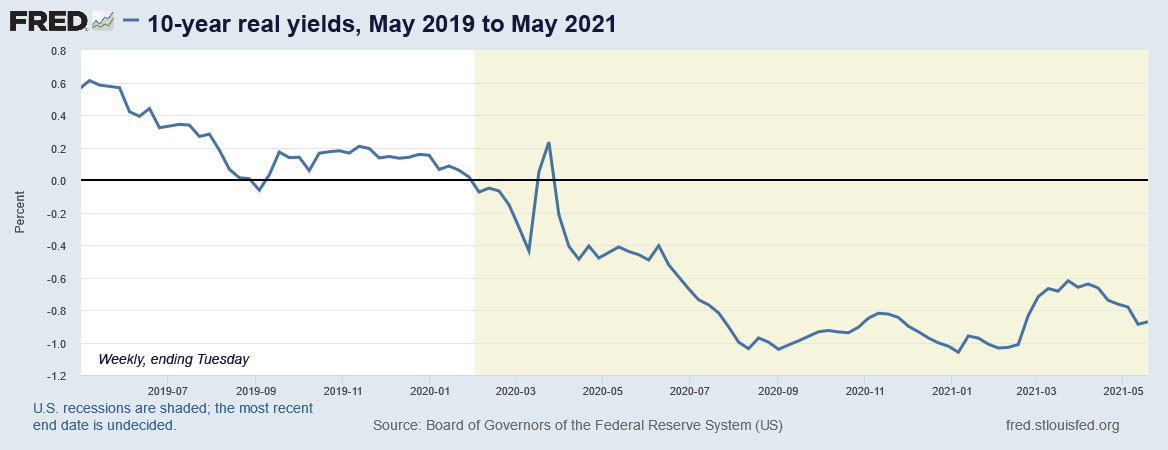

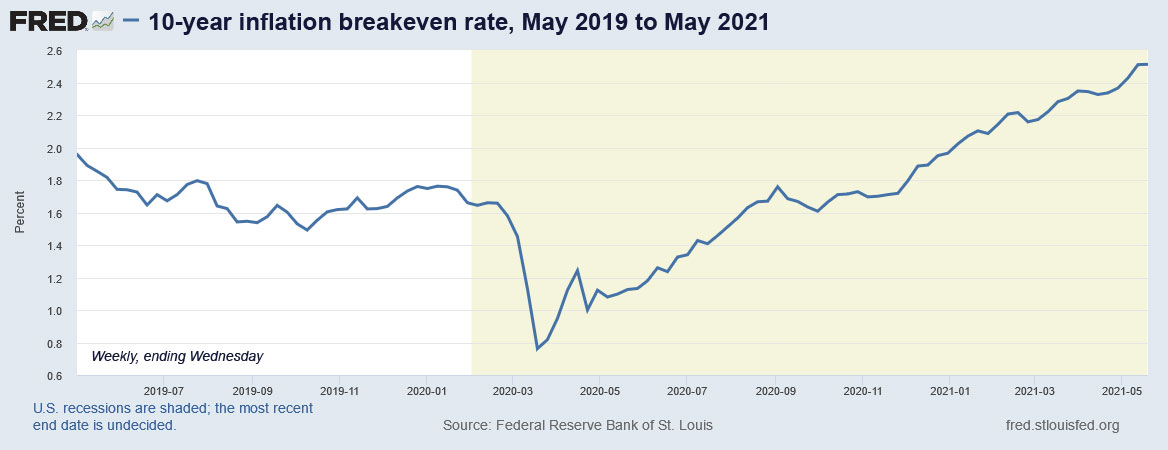

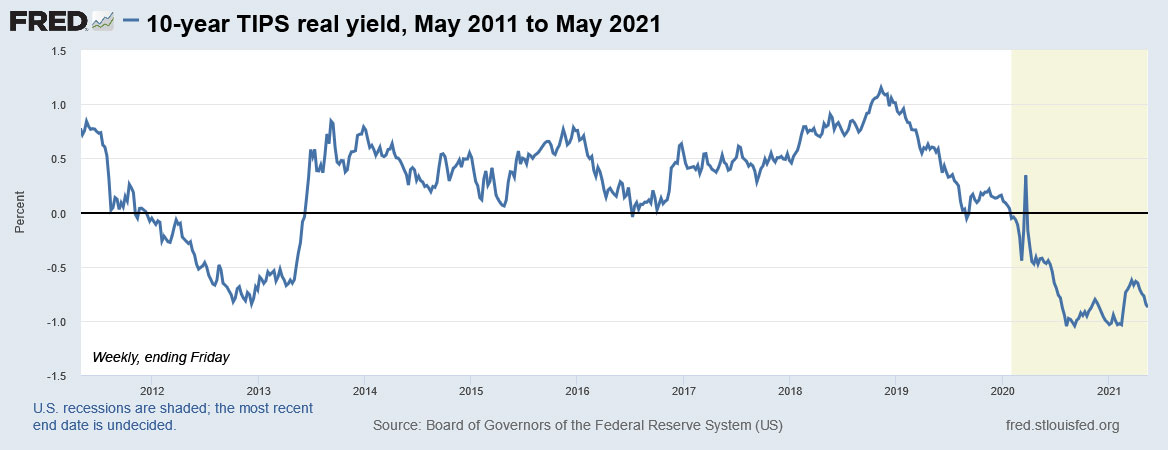

As of Friday, the yield on 10-year TIPS was minus 0.826%—meaning investors would lose money absent any inflation—compared with 1.629% for the nominal 10-year Treasury note. That means CPI growth would need to average at least 2.45% over the next 10 years for the inflation-protected security to pay as much or more than the nominal Treasury.

