I am buying in April. A lot of you will disagree. There is no wrong answer.

By David Enna, Tipswatch.com

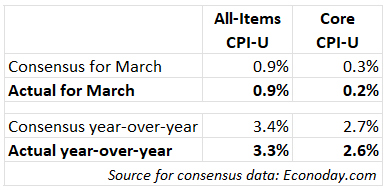

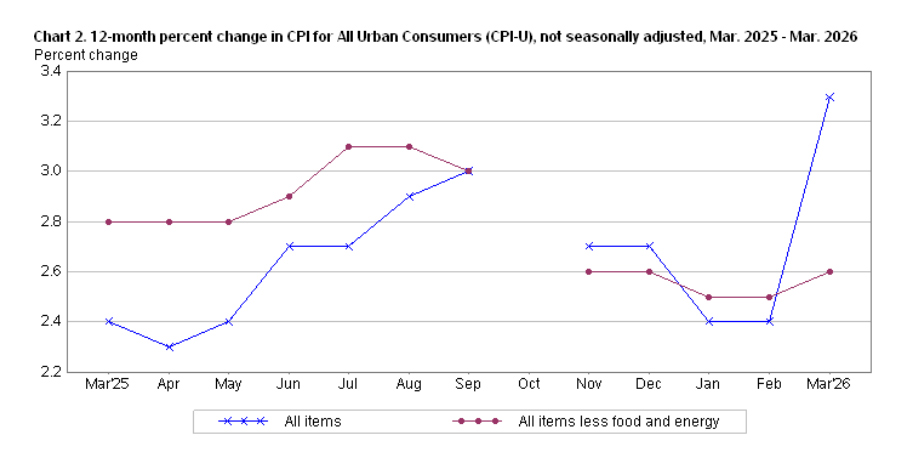

Let’s take a moment to ponder what happened in March: The United States went to war in the Mideast, gas prices surged higher, the stock market fell into chaos (briefly) and U.S. inflation took a huge leap higher.

Way down on our list of concerns was: What’s going to happen to Series I Savings Bonds at the May 1 rate reset? On February 27, I would have confidently told you:

- The variable rate was going to fall to about 2.0% from the current 3.12%.

- The fixed rate was going to fall to 0.8% from the current 0.9%.

- And the composite rate would fall (for I Bonds purchased from May to October) to about 2.81%, down from the current 4.03%.

Wrong. Wrong. Wrong.

But before we get into that, let’s look at …

I Bond basics

I Bonds are U.S. government savings bonds designed to protect your savings from inflation. They offer a combination of interest rates that adjust for inflation, making them a popular choice for conservative investors.

- The fixed rate of an I Bond will never change. Purchases through April 30, 2026, will have a fixed rate of 0.90%, which means the return will exceed official U.S. inflation by 0.9% until the I Bond is redeemed or matures in 30 years. The fixed rate will reset on May 1.

- The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently 3.12%, annualized, for six months. It will adjust again on May 1, 2026, rolling into effect for all I Bonds, no matter when they were purchased.

- The current composite rate is 4.03% annualized for six months for purchases through April 2026.

I Bonds are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also a “gift box” strategy some investors use to stack purchases for future years.

I Bonds have many positives. For example, earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures. Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

