By David Enna, Tipswatch.com

It’s almost hard to believe, but this new age of higher interest rates is only about seven months old. A lot has changed in the last year.

Back on Jan. 14, 2022, a 10-year Treasury Inflation-Protected Security had a real yield of -0.66%. In other words, an investor was accepting a return that would trail official U.S. inflation by 0.66% for 10 years. By April 1, that yield had “increased” to -0.41%. By June 1, it was 0.29%. And now, in mid-January 2023, the 10-year TIPS has a real yield of 1.31%, 197 basis points higher than a year ago.

And weirdly, that is a bit disappointing. According to Treasury estimates, the 10-year real yield peaked last year on Oct. 20 at 1.73%. Since then, a series of rather mild inflation reports has the bond market gambling on a Fed pivot, weaker economy and lower mid- to long-term interest rates. So real yields have been sliding lower, bit by bit, in recent weeks.

At the end of last week, we got a little reprieve, following a day of bond market turmoil Thursday triggered by a deflationary December inflation report. As of Friday’s market close, the Treasury was estimating the real yield of a full-term 10-year TIPS at 1.31%, down 22 basis points since the beginning of the year.

All of this points toward Thursday’s Treasury offering of $17 billion in a new 10-year TIPS — CUSIP 91282CGK1. The coupon rate and real yield to maturity will be set by results of the auction, which closes at 1 p.m ET Thursday. This is going to be the first new 10-year TIPS to be auctioned in this new era of higher real yields, and the results will be significant:

- Real yield. If current trends hold (not a sure thing with our current volatility) this TIPS should get a real yield to maturity of about 1.31%. Only two auctions of this term — both late last year — have had a real yield higher than 1% since November 2018, at the very end of the Federal Reserve’s last tightening cycle.

- Coupon rate. A real yield of 1.31% would result in a coupon rate of 1.25%, the highest for any 10-year TIPS since a new issue in January 2011. There have been 72 opening and reopening auctions of this 10-year term since 2011. That is a long time and a lot of auctions. So Thursday’s auction will mark a milestone.

- Inflation index. CUSIP 91282CGK1 will have an inflation index of 0.99948 on the settlement date of Jan. 31. That is because non-seasonally adjusted inflation ran at -0.1% in November. And then … the inflation index will continue to go lower in February, based on -0.31% inflation in December. The big-money investors are going to price this in, trust me. Will that result in a slightly higher real yield than expected? It’s possible.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.31% means an investment in this TIPS will exceed U.S. inflation by 1.31% for 10 years. If inflation averages 2.2%, you’d get a nominal return of 3.51%, on par with a nominal 10-year U.S. Treasury, currently 3.49%. But if inflation averages 4.5%, you’d get a nominal return of 5.81%.

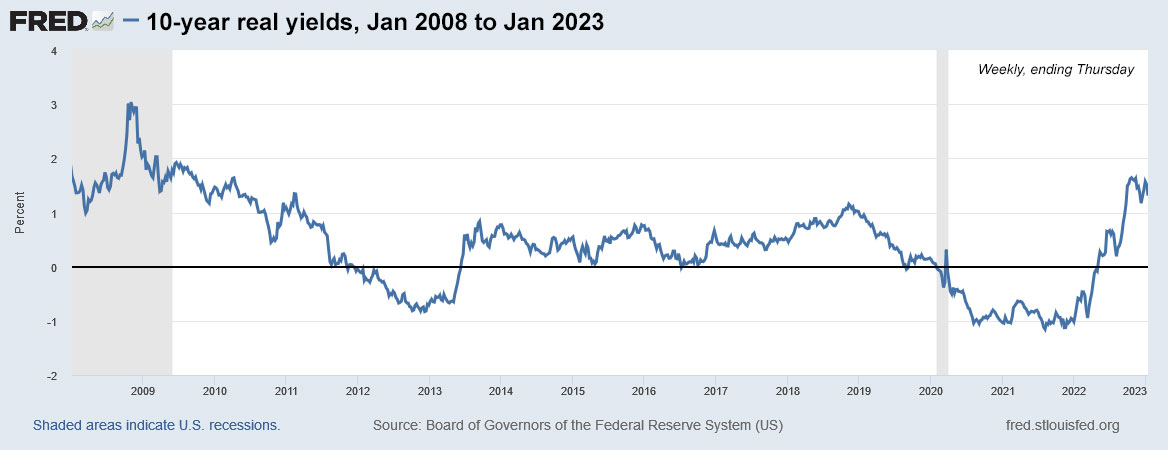

Here is the trend in the 10-year real yield over the last 15 years. I am showing the “big picture” here because this span includes two recessionary periods, which resulted in Federal Reserve intervention and eventually deeply lower real yields. Are we at the brink of another recession? If so, how will the Federal Reserve react? How long can real yields sustain at relatively high levels? Lots of questions:

