Fed president James Bullard gave auction investors a gift today.

By David Enna, Tipswatch.com

Investors in today’s Treasury offering of $15 billion in a 10-year TIPS reopening auction should give a tip of the hat to St. Louis Fed president James Bullard, who shook up the bond market (just a bit) with some hawkish rhetoric on interest rates. According to CNBC:

“Thus far, the change in the monetary policy stance appears to have had only limited effects on observed inflation,” Bullard said. “To attain a sufficiently restrictive level, the policy rate will need to be increased further.”

Bullard contended that 5% could serve as the low range for the where the funds rate needs to be and that upper bound could be closer to 7%.

A federal funds rate of 7%? That’s a mighty jump from the current range of 3.75% to 4.00% and seems rather alarmist. But Bullard is continuing the Fed’s unofficial strategy of talking tough whenever the stock and bond markets seem to be getting euphoric. The result: Stock and bond markets yawned and took it mostly in stride, with bond yields inching — but only inching — higher this morning.

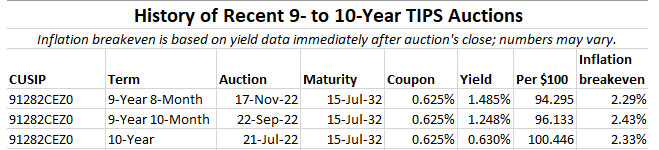

All of this led to the 1 p.m. close of the reopening auction of CUSIP 91282CEZ0, creating a 9-year, 8-month Treasury Inflation-Protected Security. This TIPS, which trades on the secondary market, closed Wednesday with a real yield of 1.37%. But Bullard’s comments appeared to give investors some caution, pushing the auctioned high yield up to 1.485%. The bid-to-cover ratio was a mediocre 2.25, indicating fairly weak demand.

Because the auctioned real yield was much higher than the coupon rate of 0.625%, investors got this TIPS at a discount, with an adjusted price of about $94.29 for about $102.15 of principal, after accrued inflation is added in. This TIPS will have an inflation index of 1.02147 on the settlement date of Nov. 30.

For today’s investors, all is good. The real yield of 1.485% was the highest for any 9- to 10-year TIPS auction since April 2010, when a 9-year, 9-month TIPS got a real yield of 1.709%. For anyone counting, there have been 75 TIPS auctions of this term since April 2010. Today was a milestone.

Real yields have been climbing throughout 2022, a trend that escalated in March once the Federal Reserve committed to increasing interest rates and cutting its balance sheet in the face of 40-year-high U.S. inflation. Here is the year-to-date trend in 10-year real yields:

Inflation breakeven rate

At the auction’s close at 1 p.m. ET, the nominal 10-year Treasury note was yielding 3.77%, giving CUSIP 91282CEZ0 an inflation breakeven rate of 2.29%, the lowest for this term since an auction in July 2021. That’s an attractive rate, in my opinion, making this TIPS a decent bet versus a 10-year Treasury. If inflation averages more then 2.29% over the next 10 years, this TIPS will out-perform. Inflation over the last 10 years, ending in October, has averaged 2.6%.

Here is the year-to-date trend in the 10-year inflation breakeven rate, showing how inflation expectations have been trending downward as the Federal Reserve maintains its hawkish posture:

Reaction to the auction

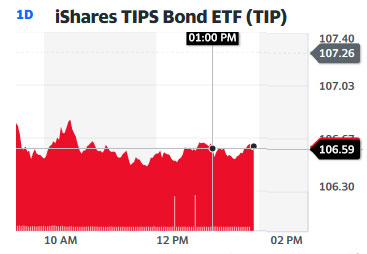

The overall TIPS market had been trading lower all morning, indicating higher yields, as shown in the one-day chart for the TIP ETF, which holds a broad range of maturities. This chart is all about the statements by Fed president James Bullard, and the auction result had almost no effect on TIPS prices.

So, investors at today’s auction got a gift from Bullard, amounting to an 11-basis point increase in real yield over the next 9-years, 8 months. Getting the highest real yield in 12+ years looks like a solid investment.

