By David Enna, Tipswatch.com

This article is the second in a series looking at how my three favorite bond funds — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed after 2013, when the Fed signaled it would back off on bond purchases and eventually raise short-term interest rates.

Why do this? Because we may be heading into a similar scenario in 2022 and beyond, with the Fed tapering off bond purchases and eventually (and gradually) raising short-term interest rates. The performance after 2013 could tell us a lot about what’s ahead.

None of this happened in 2013, but the Federal Reserve issued enough signals that the bond market reacted with a “taper tantrum,” sending both real and nominal yields sharply higher. Read about what happened in 2013 here.

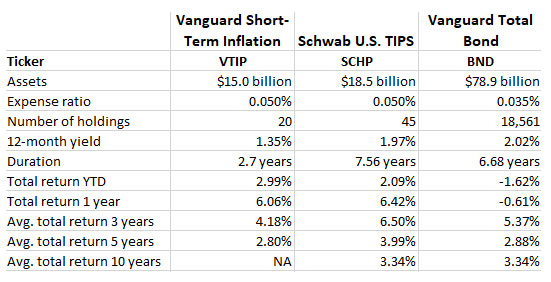

To recap, here are the three bond funds I am tracking; they are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a summary of their basic statistics and performance:

2014: The deck was stacked against TIPS funds

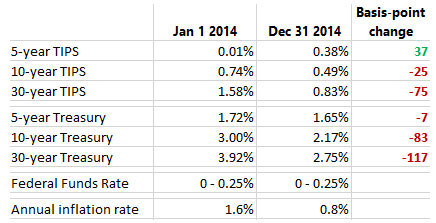

Even though real and nominal interest rates declined in 2014 — reversing the overreaction of 2013 — this wasn’t a good year for TIPS and TIPS funds. Why? Because the yield curve began flattening (with shorter-term yields rising and longer-term yields falling) and inflation slumped to 0.8% year-over-year. Here are the 2014 statistics:

Again, note that the Federal Reserve did not raise interest rates in 2014. But it did taper away from its bond purchases, gradually tightening the money supply. This raised recessionary fears, and longer-term interest rates declined. But there was one exception: Real yields rose for shorter-term TIPS, in reaction to short-term deflationary fears. The annual inflation rate came in at 0.8%, so those fears were justified. TIPS perform best when interest rates decline or stay stable, and inflation rises. The opposite was happening in 2014. The overall TIPS market is heavily skewed toward the shorter-term, with about 20 of 44 total issues maturing in the next five years. This yield flattening trend was not good for a short-term TIPS fund like VTIP, or even a broad-based TIPS fund like SCHP.

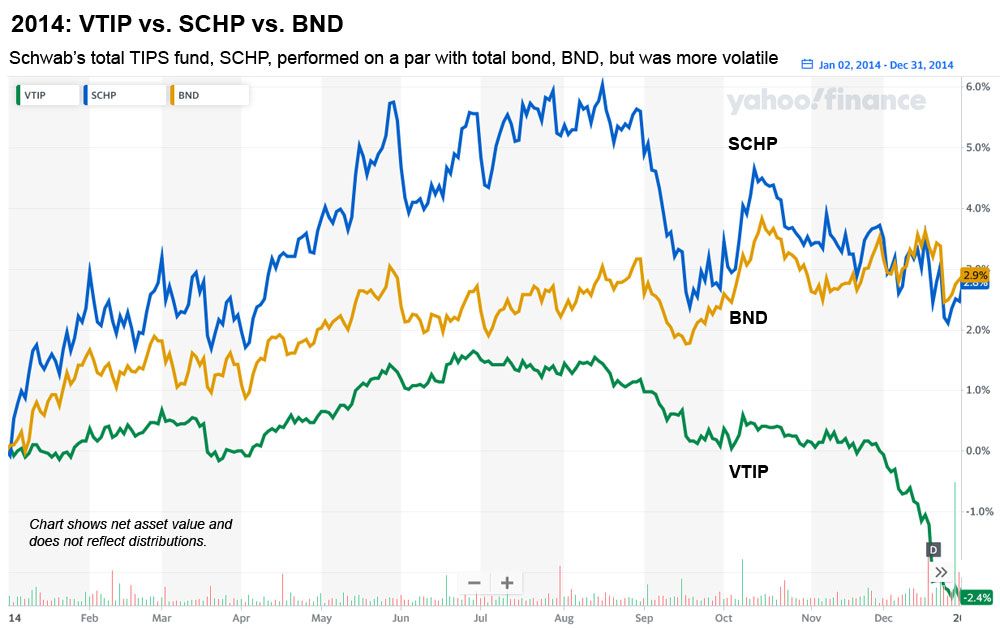

Here is how these funds performed in 2014, with the chart showing changes in net asset value and not reflecting distributions:

The TIPS market took a deep dive beginning in September 2014, an issue I addressed back then in this article. The trigger was the Sept. 17 release of minutes from a July Federal Reserve meeting. In those minutes, the Fed said:

In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions since the inception of the current asset purchase program, the Committee decided to make a further measured reduction in the pace of its asset purchases. …

If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will end its current program of asset purchases at its next meeting.

The Fed, in essence, said it was preparing to end its asset purchases within a few months. Purchases were eventually halted two months later, in October. But the Fed did not change its policy on near-zero short-term interest rates. The first rate increase didn’t come until Dec. 16, 2015.

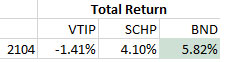

Those Fed meeting minutes halted the rally in longer-term TIPS, and sent shorter-term TIPS yields higher. For the year, VTIP was the worst-performing fund of the three, hit by a combination of higher real yields and very low inflation. BND’s total return out-performed SCHP’s, mainly because the inflation gains for TIPS were too weak to match the higher nominal yields of the overall bond market.

BND was the winner in 2014. SCHP took a volatile course toward a fairly good year. VTIP was the loser.

Conclusion

It’s highly likely that after the Fed acts to halt bond purchases and — eventually — raise short-term interest rates, we will see the yield curve flattening, which will benefit longer-term issues. VTIP could do fine in that scenario, as long as U.S. inflation remains rather high. SCHP would do even better, most likely.

- 2013: A year of surging real and nominal yields

- 2015: The Fed actually did something!

- 2016: Inflation rises; TIPS out-perform the overall bond market

- 2017: ‘The calm before the storm’

- 2018: Did the Federal Reserve go too far?

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hello, basis points change on 5 yr TIPS should be 37 not 39

Thank you for checking behind me! This is now fixed.