Core inflation continues at 5.9%, an unsustainable rate.

By David Enna, Tipswatch.com

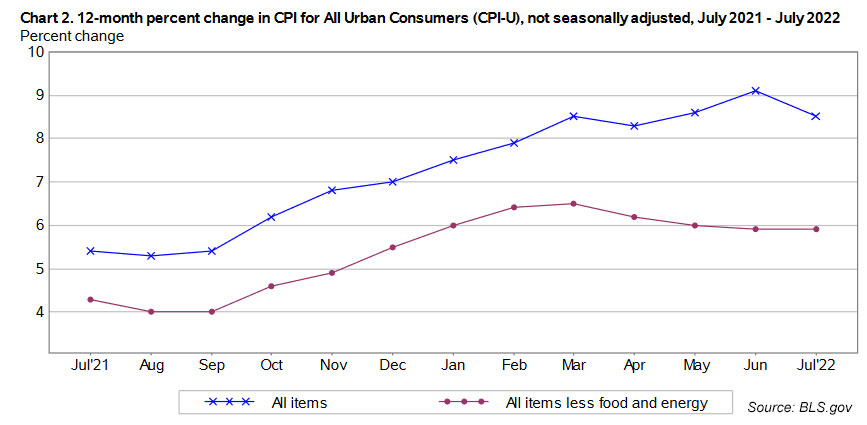

I warned you: Inflation numbers are notoriously fickle in the summer months, and so here we go: All-items U.S. inflation increased 0.0% in July on a seasonally adjusted basis, the Bureau of Labor Statistics reported today. The year-over-year number dipped to 8.5%, down from June’s 41-year-high of 9.1%.

Inflation was expected to dip in July because of a strong drop in gasoline prices, a trend that continues in August. But today’s inflation numbers were well below the consensus estimates of 0.2% for all-items and 8.7% for the annual rate. Core inflation, which removes food and energy, came in at 0.3% for the month and 5.9% for the year, also below consensus estimates.

For American consumers, this is good news. We seem to have finally passed “peak inflation” and prices are heading down. But keep in mind that annual inflation is still running at 8.5%, a dangerously high number.

The BLS noted that gasoline prices fell 7.7% in July, after increasing 11.2% in June, and still remain 44% higher than a year ago. The decline in gas prices helped offset a 1.3% increase in the cost of food at home, now up a painful 13.1% over the last year. June was the seventh consecutive month where food prices increased 0.9% or more.

Other notable trends:

- Shelter costs increased 0.5% in July and are up 5.7% year over year. The rent index rose 0.7% in July. The BLS said shelter costs accounted for about 40% of the increase in core inflation.

- Costs for used cars and trucks dipped 0.4%, but are still up 6.6% over last year’s highly elevated prices.

- Prices for new vehicles increased 0.6% and are up 10.4% for the year.

- The index for natural gas declined in July after sharp recent increases, falling 3.6%. (Let me know when you see your natural gas bill decline in response.)

- The medical care index rose 0.4% in July after rising 0.7% in June, and is now up 5.1% year over year.

- The index for airline fares fell sharply in July, decreasing 7.8%.

So, while overall inflation was down in July, the complete picture remains complex. Gas prices down, food prices up and everything else … mostly up, with core inflation continuing to run at 5.9%. Here is the 12-month trend for all-item and core inflation, showing that while overall inflation seems to have peaked, core inflation appears locked in at around 6.0%:

What this means for TIPS and I Bonds

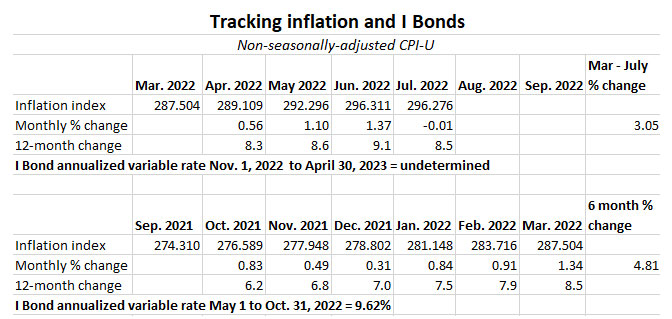

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances of TIPS and set future interest rates for I Bonds. For July, the BLS set the CPI-U index at 296.276, down 0.01% from June’s number of 296.311.