As this graph shows, today’s real yields remain close to a 14-year high. Yes, real yields have fallen off a bit, but remain attractive, in my opinion.

Pricing

Because this will be a new TIPS with a positive real yield, the auction is going to result in an unadjusted price that is less than $100 for $100 of par value. That is because the Treasury will set the coupon rate at 1/8-percentage-point below the auctioned real yield. As I noted above, a real yield of 1.31% would result in a coupon rate of 1.25%. A real yield of 1.4% would result in a coupon rate of 1.375%.

Plus, because the inflation index will be less than 1.0, the adjusted price should also be slightly below $100, but there will also be a small amount of accrued interest, probably about 5 cents per $100.

Add it all together and an investor might pay about $99.60 for about $100 of par value, but will end up with about $99.95 of actual principal at the settlement date. That’s a rough estimate, and things will change by Thursday. The key thing for investors is that the cost of the par value you purchase should be very close to par value. No surprises.

Want to know more about TIPS pricing? Read this.

Inflation breakeven rate

With a 10-year Treasury note closing Friday at 3.49%, this TIPS would have an inflation breakeven rate of 2.18% if the real yield holds at 1.31%. That seems perfectly reasonable. Inflation over the last 10 years has averaged about 2.6%. I would be more willing to gamble on a 10-year TIPS with a real yield of 1.31% versus a 10-year nominal at 3.49%.

Inflation protection at this point in the cycle isn’t very expensive because the market seems to believe the recent surge in inflation has been tamed. But even if that is so — and I doubt it in the medium-term — projecting future inflation at 2.18% seems like an easy target.

Here is the trend in the 10-year inflation breakeven rate over the last 15 years, showing the surge higher in March 2020 in response to post-Covid stimulus and the gradual move lower beginning in March 2022, as the Fed began to respond to surging inflation:

Final thoughts

I have been targeting this TIPS for purchase for several months because I want to fill a 2033 spot in my TIPS ladder. So I will probably be a buyer, even if real yields decline a bit. But how big a purchase? Should I space out my purchases throughout 2023?

There will be six 10-year TIPS opening and reopening auctions in 2023 — this one in January, and then every other month through November. So investors will have many opportunities. But the key concern is how long real yields can remain at historically high levels. They could certainly go higher, but they certainly could move lower if recession looms.

Let’s look back at January 2019, when the Treasury offered a new 10-year TIPS, CUSIP 9128285W6. At the time, just like now, 10-year real yields had been drifting lower as the auction approached. Using all the wisdom I could muster, I wrote:

“A few months ago, I had targeted this new 10-year TIPS as a purchase, in the hopes of a real yield and coupon rate of at least 1.00%. … Yet, I am committed to adding a 10-year TIPS to my bond ladder sometime during 2019. Hopefully, I can find a higher real yield through the year.”

That January 2019 auction ended up getting a real yield of 0.919% and it was the last “great” auction of 2019, as the Fed began cutting interest rates. I didn’t buy in January and ended up buying no other 10-year TIPS in 2019. Here is how 10-year real yields trended through the rest of that year:

Reality check: I don’t think 2023 is likely follow the pattern of 2019, for several reasons: 1) the Fed is much more committed to holding interest rates at high levels, 2) quantitative tightening will continue throughout the year, and 3) global interest rates are also higher, providing competition to U.S. Treasurys. But toss all that out if the economy moves strongly toward recession.

Conclusion. I will be a buyer Thursday, but I’ll be watching conditions before I make the purchase. That’s my view. If you are considering this TIPS, you can track the Treasury estimates of real yield here, updated daily. Reminder: Anything can happen in the days and hours before a TIPS auction, sometimes good, sometimes bad. The bond market is volatile.

Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting results soon after the auction closes at 1 p.m. ET Thursday.

