Real yields are rising. Noticed that your TIPS fund or ETF has taken a hit?

By David Enna, Tipswatch.com

Maybe it’s not really an Earth-shattering event, but something significant happened Friday: The real yield on a 30-year Treasury Inflation-Protected Security rose above zero for the first time since May 21, 2021.

At Friday’s market close, the U.S. Treasury estimated the real yield of a full-term 30-year TIPS at 0.06%, up 39 basis points since the beginning of the year. This happened the day after the Treasury revamped the presentation of its Yields Curve site, which sent my head spinning. But Bloomberg’s Current Yields site showed that a 29-year, 6-month TIPS closed Friday with a real yield to maturity of 0.04%, so there you go … confirmation that the entire TIPS yield curve is no longer negative to inflation.

Bloomberg took note of this in a story posted Friday morning, noting the surge in yields after an important jobs report surprised to the upside earlier Friday:

It’s already been a tough start to a year for Treasury investors. U.S. government bonds lost about 2.1% this year through Thursday, according to the Bloomberg U.S. Treasury Total Return Index. The loss is already approaching the full-year decline of 2.3% last year, which was the first annual decline since 2013.

“We have to price in more risk that the Fed goes really aggressively, so we’re seeing most of the pressure on the front end of the curve,” said Michael Cloherty, head of U.S. rates strategy at UBS Securities. “As central banks get tighter that should push up real rates.”

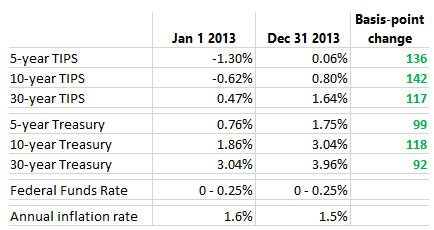

I have been speculating that both real and nominal yields could quickly surge higher as the Federal Reserve approaches actions to raise short-term interest rates and eventually to pare back its massive balance sheet of Treasurys and mortgage-backed securities. It turns out that 2022 is starting to look a lot like 2013, when real and nominal yields burst higher in anticipation of Fed actions:

Note in this chart that annual inflation was running at a muted 1.5% through 2013, which allowed the Federal Reserve to delay tightening. This year, with inflation running at 7.0%, the Fed can’t put off decisive actions, and the market is adjusting quickly to that reality.

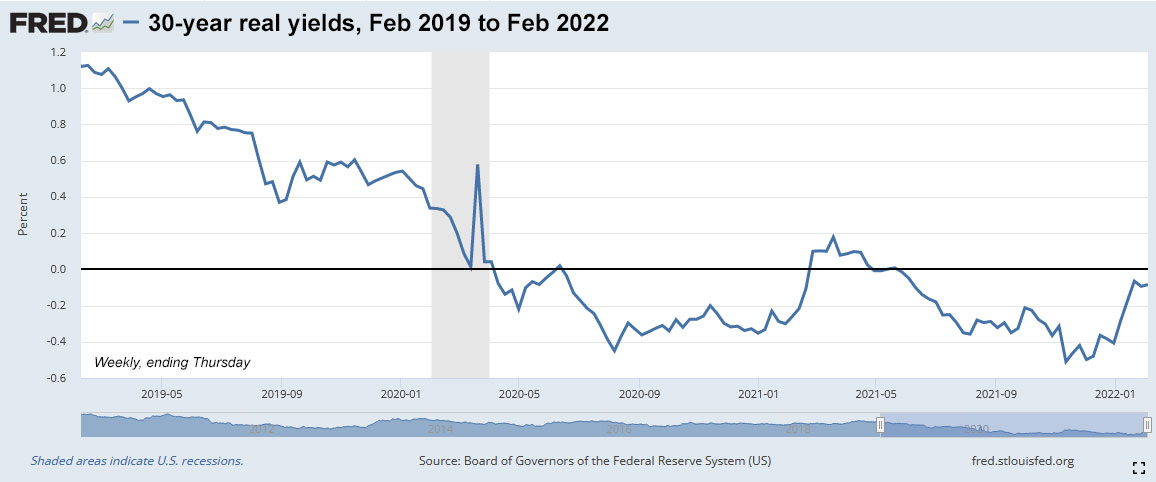

Here is the trend in the 30-year real yield over the last three years:

These three years have been a remarkable era for Fed policy, beginning in 2019 with the tail end of a period of tightening, through a period of moderate interest rate cuts in 2019, to all-out massive stimulus in 2020 and 2021 to calm the market shock that resulted from the pandemic surge in March 2020.

Now we are entering the “next era,” with inflation surging and the Federal Reserve almost certainly ready to raise short-term interest rates multiple times in 2022. Here is how real yields have increased over the last five months:

It’s no surprise that short-term real yields are rising faster than the longer-term yields. Fed actions to raise short-term nominal interest rates will have the greatest effect on the 5-year TIPS because it is the shortest maturity. Eventually, as short-term rates rise, longer-term yields may ease off, flattening or even inverting the yield curve. This happened in late 2018, setting off stock market panic and forcing the Fed to back off on tightening in 2019.

What’s happening to TIPS funds?

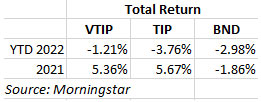

When real yields rise, the value of a TIPS falls. So, obviously, TIPS mutual funds and ETFs have hit a difficult stretch in recent months, but returns have been aided by high inflation accruals over the last year. This is why it is important to analyze TIPS funds based on total return, not net asset value.

The chart compares total returns for Vanguard’s Short-Term TIPS ETF (VTIP), the iShares TIPS ETF (TIP) and Vanguard’s Total Bond Market ETF (BND). Even though shorter-term real yields have been rising faster than longer-term yields, VTIP has outperformed the overall TIPS market and the overall bond market. TIPS funds have the advantage of inflation accruals, and as long as inflation continues running hot, these funds can balance off some of their net-asset-value losses caused by rising interest rates.

But I would still expect TIPS mutual funds and ETFs to have a difficult year in 2022, as interest rates rise. VTIP, with its shorter duration, should perform the best in this scenario, but it could still end up with a negative return for the year. Taking a longer view, higher real and nominal interest rates will be a positive for investors looking to add new money in inflation-protected investments.

Is the I Bond’s fixed rate affected at all?

The U.S. Treasury will reset the fixed rate of the U.S. Series I Savings Bond on May 2. The rate is currently 0.0%, and in my opinion looks very likely to remain at 0.0% through the May reset. The 10-year real yield is currently -0.48% and would need to rise at least 75 basis points in the next three months to make a higher fixed rate at all likely. I don’t see that happening, but you never know.

If real yields surge higher through 2022, it’s possible the fixed rate could rise in November. Still, the current annualized variable rate of 7.12% on I Bonds is too attractive to pass up. I think an investment before May 1 is the wisest course. The next variable rate, also to be reset on May 2, should be at least 4.5%, maybe much higher. Can’t pass up 12 months of very strong returns for the outside chance for a higher fixed rate in the future.

Look back at the Fed’s last tightening cycle

Back in July I did a series of articles looking at how real and nominal yields reacted when the Fed first began discussing tightening in 2013, stopped bond buying in 2014, and eventually began raising interest rates in late 2015. Through most of this period, surprisingly, the stock market did very well. Bond markets took some hits, but eventually recovered.

2013: A year of surging real and nominal yields

2014: The deck was stacked against TIPS funds

2015: The Fed actually did something!

2016: Inflation rises; TIPS out-perform the overall bond market

2017: ‘The calm before the storm’

2018: Did the Federal Reserve go too far?

2019: The Fed cries ‘uncle’; bond investors celebrate

2020: Chaotic year of pandemic fears, stunning stimulus

2021 and beyond: What’s ahead for U.S. financial markets?