Today’s auction closes the books on CUSIP 91282CEZ0, a TIPS that transitioned the 10-year market from remnants of the easy money days of 2021 to the tighter policies of 2022. Its coupon rate of 0.625% — which now looks low — was the highest for any TIPS of this term since May 2019. A new 10-year TIPS will be auctioned on Jan. 19, 2023.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: 10-year TIPS reopening auction gets a real yield of 1.395%, 2nd highest in 12 years | Treasury Inflation-Protected Securities

I am new to this blog and find it quite informative. Since the FOMC meeting and Powell’s press conference, equity markets, for now, are buying into Powell’s hawkish stance, and treasuries yield have also crept up from the initial drop. Looking at the real yields, I am convinced of buying my first ever 5 year TIPS next week. I am buying these in my wife’s Rollover IRA. I know guessing longer-term inflation and/or yields is hard, at best. I do checkout some of the Federal reserve webiste or CME futures site to get started on my guess work. How will you assess 10 year TIPS vs. 10 year nominal treauries now?

I’m a buyer of TIPS right now. I’ll be posting a preview of the 5-year auction tomorrow morning.

Looking forward to your preview on the upcoming 5 year TIPS auction.

Hi David,

I’d like to ask the opinion of you and your readers on this question:

Why would I want to own bonds which are nominal instead of inflation-linked?

Here’s why I ask.

My wife and I will retire in the next few years. We’ve saved enough for our retirement. Our goals for the retirement portfolio are standard:

– Have enough money to fund a comfortable-but-moderate lifestyle of goods and services

– Never run out of money. Not even come close to a scare of not having enough.

I’ve been researching a lot about inflation-linked vs. nominal. The more I understand, the more I’ve come to think that for almost all retirees, inflation-linked fixed income is better than nominal.

The reason: inflation can destroy our retirement savings, and inflation-linked bonds like TIPs eliminate this risk.

There are some caveats to the idea of completely eliminating inflation risk. You can argue about whether the CPI basket for TIPs reflects your own personal inflation rate. There are also good arguments about whether your own needs will change and increase as society and technology progress, i.e., to “keep up with society” requires more increase in spending than represented by the PI. I’ve spent time looking into these issues.

But at least as a first-order effect, the inflation-linked fixed income eliminates the inflation risk.

Inflation is a killer for all savers. Why? As we enter into retirement, we won’t be earning money. We have no sources of income which will grow when inflation rises (no pensions, no SS to speak of, no rental income, etc). On the other hand, our expenses will all be increasing with inflation. This mismatch between our stagnant savings and our expenses growing with inflation can become enormous. With an average inflation of 2% p.a. over our retirement, we’re fine… but an overall inflation rate of 4% would massively cut our standard of living. Moreover, inflation rates even higher than that – rates which have occurred in developed economies in our lives – could completely wipe out our savings and leave us with not enough to live. And inflation isn’t constant: the sequence of inflation cycles (e.g., high inflation followed by low inflation) matters a lot and can also hurt us.

The more we’ve come to understand the risk of this mismatch between our stagnating savings and our inflating costs, the more dread we have of inflation… and the more attractive is the full protection offered by TIPs.

I frequently see analyses which use the breakeven inflation rate between TIPs and nominals to determine which is “better” to buy. But to me, that misses the fundamental benefit of TIPs: inflation-linked bonds ** eliminate ** the risk you face from inflation. Maybe after 30 years, it might turn out that it would have been more profitable to have bought nominals. But we don’t have a perfect crystal ball. And more importantly, we’re not trying to trade or arbitrage markets, betting on future inflation rates. Instead, for us the inflation-linked fixed income is insurance: we’re trying to eliminate risk. TIPs offer us the certainty now that our savings won’t be decimated by inflation.

That represents decades worth of peaceful sleep.

Inflation is a skewed risk. If it’s high, it could be very, very high. As retirees living from our savings, that high inflation would kill us. But on the other hand, if it’s low, it’s only going to be a bit low; there’s a limit to how much actual deflation can occur. And even if there’s disinflation, we still wouldn’t suffer with TIPs because our future expenses which we need to fund in retirement – which are why we have a retirement portfolio, after all – would be decreasing in nominal terms, so on a real basis, we would be even. (Plus we even have the possibility of a bonus if disinflation is enough that the TIPs price on redemption hits the floor at 100. I think it’s unlikely, but it’s a nice bonus to have).

Given all this, why aren’t inflation-linked bonds suggested as the main fixed income investment for most retirement portfolios?

I can think of some scenarios where an individual has nominal liabilities which need to be matched. So for those liabilities, then nominal bonds would be more appropriate than inflation-linked securities.

But it seems to me that most future expenses of most retirees are real: our costs will go up with inflation. So why would you ever want to have nominal bonds? Why not have all TIPs in almost all cases?

