By David Enna, Tipswatch.com

There’s been a lively discussion going on over at the Bogleheads forum about the possibility that the recent rise in real yields could prompt the Treasury to raise the fixed rate on the Series I Savings Bond above its current 0.0%. And that leads to the question: “Should I buy I Bonds now, or wait until later in the year?”

The correct answer is: “It doesn’t matter.” The Treasury will reset the I Bond’s fixed rate on May 1 and then again on November 1. I’d say with 99% certainty that the fixed rate will remain at 0.0% in the May reset, and it’s “highly likely” it will stay at 0.0% in November. I already bought my full 2021 I Bond allocation — in January — because I had a maturing TIPS that provided the needed cash.

Want to know more about I Bonds? Check out the Q&A at the bottom of my “Tracking Inflation and I Bonds” page.

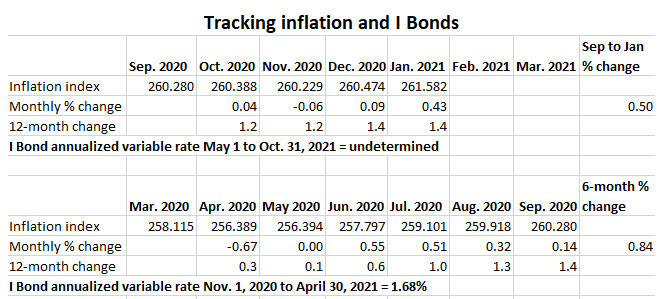

I Bonds purchased today through April 30 will carry that permanent fixed rate of 0.0% and a six-month inflation-adjusted variable rate of 1.68%. Both the fixed rate and the inflation rate will be reset on May 1. I’m predicting the fixed rate will stay at 0.0%, and the inflation rate should be somewhere close to the current 1.68%.

The reset of the inflation-adjusted rate will be determined by official U.S. inflation from September 2020 to March 2021. As of the January inflation report, inflation was running at 0.50%, with two months remaining in the rate-setting period. That translates a variable rate of 1.0%, with two months remaining. Here are the numbers:

Because gas prices have been rising recently, it looks likely that inflation is going to be moderate to moderate-high over the next two months. That should push the inflation rate up to at least the 0.80% to 1.00% range, which translates to an I Bond variable rate of 1.6% to 2.0%. It could even be higher, but guessing future inflation is a loser’s game.

Anyway, the current variable rate of 1.68% is highly attractive given near-zero interest rates for safe investments of up to five years (you can’t find bank CDs or Treasurys anywhere close to that), and the new rate coming in May should also be attractive. If you buy an I Bond today, you’d get the 1.68% annualized rate for six months, then the next annualized rate for six months. My personal opinion: Buy anytime before May 1, but it’s not going to make a huge difference.

But could the fixed rate rise on May 1?

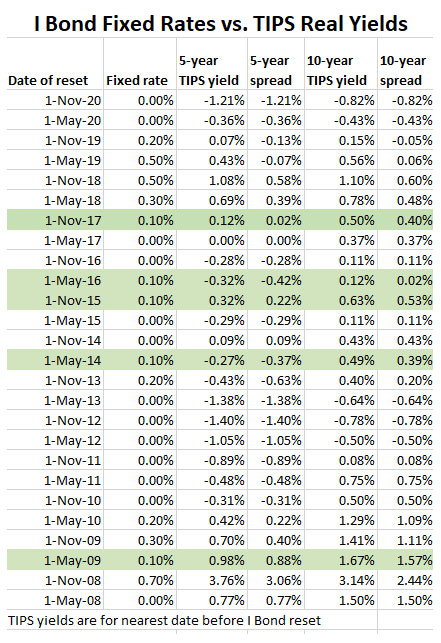

Short answer: No. The Treasury isn’t going to raise the fixed rate of an I Bond above 0.0% as long as the real yields of 5-year and 10-year TIPS are deeply negative. Here are the Treasury’s real yield estimates at today’s market close:

Understand that the I Bond’s fixed rate of 0.0% is equivalent to its “real yield to maturity.” In other words, it will almost exactly match official U.S. inflation for as long as you hold the I Bond. Therefore it has an 172-basis-point advantage over a 5-year TIPS and a 74-basis-point advantage over a 10-year TIPS. Those are huge advantages, equivalent to 8.6% of the value of a 5-year TIPS and 7.4% of the value of a 10-year TIPS.

Because the Federal Reserve is committed to holding short-term nominal rates near zero for more than a year in the future, and may step in to knock down longer-term nominal yields, it’s not likely that real yields in the 5- to 10-year range can climb above 0.0% in 2021. So I think the I Bond’s fixed rate will stay at 0.0%, at least through May 2022.

Take a look at this chart comparing the I Bond fixed-rate resets with the current 5- and 10-year TIPS yields just before the change. I’ve highlighted all the times the Treasury set the fixed rate at 0.1%. In every one of those times, the 10-year real yield was above 0.0%. There are instances where the 5-year TIPS yield was below 0.0%, but nowhere near the current -1.72%.

However, the Treasury does do odd things at times, so I am not 100% certain. But keep this in mind: If the Treasury raises the I Bond’s fixed rate to 0.1%, that is the equivalent of $10 a year on a $10,000 investment. It is no big deal. But I totally understand the desire of I Bond investors to fret about that fixed rate, because of psychology. We want the best possible investment, and a higher fixed rate is better than a lower fixed rate, even if just $10 is at stake.