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

If you bought a TIPS for 0% real and held it until maturity would that result in the same return as current purchases of I bonds (ignoring taxes) since the fixed rate on I bonds is currently 0%?

That’s a good question. I think it is likely that an I Bond with a 0.0% fixed rate would out-perform a 30-year TIPS with a real yield to maturity of 0.0%. The reason: During a deflationary period, the TIPS will lose value and have to make up ground. The I Bond never loses ground and gets the full benefit of the inflationary bounce higher after the deflationary period. I Bonds, obviously, have other advantages, too: A flexible maturity and tax-deferred interest are two examples.

Is there a way to track short term tips real yields and break even rates? I only seem to be able to find that data for 5+ years

The Treasury’s official real yield estimates for TIPS begin at 5 years, so there isn’t an easy way to get this information.

Vanguard shows a -2.2% current real yield for VTIP with average maturity of 2.5 years. So I believe that implies a breakeven rate of about 3.7% over the next 2.5 years? I bonds seem likely to remain attractive for several more years relative to other savings products.

The current yield numbers presented for TIPS funds can be misleading and Vanguard tends to show the yield in the most negative way possible. For example, the iShares STIP ETF, which has essentially the same portfolio, claims a 30-day SEC yield of 4.93% and a real yield of -1.79%. So it is hard to make a judgement based on that number, and inflation accruals lag two months into the future. At any rate, it is highly likely that VTIP’s yield will lag official U.S. inflation in the near term, and I Bonds will match official inflation for as long as you hold them.

Nice mention of your site in today’s WSJ: https://www.wsj.com/articles/tips-what-investors-should-know-treasury-inflation-protected-securities-11643849892?mod=hp_lista_pos1

Yes, reporter Randall Smith and I had many discussions about TIPS and their complexities.

Good analysis, as usual. But I have never understood why anyone would utilize a bond fund or ETF, except for speculation. Does owning the bonds directly shield you from rising interest rates? Yes, unless you subscribe to Wall Street doubletalk about ” lost opportunity cost.” Cheers

Does owning the bonds directly shield you from rising interest rates? Only if you hold them to maturity! Would you hold your bond to maturity and get less than the market value in a falling interest rate environment? So ETF worked better in a falling rate situation.

I do own VTIP and SCHP in a tax-deferred account, and I understand the risks. Rising real yields could overtake high inflation, and these funds could lose money. These funds could be used for strategic trading (as Don Geo notes in his response), but that’s not my plan. My strategy for individual TIPS is “buy and hold to maturity” and so I focus on the 5- and 10-year maturities.

When you buy TIPS in a tax-deferred brokerage account, you are going to see the “market value,” meaning the price adjusted for current real yields compared to the coupon rate. If you are a buy-and-hold investor, you can just ignore the market fluctuations and focus on the par value plus accrued inflation.

So glad to have found Tipswatch as my wife and I round the corner to retirement. We’re learning quite a bit and feeling better about our options thanks to your work. We are looking closely at 5- and 10-year maturities as you suggested you do.

Regarding your very last comment, you say to just keep an eye “on the par value plus accrued inflation.” Do you have an example or table of finding accrued inflation?

You can find the inflation accruals, which update each day on this page: https://www.wsj.com/market-data/bonds/tips The numbers you see in the right-hand column can be translated to a multiplier by adding a decimal in front of the third numeral. For example, for 1172, the multiplier would be 1.172.

You multiply the original par value of the TIPS you purchased by this multiplier. So if you bought $10,000 of the TIPS that matures July 15 2025, you would multiply $10,000 x 1.172 giving you a current value of $11,720. You can set up an Excel spreadsheet with all your holdings and have original par value in one column, the inflation index in the next column, and the current accrued principal in the last column. When you need to update, just fill in the new inflation indexes.

This isn’t the market value of the TIPS if you sold it today. It is the par value plus accrued principal. If you are holding to maturity, you don’t need to worry about market value.