The newest fund, IBIM, holds just one TIPS, but will expand. I have cautions.

By David Enna, Tipswatch.com

Blackrock’s iShares division in March launched a unique ETF holding just one bond: CUSIP 91282CPU9, a 10-year TIPS that matures in January 2036.

The formal name is the “iShares iBonds Oct 2036 Term TIPS ETF,” with the ticker IBIM. The goal: To track the performance of U.S. Treasury Inflation-Protected Securities maturing in 2036. Later this year IBIM will add a second TIPS, to be issued in July, and then add two more 5-year TIPS to be issued in April and October 2031.

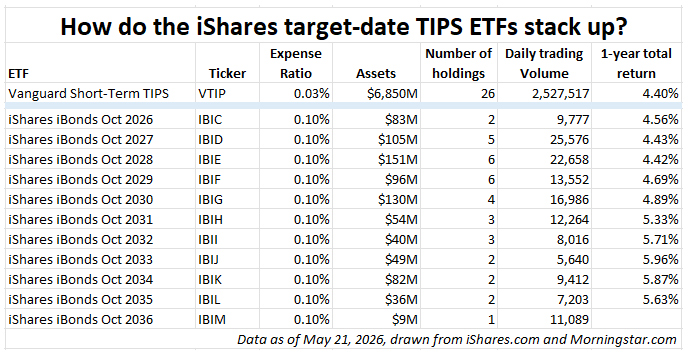

This is the 11th currently existing ETF of this type, holding TIPS maturing in a certain year. Others, such as IBIA and IBIB, have now matured. I have been following these funds for several years, and as time passes, I am easing off my initial qualms: Too weird and too small to be successful.

I had questions: Who is the target market for an ETF that will be holding only two to six bonds until maturity? Why not just buy and hold the individual TIPS? Would these ETFs provide tax-reporting benefits in a taxable account? Are these ETFs targeted at customers of assets-under-management financial advisers (which would possibly increase the cost to investors)?

The iShares suite of defined-maturity TIPS funds currently offers maturities for 2026 to 2036. Ideally, you buy the ETF — intending to hold to maturity — and then after a defined period, it distributes all proceeds and closes down. You can download the prospectus for the new 2036 fund here and the fact sheet here.

iShares has said these ETFs are designed to “mature like a bond, trade like a stock.” These are useful ETFs, I think, especially for an investor looking to quickly build a diversified TIPS ladder out to 2036. These funds should closely track the performance of the underlying TIPS. Here is a comparison of data for each ETF, along with VTIP, Vanguard’s Short-Term TIPS fund, for comparison:

The expense ratios for the iShares ETFs are only 0.10%, higher than VTIP’s 0.03% but quite good for such small funds.

Analysis

These funds are designed to be held to maturity and the asset value will rise and fall with market trends through maturity, just like any other bond fund.

Because the expense ratio is just 0.10%, I really have no problem with using these funds as an alternative to buying individual TIPS. You could quickly build a ladder through 2036 in 15 to 30 minutes.

However, the limited span of maturities means these ETFs aren’t the total solution for building an inflation-protected ladder of investments to cover 20 to 30 years. I raised this point in an April interview with Jason Zweig of the Wall Street Journal. He wrote:

You could use them as a “bridge” to Social Security if you’ll be retiring within 10 years, says David Enna, editor of Tipswatch.com. They aren’t yet a complete solution if you want to protect your purchasing power for, say, the next 30 years.

The size and trading volumes of these funds have increased nicely over the last two years, but still remain small compared to VTIP, an ETF giant. I suspect the ETFs are attracting many investors working with financial advisers. TIPS are complicated, and these funds are much easier to grasp.

The ETF trades as stock, so there is no minimum investment required. The cost of one share of IBIM was $25.13 at the close on Thursday. However, investors could face some bid-ask issues for very large orders. (Note: For a buy order, make sure to place a limit order because of the low volume for these funds.)

Income and inflation accrual distributions

One of the advantages of owning a TIPS to maturity is that inflation accruals continue to build over time, increasing the amount of principal and also increasing the semi-annual coupon payment as the principal increases. An individual TIPS gets the benefit of compounding, even though the coupon is distributed twice a year.