Here’s a history of 9- to 10-year TIPS auctions going back to 2017, a span that includes the end of the Fed’s last tightening cycle in early 2019. I have highlighted the three auctions with real yields above 1%:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you, David and other readers who help answer questions.

I have been trying to absorb as much as I read to understand this a bit complex investment, TIPS.

If this auction were to yield as projected 1.31% real yield, if we were to go through a deflationary period (not just the change in inflation as negative from period to period), the TIPS yield can go below zero, is that correct? Will this be the reason why some investors do not like to pay the net cost above par value?

If an investor cannot hold a long-term TIPS such as 5 or 10 years, will purchasing short-term TIPS make sense in the secondary market in this high inflation period of time? For example, 9128284H0 trading pricing $99.516 with a Yield to worst of 2.684% (maturity date of 04.15.23). At the inflation, the factor is 1.19906 plus accrued interest of $1.98, this $1,000 purchase will cost $1,195.23. If I use the calculation you have provided (assuming that I am using it correctly), the value of the investment will be $1,201.04. Given the short-term inflation is still high, will this investment make sense compared to a short-term T-bill at $4.58% with a similar maturity date?

Thank you in advance for anyone’s reply and help to educate me.

MW, this new TIPS is going to auction very close to par value and at maturity you are guaranteed to receive par value. If we hit an extended deflationary period, it is true that accrued principal is going to fall and the bi-annual coupon payment will also fall, but it can’t go to zero. As for 9128284H0, you are looking at an extremely short-term TIPS and the real yield you see is pretty much irrelevant. The inflation accrual is -0.1% for January and -0.31% for February. That leaves 1 1/2 months of potential gains from inflation (non-seasonal inflation for January and 1/2 of February). It could very well make sense, but the actual nominal gain on that investment will be in line with short-term Treasurys.

Thank you for your reply.

At what length of maturity will the real yield be relevant? Is there a formula to calculate that? Or, is it because the month-to-month inflation number is negative?

MW, the real yield to maturity is simply a calculation based on how much you paid versus the coupon rate and par value. After the purchase is completed, you are earning inflation accruals plus coupon interest, which also grows (or declines) with inflation. That’s it. So if the price is discounted, the real yield is higher than the coupon rate. If the price is at a premium, the real yield is lower than the coupon rate.

Hi David, a few minutes ago, I noticed the 10-year real yield moved up from 1.31% t0 1.36%. We have one more day to see if the direction holds; what is your threshold to make it a sufficiently convincing buy?

I will make the decision tomorrow. I will be buying, but I may decide to go half now, half later. There’s no right answer. Even if the real yield hangs in above 1.35% on Wednesday, things can change on auction day.

I agree feel the same way.

At 8:10 am Wednesday, 10-year real yield is down to about 1.28% (on secondary market). Early trading, though.

Now it is down to 1.23%. Is there a threshold where it might be better to wait and see or not buy right now? Or do the half and half approach that you mentioned. As you said , things can still change. We would be putting in our buy at schwab, so I think you said it is best to put the order in today or very very early tomorrow (thursday)?

I decided to follow David’s suggestion and buy $5,000 rather than $10,000 tomorrow. I had already placed the $10,000 order at Schwab a few days ago, so I needed to cancel that first. I was unable to cancel the order online (where I had placed it) and it took over half an hour on the phone to get it canceled, followed by about a 15 minute wait for the cancellation request to be approved and processed. So I guess the message is: at least at Schwab, don’t leave a decision to cancel an auction order to the last minute.

I also asked the rep while I was on the phone what the deadline for placing a TIPS order was; he told me it was 11:00 a.m. the day of the auction (later than the 9:30 a.m. cutoff for T-Bills or 10:30 a.m. for T-Notes). Of course, he might be mistaken or the might be a delay in placing the order.

I was able to cancel it on Fidelity online just now. Vanguard doesn’t show the button to cancel it online but I guess I will keep it.

Same here–I decided to cancel my order and split it in half between 91282CGK1 (10-year TIPS) and 912796Z77 (8-week bill), which will mature just in time on 3/21 for the 10-year TIPS re-opening on 3/23. No issues at Fidelity with cancelling a TIPS order online–you click “cancel” and it’s done immediately.