The variable rate

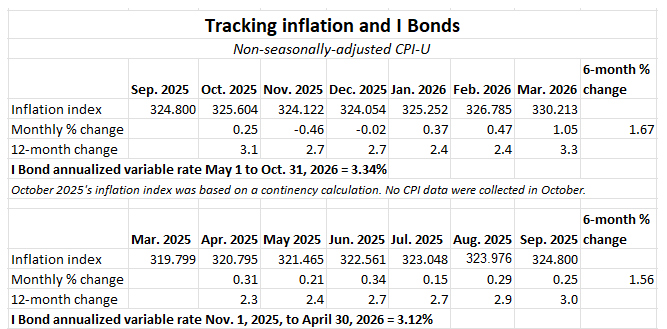

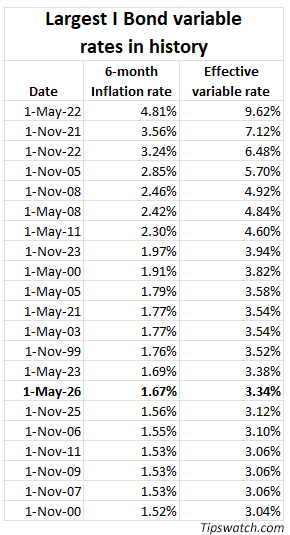

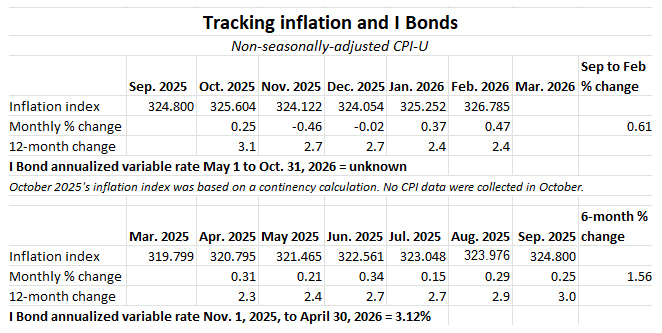

This is set in stone: Because of March’s lofty inflation, the I Bond’s inflation-adjusted variable rate will rise from the current 3.12% to a new rate of 3.34%. This is based on non-seasonally adjusted inflation for the months of October 2025 to March 2026, an increase of 1.67%. The I Bond’s rate-setting formula doubles the six-month inflation rate to create the new variable rate.

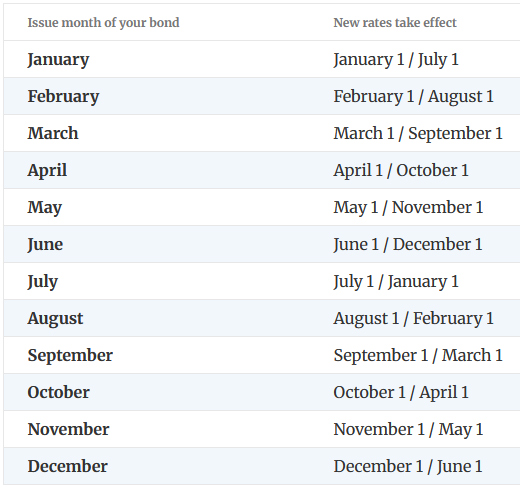

All I Bonds, no matter when they were issued, will eventually get the variable rate of 3.34% for six months, with the starting month depending on the original purchase month. From TreasuryDirect:

It’s important to remember that the new variable rate will apply to all I Bonds ever issued (no I Bonds have yet matured). A purchase in April will get that new, higher variable rate starting in October.

Conclusion: The I Bond’s variable rate will rise to 3.34% at the May 1 reset.