I’d love to hear the thoughts of you and others.

Thank you very much for your blog. It’s a phenomenal resource with great resources, clear explanations, and insights which are timely, thoughtful, and well-written. I wasn’t sure under which of your posts to leave this comment/question of mine. Feel free to move it to wherever you think is appropriate.

Best wishes,

Matt

Thanks for this thoughtful comment.

Now that TIPS real yields are well above zero, I agree that TIPS make a lot of sense for people nearing or in retirement. Not a way to “get rich” but to preserve capital for future spending. I prefer to mix in some nominal investments, which will do better during times of very low inflation or deflation. (Plus, obviously, for 1-year cash needs.) I tend to focus on inflation protection, and my wife tends to look for attractive nominals (5-year CDs paying 5% would be an example), so we balance each other off. We just went through a decade-plus period when real yields were very low or negative, and inflation was also very low. TIPS were not offering a true real return, especially after taxes. Nominals were often the better investment during that time.

Now we are in a new era, with high inflation, high real yields and relatively low future inflation expectations, meaning that longer-term nominal Treasurys may not be pricing in a realistic yield. So TIPS seem extremely attractive in November 2022. But who knows what the future will bring? TIPS with positive real yields are very safe, very conservative if held to maturity.

Interesting discussion, Matt. I was a little confused by your paragraph beginning “Inflation is a skewed risk;” I think you may have mixed up “deflation” and “disinflation.”

“Inflation” is the rate of change in prices, and particularly a >positive< rate of change, i.e., prices are increasing. If the inflation rate is negative (prices are decreasing), that's "deflation." I think my calculus teacher back in the Pleistocene would call inflation/deflation the first derivative of prices.

"Disinflation" is the (negative) rate of change in inflation: if monthly inflation ran at an average rate of 4.81% for a six-month period, and then at and average rate of 3.24% during the following six-month period, we experienced disinflation. Dr. Pleistocene, rest his soul, would have said that disinflation is the second derivative (the rate of change of the rate of change) of prices. Prices increased, but not as quickly as during the earlier period.

So when you said "there’s a limit to how much actual deflation can occur. And even if there’s disinflation, we still wouldn’t suffer with TIPs because our future expenses . . . would be decreasing in nominal terms, so on a real basis, we would be even," I think you swapped the two terms. The theoretical limit on how much deflation can occur is 100% (asteroid destroys the planet and the are simply no buyers, so the price of everything goes to zero) (but our TIPS will mature at 100, yay!). And if there's disinflation, our expenses are still rising, just not as quickly, and TIPS are still appreciating, since the inflation factor is still increasing, but more slowly.

Interesting points from both David and Woody. Thanks for a good discussion. Several separate points, so I made several responses.

[David:] “I prefer to mix in some nominal investments, which will do better during times of very low inflation or deflation… ”

If the actual inflation rate over the life of the TIPs bond is less than the breakeven when I buy it, then yes: a nominal investment of the same maturity would have done better. But if you buy the nominal bond for that reason, then you’re making an explicit bet that you want to benefit from future inflation which turns out to be lower than the current market expectation. The risk of this bet is that you’ll lose if there is higher inflation.

In contrast, at least as I’ve come to look at it, TIPs **eliminate** the risk of inflation. With TIPs, I no longer care about inflation: my investment earns a known amount in **real terms**. So regardless of what the rate of inflation is – high, medium or low – it doesn’t matter to me because both the principal and return of my investment is fixed and known in real terms.

I understand the argument that my purchase of TIPs – instead of a nominal Treasury – is also an explicit bet. In this argument, I’m betting that inflation will be higher than the market expectation. If I don’t believe inflation will be higher, than I would buy the nominal bonds instead of the TIPs.

However, I’ve come to think that this argument doesn’t accurately reflect the situation of someone in, or near, retirement.

The purpose of our retirement portfolio is to fund our future expenses. Our expenses will be entirely real: they will increase with inflation. So to me, the default perspective when thinking about retirement portfolios should be investments in real terms where your inflation-linked securities match your inflation-linked future expenses. In this way, you don’t have any inflation risk because your assets and your liabilities are matched in real terms.

In contrast, nominal investments are a deviation from this default where you consciously decide to introduce a bet on inflation.