For quite some time now, there is a back and forth going on between the Inflation data + markets vs. the Fed. For example, today’s PPI inflation data declined more than expected and markets liked it, however, then the following:

“St. Louis Fed President James Bullard joined The Journal for a live Q&A, telling Nick Timiraos that the Fed should keep rapidly raising interest rates until it gets above 5%.” and markets came down quick. Two more Fed official are scheduled to speak today. My take for 2023: the Fed will control the narrative to make sure they are convinced to have the Inflation gennie back in the bottle. They do not want to repeat the 70s mistake with coming across stop tightening too early. They will rather be late. From the last FOMC, consensus terminal rate is 5.1%. Ok, what does it has to with with 10-Year TIPS buying….we are not going to know the real yield until after the auction. To feel good about having done my due diligence, whatever worth it may or may not be, I will wait until tomorrow morning…since I have nothing better to do anyway… 🙂 … given the fact that I am not good at typpppping or spellllling, is there a way to turn on spell check on this blog?… if not, no big deal…thanks!!…best

David, what is the best link to track real yields in secondary markets?…thanks!!!

Most likely you all know this, I find this link quite useful: https://www.wsj.com/market-data/bonds

Bloomberg Current Yields, which I have listed on the right side of the desktop version of this site, shows real-time quotes for the most recent Treasurys currently trading. As of 3:45 p.m., the 10-year was at 1.24%. https://www.bloomberg.com/markets/rates-bonds/government-bonds/us. (Normally, you’d expect a full-term 10-year to get a very slightly higher yield, but nothing is normal right now. It’s very hard to judge potential demand for this new TIPS issue.)

Thanks!!!

Your analysis seems sane, and your typing really isn’t that bad.

Here’s my OPINION. The rate of inflation has been slowly declining over the past several months (hardly surprising given the aggressive rate hikes by the FED.) If you think this trend is going to reverse and that inflation will start rising again sometime this year, then wait to make your purchase. If you think inflation is going to continue to drop for the rest of the year or stabilize at some point, them buy now. Frankly, I don’t think anyone can accurately predict future inflation or interest rates over the next year, so if you wait I think there is basically an equal chance for prices of TIPS to go either up or down.

Your two scenarios are very well stated. I believe the Fed will continue to do its job and keep bringing down the inflation barring some black swan event like what happened last year with the Ukraine war or unexpected Supply Chain interruptions post, once in a life time, panademic.

Tomorrow is not only the first 10-year TIPS auction of the new era, it is also (if I am recalling what I read elsewhere correctly) the first day that Treasury will need to begin taking emergency measures to address the debt limit breach. Some pundits are predicting that Congress will deadlock all the way to the exhaustion of the emergency measures in June or July, resulting in a default.

Obviously this site is not the place to debate whether a default will (or should! happen) but I am trying to wrap my head around what will happen to Our Favorite Federal Debt Securities if we start to get close to default or actually see it happen. I assume that a default, if it occurred, would last for a relatively short time, a few weeks or months, and not portend the final collapse of the Treasury and the whole financial system. I’d guess that interest rates on at least some nominal treasuries would move up as the rating agencies started to threaten downgrades, but how would TIPS respond? How would the Fed react? What would this all mean for IBonds? In any event, it seems like we may be doomed to live in interesting times.

It’s very had to say what the effect will be of this artificial crisis. Most likely, as an actual breach nears in June, you could see yields on nominal 4-week and 8-week Treasurys increasing in anticipation. This new 10-year TIPS will have a coupon payment coming on July 15, could that be threatened? In the end, I’d guess, the crisis will be averted (somehow) and all U.S. debt will be paid on time.

From your lips …!!

In times of a crises, even if created by our own congress, usually demand for US Treasuries goes up and yields come down. In short, only time will tell how the debt crises pans out. I have 2-3 hours to decide on placing the order for todays TIPS auction….only if I was a bitsmarter…. 8( … 🙂

From what I’ve heard, if the debt ceiling isn’t raised, the government is likely to start laying off workers and cutting other programs like education, infrastructure, environmental programs, National Parks, the military, Medicare, Social Security, etc before it would actually default on the debt. As long as it continues to make debt payments, I don’t think there would be any effect on your current Treasury holdings if you hold them to maturity. Of course, if it defaults on the debt it would be like any other bond default – you could lose some or all of your money.

