Annual U.S. inflation fell to 5.0% in March, but core inflation rose to 5.6%.

By David Enna, Tipswatch.com

Update, April 28, 2023: Treasury raises I Bond’s fixed rate to 0.9%; new composite rate is 4.30%

The just-released U.S. inflation report for March sets the new inflation-adjusted rate for U.S. Series I Savings Bonds at 3.38%, down substantially from the current 6.48%.

The inflation-adjusted rate, often called the I Bond’s variable rate, is based on non-seasonally adjusted inflation from October 2022 to March 2023, which ran at 1.69%. That number is doubled to create the annualized variable rate of 3.38%. Here are the numbers:

This new variable rate will be combined with a fixed rate (also to be reset May 1) to create the I Bond’s new composite rate for purchases from May through October 2023. The variable rate eventually will be applied to all I Bonds for six months, but the launch date depends on the month of the original purchase.

What does this mean for I Bond investors?

My immediate thinking is that this lower variable rate skews the equation toward making an I Bond purchase in April, to capture the current composite rate of 6.89% for a full six months, before transitioning to a 3.79% composite rate for the next six months.

The one unknown is: Will the Treasury raise the I Bond’s fixed rate on May 1? It’s definitely possible. I have been speculating that the fixed rate will end up in a range of 0.4% to 0.6% at the reset. No one knows. I will be writing more about this later this week.

Another consideration: Investors looking for short-term yield may want to skip buying I Bonds at this point. I Bonds purchased before May 1 will offer an annual compounded return of about 5.4%, which is very attractive. But redeeming before 5 years incurs a three-month interest penalty. That drops the annual return to about 4.4%, slightly less than a 1-year Treasury bill at 4.7%.

Does this fall in the variable rate mean I Bonds are no longer an attractive investment? Absolutely not, but it does probably mark the end of the explosively high demand for I Bonds, caused by successive variable rates of 7.12%, 9.62% and 6.48%. Back to reality: I Bonds should be viewed as an ultra-safe investment that will track or exceed U.S. inflation for as long as you hold them.

As I noted, I will be writing more about this later this week.

The March inflation report

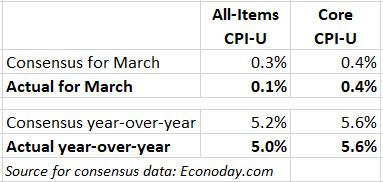

The Consumer Price Index for All Urban Consumers rose 0.1% in March on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 5.0%. Both of those numbers were below consensus estimates, and the year-over-year increase of 5.0% was the smallest since the period ending May 2021.

Core inflation, however, matched expectations with an increase of 0.4% in March and 5.6% year over year. So this inflation report was a mixed bag.

A key factor in moderating all-items inflation was a 4.6% decrease in the price of gasoline, now down 17.4% year over year. On the other side of the equation, shelter costs were up 0.6% and rose 8.2% over the last year. More numbers:

- The costs of food at home fell 0.3% for the month, a welcome break after months of raging price increases. It was the first decline in that index since September 2020. Food at home costs are now up 8.4% year over year.

- The medical care index fell 0.5% for the month and was up only 1% year over year.

- Costs of used cars and trucks fell 0.9% and are down 11.2% year over year.

- New vehicle costs rose 0.4% and are up 6.1% for the year.

- Apparel costs rose 0.3% and are up 3.3% for the year.

I’d say this was a fairly positive inflation report, given that shelter costs are a lagging indicator and should be declining in future months. But gasoline costs are notoriously volatile, so we can’t expect that downward trend to continue.

Here is the one-year trend for all-items and core inflation, showing that while overall inflation has been declining, core inflation remains stubbornly above 5.5%. The March report marks the first time in over two years that core inflation came in above all-items.

What this means for TIPS

Investors in Treasury Inflation-Protected Securities are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS. For March, the BLS set the inflation index at 301.836, an increase of 0.33% for the month. This means that principal balances for all TIPS will increase 0.33% in May, following a 0.56% increase in April.

For the year ending in May, TIPS principal balances will have increased 5.0%. Here are the new May Inflation Indexes for all TIPS.

What this means for future interest rates

Today’s report sends mixed messages. The Federal Reserve can certainly celebrate a dramatic fall in annual all-items inflation, from 6.0% in February to 5.0% in March. But core inflation — considered a more accurate measure — actually rose in March, from 5.5% to 5.6%.