This is the change in mentality that I’ve come to as I study more about TIPs and build out programs to analyze future scenarios with our retirement portfolio (I’m a computer science guy, so I’ve run millions of scenarios by now lol). I’ve come to think that the default for retirements should be real investments rather than nominal. Of course, on a practical basis, I understand that we’re limited by the supply of real inflation-linked investment possibilities which we can invest in. But to the extent possible, the starting point for a retirement portfolio should always be real investments because they match the real future expenses.

You’re (literally) the internet’s decades-long TIPs watcher :-), so I’m very interested how you think of this idea. What am I missing? Why isn’t it more standard in retirement planning to start with real inflation-linked investments as default, and then add in nominal if someone wants to bet on inflation?

[David:] “my wife tends to look for attractive nominals (5-year CDs paying 5% would be an example)”

Assuming you’re talking about CDs from banks, the CDs carry credit risk to the issuing bank. US Treasuries are risk-free exposure to the US government (leaving aside the arguments about the credit risk of the US government; for this discussion, I’m just saying that debt from the US government is risk-free).

So it doesn’t seem accurate to compare bank CDs to US Treasuries.

It’s a pity that there aren’t a wider variety of US-dollar CPI-linked fixed income securities. As far as I know, TIPs (and I-bonds) are the main option. In other countries and currencies, there are inflation-linked fixed income securities from sources other than just the national government. For example, in Canada, there are inflation-linked issues from the regional (provincial) governments. In the UK and Australia, there are inflation-linked issues from agencies and companies. So in these countries and currencies, if you want, you can get an increase in yield by taking on additional credit risk, while still investing in inflation-linked securities.

This would create a good comparison: nominal 5-year CDs from a bank vs. inflation-linked 5-year CDs from the same bank. But as far as I know, this doesn’t exist in the US, so the only comparison is between nominal Treasuries and inflation-linked Treasuries.

(If there are indeed any widely traded US inflation-linked securities other than TIPs/I-bonds, please let me know. It’s not just theoretical; I’d actually love to buy them myself!).

[Woody:] “Inflation is a skewed risk”

You’re right that I wasn’t concrete in explaining this statement. I said it in a hand-wavey way because it can open up a big discussion about money, economics, government policy, demographics, future technology, and more.

But my basic idea is that it’s not an even coin toss for a retiree. And inflation-linked securities eliminate this risk for me so that I don’t need to worry about the risk.

I look at the probability of inflation being higher or lower, and the outcome if that scenario occurs:

Low inflation:

Inflation could turn out to be a bit lower than market expectations. It could be a lot lower. It could be less than zero even.

For many reasons, I think inflation is unlikely to average less than zero over the decades of our retirement. But fortunately, my view on this doesn’t matter when I have inflation-linked securities matching my future expenses.

Even if inflation turns out much lower during our retirement, there is still no problem because our inflation-linked TIPs are funding our inflation-linked expenses: it’s all matched. Of course, with hindsight, it would have been better to have bought nominals instead of TIPs. But that’s an explicit bet which we don’t want to make. With TIPs, we avoid that bet. Even in the “losing” scenario where there is lower inflation, our expenses would also be lower in nominal terms in line with lower inflation. So we’re indifferent.

High inflation:

High inflation has occurred in developed countries in our lifetimes. I don’t want a discussion of whether and how it could occur during our retirement (in fact, it’s exactly because I don’t know and don’t want to worry about it that I think inflation-linked securities should be our default investment). Or of how high it could be: 4%? 6%? >8%…?? But regardless of what probability you assign, higher than expected inflation – and even significantly higher inflation – is a non-zero possibility.

In that scenario of high inflation, then the cost is enormous to us as retirees because we don’t have income which matches the inflation. That’s the reason that if high inflation were to occur, it would significantly harm our retirement. At fairly moderate levels, inflation would cut our standard of living. At higher but still realistic levels, inflation would completely destroy our ability to support ourselves during our retirement and forcing us to rely on family/government/charity.

So, to summarize, how I see the expectations is:

___

Low inflation: non-zero probability; limit is probably floored around zero, but who knows… but even if it occurs and is very low, our expenses would also be lower in nominal terms, so we’re indifferent

High inflation: non-zero probability; the upper limit is very, very high… if it occurs, it’s a disaster for our lives

___

This is what I mean by skewed risk.

What do you think?

Matt : “Assuming you’re talking about CDs from banks, the CDs carry credit risk to the issuing bank. So it doesn’t seem accurate to compare bank CDs to US Treasuries.”

No, I am going to say that FDIC-insured bank CDs are comparable to US Treasurys in safety. If the financial system collapses, both could face some risks, but that is extremely unlikely.