For TIPS. July’s inflation report means that principal balances for all TIPS will decline by 0.01% in September, after rising 1.1% in July and 1.37% in August. Over the year ending in September, TIPS principal balances will have increased 8.5%. Here are the new September Inflation Indexes for all TIPS.

For I Bonds. The July report is the fourth of a six-month string that will determine the I Bond’s new variable rate, which will be reset November 1. As of now, inflation has increased 3.05% in that four-month stretch, which would translate to a variable rate of 6.1%, very attractive but well below the current rate of 9.62%. Two months remain, and a lot can happen in two months. Stay tuned. Here are the numbers so far:

What this means for the Social Security COLA

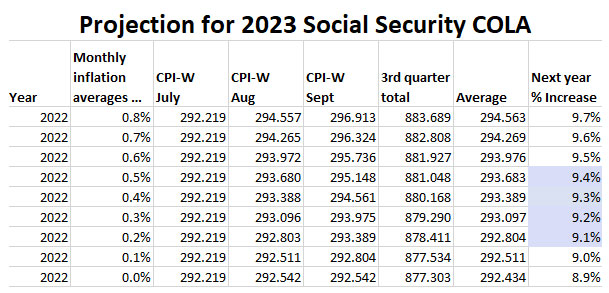

The July inflation report is the first of three — for July to September — that will set the Social Security Administration’s cost of living adjustment for 2023. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For July, the BLS set CPI-W at 292.219, an increase of 9.1% over the last 12 months. However, CPI-W actually fell 0.1% for the month. But remember, it will be the average of July to September inflation indexes — compared to the same three-month average a year ago — that will determine the Social Security COLA. A year ago, that average was 268.421. July’s number was 8.9% higher. If we have zero inflation in August and September, the COLA will be 8.9%

In a recent article, I predicted that the 2023 COLA would get an increase of 9.9% to 10.1%. That could still happen, but the current trend in gas prices should push the number lower. We’ll see. Last year, July inflation ran fairly hot (about 0.5%) but then cooled off in August and September. Here are the historical numbers used in this COLA calculation:

And here is my updated projection for the Social Security COLA in 2023, factoring in the slight deflation in the July index:

What this means for interest rates

The Federal Reserve can’t steer away from its inflation-fighting course, but the July report gives it a little breathing room. It looks like year-over-year inflation has finally peaked. But notoriously volatile gas prices are the primary reason for the dip, and food prices continue to soar. It’s significant that for the first time in many months, inflation came in under consensus estimates. The stock market is happy, with the S&P 500 index already up about 1.6% at 9:35 a.m. EDT.

There should be no “declaring victory.” Inflation remains very close to a four-decade high and cannot continue even at the core rate of 5.9%. Reducing inflation will continue to be Job No. 1 for the Fed. Could we see a 50-basis-point increase in short-term rates in September, instead of 75? I think July’s inflation report made that more possible.

From this morning’s Wall Street Journal report:

Rapidly rising prices have become persistent following a surge in inflation from goods, energy and food, said Greg Daco, chief economist for EY-Parthenon, a consulting firm.

“That divergent trend shows there’s a breadth of inflation in that housing inflation and service-sector inflation remain elevated,” he said, adding price pressures in those areas could linger. “And those tend to be stickier than goods, which can and will start to reverse.” …

“Even if headline inflation slows on account of weaker energy prices but core inflation is stubbornly high, the Fed is likely to maintain its tightening bias as it will be concerned about high inflation being entrenched in consumer price expectations,” said Blerina Uruci, U.S. economist at T. Rowe Price Group Inc.