I wasn’t thinking so much of actual final permanent default (in which case I suspect the loss of some or all of the money I have invested in Treasury securities would be the least of my worries — there would also be things like collapse of the international monetary order (no more risk-free rate!), floods, pandemics (oh wait, we’ve already got those), cats and dogs living together, and all sorts of other truly dire consequences). I was thinking more of the short-term consequences of a default that got kinda cured after a few weeks or months. Hordes of my fellow geezers pushing their walkers determinedly towards the Capitol to protest the suspension of Medicare and Social Security benefits, increased sales/suspension of reinvestment by the Japanese, Europeans, and Chinese, etc. A sharp drop in market value of Treasury bonds leading to soaring interest rates leading to the Fed cutting rates and going directly to QE5? Real yields going negative again, or jumping to 3-4%, or both within a few months? Who knows? Hopefully, David is right and saner heads will prevail to prevent default before we’re all digging those new trillion-dollar coins out from under our sofa cushions to buy our grande mochas.

I’ve been investing for over 40 years. If there is one thing I’ve learned, it’s that trying to time short term (less than 5 years) swings in the market is the surest way to decrease the overall return on your investments. Occasionally it may work out, but usually it doesn’t. The only exception I would make is that if the stock market declines by 40 to 50% or more, that is usually a good time to buy. Unfortunately, you could lose more money than you gain if you kept your money in cash or bonds while waiting for that decline to occur. And when the decline does occur, people are usually too scared to buy or decide to wait for it to decline further.

Can we predict future inflation? No. Can we predict future real yields? No. The one thing we can predict is that there will be 5 more TIPS auctions of this term through 2023. So, more buying opportunities. I am still buying Thursday to capture a real yield higher than 1%.

Since I’m just starting a TIPS ladder, I am going to use this auction to fill the 2033 slot on my TIPS ladder. I’ll use other auctions later in the year to fill some of the other slots on my ladder.

The TIPS ladder will only be a small part of my overall portfolio (less than 10%). Since I am already retired, I am looking for an investment that will guarantee the buying power of my money (i.e. the value will increase at least as fast as inflation or decrease slower than the rate of deflation.) As far as I can tell, buying TIPS at auction, with a real yield of 0% or higher, and holding them to maturity is the ONLY way to do this. So I plan to buy as long as the real yield is at least 0%. If it is higher than that, that is just icing on the cake.

There’s not much to dislike about a real yield greater than 1%. But I remember way, way back in the day, before this new security was understood by many, getting a real yield of 4.25%. Those were the days!

Oh yes, my best real yield on a TIPS was an issue maturing April 15 2029. The coupon rate is 3.875%. Still holding it, of course. The real yield was 3.899% at purchase.

Good Afternoon David, fellow Charlottean here-and I’m so grateful for you expertise and patience with all of us who are learning about TIPS. My question is regarding building my ladder, specifically covering the 2033-2037 years. I’m looking at funding those years with a single of the 10 year auction on Thursday 1/19/23 (CUSIP 91282CGK1) vs purchasing on the secondary market, (CUSIP 91282CEZ0). My goal is to provide 20k in yearly income- so 100k total purchase. Can you kindly walk me through my best option here?

OK. We are looking at cusp912819PS1 to fill our 4 year slot in the ladder. It’s price is 102.945, YTM 1.610 with an inflation factor of 1.47694 and an inflation adjusted price of 152.43588. The coupon is 2.375%.

1. If we multiply 100 times the inflation factor of 1.47694 it is 147.694. Why is the price 152.43588? Is that accrued interest?

2. Will our coupon pay 2.375 of 100 or of 152.43588?

3. If there is deflation do we risk losing $2.945 (the difference between premium priced par value) or 52.43588 (the difference between the inflation adjusted price and par value)?

Thank you again for your patience.

It’s unfortunate that we have this gap in the TIPS offerings, caused when the Treasury stopped issuing 20-year TIPS. Financial adviser Allan Roth addressed this issue in his Oct 2022 article on building a 30-year TIPS ladder: https://www.advisorperspectives.com/articles/2022/10/24/the-4-rule-just-became-a-whole-lot-easier … His solution …. “Because no TIPS mature between 2033 and 2039, I bought five years’ worth of bonds that mature in 2032 to last until 2036, and four years’ worth of bonds maturing in 2040 knowing they will be short-term in 2037, and later with far less volatility than long-term TIPS. I consider the risk of those few years minimal.” You have an advantage because you now have a 2033 option, as of Thursday’s auction. When Roth was writing this article, I talked with him about it, and I’ll give you the same answer I’ll gave him: “I’m not an expert on this issue. Go for it and let me know how it works out!”

