Inflation is running at a 40-year high. What does it mean for I Bonds, TIPS and future interest rates?

By David Enna, Tipswatch.com

Once again, U.S. inflation is running higher than expectations, a trend that will probably continue through the early months of 2022.

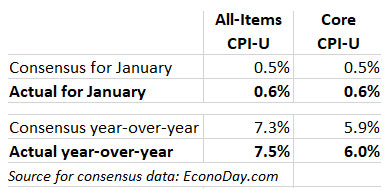

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.6% in January on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 7.5%, the largest 12-month increase in 40 years, since the period ending February 1982.

Both the monthly and year-over-year increases exceeded economist expectations of 0.5% for the month and 7.3% for the year. Core inflation, which removes food and energy, also exceeded expectations, running at 0.6% in January (versus expectations of 0.5%) and 6.0% for the year (versus 5.9%). The year-over-year number for core was the largest 12-month change since the period ending August 1982.

And this jump higher in inflation came despite the fact that gasoline prices actually fell in January, a trend that is likely to reverse in coming months. The BLS noted that a wide range of price increases contributed to January’s surge in inflation. Some highlights:

- Food-at-home prices increased a troubling 1% in the month, and are now up 7.4% over the last year.

- Gasoline prices fell 0.8% for the month, but are up 40% over the last year. This decline is highly likely to reverse in future months, as the price of WTI Crude has increased about 35% in the last two months.

- Shelter costs rose 0.3% for the month, and are up 4.4% over the last year. This is another category where higher prices can be expected into the future.

- Costs of electricity surged 4.2% in the month and are up 10.7% year-over-year.

- Apparel prices, once a sleepy sector in the CPI report, were up 1.1% in January.

- Prices for used cars and trucks continued surging higher, up 1.5% in the month and 40.5% for the year.

- New car prices held stable, but are up 12.2% for the year.

- The medical care index rose 0.7% for the month.

To wrap things up, the BLS said this: “The increase is broad-based, with virtually all component indexes showing increases over the past 12 months.”

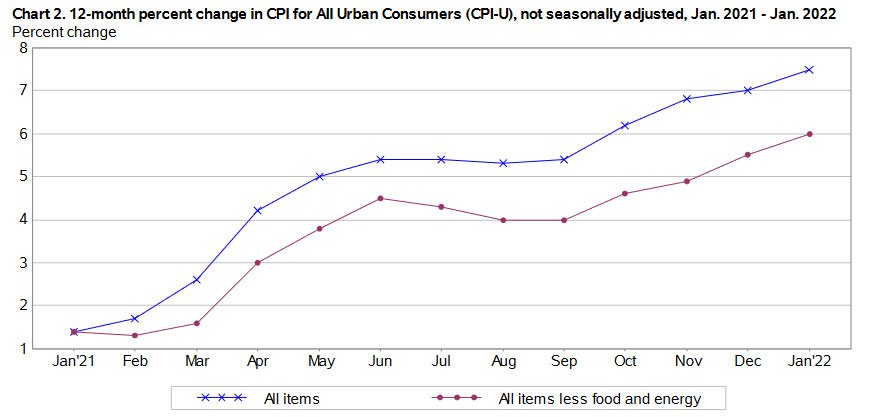

Here is the one-year trend for all-items and core inflation, showing the remarkable climb higher from very low levels of inflation in January 2021:

What this means for TIPS and I Bonds

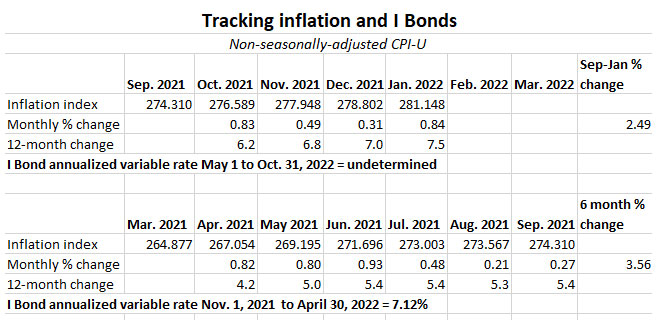

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For January, the BLS set the inflation index at 281.148, an increase of 0.84% over the December number.

For TIPS. The January inflation report means that principal balances for all TIPS will increase 0.84% in March, following an increase of 0.31% in February. For the year ending in March, TIPS principal balances will have increased 7.5%. Here are the March inflation indexes for all TIPS.

For I Bonds. The January inflation report is the fourth in a six-month series that will determine the I Bond’s new inflation-adjusted variable rate, to be reset on May 1 based on non-seasonally adjusted inflation from September 2021 to March 2022. So far, with two months remaining, inflation has increased 2.49%, which would translate to an I Bond variable rate of 4.98%. Two months remain, and that rate is likely to climb higher. Here are the data so far:

What this means for future interest rates

Clearly, interest rates are heading higher. This inflation report continues a string of higher-than-consensus numbers, even though the consensus forecasts have been rising. Already this morning the 10-year Treasury note is trading with a yield of 1.98%, very close to breaking through the 2% barrier, a level we haven’t seen since July 2019. And stock market futures are falling, indicating the markets are again adjusting to a future with higher interest rates.