But one of the disadvantages of a TIPS is that if held in a taxable account, those inflation accruals are subject to “phantom” federal income taxes in the current year, even though they are not paid out. Plus, if your account is at TreasuryDirect, you will face the “dreaded 1099-OID,” the cryptic form reporting your taxable accruals.

The ETF plus. These defined-maturity ETFs “fix” the OID issue because inflation accruals will be paid out in the current year, along with the coupon interest. (This is the same way traditional TIPS funds work). That distribution makes these iShares TIPS ETFs more attractive for holding in a taxable account, because it eliminates the phantom income problem.

I assume this also means your broker will provide a single 1099-DIV tax form covering both coupon payments and inflation accruals.

The ETF minus. Distributing the inflation accruals in the current year means that at maturity you will be receiving only the original par value and final coupon payment, since all the inflation accruals would have been distributed. Zweig noted this in his April article:

Like all TIPS mutual funds or ETFs, the iShares funds pay out the inflation adjustment as current income each year. With individual TIPS, the inflation adjustment builds over time as an increase in principal value that isn’t realized until maturity or sale. In either case, the adjustment is taxable outside a retirement account.

In essence, this means if you buy IBIM at around $25 a share this week, in 2036 you are going to get back about $25 at maturity, but you will have earned inflation accruals and coupon payments along the way.

To get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs or another similar product. That could be a problem because of the low trading volume. I don’t own these ETFs, but it appears that Fidelity and Schwab do allow reinvestments, and Vanguard … might.

I have gotten feedback from readers saying they have been able to reinvest the dividends in these low-volume funds. Beyond the cost of any bid-ask spread, that is great news. If anyone has further experience with buying these funds and/or reinvesting the dividends, please provide the information in the comments section.

Do you need cash flow? To recap, these ETFs offer a cash-flow solution if held in a taxable account, with coupon interest and inflation accruals being paid out (and taxable) each year. If you don’t need the cash flow and are going to reinvest the dividends, they would work better in a tax-deferred account.

Thoughts

I buy individual TIPS with the intention of holding to maturity, so I already own CUSIP 91282CPU9 maturing in January 2036. But I can see the appeal for investors looking for a simpler way to invest in TIPS, especially in a taxable account.

The expense ratio of 0.10% is very good, especially if you can make your trades commission-free. But I do warn against using these ETFs in an assets-under-management account, which could wipe out 1% or more of your annual earnings. And in fact, I suspect these ETFs may have been designed for AUM financial advisers who really don’t understand TIPS (a lot of them don’t).

In summary, these target-maturity ETFs are a good investment for cash flow, would work well in a taxable account, and I really have no problem with them.

A new PIMCO ETF

On April 6, the investment firm PIMCO launched a new-fangled inflation-tracking ETF dubbed PIMCO Inflation PLUS Active ETF (PCPI). The press release says:

PCPI aims to provide investors who are concerned about rising inflation with a more direct hedge, lower volatility and limited interest rate risk versus traditional Treasury Inflation Protected Securities, known as TIPS.

PCPI is designed to limit interest rate risk and add incremental return potential through active management. It seeks real returns by investing primarily in short-term TIPS and other inflation-linked securities, and by actively managing the portfolio as market and inflation conditions change.

Sigh. This new fund might be fine, but I grit my teeth at the term “active management.” We are talking about, at most, seven TIPS and Treasury holdings? The expense ratio is 0.25%, which is eight times higher than VTIP’s 0.03%. The duration is defined as “ultra low” at 0.5 years, versus 2.5 for VTIP.

This ETF has very little trading history and I really don’t understand the premise. When a company uses the term PLUS in the ETF name in capital letters, there is something going on. Here is the prospectus if you want to dive in.

The ETF’s assets currently total $55 million, versus $6.8 billion for VTIP. This ETF is too new to draw any conclusions, but I would definitely shy away from any fund this new, this small, and this unproven.

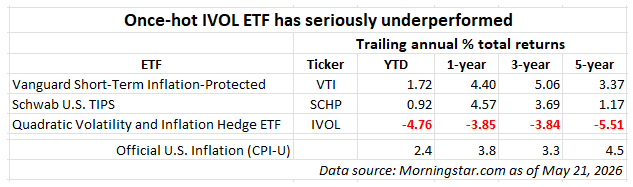

The IVOL lesson

Back in the fall of 2020, when I was still writing for SeekingAlpha, I was getting a lot of questions about a new ETF with a tongue-twisting title: the Quadratic Interest Rate Volatility and Inflation Hedge ETF. Its ticker: IVOL.