Pamela, you’ve picked one of the most complex TIPS in the entire yield curve for purchase. It is actually 912810PS1. It matures Jan 2017.

This one has some big statistics: 1) an inflation index of 1.47689, meaning you will be buying 47.7% additional principal, and 2) a price right now of about 102.664 for 100 of value, so you are buying that additional principal at a premium price.

So, let’s say you want to buy $10,000 par of this TIPS: 10,000 x 1.47689 = $14,769 principal you are purchasing. The price is 102.664 so … 14,769 x 1.02664 = $15,162 cost of investment, not including any accrued interest. In this scenario, $5,162 is not guaranteed to be returned at maturity, only the par value of $10,000 is guaranteed.

Thank you! Going through an example like that was really helpful.

My question is:

Now that TIPS mutual funds and ETFs have largely taken their interest rate hits, what do you feel about new ETF/MF purchases in 401K accounts that will not allow individual bond purchases? In the near future major interest risk seems less likely than continued inflation risk.

What a terrific site. I look forward to ever new post and save most for reference. Thank you for sharing your expertise.

Just my opinion, but TIPS mutual funds and ETFs seem much less risky now than a year ago, with real yields now near 14-year highs. There is even potential for capital gains if real yields start falling. I had a similar situation until 2019, and my 401k didn’t have TIPS funds at all. Eventually, I was able to convert to a brokerage IRA where I can buy individual TIPS.

We are trying to be sure we understand the potential loss of tips bought at a premium in times of deflation.

How is the principle balance adjusted for inflation. We understand that it is par value times the inflation index….but …how does that index change year to year and how does it account for the years..If it is based just on the cpi from 2 months ago. In your example above the inflation rate decreased .1% so the index would be less than one and your TIP would go down in value by that amount? So if you buy a tip, for example at $104, and the index is .98 then would you tip be worth 104 times .98 (101.92) or 100 times .98? (98) If the index increased to 1.02 the next month would it then be the first number, 101.92 times 1.02 or would it be 100 times 1.02? In other words, if you buy $4 over par value, there would need to be deflation of $4 over time for you to lose that extra inflation adjusted principle?

Conversely, If I buy a TIP for 100 and the index is 1.02 one month, then 1.045 the next month, but 1.03 the following month, is my tip simply worth $103 – its as simple as that? But then over 10 years if inflation was 3% per year how do we get that compounded inflation on the principle balance if the inflation index only reflects the month over month inflation??

Thank you so much – we believe that TIPS will be really important in our retirement portfolio, we just want to be sure we understand them.

If you buy a TIPS at near par value (such as at auction when the real yield is positive to inflation) there is very little risk that you won’t get your full investment back at maturity. The risk enters in more for TIPS on the secondary market with very high inflation accruals, and possibly a premium price (so you buy extra principal at a higher price). On pricing, read my Q&A on TIPS: https://tipswatch.com/why-tips/ …. The inflation accrual changes every single day of the year, based on non-seasonally adjusted inflation two months earlier. It doesn’t matter what you originally paid for the TIPS. Accrued principal is par value x inflation index, all the way to maturity.

Once you purchase TIPS your return is going to be par value + inflation accruals + coupon interest. The coupon interest, paid twice a year, increases (or possibly decreases) every six months as the accrued principal rises (usually) or falls (sometimes) over the six-month period.

The principle at maturity cannot be less than the par value. Corrrect?

That is correct.

Thank you David, your website has been invaluable to us. We have read the pricing Q&A quite a few times😀. So when buying on the secondary market that price can be higher from 1) higher inflation accruals and 2) a premium price due to the market? When looking at the price is there a way to tease out those 2 factors so you know how much extra you are paying for inflation accruals vs premium price?

If the inflation accrual is based on the CPI from 2 months earlier, how is the inflation over the years taken into account. So for a 10 year TIPS you bought in 2018, and that TIPS is now 5 years old , that inflation index somehow takes into account inflation over the past 5 years? How does it do that if it is based on inflation month over month from 2 months before? Thank you for your patience.

