By David Enna, Tipswatch.com

If you follow the bond market at all, you know that longer-term nominal yields have been inching higher since the beginning of the year, and longer-term real yields (meaning yields above inflation) have been climbing, too. But the action has been primarily focused on the 10+-year maturities, and that means that the yield curve is steepening.

Here’s the trend in nominal yields:

- 4-week bill: Started the year at 0.09%, now at 0.03%, a decline of 6 basis points.

- 5-year note: Started the year at 0.36%, now at 0.59%, an increase of 17 basis points.

- 10-year note: Started the year at 0.93%, now at 1.37%, an increase of 44 basis points.

- 30-year bond: Started the year at 1.66%, now at 2.21%, an increase of 55 basis points.

And for real yields:

- 5-year TIPS: Started the year at -1.62%, now at -1.76%, a decrease of 14 basis points.

- 10-year TIPS: Started the year at -1.08%, now at -0.79%, an increase of 29 basis points.

- 30-year TIPS: Started the year at -0.39%, now at 0.08%, an increase of 47 basis points.

These moves higher in the longer terms are pretty dramatic in just two months, but at the same time, the shorter-term yields have actually declined. Here’s a chart comparing the Treasury’s real yield estimates for 5-, 10- and 30-year TIPS over the last 5+ years, with the simultaneous changes in the Federal Funds Rate during that period:

A couple of things are remarkably well demonstrated here: 1) Times of “easy money” (meaning times the Fed is holding short-term interest rates very low) tend to widen out the yield curve, and 2) times of tightening (when short-term interest rates are increasing) tend to flatten out the yield curve.

A flat yield curve, or the even more ominous inverted yield curve, is seen as an omen of upcoming economic distress. A widening yield curve, as we are seeing now, is considered a good omen for the economy. Certainly, talk in Congress of another $1.9 trillion in stimulus spending is having an effect on the longer yields.

The Federal Reserve has a lock on short-term interest rates, and Fed Chairman Jerome Powell made clear this week that very low short-term rates will continue well into the future. And he said he didn’t think increased stimulus spending would trigger higher inflation:

“Inflation dynamics do change over time but they don’t change on a dime, and so we don’t really see how a burst of fiscal support or spending that doesn’t last for many years would actually change those inflation dynamics.” …

But while the Fed can control short-term interest rates, it can only “influence” longer-term interest rates, which are much more market driven. The Fed is continuing asset purchases to stabilize the Treasury market, but hasn’t stepped up those efforts in 2021 as longer-term rates have been increasing.

And in fact, the Fed could be allowing longer-term rates to creep higher in an effort to cool speculation in stock and currency markets. From a MarketWatch report:

“The Fed is not bothered by the move and may be slow to fight it,” said Mark Cabana, head of U.S. rates strategy at BofA Global Research, in a Wednesday note. …

“It seems so far that what the Fed is viewing in the bond market as constructive,” said Padhraic Garvey, regional head of research for the Americas at ING, in an interview.

What this means for the TIPS market

If you are an investor in TIPS mutual funds or ETFs, you’ve probably seen the value of your holdings decline this year, after a very good performance in 2020. When real yields rise, the value of a TIPS declines. The TIPS universe includes only 46 total issues, and of those, 18 have maturities of 0 to 5 years, and 34 have maturities under 10 years.