The ETF’s creator, Nancy Davis of Quadratic Capital, was hailed as an innovator for this fund. Barron’s named her one of its top 200 Women in Finance in March 2020. But for me, IVOL was never particularly attractive. It was very new, with just a year of trading history. It was a fixed-income fund with a 1% expense ratio and a complex hedging strategy I couldn’t understand.

IVOL was investing 85% of its assets in SCHP, Schwab’s U.S. TIPS ETF, my favorite full-maturity-spectrum TIPS fund. On top of that, it was overlaying hedging strategies that sought to benefit from interest rate volatility. (Sound the alarms.)

IVOL had a sensational year in 2020, with a total return of 14.6% versus SCHP’s 10.9%. Readers began telling me: “This strategy works!” But In 2021, as both short- and long-term interest rates stabilized at very low levels, IVOL under-performed its two TIPS fund competitors by a wide margin.

Here are the total return results for IVOL over the last 1-year, 3-year, and 5-year periods:

Instead of looking for “new-fangled” solutions, an investor could have done much better by investing in tried and true TIPS ETFs like VTIP and SCHP. IVOL has grossly under-performing one hugely important metric: U.S. inflation.

Conclusion

Beware of the “new thing.” I don’t think the newly launched PIMCO fund is trying to push the envelope, so it may actually do fine investing in very short-term TIPS. If it is successful, let’s hope the 0.25% expense ratio begins to decline.

On the other hand, the iShares target-date TIPS ETFs have earned a look for investors who need a simplified way to buy TIPS.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I find the ishares target date tips funds useful for investing the coupon payments from my individual tips holdings with the same maturity.

in 2024 I built a ladder using IBIB, IBIC, and IBID to take me to social security. I liked the convenience of re-investing the dividends because I didn’t want/need the incremental interest payments. Since they matured in October I still had to invest at maturity until the next calendar year but money market funds have done pretty well so that hasn’t been an issue.

one thing to be careful of is the price spread above NAV. Since you are getting NAV – fees at maturity you are giving away basis points if the price is above NAV.

A concern for TIPS, TIPS funds, and iBonds is that the government may underestimate inflation such that the “real” yields aren’t what they appear. New Federal Reserve Chairman Kevin Warsh now advocates a “trimming” model which would bring the official inflation number from 3.8% down to 2.3% just by redefining how it is calculated.

https://www.reuters.com/markets/us/fed-chair-warshs-preferred-inflation-measure-is-cooling-big-pinch-salt-is-2026-05-28/#:~:text=Year%2Dover%2Dyear%20inflation%20by,down%20from%202.4%25%20in%20March.

“so Dallas Fed researchers compensate by lopping off more high-inflation items than low-inflation ones.”

Dontcha just love it?

To borrow Trump’s own physical description of Warsh at the time of nomination, it’s an inflation measure “from central casting.”

Let us hope the other fed governors/market committee members use their own judgment.

The “trimmed mean” debate refers to the way the Federal Reserve judges current inflation to set future interest rates. It has no direct connection to the way TIPS inflation accruals are calculated. Accruals are based on non-seasonally-adjusted CPI. If this trimmed mean was used to justify lowering interest rates today (it won’t be), the result very likely could be higher CPI inflation.

I am at the age where I need to start shifting some retirement savings out of equities. TIPS are appealing to me as I think we are and will be in a high inflation environment for some time and traditional bonds may have a negative real yield. My first choice would be to build a TIPS ladder, but all of my retirement savings are in tax advantaged accounts and I need to hold the bonds in my 401k. My employer’s plan allows purchase of ETFs and mutual funds, but nothing else – so a TIPS ladder is out.

I cant bring myself to buy a long duration TIPS ETF as when interest rates rise I will loose money. I cant bring myself to buy a short term TIPS ETF as when inflation increases the fund will be forced to reinvest in TIPS with negative real yields (and I’ll loose money). It seems these funds, if held to maturity, fulfill the promise of TIPS: no loss of principal and a guaranteed real return and would enable me to hold the asset in my 401k. In fact, it is what Google AI recommended when I expanded the constraints above. For now, I’m still researching (which is why I am at this site).

