‘Talking about talking about’ is a signal that real yields could be rising

By David Enna, Tipswatch.com

Jerome Powell, chairman of the U.S. Federal Reserve, made some significant statements last week with the potential to shake up both the stock and bond markets. But one response to a question at Wednesday’s news conference rang alarm bells for me:

“But you can think of this meeting that we had as the talking about talking about meeting, if you like. And I now suggest that we retire that term, which has served its purpose well, I think.”

Translation: Powell said, in essence, that the Fed is now willing to talk about future tapering of its aggressive program of buying U.S. Treasurys and mortgage-based securities in support of the U.S. economy. We don’t know when the bond buying will end, or how quickly it will end, but it is now on the table. In addition, increases in short term interest rates could begin in late 2022 or 2023, a year earlier than had been expected.

I’ve been thinking about how this “tapering” could affect the real yields and values of Treasury Inflation-Protected Securities. And I think the model to look at is a similar “talking about talking about” period from December 2012 to December 2014, when TIPS yields rose quickly from ultra-low levels. And all of this happened well before the Federal Reserve actually began tapering its bond buying or increasing short-term interest rates. We could be heading into a similar market trend for the remainder of 2021 and into 2022.

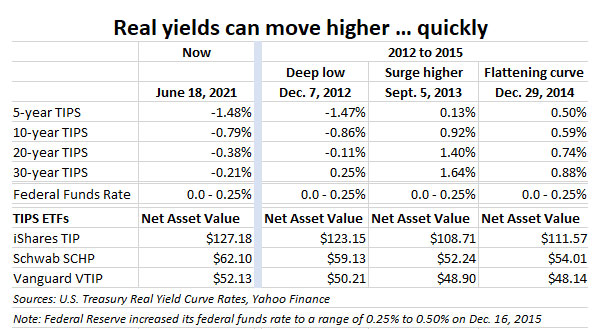

Here’s a look at our current market for TIPS compared with the December 2012 to 2014 period, showing that real yields today are very close to those of early December 2012:

Here’s the important historical context to this chart: Ben Bernanke, then the Fed chairman, had hinted vaguely that tapering of bond buying could begin in 2013, but there was no official announcement until June 19, 2013. By that time, the real yield of a 10-year TIPS had already surged from -0.86% on Dec. 7, 2012, to 0.29% on June 19, 2013, an increase of 115 basis points in only 7 months.

Here is information from Wikipedia on this tapering decision:

On 19 June 2013, Ben Bernanke announced a “tapering” of some of the Fed’s QE policies contingent upon continued positive economic data. Specifically, he said that the Fed could scale back its bond purchases from $85 billion to $65 billion a month during the upcoming September 2013 policy meeting. He also suggested that the bond-buying program could wrap up by mid-2014.

The stock markets dropped by approximately 4.3% over the three trading days following Bernanke’s announcement, with the Dow Jones dropping 659 points between 19 and 24 June. … On 18 September 2013, the Fed decided to hold off on scaling back its bond-buying program, and announced in December 2013 that it would begin to taper its purchases in January 2014. Purchases were halted on 29 October 2014 after accumulating $4.5 trillion in assets.

By September 5, 2013, the 10-year TIPS real yield had soared to 0.92%, a remarkable increase of 178 basis points in less than 10 months. But the actual tapering didn’t begin until December 2013. The psychology of tapering moved the bond markets, not the actual deed. And throughout this entire time of surging real yields, the Federal Reserve held its federal funds rate in a range of 0.0% to 0.25%. The first rate increase didn’t come until Dec. 16, 2015.

