By David Enna, Tipswatch.com

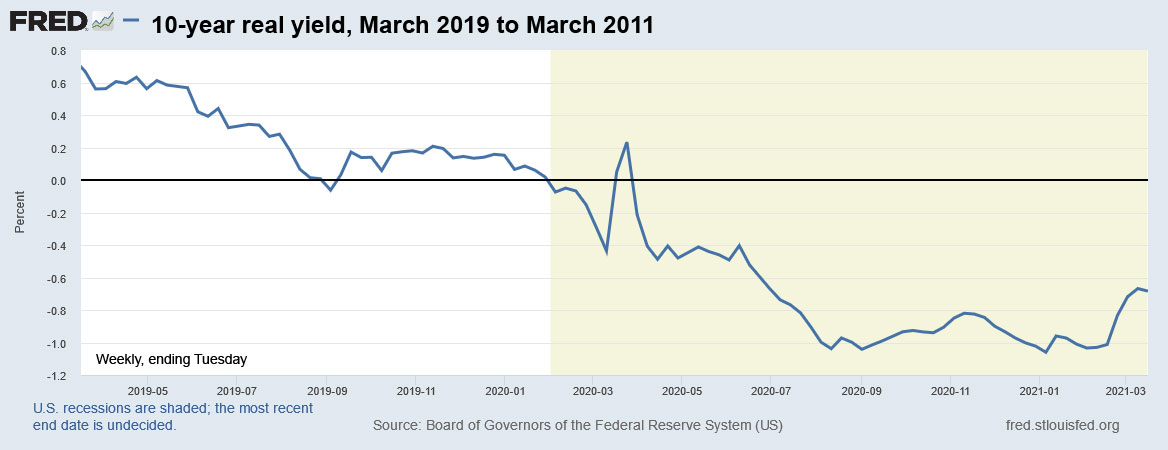

On my way to look something else up, I noticed something interesting: The yield of the nominal 5-year Treasury note has been rising nicely over recent weeks, but yields of 5-year insured bank CDs remain stuck at very low levels. That shouldn’t be happening, but here we are.

As this chart shows, this isn’t an unusual situation. Banks have been pushing customers away from 5-year CDs for several years, preferring to offer attractive 11-month or 1-year CD rates, which can bring new customers into the door. But during the early months of the pandemic, banks held 5-year CD rates relatively stable at already very low rates. Now that the 5-year Treasury yield is rising, banks are standing pat, with the national average 5-year CD rate at 0.30%. The 5-year Treasury yield closed Friday at 0.97%, up a strong 61 basis points this year.

Even when you look at yields for best-in-nation 5-year CDs, they almost always lag well below the 5-year Treasury, which is equal in safety, has no purchase limit and is not subject to state income taxes.

OK, I admit that a 5-year Treasury paying a nominal yield of 0.97% isn’t attractive. But I wonder why some banks don’t adopt a strategy of locking in customers at a 1.2% yield for 5 years, when it seems rather likely that yields could rise substantially in coming years. But the more aggressive, online-oriented banks are focusing on 1-year maturities.

The 1-year Treasury bill is currently yielding 0.07%, while many best-in-nation banks are offering yields of 0.50% and above. For the one-year term, bank CDs are much more attractive, versus Treasurys.

And, for the record, banks like BB&T and Wells Fargo that allow customers to sign up for CDs paying 0.01% interest should hang their heads in shame.

The danger of CD rollovers

My theory is that many banking customers allow their CDs to roll over at maturity, without even checking the current yield. For example, I have an 11-month CD at Ally Bank that will mature in May. It is currently yielding 1.2%. If I allow it to roll over next month, the yield will probably drop to 0.5%, a drop of 70 basis points. Well, at least that’s better than the 0.01% I’m earning in my brokerage cash account.

That Ally rollover isn’t a bad deal, and this is a no-penalty CD, so the money is always available to withdraw if conditions change.

But that’s not the case if you have a 5-year CD maturing soon. Back in 2016 to 2019, it was possible to snag 5-year bank CDs paying well over 2.0% (we used to laugh at that rate, remember?). When those CDs mature, they will be automatically rolled over to new 5-year CDs paying at the best about 0.80%, and maybe much lower.

Your bank should notify you of an upcoming CD rollover. Pay attention, and go shopping. If you are looking for safety, my recommendation is to hunt for 1) online savings accounts paying 0.5% or more, or 2) 1-year CDs yielding 0.5% or more, in a bank you like working with. Ally Bank’s “no penalty” feature is attractive, but it is only offered on the 11-month term. It yields 0.50%, the same as the bank’s online savings account. However, yields on these online bank savings accounts have been drifting lower over the last year.

The 5-year term just isn’t attractive at this point.

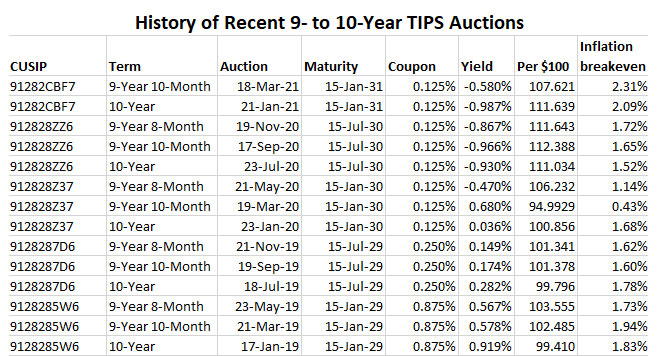

However, a new 5-year TIPS will be offered at auction on April 22. I will be taking a deeper look at that investment in a couple weeks.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It would be my pleasure to accommodate you However, the URL for 20 year TIPS at CNBC pulls up no…