Pamela, when you look at a TIPS on the secondary market, and you click through to the details page, you should see a bid/ask “price,” which is expressed as something like $105, or $89.45, or $114.15. That is the price you will pay for $100 of par value. If the price is below $100, is at a discount to par. If it is above $100, it is at a premium to par. These prices reflect how much the coupon rate is above or below the market’s current real yield to maturity for that term.

You can also find the current inflation index, which is sometimes called “inflation factor” on a brokerage site. It is a number like 1.0345, with 1.0 being exactly par value and 1.0345 being 3.45% above par value. Before you actually place the order, the brokerage should show you the price you will pay, or at least a very close estimate.

The inflation indexes build month after month — matching non-seasonal inflation from two months earlier — and after a year will match annual U.S. inflation, always with a 2-month lag. The Treasury has to do this because each month’s inflation report comes out midday through the following month. For example, we just got December’s inflation report, and that was applied to February inflation accruals.

Thank you! So the inflation index is cumulative and individual to each tips? That makes more sense. Thank you.

When deciding whether to buy now or wait for higher rates later, I think this partly depends on where the money to buy the TIPS is coming from. If it is coming from a bond fund, any future increase in the interest rate paid by the individual TIPS you are buying has to be balanced against the decline in value of the bond fund you will be selling. If your money is currently in cash, then you have to consider how much that cash is earning while you are waiting for rates to go up, compared to what it could be earning if you bought the TIPS now.

We would like to do a tips ladder. I think we have waited too long and yields are going down, but it still seems better than an ETF. I like the idea of KNOWING what my return will be and trusting that. The problem is that we would have to sell bond ETF’s to create the ladder and of course they are down right now. Does it make sense? What do you think? Thank you, Pamela

That’s a question for a financial adviser, who could look at the bonds you’d be selling. In a taxable account? Tax deferred? I have been selling out of TIPS ETFs this year to buy individual TIPS, but that is an easier decision, more or less same type of investment.

Well we could do it all in our IRA, and some of the accounts are tips ETF’s , but we will have to look at the other ones, thank you.

One thing to keep in mind is one can swap funds across different types of buckets. For example, I had a CD mature in taxable, so sold the depressed bond fund in trad IRA to free cash for TIPS purchases in trad IRA, and bought the bond fund in taxable. This may or may not make sense for everyone (taxes, etc), but I have found one can sometimes escape selling low by this approach. But, as David noted, best to consult advisor.

This might be a stupid question but can you explain to me what’s the major impact between 1.71% and 1.31% real yield difference will be? Assuming I invest $100k in principle. Thank you.

It would be about $400 a year, growing with future inflation.

Wash Sale Warning: If you are selling a TIPS ETF or TIPS Mutual Fund in a Taxable account on Tuesday (at a loss) and then buying this current offering, some of your loss will be denied by the Wash Sale Rules. Even if you are purchasing this current offering in a IRA account. “According to Revenue Ruling 2008-5, IRA transactions can also trigger the wash-sale rule. When shares are sold in a non-retirement account and substantially identical shares are purchased in an IRA within 30 days, the investor cannot claim tax losses for the sale. Plus, the loss cannot be deferred in the way described above (by increasing the cost basis of the purchase). It’s as if it never occurred.”

This isn’t correct. Purchasing a new TIPS is a substantially different investment than a TIPS mutual fund or ETF and would not trigger the wash sale rule. I’m not a tax expert, but obviously a single TIPS is substantially different than a TIPS fund. By your theory, buying a single stock would trigger the wash sale rule on the sale of a stock ETF. It doesn’t.

My Vanguard statement indicates a loss on my partial sale of VTIP of 1,561.61. Disallowed loss 132.28. Net Loss 1,428.73. I was disappointed with this result. I am hesitant to complain because I can live with the 132.28 disallowed, while being more upset if complain and they then say that even more should be disallowed. Shares were first purchased in 2020, FIFO basis. “The shares in this lot are adjusted by a wash sale.” “Covered shares – shares for which Vanguard has cost basis and is required to report this information to the IRS.”

Could this possibly be because of a dividend reinvestment in VTIP? Seems likely.

Could be. I will just try to time my sales in the future to avoid any wash sale issues. Thank you for all of the info that you provide. I’m glad that I invested in the Unicorn offering in October. I plan on holding those 5 year bonds until they expire.