Will the Federal Reserve view this March inflation report as the “positive news” it needs to call a halt to future increases in the federal funds rate? I doubt it. I think we have at least one more 25-basis-point rate increase to go, which would put the short-term rate in the range of 5.0% to 5.25%, finally slightly above the annual U.S. inflation rate.

From this morning’s Bloomberg report:

“May should still tilt to a hike,” said Derek Tang, an economist at LH Meyer/Monetary Policy Analytics in Washington. “But it does take some of the wind out of whether another hike in June will be needed at all.”

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’ve listened to the arguments against buying more I Bonds now and they haven’t dissuaded me from making purchases next week. I think recency bias regarding the 9.62% high water mark may have something to do with the negative sentiment. From a historical perspective, it’s a great time to buy I Bonds.

– The current 6.48% annualized inflation rate is the third highest I Bond variable yield ever.

– The current 0.4% fixed rate is the third highest I Bond fixed rate since November 2008 (and the two higher ones were just 0.1% higher at 0.5%).

– Even the next 3.38% annualized inflation rate is the fifth highest I Bond variable yield since May 2011.

– The 6.89% annualized composite rate for the next six months is 1.894% better than the most recent 26-Week T-Bill which came in at 4.996% annualized. But you can’t buy that one now. You have to wait for the next one which could be higher but might be lower.

– As David writes, ‘the I Bonds purchased before May 1 will offer an annual return of 5.34%, which is very attractive.” The last 52-Week T-Bill rate auctioned off at 4.617%.

– I Bonds do have the 3 month penalty before five years, as David points out, but the interest is federal tax deferred so you have the option of holding for as long as you want, unlike a T-Bill which is immediately taxable after its fixed term.

– I Bond interest compounds every 6 months. T-Bills are bought at a discount and mature at par. There is no compounding effect. To get compounding interest in a Treasury with the best rate, you’d have to buy a 2-Year T-Note which last auctioned at a much lower 3.875.

Sorry so long but one last point. October 12 will be a key date for I Bond sellers. If inflation continues its downward trend, that’s when we’ll know for sure if the November rate will be even lower than 3.38% annualized. A rate lower than that, for me, would trigger the redemption of many of my 0% fixed rate I Bonds three months after that rate applies. The ones I will buy next week will be a good long term hold.

I’m posting an analysis tomorrow morning and I came to the same conclusion. This is, of course, a personal decision. But I want I Bonds with a fixed rate above 0.0% and so I am a buyer, and I want to lock in 6.89% for six months, so I am buying in April.

The six month Treasury bill investment rate on April 10 was 4.996%. So purchasers of I-bonds for the short-term should probably be out of the picture.

I am no longer accumulating I-bonds. The average federal funds rate since 1954 is 4.6%, with great annual variations. Those recent insane near zero rates should not be seen again. The Fed has learned its lesson, I hope. My guess is fed funds will not likely go below 3 or 4 percent for a prolonged period. This view is contrary to the markets who are hoping and hoping for federal funds rates to go back to 1 or 2 percent.

If the fixed rate on I-bonds gets up to 2.0% or so (last seen twenty years ago), I might get interested in buying them again. I am not counting on that. The $10,000 annual limit also makes I-bonds less interesting to me. Twenty years ago you could buy $30,000 in a year.

Black swan events will likely change my strategy, of course.

Mr. Enna -congratulations on your estimate of .30% – which turned out to be the exact unadjusted percent change. Excellent work – as usual.

Actually, I predicted 0.4% and the unadjusted was 0.33%. Fallible, as always

I know you’re going to address “whether to buy now or wait for I bonds” later this week. Looking at how 10Y TIPS is near 1.10, the 0.4-0.6 estimate for I bonds means that it would take 10+ years to break even. So I’m going to buy before the reset.

On the other hand, I would like to hear your thoughts on EE bonds (giving it a thought as mostly liquid 20yr HYSA – because the current 5% rate environment won’t last more than 2-5 years – possibly even shorter).

Right now the EE are at 2.10%. With 20yr money double gimmick, they will yield ~3.5% if held for 20 years. The 20yr bonds are near 3.75%. Surely, treasury will have to make changes to keep EE competitive, right ? And they can’t go beyond 3.5. So do you see them both increase the rates and reduce the duration from 20yr to double ? What do you think will happen to EE around resets ? No rush for the answer – it would be great if you can touch this in your I-bond rate reset article as well.