The inversion in nominal yields continues this morning, with the 26-week Treasury yielding 2.99%, the 2-year at 3.11% and the 10-year at 2.72%. The bond market is predicting economic weakness, which will make the Fed’s job even more difficult.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Video: An economist offers a common-sense look at U.S. inflation | Treasury Inflation-Protected Securities

You mention the calculation for the variable I bond rate but is there such a calculation for the fixed rate of i-bonds? If so do you have any idea if there would be one in Nov?

No, the Treasury does not have an official formula for setting the I Bond’s fixed rate and it gives no guidance. My theory has been that the fixed rate will tend to track higher when the 10-year TIPS yield tracks higher, and now that yield is at 0.81%. So it is possible the real yield could rise on Nov. 1, but I suspect the Treasury will stand pat, because the I Bond variable rate will remain high and demand is very high for I Bonds. I highly recommend buying I Bonds up to the limit before Nov. 1, because that 9.62% variable rate is too strong to pass up. You will be able to get the new fixed rate (if there is one) for January purchases.

I’m new to investing and buying I bonds.

Asking this in 8/22:

If I buy an I bond, by 10/30/22, I get 9.62 % percent for the first 6 months?

Will it then reset on Nov 1 to the newly calculated rate for the next 6 months? (most likely around 6.1 % rate)

Is it true that I must hold it for 5 years to avoid the 3 month loss of interest?

I’ve enjoyed reading your articles, and am attempting to catch on to it all.

Thanks

All of your thoughts look correct. You will get 9.62% for six months, then the new rate for six months (probably more than 6.1%, we’ll see.) You have to hold it one year. If you sell before 5 years you lose the last three months of interest. I’d advise opening a TreasuryDirect account NOW, just in case you run into application snags. Don’t wait until the very last day of October to make the purchase; give yourself a couple days of leeway.

What am I missing here? In the current secondary market, I can buy a TIP with 6 months remaining term at a positive real YTM, OR I could buy a regular Treasury note with the same remaining term at ~3% YTM. Does anybody believe inflation will be less than 3% over the next 6 months? I am betting it will be higher.

Think you hit the right term, your “betting” with TIPs while the Treasury note is a sure thing. What is your best guess on how much more, inflation 5%, so 2% more then Treasure Notes!

I saw this in the WSJ. Does this mean I can buy these under par at the ask price and get the accrued price at maturity?

MATURITY COUPON BID ASKED CHG YIELD* ACCRUED

2023 Jan 15 0.125 99.11 99.13 -5 1.613 1276

2023 Apr 15 0.625 99.22 99.24 -4 1.037 1186

The important thing to remember is that you buy par value at the discount, but on top of that you pay full price for the inflation accrual. So if you want $10,000 of that Jan 2023 TIPS, you would pay about $9,934 for $10,000 of par value, and you would also be buying $2,760 of additional principal, at full cost. You’d be paying about $12,694 for $12,760 of principal. Also, keep in mind that September’s inflation accrual will be slightly negative, and that could also be true for a couple future months if gas prices keep falling.

Txs, At maturity am I only guaranteed to get back PAR on the bond?

Correct.

seems like 9% is the over under number for COLA in ’23 unless a dramatic change happens in the next two months. Even 8% is hefty historically. Love you posting your spreadsheets! helps keep mine straight.

Hi,

In October 2021, I purchased 4 year 10 month TIPS (CUSIP: 91282CDC2). I paid a hevfty premium of 9% approximatly. Wondering, if there is no inflation / deflation to maturity, would I upon maturity get back the par value of 100.00 and the premium or just the par value? Is the premium value ever paid back?

Please ignore the 1/8% interest paid on the TIPS in your calculation.