I faced the same situation before my “forced retirement.” All my tax-deferred assets were in a 401k with limited options. After retirement, I moved the money out of the 401k and into a traditional IRA. With any TIPS fund or ETF you are going to face potential loss of principal if real yields rise sharply. A shorter duration fund like VTIP is going to be less volatile. Its total annual return over the last 10 years was 3.18%, versus 3.4% for U.S. inflation and 1.69% for the total U.S. bond market.

Meanwhile, the Treasury Department’s top lawyer resigned in a hurry after the slush fund was made official.

But you can entrust your money to the promises of the those people. You can be certain that there’s “no risk” to USG obligations.

Seriously – everything is fine.

There’s been overt pushback on this– from Republican senators– on the slush fund as well as the President’s ballroom and “settlement” with the IRS. I just read on Bloomberg that 30 former US district judges (both Democrats and Republicans) have urged a sitting US Florida district judge to investigate possible “fraud” in the IRS settlement. Fingers crossed that there are still enough ethical officials in our government to warrant the long standing trust we place in loaning the US government our money.

Well, don’t hold your breath on Phil Alito, that’s all I can say.

This is the elephant in the room. Nobody wants to say it. Nobody wants to believe it. Justifications abound – it can’t happen because it would be catastrophic, etc. Ignore the risk of US government debt at your own peril.

I can’t gauge the risk, but it is not non-zero, as it was for my entire life.

Rocky, I have to agree there is more than zero risk in U.S. government debt, and the problem gets worse month by month. No credible politician of either party is focusing on this ballooning debt, and the danger is the greatest in my lifetime. The problem is … if U.S. debt collapses, there goes the entire economy. More likely, borrowing costs will continue to rise.

In the history of the world that I have read, when a leading entity’s national debt gets unsustainably high two or three solutions come around.

The usual options are to Raise the public taxes or let the inflation turn the debt into a lower nominal liability or… start some wars (sometimes after an ‘austerity effort’)

It appears that any true Austerity efforts seem to lead to that most horrible third option as ‘they’ try to place blame for the fiscal crisis on some scapegoat.

This is perhaps an argument for holding more in international bonds. I am a self- directed investor and yet Vanguard provides me with a “portfolio watch” function which provides automated feedback when something in my asset allocation looks out-of-whack. For some time now they have been telling me to consider buying more international bonds. The automated advice reads something like “allocating 20-50% of your bond portfolio in currency hedged international bonds may reduce the volatility of your bond portfolio..” I haven’t been much interested because the yields on developed country bonds (think Germany, France, Japan) have been well below that of the US. However considering the discussion above perhaps that deserves a re-think. When you look at the target date retirement funds Vanguard offers, international bond holdings for those either in or near retirement range from 11-15%.

Instead of these funds, I wish someone would start offering the TIPS version of STRIPS. That would solve the reinvestment problem.

I’ve been trying to understand how a TIP fund is supposed to protect principle compared to owning until maturity a TIP bond ladder directly.

It seems like your principle in the shares of a TIPs fund may or may not ever be cashable at full value if rates go higher or stay higher for years after you buy a share.

There seems to be no defined end point of return of principle nor the guaranteed return of inflation adjusted invested principle as you would receive with the TIP bonds owned directly in your own account.

What are the benefits of a TIP fund vs TIP bonds you own directly with defined maturity dates?

I would always prefer to own the individual TIPS instead of a TIPS fund. But I do own BND, the total bond market, so I am not opposed to bond funds. Because of the unique certainty of an inflation-adjusted total value at maturity, TIPS are ideal for stacking in a ladder with a defined-year of maturity. TIPS funds are open-ended and easier to grasp, plus eliminate the OID quirk of individual TIPS. A lot of Bogleheads swear by the idea of maturity-matching your fund to a future need, but the bond market might not cooperate.

You wrote: “To get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs….”

I’m just wondering if that process introduces an element of reinvestment risk with the ETF that you don’t have with the bond, since the price might be higher later on when it comes time to reinvest the inflation-accrual. With the TIPS bond, you only purchase it once, and from then on it accrues automatically.

It does introduce uncertainty, but not huge uncertainty. The variations could be negative, or positive. But the return of the individual TIPS is more certain.