EE Bonds remain a “reasonable” investment for people willing to hold for 20 years, and the current fixed rate of 2.1% makes that less painful. Will the Treasury change the EE terms? It’s possible the fixed rate will rise, a bit, but I don’t think you will see the 20-year holding period change. (But the Treasury does odd things.)

David if you have time please comment on the 5 year tips that will be auctioned on April 20.

I will be writing a preview article on that auction to publish on Sunday, April 16. As of today it looks like the real yield would be around 1.16%. I expect to be a buyer, unless things change.

Oil is up $13/bbl since the reporting period in this report ended. Core YoY and MoM were same or higher. The rate of increase has slowed but not gone. I might hold but I sure like the flexibility of buying treasuries and not being penalized and locked for 5 years. Tough call.

I am redeeming all zero fixed rate bonds purchased in 2021 and 2022, including gifts bought in 2022 and to be presented this year. I’ll wait for each bond to reach 16 months and cash out a great run with among the top rates in I Bond history.

Remember to redeem at the beginning of month as interest accrual occurs on day 1. Redeeming on May 1, for example, will include all of the interest for that entire month.

To buy or not to buy? That is the question.

Here are the breakeven dates for I Bonds bought in May (at the new 3.8% variable rate and different fixed rates) vs. I Bonds bought this month (at the current 6.48% variable rate and 0.4% fixed rate).

0.4% — Breakeven: Never

0.5% — Breakeven: April 2040 (16 years 11 months)

0.6% — Breakeven: May 2032 (9 years)

0.7% — Breakeven: June 2029 (6 years 1 month)

0.8% — Breakeven: October 2027 (4 years 5 months)

0.9% — Breakeven: January 2027 (3 years 8 months)

1.0% — Breakeven: May 2026 (3 years)

This is very helpful, but the new variable inflation rate is 3.38%, not 3.8%. Was that a typo or do you have to redo the breakevens?

Sorry, that was a typo. The calcs are based on the new 3.38% variable rate.

Thanks for the clarification. Your chart is super helpful. I can’t imagine the fixed rate doubling so that tips the scale to buy now rather than after May 1. In my view, the break even has to be less than the five year no penalty mark to justify holding off.

I learned from doing this exercise last year that it is not a *simple* math problem because the higher fixed rate generates higher interest payments over time with compounding and the effect of inflation. If I buy in April at 0.4% and the fixed rate rises in May to 0.8%, I’d definitely look at gift-boxing another set for the future.

The Excel formula I used to calculate the breakeven dates takes into account the semiannual compounding.

I, along with many others, bought into I Bonds recently when the rate hit 7.12% in November 2021 and we’ve held them through the 9.68% and 6.48% rate changes. For these owners, what is the interest rate hit if we sell 3 months into the new 3.38% rate?

Without compounding, (.5*7.12 + .5*9.68 + .5*6.48) / (21/12) = 6.65 annualized

With compounding, ~7% annualized over the 21 months

Sorry, meant “average annual rate”, not annualized rate

“For March, the BLS set the inflation index at 301.836, an increase of 0.33% for the month. This means that principal balances for all TIPS will increase 0.33% in May, following a 0.56% increase in April.

For the year ending in May, TIPS principal balances will have increased 5.0%. Here are the new May Inflation Indexes for all TIPS.”

In the last paragraph, is that the final principle at maturity? I guess I am a little confused between the 0.33% and the 5.0% increase in principle. Thanks.

The 0.33% is the inflation accrual for the one month of May. The 5.0% is the one-year increase in accrual at the end of May.

So in order for me to calculate the adjusted principle on 4/15/23, I would need to add up the previous six months’ accruals? I bought the 5-Yr TIPS with the issue date of 10/15/22 and paying coupon on 4/15/23. Thanks.

Easier than that: grab the TIPS sheet of index ratios that applies from the TreasuryDirect.gov website and look up your TIPS (91282CEJ6, right?) and the date of interest and you can directly read the index ratio to multiply by your par value. In this case, if I have the right CUSIP, the index ratio is 1.06235 and your adjusted principle would be $106.235 per hundred of par value. https://treasurydirect.gov/instit/annceresult/tipscpi/2023/CPI_20230314.pdf

David, do I have that right?

Sorry, I looked up 4/15/22 rather than 10/15/22. So I thik your TIPS is 91282CFR7. Find it on the same PDF sheet. 1.01256 index ratio.

That is CUSIP 91282CFR7. Here is the link to all the inflation indexes for May: https://www.treasurydirect.gov/instit/annceresult/tipscpi/2023/CPI_20230412.pdf … You can find that CUSIP in that list. On May 1 the inflation index will be 1.01557. The index for April 15 is1.01256.