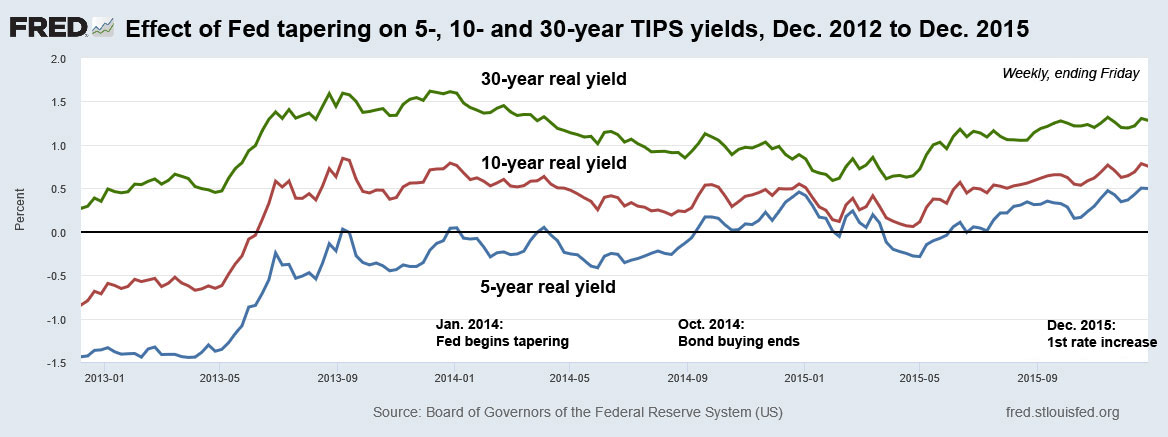

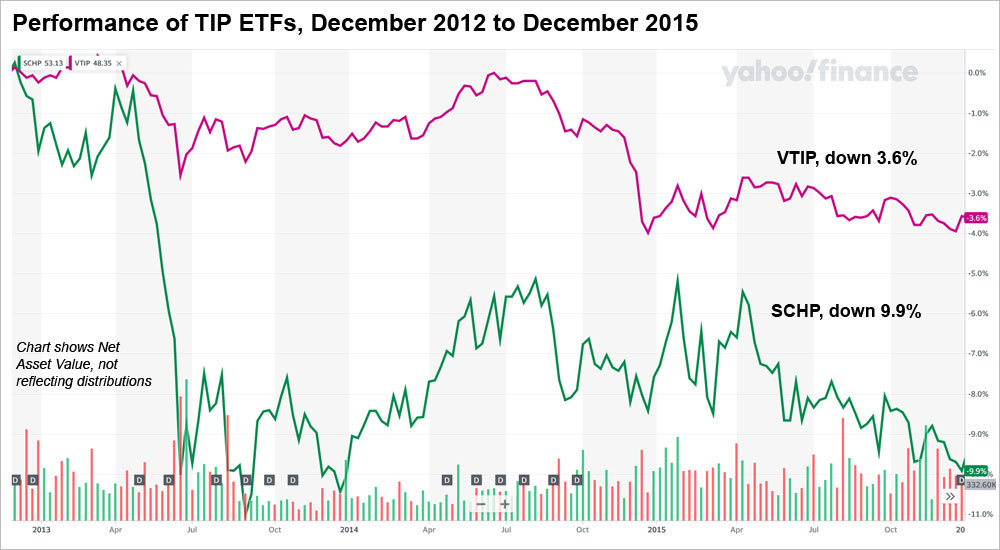

And that is why Chairman Powell’s “talking about talking about” statement is so significant: It is setting in motion a psychology of increasing interest rates, even if the Fed does nothing in coming months. Here is a chart showing TIPS real yields from December 2012 to December 2015, showing that the strong surge higher happened well before the Fed actually began tapering, and nearly 2 years before the first increase in short-term interest rates:

Notice that by December 2014, after the bond buying had ended but a year before short-term interest rates began increasing, the yield curve was flattening in anticipation of future rate increases.

What did that mean for TIPS and TIPS funds?

When real yields rise (or fall) more than 100 basis points, that will have a significant effect on the value of individual TIPS and TIPS ETFs and mutual funds. For a fund like the TIP ETF, which has a duration of 7.53 years, you can expect the net asset value to fall (or rise) by 7.5%, independent of any inflation adjustments.

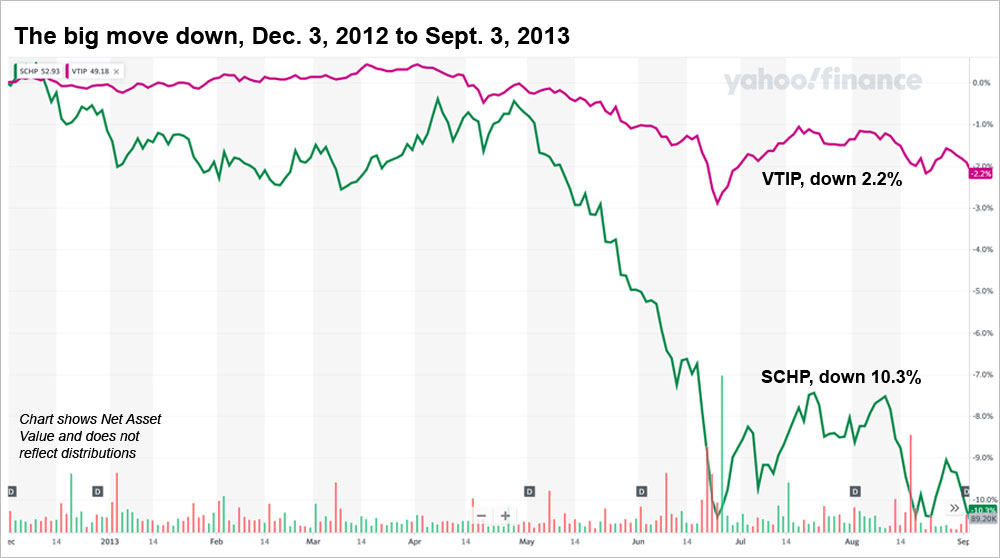

And that is what happened. Here is a chart showing the how the net asset values of my preferred TIPS funds — Schwab’s full-maturity SCHP ETF (duration of 7.4 years) and Vanguard’s VTIP, which invests in 0- to 5-year TIPS (duration of 2.6 years) — performed during the surge in real yields from December 2012 to September 2013:

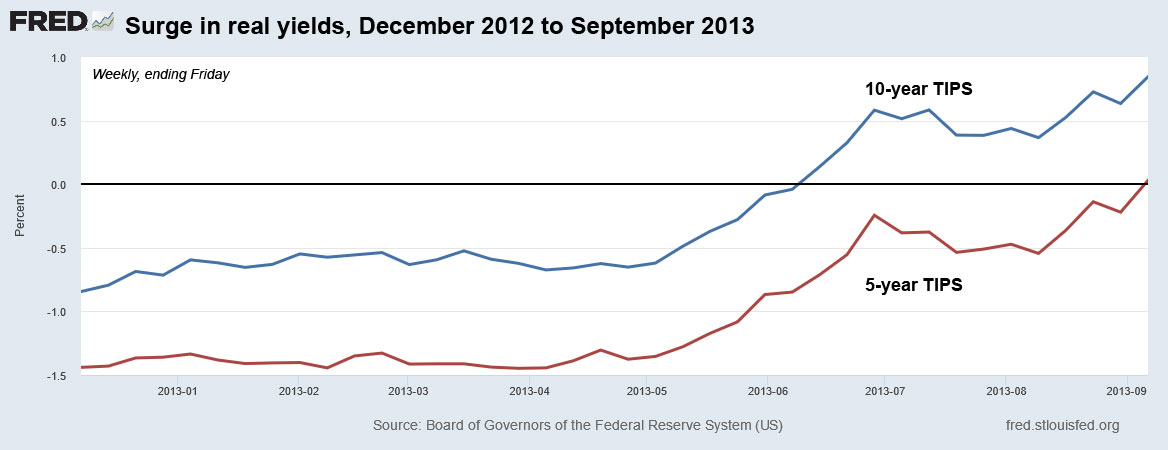

For context, here is how 5- and 10-year real yields surged higher during this period, with the obvious correlation being that higher yields create lower bond values:

After the Fed acted, the yield curve flattened …

This next chart shows the extended period of December 2012 to December 2015, which captures the Fed’s end to bond buying in October 2014 and the first interest rate increase in December 2015. VTIP, the shorter-term TIPS fund, had been performing well for most of 2012-13 and into 2014, but the signaling of higher short-term interest rates started flattening the yield curve, hurting VTIP’s performance. In other words, shorter-term TIPS yields began rising faster than longer-term real yields, and so VTIP took a bigger hit in late 2014, relatively speaking.

Nevertheless, it is clear that VTIP is the preferred TIPS investment in times of rising real yields, because the shorter duration holds down potential losses.

Should you sell out of your TIPS funds?

I can understand the question. TIPS mutual funds and ETFs are a bit more volatile than your typical broad-based intermediate bond fund. They are focused on one esoteric security and hold fewer than 45 issues, generally. Real yields can often move in the opposite direction as nominal yields, at least for short periods of time.

But the key advantage of TIPS and TIPS funds is that they offer a return that is adjusted for official U.S. inflation. That means even if the net asset value declines in coming months, surging inflation could balance off that decline. The outlook isn’t as bad as it might look, assuming inflation continues at a pace of 2.5% or higher.

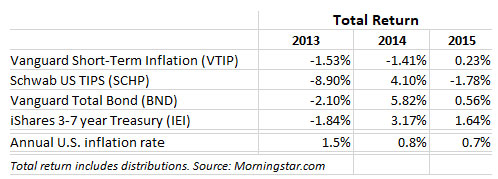

Here’s a look at the total return (including distributions) for four big intermediate term bond funds for the years 2013 to 2015:

Schwab’s broad-based TIPS fund, SCHP, did take a hard hit in 2013, but recovered well in 2014. VTIP also stumbled, but not too badly because of its short duration. But here is the key: Notice the very low inflation rates of those years, averaging 1.0% a year. Our near-term future, transitioning into tapering, could see higher inflation rates, maybe much higher. So TIPS funds seem like a “hold.” My personal preference (for what that’s worth) is to overweight VTIP vs. SCHP, but I will continue to own both.