Whats really curious with Warsh the new fed chair, and his possible ideas/policies , that are out there, seems golden bullets, no one seems to bring up the actual word “inflation” in the discussions or even cares to guess which sectors might do well. I seemed to read that interest rates will come down, and bonds get hammered. Since Tips are based on an actual formula has he found a way where inflation will not show up in the CPI but its really there? Im 78 and have no patience for Treasury Direct Auctions, etc. That game is for young men. So I would go the ETF route. Some of you need the 20 foot ladder, where I only need about an 6 or 8.

Here are a couple data points for these ETFs:

First, IShares publishes an annual update to their case study on how matured defined term bond ETFs did over their history. The latest one is here: (https://www.ishares.com/us/literature/presentation/ibonds-series-case-study-en-us.pdf

Looking at the charts, Treasury ETFs (nominal and TIPS) basically matched their initial YTM while High Yield and Muni’s had greater variance.

Second, IShares launched a new TIPS ETF that has less than a year duration – ICPI. That could be helpful for folks who are duration matching with other TIPS ETFs and/or want some inflation protected in short term cash. I looked at how its index (ICE U.S. Treasury 0-1 Year Inflation Linked Bond Index) did against a nominal Treasury index of the same duration and the inflation linked one did better. The ETF has done better than SHV since inception but had higher volatility.

Great information, thanks.

Vanguard does not permit reinvestment on an earlier iShares TIPs ETF (IBIC) that matures this year. You could manually reinvest in VTIP.

Good to know, thanks. A few years ago I planned to do a “test case” investment in IVOL vs SCHP and then realized Vanguard would not allow IVOL reinvestments because volume was too low. So I ditched that plan. (Good for me, it turns out.)

I don’t understand VTIP. It looks like it’s returned 1.9% over the last year (nominal). Is that due to interest rate fluctuation? If I buy $1k today, I have no idea what it will be worth at any point in the future. It all depends on interest rates, right? So it doesn’t really seem to me like it protects against inflation. Am I missing something?

Thanks!

When you look at any TIPS fund, you have to look at total return, including dividends. VTIP’s total return over the last year was 4.24%, according to Morningstar. But it is also true that when you buy any TIPS fund or ETF, you cannot predict the value when you sell, because the investments have rolling maturities. If real yields rise sharply, the value to VTIP will decline. VTIP is a fairly low-volatility ETF, but its value will fluctuate.

Speaking of inflation (in general)…

The University of Michigan consumer sentiment data has the mid-term (5-10 year) inflation expectation at 3.9%, with an expected rise to 4.8% for the short term.

That mid-term expectation concerns me — especially if it ratchets up yet further — as businesses will start to use that expectation to set future pricing, given their expectations of the costs of their inputs (labor, etc.) going up just the same. Sure, it’s not the 9% mid-term expectation of 1980 <shudder>, but you’re still talking at prices rising 2.5 – 3x the normal rate compared to the historic 2% target the Fed has historically tried to maintain.

Might this be the first whiff of stagflation? It functionally preceded me (or I was too busy watching Sesame Street), but I’m aware that stagflation tends to self-perpetuate and feeds on itself unless very overt and unpopular policy decisions are made to wrest things back under control. Or that incorrect policy decisions (see: Japan) can let that economic stagnation fester for decades. Simply put, “entrenched inflation” is a real beast that can’t be defeated quickly. It takes at least a chunk of painful years and smart, consistent policy to really take it down.

Thoughts?

A return to late 1979 to late 1985 interest rates would be “interesting” for those adding treasuries to their portfolio, but only if some head policymakers are willing to “fall on their sword” ala Volcker did to stop the bleeding.

I remember buying 8% bank CDs and the price of gas doubled quick. Troubles in the same place as now in the middle east.

Indeed. Bank of America just published a survey where 62% of global fund manager respondents expected 30Y Treasury rates to hit 6% sometime this year.

That’s where my head’s been at. Having spent my 20s in a hedge fund (in research, on model dev.), I’m acutely aware the impact that’ll have. Particularly the “fantasy camp” portion of equity markets eating the pavement first as the value of future dollars is quickly eroded. 5-year and 10-year projected valuations tank hard as inflation ramps up, compared to the past 15 years.

Obviously it will require firm, measured policy implementation to correct (BIG if), but I wonder if I’ll have the opportunity of those prior to my birth where there’ll be a window where I add high-yield treasuries to my SE 401K and sleep tight. As with a proper correction, I could secure equity market-like returns by merely sitting on my hands for 10 to 30 years, knowing that portion of my assets shrugs its shoulders at market volatility.