Thanks, David and Paul,

I guess I am trying to relate the index ratio to an inflationary increase. Is the 1.01256, a six-month inflationary increase?

Max, when you buy an I Bond, the par value is aligned to an inflation index of 1.0000. It doesn’t matter if you paid a premium or discounted price. The index is 1.0000. So, if you bought $10,000 par of that TIPS its inflation-adjusted principal is now $10,125.60. This number changes every day of the month because the Treasury sets an inflation index for every day of the month.

I’ll probably switch to 3 month Tbills.

Redeeming my August 2021 and February 2022 I-Bonds and purchasing a 9-month or 1-year CD paying 4.9% interest would result in a 7-month break-even point for the 3 months of lost 3.38%

I-Bond interest.

I would be waiting to redeem these on November 1, 2023.

I don’t know how about calculating this, but would you need to factor taxes into the equation with CDs?

I plan to buy my annual allotment by the end of April again. Considering the 3-month interest penalty, is there any strategic difference between buying one $10,000 I Bond vs. two $5,000 bonds in the same calendar month?

Last year I bought five $2,000 bonds in late April. My thinking at the time was that if I later needed to redeem a portion early, I could redeem one or two of the five bonds and leave the rest untouched. However, I’ve since learned that TreasuryDirect allows partial redemptions. It looks like the interest penalty on partial redemptions is proportional to the value of the bond? I’m certainly avoiding any early redemptions with current variable rates still high, but just thinking ahead to the future.

Thanks for being my go-to resource on bonds and inflation protection.

I don’t think there is any difference in buying one $10,000 I Bond or 2 $5,000 I Bonds, if the purchases occur in the same month.

“… is there any strategic difference between buying one $10,000 I Bond vs. two $5,000 bonds in the same calendar month?”

Pretty much none whatsoever. One $10k or 2 $5k bought in the same calendar month are functionally the same thing.

There is one potentially significant difference that hasn’t been mentioned in the responses thus far. You can have two different beneficiaries (POD) if you split the one $10K purchase into two $5K purchases. I have two children and so I sometimes split the POD registration of I Bonds and T-Bills for this reason.

Excellent point, thanks.

Thanks for the quick rate update. The two other things you have to keep in mind with I-bond purchases are:

– (lack of) liquidity: if you’re fixed income is essentially “cash” until equity valuations are more favorable, a treasury money market or short-term treasury (on secondary market) may be more suitable given the current 4.5-4.8% yields and ability to convert to equities same-day, as opposed to the 1yr I-bond lockup

– deferred taxability: if you are currently in 24% marginal bracket and going to retire or be out of work in the year when you plan to cash out the I-bonds, it will increase the net yield relative to treasuries (which must have interest realized this year, e.g. via “phantom income”)

Assuming the new fixed rate @ 0.62%, the new composite rate will hover around 4%. Not too shabby considering the opportunity to defer federal taxes and skipping state taxes. Worthwhile to buy in May.

Even better, buy in April and capture the current 6.84% first.

If you buy in April, you would not be capturing the new fixed rate.

True, but at the moment the new fixed rate is anybody’s guess whereas the details for the April purchase require no guesswork.

David expects the new fixed rate between 0.4-0.6, why do you expect it to be 0.62? Are there any calculations/knowledge that you can share behind this number? Thanks.

No insight or formula. Just a conservative guess. To the best of my recollection, David had 0.80% as a fixed rate in one of his write-up. Since then, because of the SVB debacle, I trimmed my fixed rate guess to 0.62%. I like to think in terms of 1/8th increment 🙂.

I believe that the fixed rate is always rounded to the nearest 0.10%.

Thanks. I was not aware of this fact. Still, I just like to work with the fractions. Whether it is 0.6 or 0.62, close enough for approximation as long as you’re not working with really large numbers

Still better than the 0.01% interest rate I’m getting at my brick-and-mortar bank. I think I’ll keep buying I Bonds (AND EE Bonds if the interest rate remains respectable).

Try Fidelity. Their MM paying over 4%.

Same as Vanguard, money market funds at 4.7% currently, FDIC insured cash deposits at 3.8%, lots of options. Several banks have decent savings accounts, i get 3.65% at Ally currently for savings account and 0.25% for checking. but keeping cash not needed for >2months in the Vanguard MM account (which is my settlement fund anyways).