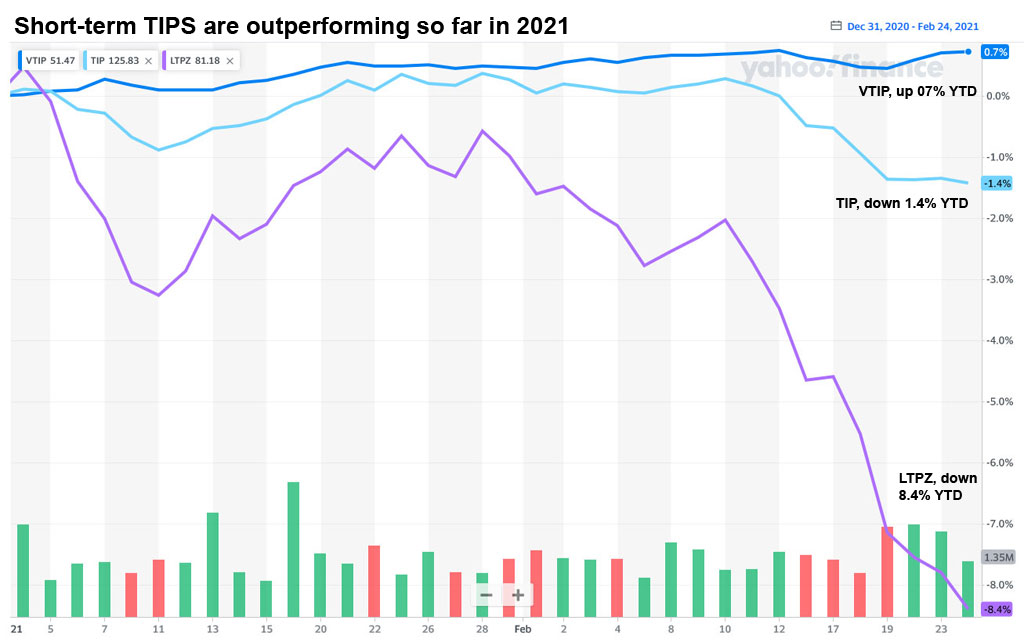

So given the events of 2021 so far, you’d expect that a short-term TIPS ETF (like Vanguard’s VTIP, which holds 0-5 year maturities) to be outperforming a broad-based TIPS ETF (like iShare’s TIP, with 1-30 year maturities) or a longer-term TIPS ETF (like Pimco’s LTPZ, with TIPS of 15+ year maturities).

And that is what is happening, as this stock chart shows:

Will this trend continue?

Anything I say is pure speculation, okay? But yes, I think this trend could continue, as long as the Fed remains committed to holding short-term interest rates near zero, while also allowing the longer-term yields to climb higher.

No matter what happens in the rest of 2021, I think the Fed will resist the urge to force short-term interest rates higher. And if the pandemic wanes and the economy gradually improves, the Fed shouldn’t be overly worried as yields creep higher for longer-term bonds.

But what if the stock market hits a deep correction or even falls into a bear market? Then the Fed, as it always does, will attempt to come to the stock market’s rescue. And at that point it will try to force longer-term rates lower through aggressive bond buying. Just my opinion.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he recommends can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David – Do you have any thoughts on the Fidelity Inflation-Protected Bond Index Fund (FIPDX)? I have read conflicting info on when it will be the right time to buy into TIPS bond mutual funds. Should it be viewed as in/out every two years or so? Have you ever done a comparison of Vanguard, Fidelity, et al, TIPS funds, side-by-side?

My favorite broad-based TIPS fund (ETF) is Schwab’s SCHP, with an expense ratio of 0.05% and a duration of 7.6 years. FIPDX is probably just as good, with the same expense ratio, and a shorter duration of 5.35 years. So it should be less volatile. But these two funds seem to track closely. SCHP is down 1.3% YTD total return, with FIPDX is down 1.26%.

My favorite shorter-term TIPS fund is VTIP, same 0.05% expense ratio, and a duration of 2.8 years, so it is a lot less volatile. It is up 0.63% YTD total return.

All of these funds have at least a full duration worth of risk when interest rates begin rising, meaning that the downside risk is at least 2.8% for VTIP or 7.6% for SCHP, and I think we’d probably eventually see a fall of 11% or so in the broad-based funds.

But that’s true for just about every bond fund out there. TIPS funds present some interest-rate risk, but not credit risk.

So, dollar-cost average into the funds, or buy on the dips? (Disclosure: I own VTIP and SCHP in a retirement account.)

Definitely think that rising yields may be forecasting inflation. Besides TIPS, would you advise any other securities, or do you believe that TIPS will serve as sufficiently effective, as a hedge against the devaluation of the dollar?

The devaluation of the dollar is a part of this equation that few analysts mention as a cause of potential future inflation. Chairman Powell emphatically stated this week that he is not concerned about inflation, and more worried about “disinflation.” The U.S. Dollar Index has fallen from 102.82 on March 19, 2020, to 90.19 today, which is a drop of 12%. I have a horrible record of predicting future inflation, which has me in a very large crowd, including the majority of big-money TIPS investors. Other possible investments might include Bitcoin, but it is being speculated wildly higher, out of line with inflation. Really good quality stocks probably will do fine in an inflationary environment, too. But are they too pricey right now? Gold? I don’t do gold. My feeling is that U.S. Series I Savings Bonds are the best inflation-protected investment right now.

Thanks, my understanding is that IVOL benefits from steepening yield curve…

IVOL is an interesting fund. Also if you are looking for other liquid bond alternatives…check out DRSK – bond like volatility with upside potential from the option overlay and very minimal duration risk within the bond portfolio.

Would VTIP be a good place to stash my cash? What are the risks?

VTIP will work out well IF … and it is an IF … short-term interest rates continue at a very low level and inflation perks up. It’s not a risky fund, but because the duration is 2.8 years, then it will drop in value if short-term real yields begin rising. Overall, it is not risky and it has a great expense ratio of 0.05%.

David, do you have comments about IVOL?

I looked at IVOL awhile back, which basically overlays the Schwab TIPS fund (SCHP) with derivatives to try to take advantage of volatility. I was going to write a real-life side-by-side comparison with SCHP, and bought the same amount of both funds on the same day. But … I realized Vanguard would not reinvest my dividends in IVOL because its trading levels are still too low. So I ditched it. So far in 2021, IVOL has been out-performing SCHP, with a positive gain of 2.9% versus -1.2% for SCHP. It’s intriguing, but the expense ratio is 0.99% and it is a very new fund.

Thanks, my understanding is that IVOL benefits from steepening yield curve…