The fixed rate

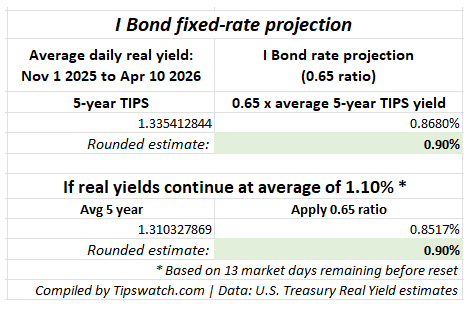

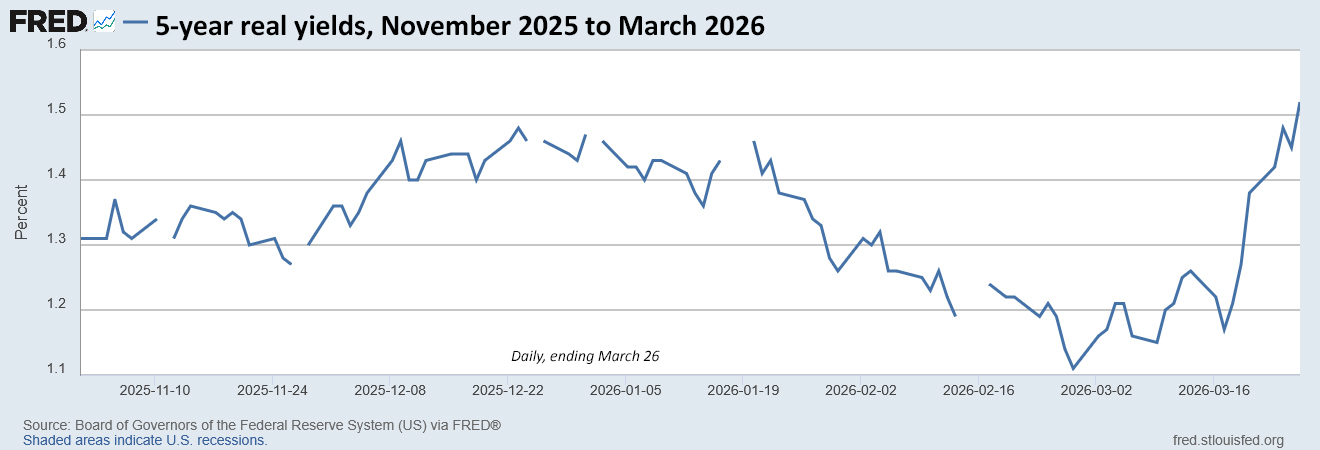

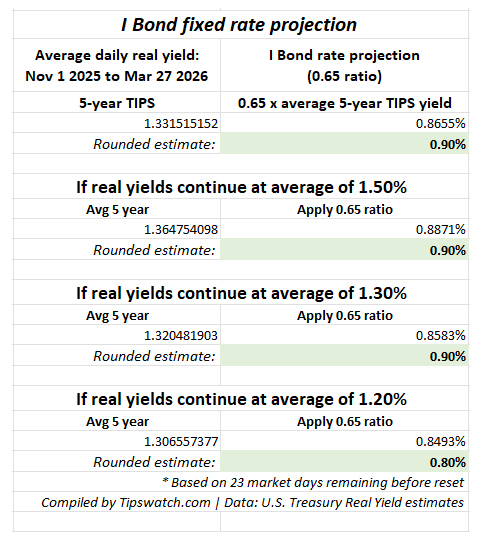

The Treasury has no legal requirement or public formula for setting the I Bond’s fixed rate. The decision is at “the discretion of the Treasury Secretary.” However, we know Treasury tracks trends in real yields and adjusts accordingly. This forecasting formula has worked for the last decade: Take the average real yield of the 5-year TIPS over the preceding six months and apply a ratio of 0.65.

For this reset, we are interested in 5-year real yields from November 2025 to April 2026. There are only 13 market days left before the reset, so we can now get a solid projection:

The formula, which has been accurate for a decade, projects that the fixed rate will remain at the current level, 0.9%. That would be true even if the 5-year real yield — currently at 1.36% — suddenly plummeted to an average of 1.10% for the next 13 market days.

However … This projection is based on 10 years of Treasury history in setting the I Bond’s fixed rate. But the Treasury could change course at any time and we should be aware of that. President Trump’s first-term Treasury followed the formula and has continued to do so in his second term.

Conclusion. It looks highly likely that the I Bond’s fixed rate will hold at 0.90%.

Composite rate

If we assume the fixed rate holds at 0.90% and the variable rate rises to 3.34%, we are looking at a new composite rate of 4.26%, up from the current 4.03%, for I Bonds purchased from May to October 2026. This is based on the formula the Treasury uses to calculate the composite rate:

[Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

If I did my math right, this formula results in the composite rate of 4.26%.