(If the yield curve seriously flattens over time, longer-term TIPS could end up out-performing shorter-term TIPS, so that would benefit SCHP over VTIP. That is what happened in 2014, after Fed tapering was in progress.)

One other thing: I’d be willing to see some of my fixed-rate investments lose some value, if that meant interest rates would “normalize,” having nominal rates above the rate of inflation. So maybe a 5-year CD would pay a paltry 3.0% again and a 10-year TIPS could get a real yield of 1.0%.

Conclusions

My gut feeling is that the Fed will soon start “backing off” on its tapering hints, especially if the U.S. stock market declines sharply. (The backing-off phase is totally predictable, and expected.) Tapering is coming, but it could be as long as a year away. The Fed seems to like to make “big decisions” at its December meeting, so that will be one to watch.

Powell’s statements this week have already had the effect of strengthening the U.S. dollar, which will in turn help hold down surging inflation. If inflation cools off dramatically later this year, that will take pressure off the Fed. It will not need to move quickly.

But Powell was clearly setting the stage for higher inflation expectations at his Wednesday news conference:

“Inflation has increased notably in recent months. The 12 month change in PCE prices was 3.6% in April and will likely remain elevated in coming months before moderating. Part of the increase reflects the very low readings from early in the pandemic falling out of the calculation, as well as the pass through of past increases in oil prices to consumer energy prices.

“Beyond these effects, we are also seeing upward pressure on prices from the rebound in spending, as the economy continues to reopen … raising the possibility that inflation could turn out to be higher and more persistent than we expect.”

We are entering an uncertain period for investors in Treasury Inflation-Protected Securities. Real yields could be rising. That will be great for future investors; not so great for TIPS traders and holders of TIPS mutual funds.

But … We have to admit that the economic environment of 2021 is “different” from 2013, and this Fed is much more willing to accommodate economic growth and the wealth effect from stock market gains. It will take months of sustained, higher-than-expected inflation — as we saw in February, March, April and May — to force Fed action. Inflation will be the key.

The key point is: It isn’t the Fed actions that drive the markets. Instead, it is the Fed’s signals. And this week we got a huge signal that tapering is coming.

Take a look at the 2013 ‘taper tantrum,’ and what followed …

- 2013: A year of surging real and nominal yields

- 2014: The deck was stacked against TIPS funds

- 2015: The Fed actually did something!

- 2016: Inflation rises; TIPS out-perform the overall bond market

- 2017: ‘The calm before the storm’

- 2018: Did the Federal Reserve go too far?

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David,

If moderate to high inflation becomes a prolonged phenomenon (i.e. 5%+), are there any provisions in I Bond legislation to make the bonds callable? In that case investing in I Bonds may have been a fool’s errand since the Government won’t honor the guarantee. I won’t even ask you to speculate what the government would do about I Bonds if the US experiences Weimar Republic type hyperinflation.

No, I Bonds are not callable. They are like any other Treasury issue, and I am highly confident the terms will carry through to maturity. If the U.S. government defaults on its debt, it would be across the board for all Treasury bonds of all types, which would basically be a financial disaster for all your holdings, including stocks. Again, highly unlikely. The more logical conspiracy theory would be to question if the U.S. would mess with how the inflation rate is calculated.

Excellent article . Very insightful, and this kind of insight will not be found elsewhere .

Thanks Mr. Enna

I could not agree more.

David, I suggest adding a Tips (Paypal) button on your site for those of us who would like to contribute a few bucks to keep it alive and well. I would hate to lose it.

Robert Kessler had a good take on the economy and Treasury Bonds on Wealthtrack on Friday. You think the I bond rate will increase in the next term? Based on your experience you know more than I do. I think it will. Inflation is kinda crazy right now.

For the I Bond rate to increase above 0.0% on Nov. 1, I think we’d need to see the 10-year TIPS real yield rise to at least 0.20%, probably more like 0.30%. That’s an increase of 100+ basis points in less than five months. It probably won’t happen.

Concrete Money, are you asking about the fixed rate on the I bond or the inflation rate on the I bond? seems almost certain that the inflation rate component will exceed the current 3.54% by September’s reading. the most recent CPI-U measurement has already increased 3.26% annualized in the last 2 months since the last I bond rate change.

My question is the 3.54% rate on the I bond going to go up? I’m not a expert on those kind of things.

The next inflation-adjusted rate for the I Bond will be determined by non-seasonally inflation from March to September, basically that number X 2, annualized. Right now, after two reported months, inflation has run at 1.62%, which translates to an annualized rate of 3.24%. So … will it be going up? Probably, but not for certain. Inflation during summer months can be very unpredictable. At some point, it will also probably go down. I Bonds at this point just match the rate of inflation, whatever it is.