Let’s say the Treasury goes nuts and raises the I Bond’s fixed rate to 0.50% on November 1. I would celebrate, even though I have already bought my 2021 allocation of $10,000 per person per calendar year. Why? Because in January, I’d be able to snag that 0.50% fixed rate with my 2022 allocation.

So, wait or not wait to buy I Bonds? It won’t matter much. I will address this topic again late in April, after the new variable rate is set by the March inflation report. The key thing is: Buy them every year, up to the maximum or whatever level you can afford. Because of the $10,000 purchase limit, it takes years to build a sizable holding of I Bonds.

Could the Treasury set a negative fixed rate?

The Treasury does not reveal how it sets the I Bond’s fixed rate and there is no apparent formula. The evidence suggests they at least look at the 10-year TIPS real yield, but there’s no precise calculation. This has led to speculation — including by me — that the Treasury could consider setting a negative fixed rate, letting it drop below 0.0%. It has never done this, but I couldn’t find any wording on the Treasury site that guarantees this. This is the Treasury’s totally vague explanation:

Treasury announces the fixed rate for I bonds every six months (on the first business day in May and on the first business day in November). That fixed rate then applies to all I bonds issued during the next six months. The fixed rate is an annual rate. Compounding is semiannual.

But … one of the Bogleheads heros, HueyLD, solved this vagueness by finding very specific language in the Federal Register that states the I Bond’s fixed rate can never drop below 0.0%, and that its composite rate can also never drop below 0.0%, even in a time of severe deflation.

Click here to read the full citation. From that text:

The (Treasury) Secretary, or the Secretary’s designee, determines the fixed rate of return. The fixed rate is established for the life of the bond. The fixed rate will always be greater than or equal to 0.00%. The most recently announced fixed rate is only for bonds purchased during the six months following the announcement, or for any other period of time announced by the Secretary.

… Composite rates are single, annual interest rates that reflect the combined effects of the fixed rate and the semiannual inflation rate. The composite rate will always be greater than or equal to 0.00%.

So, at least that issue is settled. The I Bond’s fixed rate, under current regulations, cannot go below 0.0%, even when other real yields have fallen deeply negative. And that means that I Bonds remain the world’s best inflation-protected investment in March 2021.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he recommends can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

@SponsoredLynx, I have wondered how many people might be using the accrual method for tax payments on I Bonds and EE Bonds. It does mean negative cash flow until you actually redeem the I Bond. I personally love that Savings Bonds work as the equivalent of a “traditional IRA,” where all the interest compounds with no taxes due until redemption. … I shoot for a “target AGI” each year and try to get close with a combination of traditional IRA withdrawals and/or Roth conversions. Next year, when the EE Bonds pay out, I will just add that into the target AGI and cut back on other withdrawals/conversions.

The Tax Reform Act of 1986 did very well for me and ever since I have been concerned with hedging against the return of what many would–today–consider obscene marginal tax rates. But you and I are old enough to know better!

One of the many advantage of I-bonds, as you note, is that the composite rate will never be negative. I have some nice 3.0% fixed rates I bought back in 2001, when you could buy $30,000 a year. I never really thought that would be one of my better investments. Maturity will be tricky, because that’s when the IRS comes in. I figure it would be best to cash out over a three or four year period prior to maturity to minimize the annual tax burden. I have to do the math. You might want to write about it. Thanks for your fine columns.

Given current interest rates being very close to zero, I’d probably hold those I Bonds to maturity. They are now paying something like 4.68%, and you can’t beat that elsewhere. I also have those 2001 I Bonds, but a smaller initial investment. I’m going to wait it out until 2031 and just take the tax hit. I have a similar situation next year with EE Bonds from 1992 that are still earning 4%, after a doubling period paying 6%. They will be worth about 4x my initial investment. Nice problem to have. I’ll just have to adjust my other income lower (Roth conversions, for example) that year.

I’ll probably have at least $120,000 in interest on I-bonds if I cash out out in 2021. I’ll probably cash out a third in 2019, a third in 2020, and a third in 2021. The end game is something people don’t talk much about. It is more-or-less a math problem. But I have to think the worst thing to do would be to hold completely to maturity and get hit with taxes on $120,000 interest income in one year.

The simple fact that the government is now less enthusiastic about people buying I-bonds (going from $30,000 a year to only $10,000 a year per social security number) suggests to me that I-bonds must be a good deal.

I’ve got a full load of 2001 I Bonds as well, but I’m on an accrual basis for all my savings bonds, which I think will be advantageous in the long term. This also increases my comfort level with adding EE bonds each year since 2015, which I might not have done if I faced huge looming tax bills on I bonds. I think new investors should *strongly* consider being on an accrual basis, especially since recent EE bonds will give you enough of a balloon tax bill even with accrual accounting (at 0.1% nominal interest).

I too bought my full I Bond allocation after struggling with the fixed rate dilemma. Like you, I could not see a nonzero fixed rate for the May 2021 announcement. However, I think a hike in November 2021 is not out of the question. But the 1.68% tax-advantaged interest from now to November more than compensated me for foregoing the risk-adjusted November fixed rate.

I also write to add my name to the chorus of those who laud your efforts. Thanks again for your consistent, high-quality analysis.

Thanks for the update. As always I appreciate your insight.

Thanks for the update. Quality content as usual.

David – This is well-received. As usual, it is well-researched, timely, and explained quite well. I have been reading your articles for sometime, and enjoy investing in both Series I bonds, and EE bonds, and have been buying them to the max each year. The light bulb went on the first time I read one of your articles. I am gradually coming around to TIPS, and I have you to thank for that, also. You do a great job – please keep up the good work.