From this morning’s Wall Street Journal report:

High inflation is the dark side of the unusually strong economy, posing a challenge to the Federal Reserve as it tries to quell rising prices without damping growth.

“This is not encouraging news for the Fed in its battle to get inflation heading back towards the 2% target,” said James Knightley, chief international economist at ING. “Rate hikes will do nothing to resolve supply chain strains and worker shortages, but they can contribute to taking some of the steam out of the economy and allow demand and supply to start moving towards a better balance, at the expense of weaker growth.”

I’m sure the Federal Reserve has a very good idea where prices are heading, and the current trend of 40-year inflationary highs must be addressed. An easy prediction: Expect the Fed to begin raising short-term interest rates in March, and continue raising them through 2022.

What will happen to longer-term rates? That will depend on the economy and the stock market’s reaction to Fed actions. In the next few months, longer-term rates should climb higher, but possibly stabilize if the economy begins sinking or the stock market plummets.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I have about $2,000 worth of EE bonds and $200 worth have matured (owned over 30 years) All have either my Mothers’ or my Fathers’ social security# on them. I read this means the IRS will send them the 1099 to tax the interest. Any ideas how I can change this to my Social security#?

Thanks!

So I am assuming your parents are still alive? Then you cannot cash the EE bonds until the registration is changed. TreasuryDirect says: ” Savings bonds cannot be transferred. If you find a bond that belongs to someone else or buy a bond on an online auction site, you cannot cash it.” So you will need your parents to have the bonds reissued in your name. However: “Reissue will not be made if the request for reissue is received less than one full calendar month before the final maturity date of a bond.”

It’s going to be complex. I think you will need to convert the EE Bonds to electronic form and then have the registration changed. Details: https://www.treasurydirect.gov/indiv/research/indepth/smartexchangeinfo.htm

Lots of good information can be found at https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eereplace.htm#reissue that addresses how, when and under which circumstances (including inheritance) Series EE bonds may be reissued in a new name.

Isn’t there a hidden danger with purchasing TIPS because of the recent run-up in inflation? With the drastic uptick in inflation the corresponding index has gone up dramatically. If the reverse happens that index is going to go down just as dramatically. If the supply chain issues are resolved, it could stay lower indefinetly. Assuming you could purchase TIPS at par at an auction, you could be in for a nasty surprise when it matures. You’ll end-up getting less than you paid for it if the index is lower at that point in time.

I wouldn’t call it a “hidden danger.” TIPS perform better (versus a nominal investment) when inflation is higher than expected. Right now inflation expectations are around 2.5% for a 10-year TIPS. If inflation runs higher than that, the TIPS does better than a regular 10-year Treasury. If inflation runs lower, then the nominal Treasury does better. If inflation continues on at 4% for several years, TIPS are going to do a lot better than nominal Treasurys.

Also, if you purchase a TIPS “at par” you are guaranteed to get no less than the par value back when the TIPS matures. It can’t go down in value. I’m pretty sure no TIPS purchased at auction has ever returned less than par value. However, if you pay a premium price over par, that premium price isn’t guaranteed.

Over the last 50 years, we’ve never had a 10-year period where inflation averaged less than 1.6% a year.

If you owe the IRS money (instead of getting a refund) is there any way to get a paper I bond from them? Only way I can think of is by overpaying, somehow? Probably not worth the trouble/risk.

Use online IRS Direct Pay with form 4868 to overpay $5K plus what you owe if you’re not getting a return. I’ve been doing it for years. Easy process.

Quite a few tutorials online to walk you thru step by step. Here is one:

https://thefinancebuff.com/overpay-taxes-buy-i-bonds-better-than-tips.html

I don’t use this strategy, but a LOT of investors do overpay their federal income taxes — either by over-withholding or through excess estimated tax payments — to try to get the $5,000 in paper I Bonds. It is a very common strategy, totally legit.

Excellent information. Just checked the 10-year Treasury note and it’s above 2% at this moment 😯

As expected, the stock market isn’t liking it too much.

You can only use your federal income tax refund to buy I-bonds. You will need to include Form 8888 with your return to tell the IRS just how much of your refund you want in I-bonds and how you want the bonds registered. Turbo Tax will give you the option to get some of your refund as I-bonds.

I have a question: I had read that you can also use your IRS Tax Refund to purchase I PAPER Bonds up to $5,000 per year (presumably at the same rate). How would you do that? I am using TurboTax and they will likely file electronically. Can you re-direct the refund to I Bonds? Can you include state refund? A huge than you for all your efforts on this.

When TurboTax (downloaded software) asks you whether you’d like to receive your refund by direct deposit or by check, choose direct deposit.

You check a box at the bottom to say you want to split your tax refund and use part of it to buy I Bonds.

From the Treasury Direct website: ” When you file your tax return, include IRS Form 8888. Complete Part 2 to tell the IRS you want to use part (or all) of your refund to purchase paper I bonds. Purchase amounts must be in $50 multiples and you can choose to have any remaining funds delivered to you either by direct deposit or by check. You do not need to open a TreasuryDirect account; just follow the instructions on the form. Once your tax return has been processed by the IRS, your paper savings bonds will be mailed to you.” Full instructions are at: https://www.treasurydirect.gov/indiv/research/faq/faq_irstaxfeature.htm

Great answers, Judy, John and Jim. A state tax refund cannot be used to buy paper I Bonds.