To some, this makes TIPS the safest and best inflation hedge. Investors are nearly guaranteed to get their principal back if they hold the bonds to maturity. At current yield differentials, they can earn significantly more than regular Treasurys if inflation fears are realized.

Still, TIPS returns are likely to be paltry under almost any scenario, particularly if inflation comes below expectations.

Yahoo! Finance, May 21

About one in three U.S. adults say they’re spending more on groceries than they were at the start of 2021, according to a Morning Consult survey of 2,200 U.S. adults conducted May 17 to 19 for Bloomberg News. Red meat was the ingredient cited most often for its higher prices, with chicken right behind.

CNBC, May 21

“In general, inflation is usually negative for stocks,” said Amy Arnott, a portfolio strategist at Morningstar. She pointed to history as proof: Between 1973 and 1981, inflation rose by more than 9% a year. During the same period, stocks shed about 4% annually. …

Another good match for investors worried about inflation are Treasury Inflation Protected Securities, or TIPS, said CFP Nicholas Scheibner, a wealth management advisor at Baron Financial Group in Fair Lawn, New Jersey. These securities carry a similar risk as other fixed income investments, he said, but they add an adjusted principal amount if inflation increases.

E-piphany by Michael Ashton, May 20

The Federal Reserve has recently started to use the word “transitory” when describing inflation pressures in the U.S. economy. What they’re trying to indicate is that we shouldn’t worry, the pressures we are seeing right now will eventually pass. But that’s stupid. All inflation is transitory. …

Maybe what they mean is that “these price changes we are seeing are all the results of supply and demand imbalances in nominal space, so they’ll all reach equilibrium and inflation will go away.” If that’s so, then (a) they’re probably wrong, (b) that’s what inflation looks like anyway; it doesn’t manifest as smooth price changes across all goods at the same time, and (c) you still haven’t told me over what period it will take for this equilibrium to occur.

New York Times, May 20

It is too soon to show up clearly in the data, but there are anecdotes aplenty that companies are rapidly increasing pay. Just this week, Bank of America said it would start a $25-per-hour minimum wage by 2025, up from $20, and major chains like McDonald’s, Starbucks and Chipotle have announced significant moves toward higher pay in recent weeks.

Associated Press, May 20

Many economists, as well as the Federal Reserve, say not to worry about any of this. They’re convinced these fast price gains will prove fleeting. If the experts are wrong, however — remember last month’s jobs data, where economists’ predictions were wildly off the mark? — it could ravage the economy and force the Fed to reverse its record-low interest rate policy and trim the bond purchases that are boosting markets. … (B)e prepared to experience even more swings in the stock market as Wall Street’s biggest question waits even longer to be answered.

Barron’s, May 17

For business owners and consumers on the ground, official inflation data and policy makers’ commentary are an alternate reality. Inflation is here, say grocery shoppers, home buyers, manufacturers, and retailers who insist that their dollars are buying less. …

The gap between reported price inflation and the experiences of businesses and consumers is a signal to investors that inflation is hotter than it looks. Implications of the disconnect are vast, affecting Social Security payments, tax-bracket adjustments, and economic growth calculations, in addition to investment returns, inflation expectations, and interest rates.

“All you have to do is open up your eyes to see there is inflation pressure everywhere,” says Ed Yardeni, president of Yardeni Research. “We are in stimulus shock.”

MarketWatch, May 12

The Fed has been hit by two major data surprises. Last Friday’s weaker-than-expected April job report and Wednesday’s hotter-than-expected April consumer prices. …

As the economy reopens, “we could have more persistent imbalances between aggregate demand and supply that would put more persistent upward pressure on inflation than we and outside forecasts expect,” (Federal Reserve Vice Chairman Richard) Clarida said Wednesday after the inflation data was published.

“I expect inflation to return to – or perhaps run somewhat above – our 2% longer-run goal in 2022 and 2023,” he said.

Final thoughts

I was at a dinner party recently (with fully vaccinated friends) and the topic turned to cooking and shopping in general. I asked the group: “Do you think prices are rising much faster right now?” The immediate reaction was a loud “YES,” across the board, with people giving examples of the price of onions, meat, lumber, used cars, housing.

Consumers have been noticing higher inflation for months. In May, the U.S. media also noticed. The overall effect is that “inflation consciousness” is seeping into the U.S. economy. This trend will continue for several months, but could dwindle later in the year. Or not. We’ll see.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…