Chester K. Goofington (great user name!): “A return to late 1979 to late 1985 interest rates would be ‘interesting’ for those adding treasuries to their portfolio . . .”

ThomT: “I remember buying 8% bank CDs . . .”

I remember the early 1980s, when my wife and I paid points for the privilege of being “allowed” to get a home mortage at “only” 13.5% interest.

If we’d been thinking solely of money, we should have taken our house downpayment, and all the other cash we could lay our hands on, and bought 30-year Treasury bonds. But in the climate of the time–i.e., inflation and Volcker Fed rates–financial markets feared things might get even worse. And we were so tired of renting, and had just reunited after a job-related geographical separation, that we just wanted the settled life of a house.

Yes, we did refinance, more than once, after rates began to drop, drop drop, because the savings on interest far outweighed the refinancing charges.

But, as a financial memory from the perspective of 2026, the whole experience seems quite surreal–as indeed it also seemed at the time.

“Why not just buy and hold the individual TIPS?” That’s the best question.

If the various central banks and sovereign funds continue to sell heavily as reported that they have been recently, it could make rates go a good bit higher.

But I do buy to hold, not trade, but I also keep replenishing ammo to be ready and handy in MMFs and short CDs in case yields get wildly better.

I’m happy with the real yield rates I’ve gotten recently on TIP bonds.

What do you see as the advantage or disadvantage of holding a tips ETF maturing in a certain year in a traditional IRA?

I’d say the optimal route is buying and holding an individual TIPS to maturity. The ETF route, while acceptable, will bring a small annual expense plus some complexity as the ETF purchases additional TIPS maturing in that year.

In my 401k the only TIPS option is a TIPS mutual fund. Individual TIPS are unavailable. However, one can buy target-date TIPS ETFs via a brokerage window.

These target duration and laddered TIPS products have sparked my interest because of the legwork and tax issues involved with buying and holding individual TIPS in a taxable account. I have wondered about the investor experience for an investor who purchases and holds a fund like IBIM today (with a real yield around 2%) and how that investor is impacted by future fund flows and additional purchases by the fund. Also, the 10 year max target duration does not help someone wanting to build a 20 to 30 year ladder in a manner akin to purchasing individual bonds (via something like tipsladder.com). LIFEX and also Northern Trust with its distributing ladder (TIPS-based) ETFs are interesting but come with more complexities (e.g., fees, similar questions about investor experience with flows, etc.) and also closure risk (i.e., these funds have had difficulty generating AUM).

If you are considering purchasing an iShare defined-maturity fund through E*trade from Morgan Stanley be aware that they charge your account a “mandatory reorganization fee” when the fund liquidates upon maturity. I have owned numerous series of iShare defined-maturity funds through Schwab and Fidelity and have never been charged a fee at maturity. Needless to say, I was surprised by what E*trade characterized as a service fee. Some service! A complaint to FINRA when nowhere.

Re: “When a company uses the term PLUS in the ETF name in capital letters, there is something going on.”

I view the term “Plus” in an ETF or mutual fund name as a sort of Orwellian red flag that the investor may experience a “Minus” in the form of extra fees allegedly necessary to seek the “Plus”–because, of course, the fees are guaranteed to the investment company in advance but any particular sur”plus” return to the investor is not.

So much of the financial “industry” involves taking simple vanilla things and larding them up with extra-cost sparkles that most people could, and should, do without.

iShares target-date TIPS ETFs may be the solution to having the cash needed to pay taxes during high inflation years on a portfolio comprised mostly of TIPS (a 30 year TIPS ladder, for example). This would prevent you from needing to sell a TIPS at a time of likely high interest rates. You’re giving up some portfolio yield in exchange for protection from forced sale losses.

I bought IBIK (Oct 2034) through Fidelity in May 2024. I treat this as a regular part of my TIPS holdings alongside individual bonds.

“To get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs or another similar product” … “I have gotten feedback from readers saying they have been able to reinvest the dividends in these low-volume funds.”

In a taxable account you still face the tax man for the gains of the current year impacting what is available for reinvestment elsewhere, or your wallet if reinvested directly into the same ETF, correct? So I don’t really see the phantom income issue being abated unless it is as a tradeoff to losing a portion of the inflation protection of keeping the gains invested.