That auction happened to get the lowest real yield in history for this term, -1.685%, and yes, the adjusted price was about $109.51 for about $100.14 of value, after accrued inflation and interest were added in. The premium you paid above par value is not guaranteed to be returned at maturity, which would happen if we get four years of deflation or very low inflation. On the positive site, this TIPS will have an inflation index of 1.08424 on September 30, so you are close to recapturing the entire premium. You are highly likely to end with a value above your cost.

In my opinion, the 10 YR Treasury note is the best barometer for a 30 year mortgage. Since many homeowners move within 5 to 7 years from their home or refinance to a lower interest rate, the 10 year Fixed mortgage rates and Treasury yields generally move together. As a fixed-rate asset, mortgage-backed securities (MBS) are in direct competition with Treasury instruments for investor money. Slightly off tangent, for every 100 basis points up on the 10 year, property values should fall 10%. Mortgage rates have historically ranged between 1.70% to to 2% above the 10 YT yield. So when the Federal Reserve begins to purchase a ton of 10 year Notes, they in essence manipulate the 30 year mortgage rates making home borrowing less expensive, but inflating the purchase price of a home. When inflation starts to kick in, the primary element of inflation is housing. The primary element is the cost of housing as it represents the largest chunks of inflation. And as a result many home prices across the nation are highly over valued.

Let me know where “shelter” costs have only gone up 5.7% and I’m moving there! My rent is up 25%. As Don noted, inflation going to 0 only means what has happened inflation wise is already baked in. Unless we go to 0 or negative YOY in a month or two, we will have a permanent 8-10% cost of living hit inked in once June is lapped again and the Fed is OK with 2% inflation on top of that….

Great article, but not sure I agree with the new iBond rate being at6%. What are tour thoughts on this article on the same subject?

A Happy Lag

The best news is yet to come. The Treasury’s inflation-rate payments sharply lag contemporary events. The current inflation rate for I Bonds is based on price changes that occurred from October 2021 through March 2022. When the yield on I Bonds is reset, on Nov. 1, that adjustment will include this spring’s price surges, thereby creating a fat payout. Even if inflation were to suddenly disappear, the yield on the I Bond would reset to 6.13%, based solely on the amount of inflation that occurred from this past April though June. Of course, inflation will not abruptly vanish. Almost certainly, the next I Bond yield will also surpass 9%.

https://www.morningstar.com/articles/1108067/run-dont-walk-for-i-bonds

David always gives the I Bond rate as the “already baked in” value without accounting for any inflation/disinflation in the remaining months of the 6-month window. That’s why his value agrees with the 6.13% in your quoted article.

Because inflation is generally slow moving, I prefer to extrapolate the recent months to the future ones as my approximation. And the last four months extrapolate to an annualized inflation of 9.44%, thus that’s my initial “best guess” for the next I Bond rate and similar to your article’s value. This isn’t perfect, of course, and I do try to adjust it for gas prices, which can be followed in real time pretty accurately.

The truth of the matter is that projecting inflation on a month-to-month basis is very difficult.

This summer — like every summer — is throwing a curve ball and this time it is energy prices trending lower. That is going to hold down overall non-seasonally adjusted inflation. My guess right now for the next variable rate is about 7.3%. It’s a guess.

I can’t understand how market interest rates remain so low, while inflation has been above 5% annually for more than a year, and now the core is increasing around 5%. It seems like studious savers are being forced to take risk, to have a chance at any sort of yield.

Americans should be angry at banks and Congress, not fighting each other.

My sense of “common sense” tells me that rates should be higher, heading toward 3.5% on the 5-year and a bit higher on the 10-year nominal Treasurys. I did expect the yield curve to flatten, but now it is inverted at a historically high level.

Thanks for the update. The differences in the CPI print between April 12th & Oct 13th are used to determine Nov’s official I-bond rates. Therefore, I don’t think it is correct to use the price increase from Mar 10th to April 12th when extrapolating for Nov’s rate.