This same annualized composite rate, 4.26%, will apply to I Bonds purchased in April, after six months of earning the current rate of 4.03%.

So we know that an investor purchasing in April will earn 4.03% for six months and then 4.26% for six months, earning a combined rate of 4.16%. An investor purchasing any time from May to October will earn 4.26% for the first six months and then an undetermined rate for the next six months.

Conclusion. The I Bond’s composite rate will rise to 4.26% at the May 1 reset.

The buying decision

Buy now. As I noted at the top, I will buy my full allocation of I Bonds ($10,000 per person per year) later in April. With that decision, I know I will earn 4.16% over the next 12 months, while retaining the permanent 0.90% fixed rate. This is the “sure thing” decision, and I happen to have cash available to make the purchase.

If you are buying in April, I recommend setting the purchase date no later than April 28 on TreasuryDirect to make sure it gets processed ahead of the rate shift.

Buy later. Buying in May would be fine, but most investors who don’t buy in April will hold off investing until at least October 14, when the September inflation report is released and sets the next variable rate, to be reset November 1. At that point investors will also have a very good idea of the next fixed rate.

If you think the fixed rate could be rising in November, it makes sense to wait. Using our standard formula, the 5-year average real yield would need to rise to 1.47% over the next six months to boost the fixed rate to 1.0%. That isn’t unreasonable. So waiting could make sense.

One thing to consider is that the fixed rate announced in November will be available for purchases through April 2027, when the purchase cap resets. Also, realize that a 10-basis-point increase in the fixed rate amounts to $10 a year on a $10,000 investment. It’s not life changing.

Risks of buying now. The fixed rate soars higher in November and you feel miserable about your impatient purchase. (Not likely, but anything can happen.)

Risks of buying later. The biggest risk (also slim) is that the Treasury tosses out its traditional rate-setting formula and drops the I Bond’s fixed rate at the May reset. Another more possible risk, but not as important financially, is that inflation will plummet from April to September and the November variable rate is lower than the current 3.12%.

Short-term investment?

A combined composite rate of 4.16% looks attractive when you compare it to the nominal yields of a 4-week (3.67%) or 1-year (3.70%) T-bill. But remember that you have to hold an I Bond for one year and if you redeem at that point you lose the latest three months of interest.

Not worth it. If you buy late in April and then redeem in April 2027, you will lose the last three months of interest, meaning your total return would be 3.08%. You can do better buying a 1-year T-bill.

Rolling over I Bonds

If you are holding I Bonds with 0.0% fixed rates, you are currently earning a composite rate of 3.12%, and that will rise to 3.34% when the new variable rate kicks in. That’s not bad. There’s no reason to rush to sell these, but if you need to raise cash to purchase 0.90% I Bonds, redeeming and repurchasing makes sense.

I generally encourage people to continue holding I Bonds “until you need the cash.” It’s great to have these savings bonds growing tax-deferred with zero risk.

If you do a roll over, you will owe federal income taxes on the interest earned, and if your withdrawal is more than $10,000 (because of earned interest) you’ll only be able to buy $10,000 in new I Bonds in 2026. Also, time your redemption for early in the month because you earn no interest in the month of redemption.

Gift-box strategy

I don’t think there is a compelling need to “load up” on I Bonds in 2026, but that might change later in the year if the fixed rate surges higher. Although I have used it, I am not a fan of the gift-box strategy, mainly because the Treasury has made no attempt to clarify the rules and in fact has muddied the waters.

Conclusion

When should you purchase? There is no wrong answer. Buying in April or later in the year will likely generate similar financial returns. Getting an I Bond with a fixed rate of 0.90% remains attractive. This is a personal decision, but I still encourage investing in I Bonds as an inflation-adjusted, tax-deferred store of cash.

What are your investment plans? Discuss in the comments section!

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Yes, the tax-free aspect of holding TIPS in a Roth is one of the attractions of that location. Others are…