David, I want to echo the sentiments of many others on your site by saying thanks for all of your work. I am in the process of retirement planning and have used your work as a springboard to purchase this TIPS reopen, the most recent 5 yr. TIPS, and I Bonds in October. I plan to construct a TIPS ladder once I get that process figured out.

David, thanks for doing this highly educational commentary. One question on TIPs pricing. When I look at secondary market pricing (on Schwab) similar(same year different month) maturities of 10 TIPs are a handful plus bps higher for the one specific maturity with the much higher original rate (3.75%). Since this is at a premium I understand the principal invested amount is higher, but so what, isn’t that just economically more attractive with a higher YTM and hence a better buy?

I recently answered a question on this TIPS from another reader. This is a unique TIPS (matures April 2032), because it was originally auctioned in 2002 with a coupon rate of 3.375% and so the current price is at a huge premium, at least 14.5%. It also has an inflation accrual of 67%. So to buy $10,000 par of this TIPS you would be paying about $18,600 and getting about $16,700 of accrued principal. But you also get a 3%+ coupon for 10 years, plus future inflation. The price seems fair because right now TIPS with shorter maturities and higher inflation accruals are offering higher yields than a new TIPS of the same term being offered at auction. Investors seem to be shy about picking up large hunks of additional principal, which isn’t protected against deflation.

It would be great to hear your thoughts on individual TIPS on the secondary market from time to time.

That’s a big, constantly shifting target, since there are about 45 TIPS now trading, and prices and yields are constantly in flux. I did mention in the last few articles that I have been looking to fill spots in my TIPS ladder while real yields are high, so I have been looking at TIPS in the 2030 to 2031 maturity range (I filled those spots earlier this week with real yields above 1.5%), and I bought one maturity in 2043 just to get a real yield above 2.0%. I am still focusing this site on TIPS at auctions, since those are predictable events with a deadline, and something everyone can participate in. Nothing wrong with the secondary market, though.

It’s amazing that the entire market consists of only 50 TIPS. Your writing inspired me to watch the secondary market for the past few months and some issues dip below 2% inflation breakeven rate from time to time. There is only one there now, but it would be great to hear when you see a similar opportunity.

Well, the yields on the 5 year TIPS are pretty much where they were before last week’s midterm elections and the latest inflation report. So, it looks like the FED’s jawboning has worked somewhat.

Today, I bought a small amount of the 4/15/27 maturity TIPS with a yield just over 1.8%. We haven’t seen TIPS yields this high since before the 2008 fiasco.

Since I’ve pretty much exhausted all of my liquid IRA funds until next year, this time around I bought them with taxable funds. These yields have even dispelled my fears about the dreaded phantom tax.

I read your missive on the whole phantom tax issue and found it to be your usual thorough and unbiased analysis. But of course, I just fixated on the one thing that you said that suits my purposes.

That was the fact that if you have a CD that re-invests interest you’re going to get a 1099-INT for that interest. That’s pretty much the same situation as getting a 1099-OID for TIPS inflation adjustments.

At my age the only financial goal that I have is principal protection with as little risk involved as possible. About the only thing out there that accomplishes that are TIPS.

Of course, it may well be that nominal Treasuries or even CD’s will lock in a better spread against inflation than TIPS. However, with TIPS yields at 1.5% over inflation, they’re the better deal right now.

Jimbo, I’ll probably look at the December 5-year auction, but I am pretty stocked with 2027 maturities. Same thing with 2023 maturities, so I have a bunch maturing next year. Those are all in a taxable account. It’s great because when they mature, I’ve already paid all the tax. It’s a non-event. But all my new and recent purchases have been in a traditional IRA account, where I can move money around without any immediate tax.

Bullard’s on my Christmas Card list…

David, Thank you! Because of your blog, I have made several purchases for bonds that I had known absolutely nothing about previously, which I am very, very happy with, and which have caused me to feel far more at ease with my retirement possibilities.

I participated in this auction, moving up my planned Jan. 2023 purchase to this re-opening. As you noted in your preview, it is a hard call to make. A very pleasing result! Going in I told myself to not be disappointed with anything above 1.2%, and reminded myself to consider our entire portfolio. After all, the recent down trend in yields (after the Oct. inflation report), was accompanied by a nice increase in stock prices. Watching this bond market in the past year has really highlighted the importance of a broad portfolio in fixed income of different types of instruments. David, another thank you for your site!