Not sure what you are referring to. The I Bond’s next variable rate will be determined by the official inflation reports for the months of April to October. The March number is just the baseline to determine April’s increase. Non-seasonally adjusted inflation was 0.56% higher in April than it was in March and July’s number was 3.05% higher than the March baseline. When the September inflation report comes out Oct. 13, we can compare the September CPI-U number to the March baseline and then know the I Bond’s new variable rate.

Thanks David. You are correct.

It’s good news that gas is down, but with food being up 1.3% it’s going to be hard for people to notice the savings. With volatile gas prices, who knows what’ll happen. Had gas just stayed the same or only slightly lower, then inflation would’ve been up. There was a 7.7% drop in gas, yet inflation was flat. That tells you something (everything) else is up.

You can see that in the fact that core inflation — which eliminates energy — was up 0.3%. If gas prices stay low, inflation will start to look better. If they surge higher, look out.

Core doesn’t capture food, and the increase in food is what is roughest on my large family.

Another factor to consider is that airline rates (and presumably other things) do have some correlation with fuel/energy prices, so these more variable rates can still make their way into core even at the monthly level. My worry is that the drop in energy cost (including the first part of August) will also effect core enough to get people underestimating future inflation, similar to how the rise may have caused people to overestimate it the last few months.

David, I so appreciate your passion and love for this topic. I learn so much from you. And I’m incredibly grateful for your time, wisdom, and regular commentary on these matters. If IBonds are 6% next month, I’ll have to think hard and long about adding more. I’m getting 6 % on my stocks now, but the market is really expensive. The PE Shiller ratio is sky high; it’s quite the conundrum for me.

Think of I Bonds are part of your “very safe” income asset allocation. Think of stocks as part of your “risky but usually profitable” equity allocation. I buy I Bonds every year, up to the limit, but I am still invested in low-cost stock index funds.

In updating my TIPS spreadsheet, I noticed an odd quirk in Treasury’s index ratio table. Going from 8/31/22 to 9/30/22, my TIPS increase in inflation-adjusted value by 0.032%, rather than the tiny decline expected. Tracking this down, I find that the index ratio does not reach the value corresponding to the new CPI until the 1st of the following month. The increase from 8/31 to 9/1 due to the high June inflation was enough to wipe out the decline from 9/1 to 9/30.

You can see this by comparing the bottom number in the reference CPI column to the month end CPI listed at the bottom of each page of the table. They ought to show October 1 on the bottom of the September table, since they have the data to calculate that index value.

Excellent observation, thanks. Did you actually use my link to the new Inflation Indexes? I include that every month in the inflation article and I wondered if anybody uses it. But having it there makes it easy for me to find when I need it.

I do use your link to the indexes. If you are slow to post, I might get there through Treasury Direct, but using the Tipswatch link is easier.

I think we’re in for a decade or more of financial repression, deeply negative real interest rates. It’s going to suck.

Well, it’s been true for the last two decades and especially the last 12 years. We live in an era of central bank manipulated markets. I hope this current surge in inflation has left behind some lesson.s

Inflation going flat does not mean it goes back to previous highs. At what point does the higher inflation become the norm and these instruments would yield zero?

David, I really appreciate your articles. Always clearly written and very informative. I continue to learn from you daily! Thank you

For TIPS/IBonds the headline is that we had DEflation in July. This highlights one of the underappreciated benefits of I-Bonds–the boost to real returns from deflation. As you note, TIPS “give back” some inflation adjustment, while I-Bonds do not. While this may be fleeting from a monthly perspective inflation volatility over time benefits I-Bonds.

I Bonds have a big deflation advantage over TIPS, that’s true. Plus I Bonds earn tax-deferred interest and have a flexible maturity. In “normal” times, TIPS have a yield advantage, so it somewhat balances out.

Where do mortgage rates go ?

In a past life (25 years ago) I used to write about real estate and mortgages, but today I know little about them. I am assuming the 10-year Treasury note is probably the best barometer for 30-year mortgages. The 10-year has been declining recently and so have mortgage rates. I’d guess the 10 year still has room to move higher, so mortgage rates should also move higher. But that’s a guess.