Any updated thoughts on VTP (Vanguard Total Inflation-Protected Securities ETF)?

This is a new ETF, and it is a full-spectrum maturity ETF like SCHP. I am guessing it will perform closely in relation to SCHP and Vanguard’s Admiral mutual fund of the same type: VTAPX. I wrote about VTP here: https://tipswatch.com/2025/07/11/vanguard-launches-a-new-full-term-tips-etf-vtp/. It seems fine if you want the full range of maturities, which will be more volatile (up and down) than VTIP.

I think that VTAPX is the mutual fund version of VTIP, not VTP.

You are correct. The mutual fund is VAIPX.

If you eliminate interest rate risk, how well do nominal bonds handle a period of high sustained inflation? According an analysis by TSP Folio, the TSP G Fund (which offers mid- to long-term Treasury yields with no interest rate sensitivity) would have tracked inflation pretty well between 1972 and 1983. https://www.tspfolio.com/tsp-g-fund-vs-inflation. If that analysis is to be believed, I’m wondering whether the G Fund is a “good enough” alternative to a TIPS ladder for someone who wants inflation protection but has some possible spending needs that make him uneasy about locking in to a hold-to-maturity TIPS strategy.

The danger with any continued bet on short-term Treasury nominals is that the Federal Reserve will relaunch quantitative easing and force short-term rates well below inflation. In that case the short-term rates could be close to 0.0%. However, any longer-term holdings you purchased before the Fed acted would get a big boost.

Nominal Treasurys protect against deflation. TIPS and I Bonds protect against inflation. And in reality, the returns could be similar, except in periods of unexpected deflation or unexpected inflation (which we are seeing today.)

The G Fund is vastly superior to any bond fund someone outside the TSP could buy. The funds interest is calculated monthly by taking the average yield of all outstanding US treasury notes and bonds with a maturity of 4 years or greater. Interest is credited and compounded daily. Zero interest rate risk, never lose a penny since the securities issued to the TSP are not marketable. The share price of the G Fund cannot go down.

Ah yes, I remember many times in the past wishing I could invest in that fund.

David – you say you wish you COULD invest in G Fund. But if you could, WOULD you? In other words, would you consider it an acceptable alternative to a TIPS ladder if you wanted a bit more flexibility in the timing of when you would spend the money? The (pretax) inflation protection offered by the G Fund is certainly not as rock solid as holding individual TIPS to maturity, but would you view the G Fund alternative as “good enough”?

No, it’s not an alternative to TIPS and I Bonds. But it would be a great cash-alternative holding. (I don’t know the rules on withdrawals, however.)

How does the ETF payout the inflation accrual of the underlying TIPS? The TIPS principal inside the ETF increases, but does not provide any cash to distribute.

These ETFs do stockpile some cash (but it is hard for me to tell how much). The managers of VTIP must do the same thing, but they have a lot of flexibility since they have maturing TIPS each year.

They sell TIPS from their portfolio to pay the OID portion of the dividend. Check out the turnover ratio on these funds; it’s astonishing for funds with only 2-4 holdings. P.S. The trading costs are paid by the shareholder and not included in the headline expense fee.

Hi David,

As always, excellent analysis. One minor correction, in the table where you compare VTIP, SCHP, and IVOL, you havw VTI ticker instead of VTIP….best

I am seeing VTIP. I corrected that error before publication but the “error ghost” must linger on.

Thanks for sharing your views on these iShares target maturity ETFs. They were especially attractive to me because I can use them to fill out my bridge to SS in a retirement account where I can purchase any ETF, but not individual TIPS/bonds. The 0.10% ER isn’t ideal, but it seems reasonable enough given the relatively short term that I’ll be holding them.

I have a question about ETFs like IBIM. Say I buy into the fund at a time the TIPS held by the fund have a 2% real yield (ignoring for this comment the small fund fee). Then, 3 years later a bunch of investors invest in the fund at a time when the TIPS to be held by the fund can be purchased at a 1.4% yield. When the fund takes that new money and buys the new TIPS, won’t that drive my real yield at maturity down below the 2% I expected when I first invested?

If real yields decline, those investors would be paying more per share than you did, and getting a lower real yield than you. The more complicated question is what happens when this ETF purchases a new 10-year later this year and two more in 2031. Does it sell some TIPS to buy the new issues? That could be a negative, or a positive.